As the crypto market continues its decline, with BTC and ETH once falling near $60,000 and $1,500 respectively, both Strategy and Bitmine are facing floating losses exceeding tens of billions of dollars. At the end of May, Strategy sold 32 BTC, breaking its long-held narrative of not selling coins, putting the 'raise funds to buy coins' model into a stress test phase.

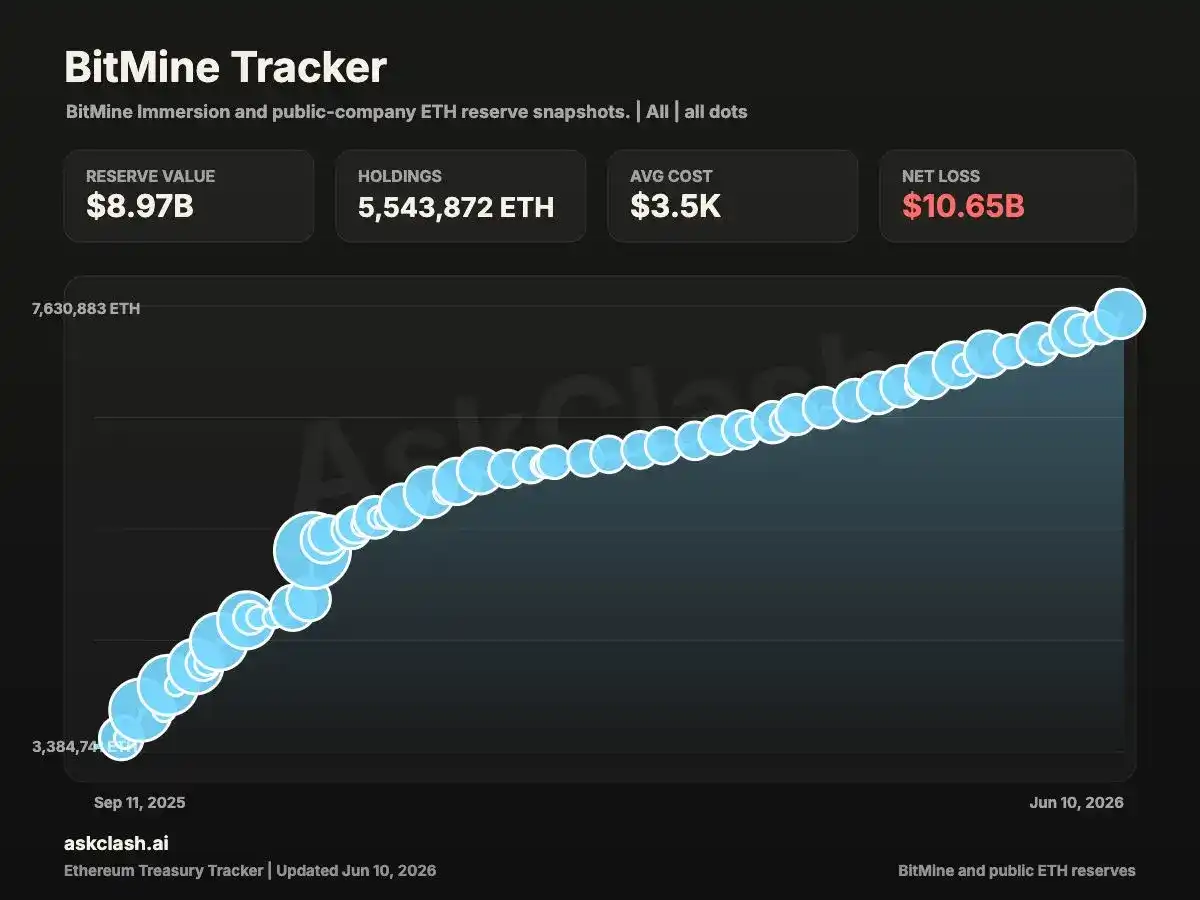

Against this backdrop, Bitmine has high-profile announced the issuance of Series A Perpetual Preferred Stock with a 9.5% annual yield, raising approximately $274 million net proceeds. As of press time, Bitmine purchased 127,000 ETH last week and accumulated a purchase of 125,000 ETH over the past 3 days. Its total holdings currently stand at about 5.66 million ETH, less than 400,000 ETH away from its 5% target.

As the most persistent and aggressive marginal buyer of ETH in the current market, Bitmine continues to add to its positions despite floating losses in the tens of billions. Now, even it needs to rely on preferred stock to replenish its funding flywheel. Once changes occur in the financing market, forcing this hoarding machine to slow down, who will be left to support Ethereum's price?

Buying 5% Before Year-End, Then What?

Bitmine began accumulating ETH in the second half of last year, planning to complete its "5% Alchemy" within 5 years. Data shows that between July 2025 and June 2026, Bitmine raised $19.2 billion through 50 equity offerings, with all funds used to purchase ETH.

