Core是一条面向Web3.0的全新公链,采用Satoshi Plus共识机制,比特币矿工可以通过共享算力来获得额外的CORE代币收入。并且Core是一条图灵完备的区块链,兼容以太坊虚拟机(EVM)。

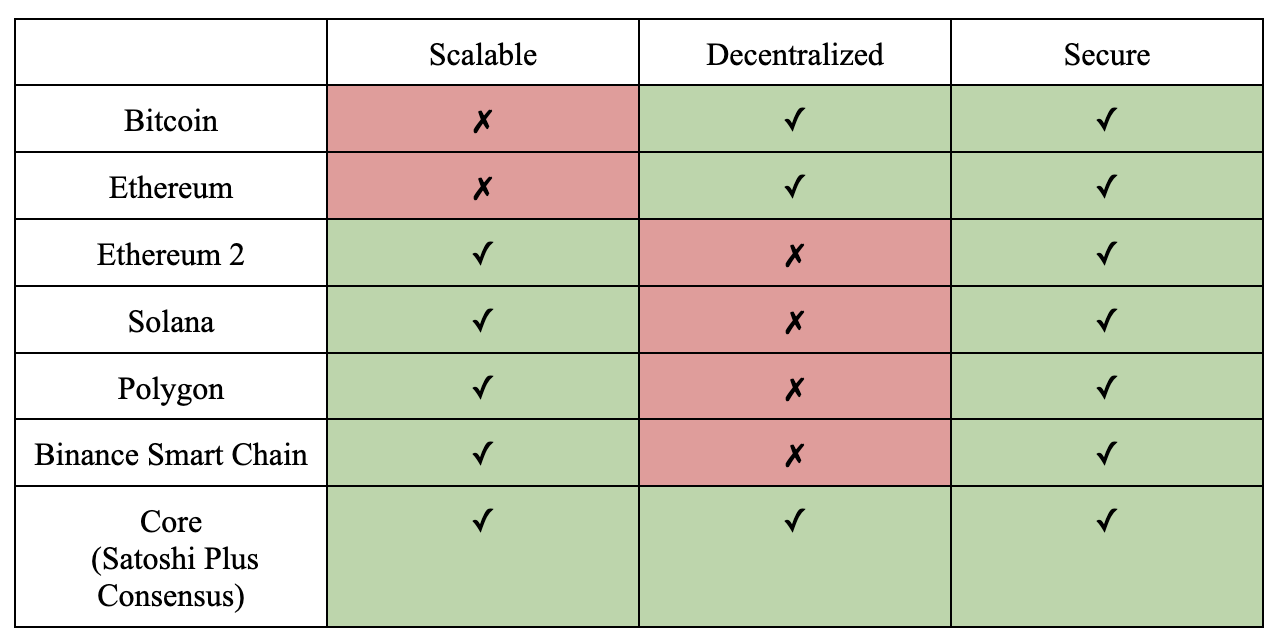

Core为了解决区块链的不可能三角问题,融合了比特币PoW和以太坊DPoS两条链的共识优势,提出了Satoshi Plus共识,完美解决了去中心化、安全性、可扩展性的三角困境。

通过Satoshi Plus Consensus,Core可以保持去中心化,而不会出现传统 PoW 共识系统中出现的性能权衡。此外,Core的混合挖矿机制基于比特币算力和CORE的抵押委托,这使得任何人都可以轻易参与到挖矿中来。

