Original Author: Eric, Foresight News

On the evening of June 30th, Beijing Time, the emergence of a new stablecoin once again stirred the stablecoin landscape.

A company named Open Standard announced it would launch the stablecoin Open USD. Features like free minting and redemption, shared revenue from reserve assets, and co-governance by partners directly address pain points in stablecoin distribution, making it seem very attractive.

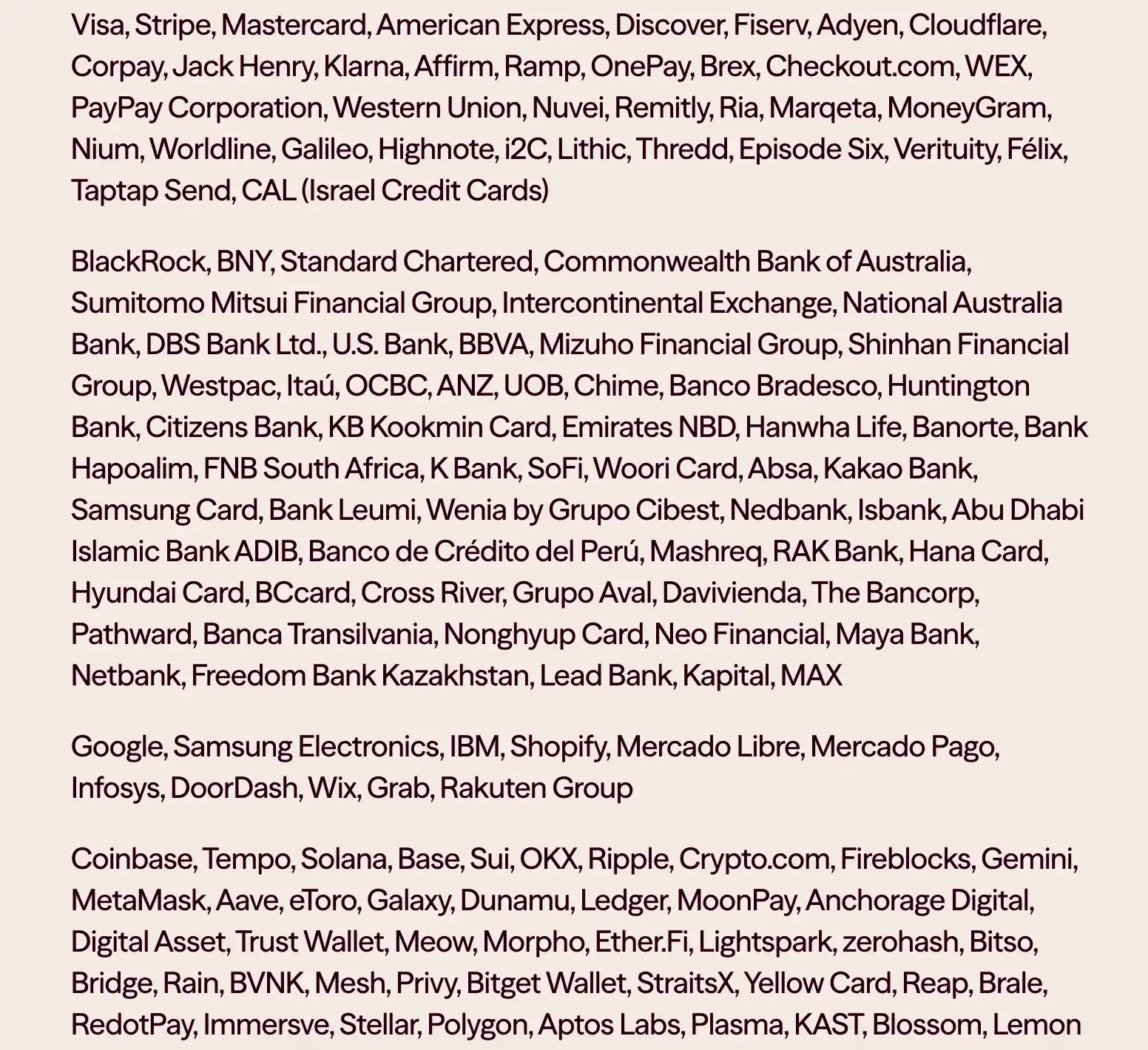

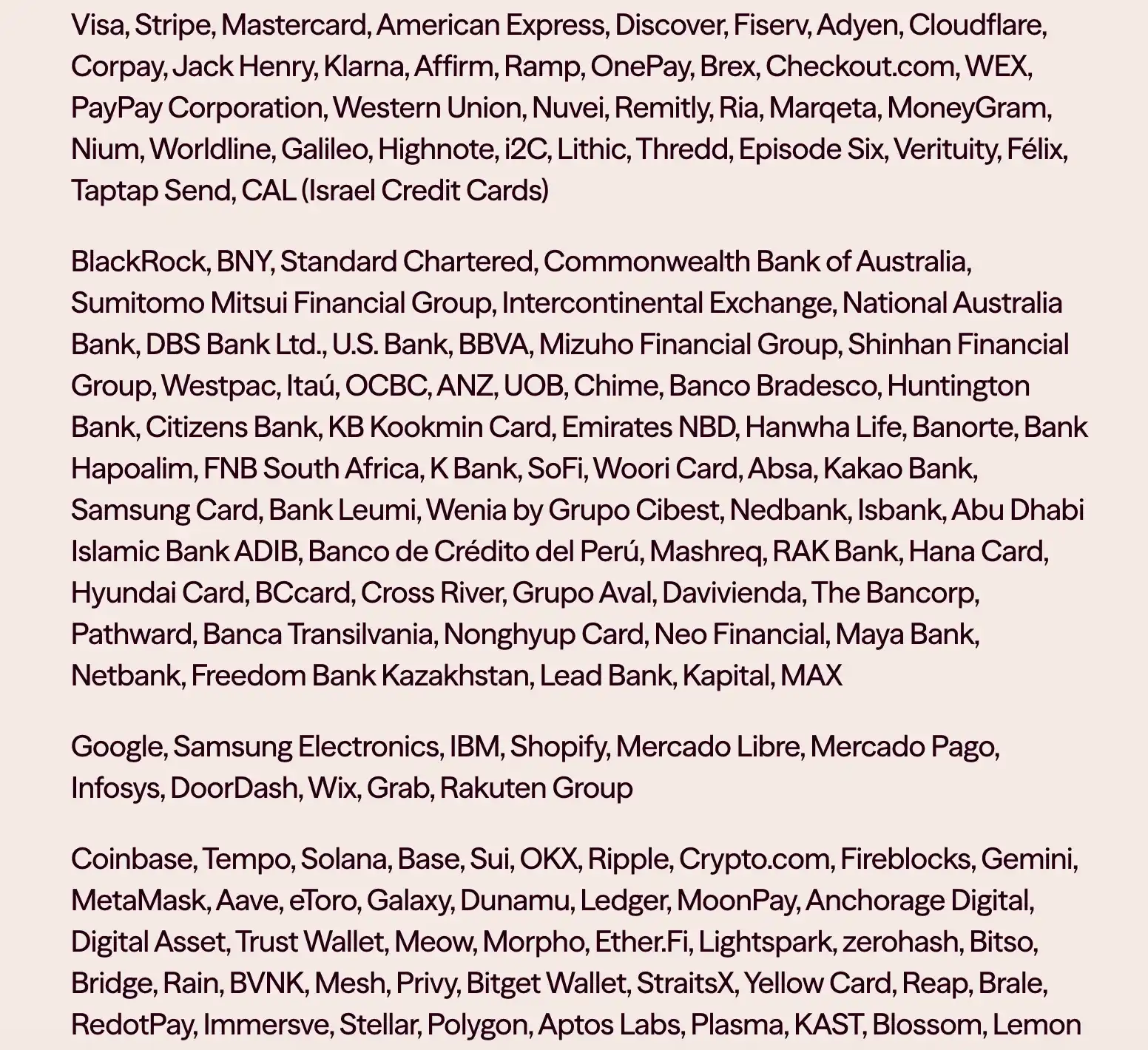

What most surprised the market was that Open Standard had already "secured" over 140 partners before the stablecoin's launch.