As of press time, Bitmine's Ethereum holdings have reached approximately 5.66 million, less than 400,000 away from the 5% target, achieving over 90% of the planned progress in about a year.

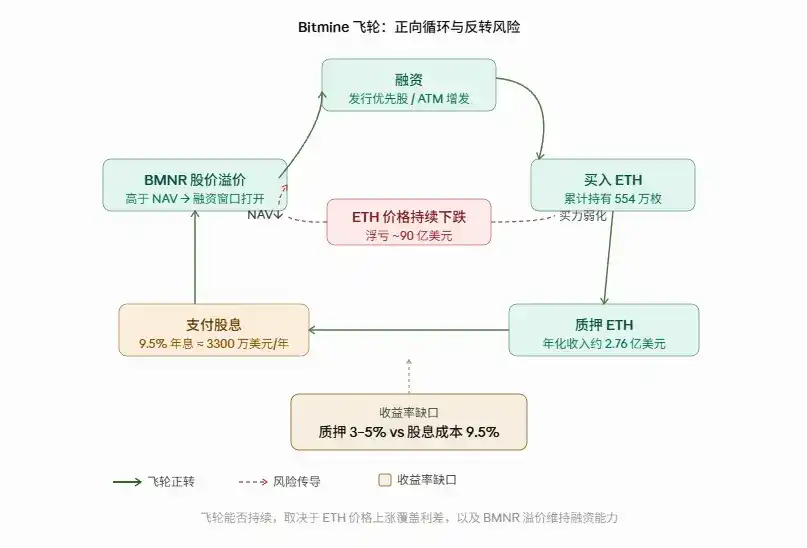

Among these, about 4.719 million ETH have been staked, accounting for over 85% of total holdings, with expected annual staking returns of approximately $230 million to $296 million. This staking system is supported by the company's self-built MAVAN validator node network, considered the key structural design that distinguishes Bitmine from Strategy.

However, the price of aggressive accumulation is also evident. With ETH currently around $1,650, the company's average cost is about $3,500. Its ETH treasury value is only about $9.3 billion, resulting in an overall company loss of $10.5 billion, a drawdown of over 50%. The company's stock price has fallen nearly 90% from its peak.

10x Research points out that Bitmine's investors face two layers of losses: the floating loss from ETH's decline is the first layer. Investors paid a premium of about $4.6 billion over the underlying ETH net asset value when purchasing BMNR stock, constituting the second layer. These two layers combined amplify the actual loss magnitude for shareholders.

Facing massive floating losses, Tom Lee has characterized this decline as superficial. He believes the existing financial system harbors a large amount of fraudulent trading, whereas Ethereum has never experienced fraudulent transactions, operates at lower costs, and both on-chain transaction volume and daily active addresses have hit record highs. The price correction is driven by macro factors and leverage unwinding, with fundamentals unharmed. The longer-term bet is that AI agent systems will rely on blockchains to operate, ETH supply continues to contract, and Ethereum is the most direct beneficiary.

Tom Lee recently revealed that Bitmine expects to complete the 5% target by the end of 2026, at which point it may no longer need to continue accumulating. He also mentioned the company is likely to be formally included in the Russell 1000 Index by the end of June. Based on market cap calculations at that time, this could bring at least $2.15 billion in passive fund inflows for BMNR.

How Can 3% Staking Yield Support a 9.5% Dividend?

On June 5th, Bitmine completed pricing for its Series A Perpetual Preferred Stock: 3.5 million shares, issue price $80 per share, par value $100, net proceeds about $274 million. The dividend yield is 9.5%, paid weekly in cash, and continues to accrue even if the board does not declare a dividend. The annualized dividend obligation is approximately $33.25 million based on par value.

Bitmine holds an early redemption right: it can redeem at 110% of par within 18 months of issuance, at 105% of par between 18 months and 3 years, and at 100% of par after 3 years, with any accumulated unpaid dividends also paid upon redemption.

At first glance, the math seems manageable. By the end of May, Bitmine had cumulatively staked 4.7 million ETH, with expected annual staking returns of $230 million to $296 million, 8 to 9 times the annualized dividend obligation.

However, the prediction exceeding $200 million is based on the assumption that the recent 4.7 million ETH are fully staked. According to the prospectus, for the six months ended February 28, 2026, the company's staking revenue was $11.18 million, annualizing to about $22 million.

It's worth noting that staking rewards are denominated in ETH, not USD. If ETH continues to fall, the company's staking income will shrink proportionally.

Here lies a fundamental difference between Bitmine and Strategy. BTC has no native yield. For STRC to pay dividends, Strategy can only rely on BTC price appreciation or selling coins, as detailed by ChainCatcher in 'Strategy Cashes Out $2.5 Million, Bitcoin Market Cap Evaporates $80 Billion'.