0

项目测试网

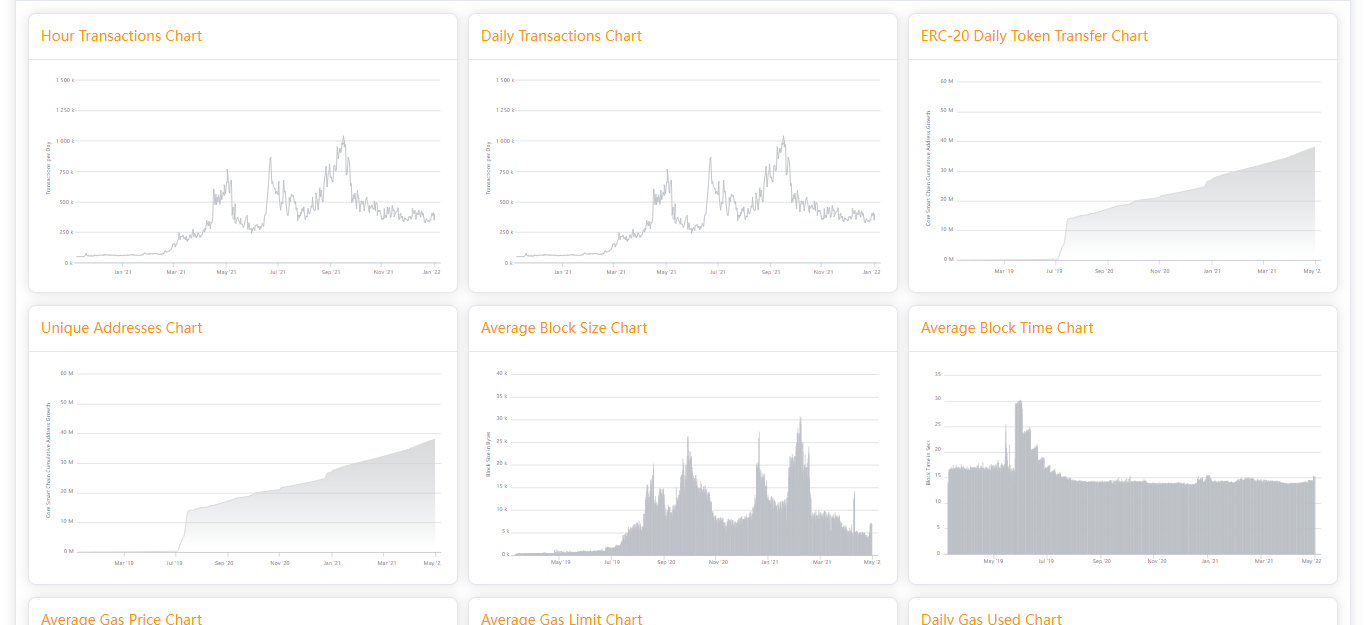

CoreDAO目前还处于测试网阶段,大家可以通过Satoshi APP进行测试挖矿,点击下载APP。在撰写本文时,CORE 已经有了下面亮眼的运营数据:

● 7000 万次 APP 下载

● 处理了 6540 万笔交易

● 137 万个地址

● 1110 万矿工

● Twitter 上有140万粉丝

● Discord 上有19.7万名成员

关于测试网的运行情况,大家可以通过测试网浏览器查看。

创世纪阶段

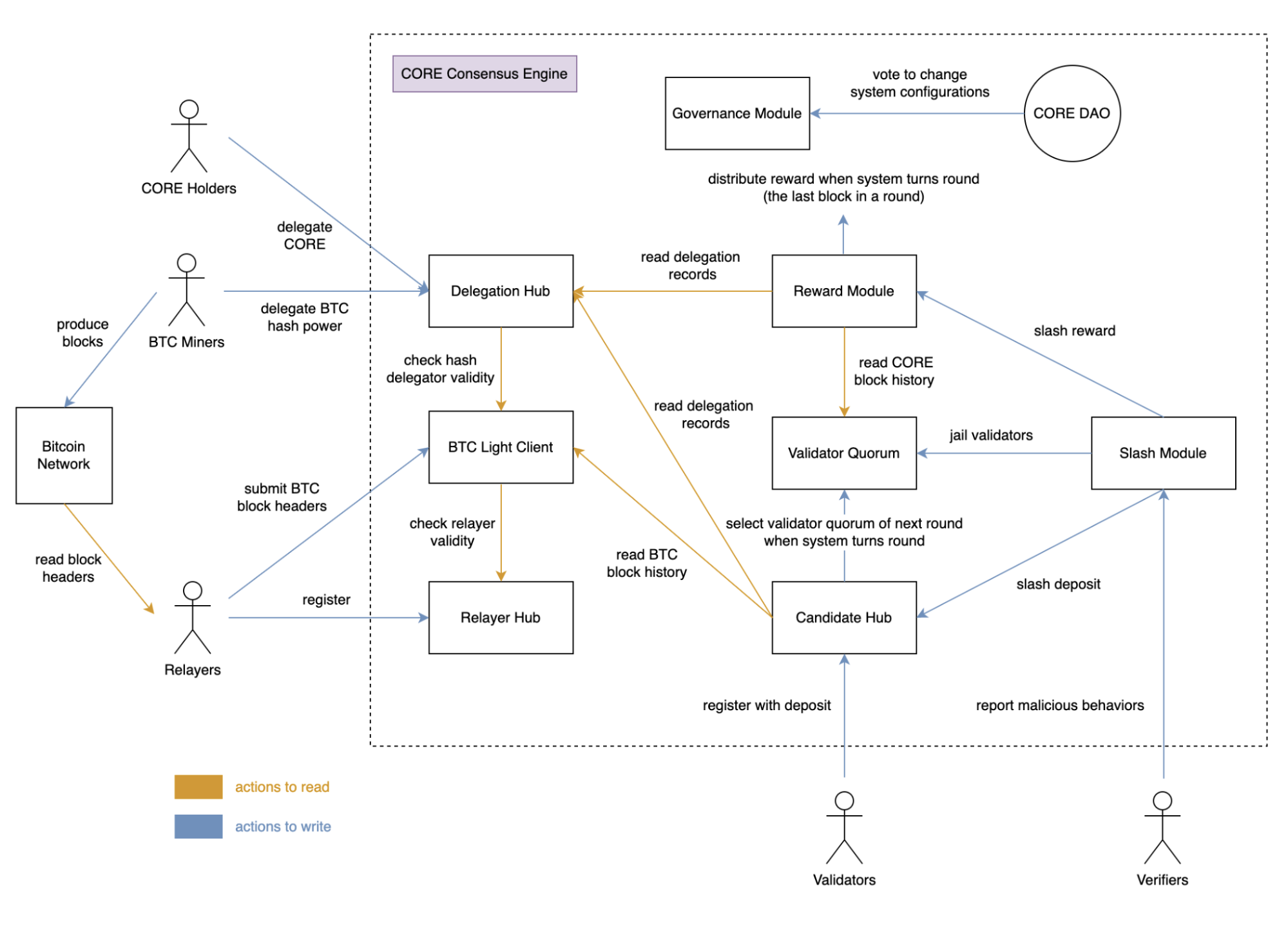

● CORE 的共识机制的 DPoS 部分将使用类似于以太坊等其他权益证明协议的功能来保护网络。

● 同时,从一开始就设计并准备好整合来自比特币挖矿生态系统的委托哈希算力,不会给比特币矿工带来额外成本。比特币矿工的参与最终将通过将其共识锚定在比特币的去中心化网络中来强化 CORE 网络。

0

早期主网阶段

CORE将专注于将比特币矿工带入网络。

● 为了激励早期采用,比特币算力的早期委托人将有资格获得激励奖励计划

● 这些计划增加了矿工通过委托他们的比特币算力而有机地获得的回报

将比特币算力委托给CORE网络的早期矿工将有三种货币化回报:激励奖励、基本奖励和交易费用(如果他们选择运行验证器)。这些早期的努力有助于进一步分散网络的安全设备,并加强比特币矿工与 CORE 网络之间的共生关系。

0

后期主网阶段

比特币的基础奖励将在 2040 年枯竭,CORE网络仍将存在,为比特币矿工提供额外奖励。通过这种方式,CORE的奖励就像额外比特币区块补贴。结合非常轻量级的实施,将比特币算力委托给CORE网络对于比特币矿工来说将是很不错的回报。通过为比特币矿工提供额外的收入机会,Satoshi Plus同时加强了CORE和比特币网络。

0

CoreDAO Staker 的被动收入

CORE持有者可以通过在Satoshi APP中称为DPoS的过程进行质押来赚币。CORE的质押者可以将他们质押的份额委托给验证者。

通过质押这些资产,用户分散了验证者获得的激励和奖励。验证者选择奖励利益相关者的多少,并受到激励使其变得有价值。

在这种关系下,委托的验证者可以以更大的能力努力达成共识。这进一步民主化了CORE区块链的共识机制,同时为线下的利益相关者提供奖励。

0

小结

目前Core的主网上线时间尚未确定,大家静静等待就好,毕竟测试网已经很成熟,主网上线时间不会太久。火必在12月30日发布公告,称将在Core主网上线后第一时间做上线审核,这也说明正式主网即将到来。