The list included major companies that have already issued stablecoins, such as Western Union, Ripple, MetaMask, Aave, and others. The fact that it could gather signatures from so many giants in both Web3 and traditional finance before launch amazed the market and filled it with high expectations for Open USD's future. The most telling manifestation of this expectation was that Circle, the leading stablecoin company, saw its stock price plunge 17.55% that day, hovering just under 20% above a new low.

However, this explosive announcement was quickly debunked.

On July 3rd, according to a report by The Chosun Ilbo, companies including Samsung Electronics, Dunamu (parent company of Upbit), Shinhan Financial Group, and K Bank stated they had never held negotiations regarding Open USD (OUSD). A Samsung Electronics representative said, "There has been no formal negotiation, and we don't know what role (we are supposed to play) in the alliance." Shinhan Financial Holdings, Dunamu, and K Bank also said that Open Standard had inquired about their willingness to participate in OUSD, and they merely stated they "would consider it briefly," yet their names were listed as alliance members.

Tony Chung, BD Head at the Korean Web3 media Blockmedia, further stated that a representative from one of the Korean companies said they learned about being included on the list from Korean media reports and were "very perplexed" because they had only casually replied, "If feasible, we will consider it."

OpenAssets founder and CEO Gabor Gurbacs reposted Tony Chung's tweet, adding that it wasn't just Korean companies being misled. After contacting some OpenAssets clients on the list, Gabor Gurbacs received responses stating: "They indicated they never signed or agreed to any deals. Either the media severely misrepresented the facts, or the participant list is misleading."

It appears that Open Standard's "list of over a hundred companies" may have included some firms that were merely contacted. In the original announcement, Open Standard stated: "Businesses across industries have signed up to use Open USD." Perhaps in Open Standard's view, not explicitly refusing equals "agreeing" to use Open USD. But agreeing to use doesn't necessarily mean "committing to using" it.

This is a very typical marketing tactic of trading controversy for attention, which indeed produced some effect, albeit one that seems to trample business ethics underfoot.

Faced with such fierce competition and a "dishonorable" opponent, Circle co-founder and CEO Jeremy Allaire published a lengthy post on X questioning the "three key features" of Open USD:

Free minting and burning: Attractive in the short term, but likely unsustainable at scale, potentially leading to insufficient funds to maintain banking relationships, regulatory licenses, and tech infrastructure. Circle already offers preferential terms via contracts for large partners, not blanket free services.

Sharing nearly all revenue with partners: Could "starve" the infrastructure, leading to systemic underinvestment and limiting platform scale. Circle already shares most revenue with distribution partners.

Alliance / multi-company governance: Circle previously co-founded the Centre Consortium with Coinbase, which was later integrated for Circle's solo issuance. He stated the historical track record for scaling multi-company products is "very poor" (slow coordination, difficult decision-making).

Jeremy expressed a welcoming attitude towards OUSD joining the "stablecoin family," but his writing between the lines conveyed one viewpoint: stablecoin is a business where a winner-takes-all situation forms over time through accumulation; simply tweaking a few mechanisms isn't enough to "get a seat at the table."

Despite these negative controversies, some companies on the list have explicitly stated they will support Open USD's development. Stripe said it will set OUSD as the default stablecoin for businesses using stablecoins on Stripe; Coinbase also stated it will integrate OUSD into Base and other chains, planning to launch in late 2026 for expanding on-chain transactions, payments, and DeFi scenarios.

Payment network giants like Visa, Mastercard, financial institutions like BlackRock, BNY Mellon, and crypto-native projects like Aave, Solana, Ripple have also expressed support, but have not clarified specific cooperation methods yet.

