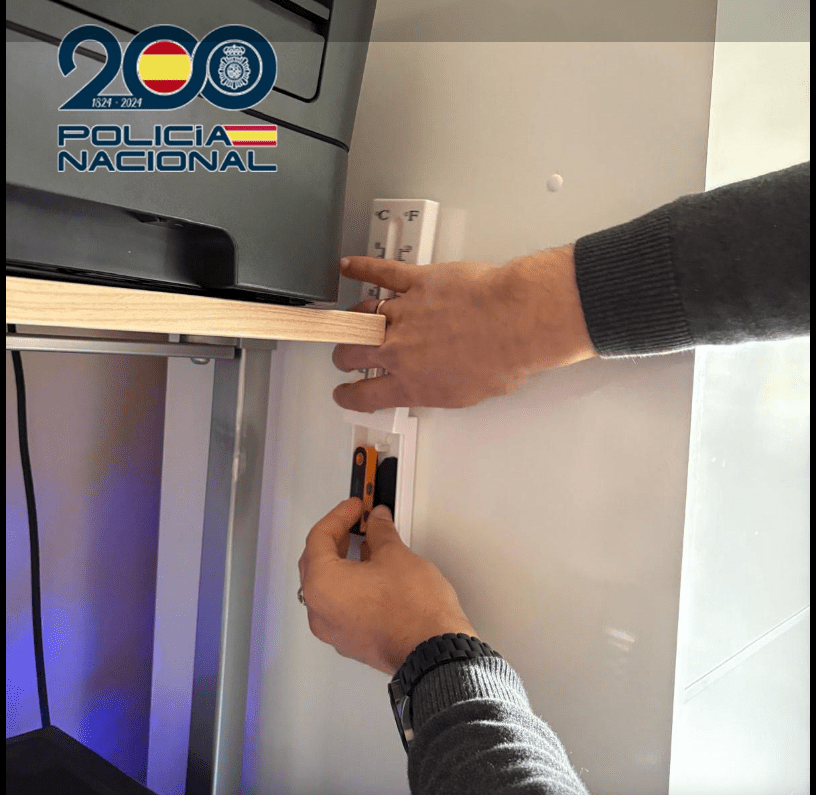

Испанская полиция обнаружила необычную находку во время обыска — два криптокошелька холодного хранения, спрятанные внутри бытового настенного термометра. На устройствах находилось около 400 000 евро, что примерно равно $467 000.

Власти задержали трех подозреваемых в Альмерии в связи с тем, что официальные лица назвали крупнейшей в истории страны платформой нелегального распространения испаноязычной манги.

Сайт работал с 2014 года. За примерно десятилетие он заработал более 4 миллионов евро — около $4,55 миллиона — в основном за счет рекламных доходов. Посетители получали бесплатный доступ к пиратской манге, в то время как операторы тихо собирали деньги за рекламу на фоне.

Министерство внутренних дел Испании подтвердило аресты и изъятие. Расследование было начато в июне 2025 года после того, как правообладатели подали жалобы на платформу.

Власти обнаружили необычную находку во время обыска: два криптокошелька холодного хранения, спрятанные внутри бытового настенного термометра. Источник: Ministerio Del Interior

Могут ли полицейские реально получить доступ к средствам, остается неясным

Изъять холодный кошелек — это одно. Попасть внутрь него — другое.

Холодные кошельки требуют PIN-код или сид-фразу для разблокировки. Без этих учетных данных оборудование по сути бесполезно — средства остаются заблокированными, недоступными для anyone, включая правоохранительные органы.

Чиновники не сообщили, получили ли они информацию, необходимую для открытия устройств. Министерство внутренних дел Испании не ответило на запросы о комментариях до публикации статьи.

Испанская национальная полиция ликвидировала крупный сайт нелегального распространения манги, который работал с 2014 года из Альмерии.

Сайт привлек миллионы пользователей и заработал более 4 миллионов € на рекламе

Офицеры задержали 3 человек по обвинениям в преступлениях против интеллектуальной собственности.... pic.twitter.com/RtkDie2kfw

— Pirat_Nation 🔴 (@Pirat_Nation) 22 апреля 2026 г.

Это дело проливает свет на проблему, над которой полицейские управления по всему миру все еще работают. Аппаратные кошельки появляются в расследованиях, которые не имеют ничего общего с мошенничеством с криптовалютой или схемами с цифровой валютой. Оказывается, пиратские операции теперь хранят заработок так же, как и криптоинвесторы.

Южная Корея столкнулась с собственными проблемами хранения

Даже когда власти могут получить доступ к изъятой криптовалюте, удерживать ее оказалось сложно. В последние годы Южная Корея столкнулась с двумя громкими случаями потери конфискованных цифровых активов.

В одном случае около 22 биткоинов — стоимостью $1,5 миллиона на тот момент — пропали из полицейского участка Каннама.

Средства были изъяты в 2021 году и исчезли без физической кражи холодного кошелька, согласно отчетам. Общенациональная проверка практик хранения цифровых активов выявила потерю.

Изображение для статьи: DualShockers, график: TradingView