ETH's staking mechanism offers Tom Lee a different path: even if the price remains stagnant, staking rewards still generate income without touching the underlying holdings. This is the real stress-resistance advantage of the Bitmine model in the current bear market.

But this path doesn't seem sustainable for long. Crypto KOL chenmo points out that in the early stages with limited issuance, covering dividends with staking revenue might not be a problem. However, as the preferred stock issuance scale continues to expand, a 3-4% staking yield is destined to be unable to cover a 9.5% annual interest rate. At that point, only a rise in ETH price can sustain this logic.

Analyst Yuyue also noted that Strategy's STRC model is already under pressure in the current market. Following up with preferred stock issuance at this time, even if a short-term positive, could be interpreted by the market as a worse signal.

According to CointelegraphMT research, two details in the prospectus warrant attention. The auditor was changed to KPMG on April 27th, with simultaneous disclosure of material weaknesses in internal controls. The audit is not yet complete, and financial data may be subject to restatement.

Additionally, the board has complete discretionary power over dividend payments. The sole enforcement mechanism for preferred shareholders is the right to nominate two directors after 18 consecutive months of not receiving dividends.

If Bitmine Stops Buying After Reaching 5%, Where Will ETH's Price Go?

On-chain analyst Yu Jin stated that at the current buying pace, the target could likely be reached next month. So, will they continue buying after reaching it? If they stop, with the market's last steadfast bull disappearing, what will support ETH?

Bitmine has been the most persistent and aggressive marginal buyer in the ETH market over the past year. Other potential buying forces are scattered and weak. ETH spot ETFs saw a net outflow of $173 million overall last week. Although turning briefly positive on June 8th after 17 consecutive days of outflows, the inflow strength was far less than the previous outflow scale.

Meanwhile, Goldman Sachs reduced its ETH ETF holdings by about 70% in Q1 2026. Harvard University's endowment fund completely liquidated its approximately $87 million ETHA holdings, selling all after holding for just one quarter. Details on institutional fund movements can be found in 'Harvard and Other Institutions Liquidate, Six Core Talents Depart in One Month: What's Wrong with Ethereum?'.

Furthermore, stablecoin legislation and institutional incremental demand brought by RWA tokenization are slow-moving variables, difficult to fill a gap of Bitmine's scale in the short term.

Without an overall reversal in the crypto market, it's foreseeable that the treasury flywheel will be difficult to sustain. The transmission effect would be: ETH price continues to fall, BMNR stock price faces pressure, the premium over net assets narrows, the window for additional fundraising shrinks, the buying pace slows, and ETH further loses marginal support. This cycle doesn't even require Bitmine to actively sell a single ETH; the mere disappearance of buying power is sufficient.

Image Source: AI Generated

In a pessimistic scenario, if the financing market's acceptance of preferred stock weakens, BMNR keeps hitting new lows, buying significantly slows, ETH could potentially test the next key consensus level (around $1,000). DWF Labs co-founder Andrei Grachev believes Strategy and Bitmine have a significant chance to create the largest market crash in cryptocurrency history. This is a tail risk judgment, not a baseline expectation.

In the baseline scenario, Bitmine maintains buying, staking returns provide a buffer, preferred stock is digested smoothly, and ETH consolidates at a bottom in the $1,500 to $2,000 range. Although Bitmine is severely battered and ETH's short-term recovery is difficult, the 10x Research report mentions that when a stock falls deep enough, the underlying asset becomes almost irrelevant. What investors are buying is essentially a pure option—a free call option on ETH's future rebound, which is not yet fully priced by the market.

In an optimistic scenario, formal inclusion in the Russell 1000 brings passive funds, and the enactment of legislation like the GENIUS Act removes barriers for institutional entry. Standard Chartered maintains its year-end 2026 ETH target price of $4,000, believing the recent price drop does not reflect the continued improvement in Ethereum's network fundamentals. It compares the current situation to Amazon's phase after the 2001 bubble burst—where price temporarily disconnected from network value, but infrastructure building never stopped. The bank expects the ETH/BTC exchange rate to recover to about 0.08 by the end of this decade, with a target price of $40,000 by the end of 2030.

Conclusion

Ultimately, how long this financing can extend the life of Bitmine's flywheel comes down to ETH's price. However, Bitmine's buying itself is an important part of supporting that price.

So the core question is: after Bitmine completes its 5% target and gradually steps back, who will pick up the baton? Traditional institutions are pulling back, ETF funds flow in and out, and real incremental demand from stablecoins and RWA has yet to manifest on a large scale.

Perhaps Ethereum lacks no narratives, but when will the liquidity inflection point appear, and where will the new marginal buyers come from? These are the key questions that will determine ETH's price trajectory going forward.