Author: Claude, TechFlow Deep Tide

Deep Tide TechFlow Introduction:SpaceX's debut on Friday attracted $117 million in net retail purchases, accounting for 56% of the total U.S. retail stock buying that day. Based on this, research firm Vanda proposed the new "FAB 10" concept, advocating for replacing the long-standing "Magnificent Seven" with a frontier AI and tech top ten, including SpaceX, OpenAI, and Anthropic. The latter two are not yet public, but are expected to list later this year with valuations potentially exceeding a trillion dollars each.

SpaceX's market debut is rewriting the way Wall Street labels tech stocks.

According to a report released by Vanda Research last Sunday, cited by Cailian Press, the frenzy among retail investors for SpaceX's IPO last Friday was a huge success, sparking discussions in the market about redefining the entire tech industry. Prior to this, this fundraising round of approximately $75 billion was already the largest IPO on record. SpaceX priced its shares at $135 each, giving it a valuation of about $1.75 trillion, placing it among the world's ten most valuable publicly listed companies.

On SpaceX's Debut, Retail Buying Constituted 56% of the Day's Entire Market

Vanda's data quantifies this frenzy. The report stated that SpaceX attracted $117 million in net retail purchases on its first trading day, accounting for 56% of the total retail stock buying across the entire U.S. market that day.

This figure only reflects secondary market buying on the first day and does not include funds from retail investors who participated in the IPO allocation through brokers. Separate data indicates that retail investors ultimately received about 20% of the allocation in this $75 billion offering, above average; hedge funds got 10%, while long-term institutional investors took 70%.

The concentrated bets by retail investors are further channeling capital towards a handful of mega-cap tech companies. Vanda believes these companies are not only dominating stock market performance but are also driving the entire wave of tech investment.

Vanda: Replace the "Magnificent Seven" with the "FAB 10"

It is based on this judgment that Vanda proposed a new classification framework.

"If markets were dominated by the 'Magnificent Seven' over the past few years, then last Friday might be the clearest signal yet that investors are starting to focus on what we call the 'FAB 10'," Vanda wrote in the report. FAB 10 is short for Frontier AI & Big Tech 10, referring to the ten frontier AI and big tech giants.

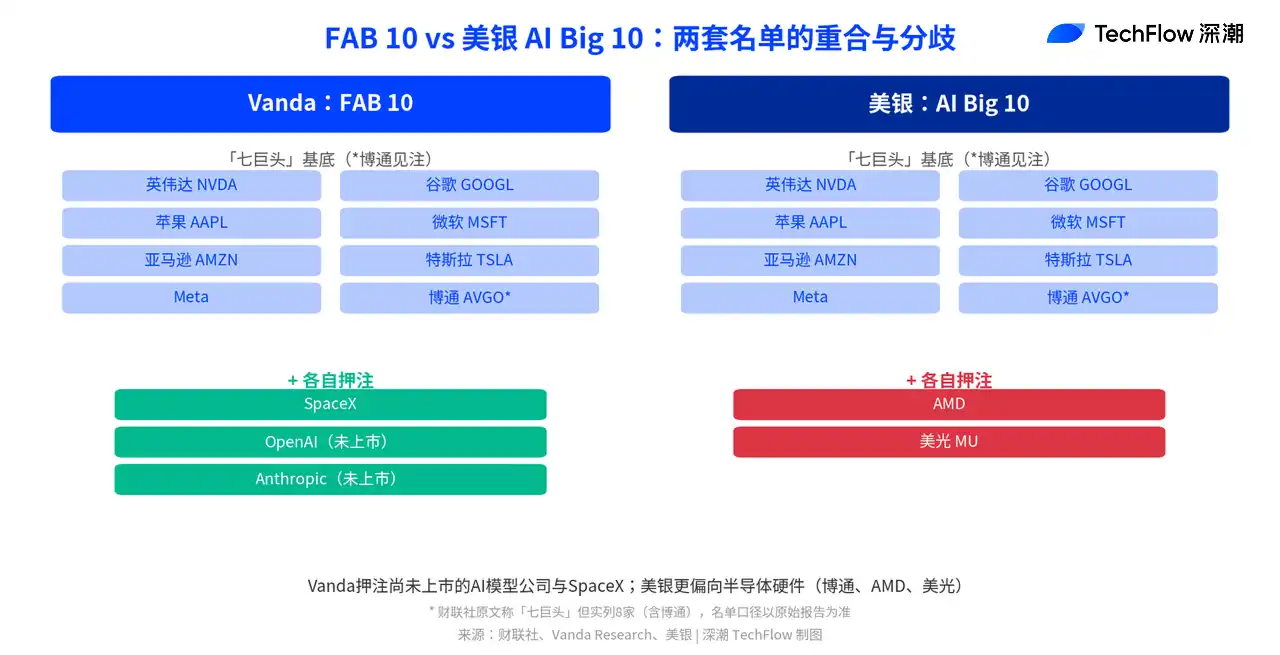

According to Vanda's definition, the FAB 10 adds SpaceX, OpenAI, and Anthropic to the original seven giants. The latter two are not yet public, but the market expects them to enter the capital market later this year, with valuations potentially reaching hundreds of billions or even trillions of dollars.

Vanda's reasoning is straightforward: these companies collectively represent the direction of the AI and tech industry for the next decade.

The Same Concept, But Bank of America's Version is Different

Vanda is not the only player packaging mega-cap tech stocks into a new index.

Bank of America's chief strategist, Michael Hartnett, previously proposed an "AI Big 10" portfolio in his "Guide to the Investment Universe." The difference from the FAB 10 lies in the stock selection: BofA's version is the Magnificent Seven plus Broadcom, AMD, and Micron, leaning more towards semiconductor hardware, while Vanda is betting on unlisted AI model companies and SpaceX.

The divergence between the two lists is essentially a different bet on "who defines the next ten years." One side favors the chipmakers, the other favors the model builders and rocket launchers.

Retail Floods into SpaceX, Chip Stocks May Suffer Capital Drain

The other side of the new concept is the redistribution of capital.

Vanda researchers noted that the fervor for SpaceX may be drawing funds away from other hot sectors, especially previously soaring chip stocks, which may be losing favor with retail investors. In other words, even within the FAB 10, favor might not be evenly spread; the capital-attracting effect of new entrants could come at the cost of pullbacks for older members.

However, analysts also caution that valuations across the tech sector are already showing signs of froth. SpaceX's IPO at a $1.75 trillion valuation itself is built on optimistic expectations for AI infrastructure. How long this optimism can last remains for the market to answer.