According to the announcement, the founding CEO of Open Standard is the CEO of Bridge. This Bridge is the fiat on-ramp/off-ramp solution provider that had previously cooperated with multiple contenders in the battle for the issuance rights of Hyperliquid's native stablecoin USDH, but whose acquisition by Stripe, which is developing the stablecoin chain Tempo, sparked controversy. Stripe was also among the first to clarify its partnership after Open Standard's announcement, indicating a relatively close connection between the two.

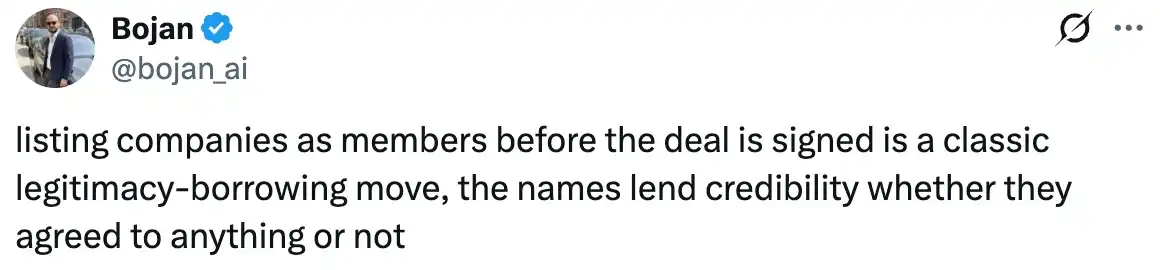

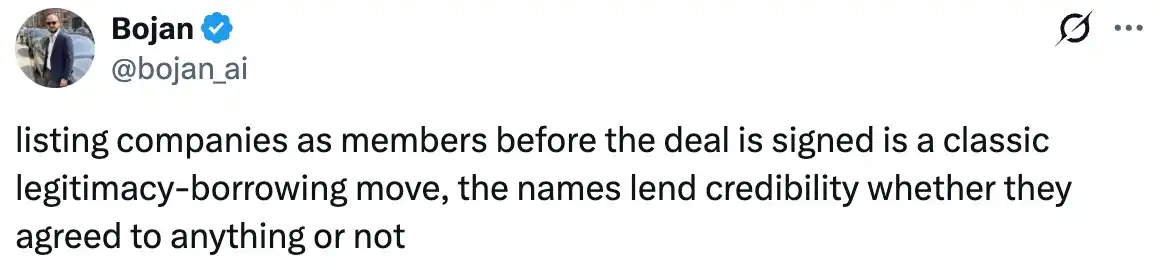

A user named Bojan on X stated that Open Standard's promotion is a typical "legitimacy-borrowing" behavior—quickly enhancing its own legitimacy and credibility by borrowing the reputation or endorsement of other well-known, reliable entities, without actually having obtained their deep recognition or formal authorization. For the stablecoin track, which requires trust as its foundation, OUSD seems to have left a somewhat negative first impression even before its debut.

On the evening of June 30th, Beijing Time, the emergence of a new stablecoin once again stirred the stablecoin landscape.

A company named Open Standard announced it would launch the stablecoin Open USD. Features like free minting and redemption, shared revenue from reserve assets, and co-governance by partners directly address pain points in stablecoin distribution, making it seem very attractive.

What most surprised the market was that Open Standard had already "secured" over 140 partners before the stablecoin's launch.

The list included major companies that have already issued stablecoins, such as Western Union, Ripple, MetaMask, Aave, and others. The fact that it could gather signatures from so many giants in both Web3 and traditional finance before launch amazed the market and filled it with high expectations for Open USD's future. The most telling manifestation of this expectation was that Circle, the leading stablecoin company, saw its stock price plunge 17.55% that day, hovering just under 20% above a new low.

However, this explosive announcement was quickly debunked.

On July 3rd, according to a report by The Chosun Ilbo, companies including Samsung Electronics, Dunamu (parent company of Upbit), Shinhan Financial Group, and K Bank stated they had never held negotiations regarding Open USD (OUSD). A Samsung Electronics representative said, "There has been no formal negotiation, and we don't know what role (we are supposed to play) in the alliance." Shinhan Financial Holdings, Dunamu, and K Bank also said that Open Standard had inquired about their willingness to participate in OUSD, and they merely stated they "would consider it briefly," yet their names were listed as alliance members.

Tony Chung, BD Head at the Korean Web3 media Blockmedia, further stated that a representative from one of the Korean companies said they learned about being included on the list from Korean media reports and were "very perplexed" because they had only casually replied, "If feasible, we will consider it."

OpenAssets founder and CEO Gabor Gurbacs reposted Tony Chung's tweet, adding that it wasn't just Korean companies being misled. After contacting some OpenAssets clients on the list, Gabor Gurbacs received responses stating: "They indicated they never signed or agreed to any deals. Either the media severely misrepresented the facts, or the participant list is misleading."

It appears that Open Standard's "list of over a hundred companies" may have included some firms that were merely contacted. In the original announcement, Open Standard stated: "Businesses across industries have signed up to use Open USD." Perhaps in Open Standard's view, not explicitly refusing equals "agreeing" to use Open USD. But agreeing to use doesn't necessarily mean "committing to using" it.

This is a very typical marketing tactic of trading controversy for attention, which indeed produced some effect, albeit one that seems to trample business ethics underfoot.

Faced with such fierce competition and a "dishonorable" opponent, Circle co-founder and CEO Jeremy Allaire published a lengthy post on X questioning the "three key features" of Open USD:

Free minting and burning: Attractive in the short term, but likely unsustainable at scale, potentially leading to insufficient funds to maintain banking relationships, regulatory licenses, and tech infrastructure. Circle already offers preferential terms via contracts for large partners, not blanket free services.

Sharing nearly all revenue with partners: Could "starve" the infrastructure, leading to systemic underinvestment and limiting platform scale. Circle already shares most revenue with distribution partners.

Alliance / multi-company governance: Circle previously co-founded the Centre Consortium with Coinbase, which was later integrated for Circle's solo issuance. He stated the historical track record for scaling multi-company products is "very poor" (slow coordination, difficult decision-making).

Jeremy expressed a welcoming attitude towards OUSD joining the "stablecoin family," but his writing between the lines conveyed one viewpoint: stablecoin is a business where a winner-takes-all situation forms over time through accumulation; simply tweaking a few mechanisms isn't enough to "get a seat at the table."

Despite these negative controversies, some companies on the list have explicitly stated they will support Open USD's development. Stripe said it will set OUSD as the default stablecoin for businesses using stablecoins on Stripe; Coinbase also stated it will integrate OUSD into Base and other chains, planning to launch in late 2026 for expanding on-chain transactions, payments, and DeFi scenarios.

Payment network giants like Visa, Mastercard, financial institutions like BlackRock, BNY Mellon, and crypto-native projects like Aave, Solana, Ripple have also expressed support, but have not clarified specific cooperation methods yet.

According to the announcement, the founding CEO of Open Standard is the CEO of Bridge. This Bridge is the fiat on-ramp/off-ramp solution provider that had previously cooperated with multiple contenders in the battle for the issuance rights of Hyperliquid's native stablecoin USDH, but whose acquisition by Stripe, which is developing the stablecoin chain Tempo, sparked controversy. Stripe was also among the first to clarify its partnership after Open Standard's announcement, indicating a relatively close connection between the two.

A user named Bojan on X stated that Open Standard's promotion is a typical "legitimacy-borrowing" behavior—quickly enhancing its own legitimacy and credibility by borrowing the reputation or endorsement of other well-known, reliable entities, without actually having obtained their deep recognition or formal authorization. For the stablecoin track, which requires trust as its foundation, OUSD seems to have left a somewhat negative first impression even before its debut.