Автор: Sanqing, Foresight News

23 января, согласно последнему объявлению Binance, официально запущена специальная программа аирдропа для держателей World Liberty Financial USD (USD1). В рамках мероприятия будет распределено токенов World Liberty Financial (WLFI) на общую сумму, эквивалентную 40 миллионам долларов США.

Данное мероприятие является продолжением предыдущей акции Binance по заработку с гарантией капитала для USD1. С 24 декабря прошлого года по 24 января текущего года Binance предлагала вознаграждение в USD1 с годовой доходностью 20% для депозитов до 50 000 USD1. Под влиянием новостей об этой акции спотовая цена USD1 на Binance перешла с отрицательного премиума к положительному премиуму в 0.19% по отношению к USDT и в настоящее время котируется на уровне 1.0019 USDT.

Период проведения и распределение вознаграждений

Аирдроп продлится четыре недели, с 23 января 2026 года по 20 февраля 2026 года. В течение периода проведения акции Binance будет еженедельно распределять токены WLFI на сумму, эквивалентную 10 миллионам долларов США.

Первые вознаграждения планируется распределить 2 февраля, они покроют статистику холдингов за первую неделю акции. Последующие вознаграждения будут распределяться еженедельно по пятницам в течение периода акции, токены будут напрямую зачисляться на соответствующие индивидуальные спотовые счета.

Условия участия и механизм расчета

Согласно объявлению, для участия в данном аирдропе пользователи должны соответствовать определенным требованиям к активам на счете.

Квалифицируемые активы: Пользователи должны иметь чистые активы в USD1 на спотовом счете Binance, счете Funding, маржинальном счете или счете фьючерсов в USDT. Обратите внимание, что USD1 на сберегательных счетах не учитывается в статистике данного аирдропа.

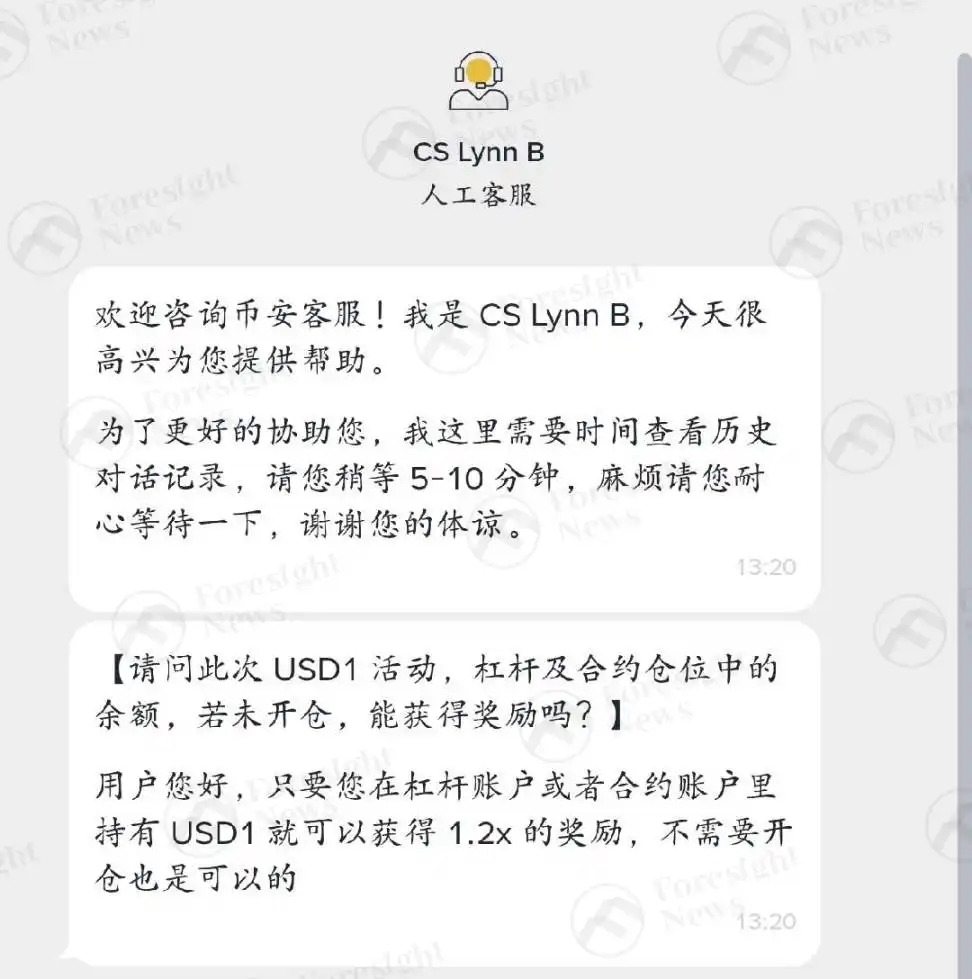

Повышающий коэффициент: Пользователи, использующие USD1 в качестве залога на маржинальном или фьючерсном счете, получат повышающий коэффициент вознаграждения 1.2. По подтверждению службы поддержки Binance, для получения коэффициента достаточно перевести активы, обязательные требования к торговле (открытию позиций) отсутствуют.

Рис. - Ответ службы поддержки Binance

Стандарт расчета: Система будет отслеживать остатки с помощью нескольких ежечасных снепшотов, а для расчетов будет использоваться минимальный дневной остаток по снепшотам.

Определение чистых активов: В квалифицируемый баланс учитываются только чистые активы в USD1 (т.е. холдинги за вычетом обязательств в USD1, возникших в результате займа или маржинальной торговли), остаток на отдельном счете должен превышать 0.01 USD1.

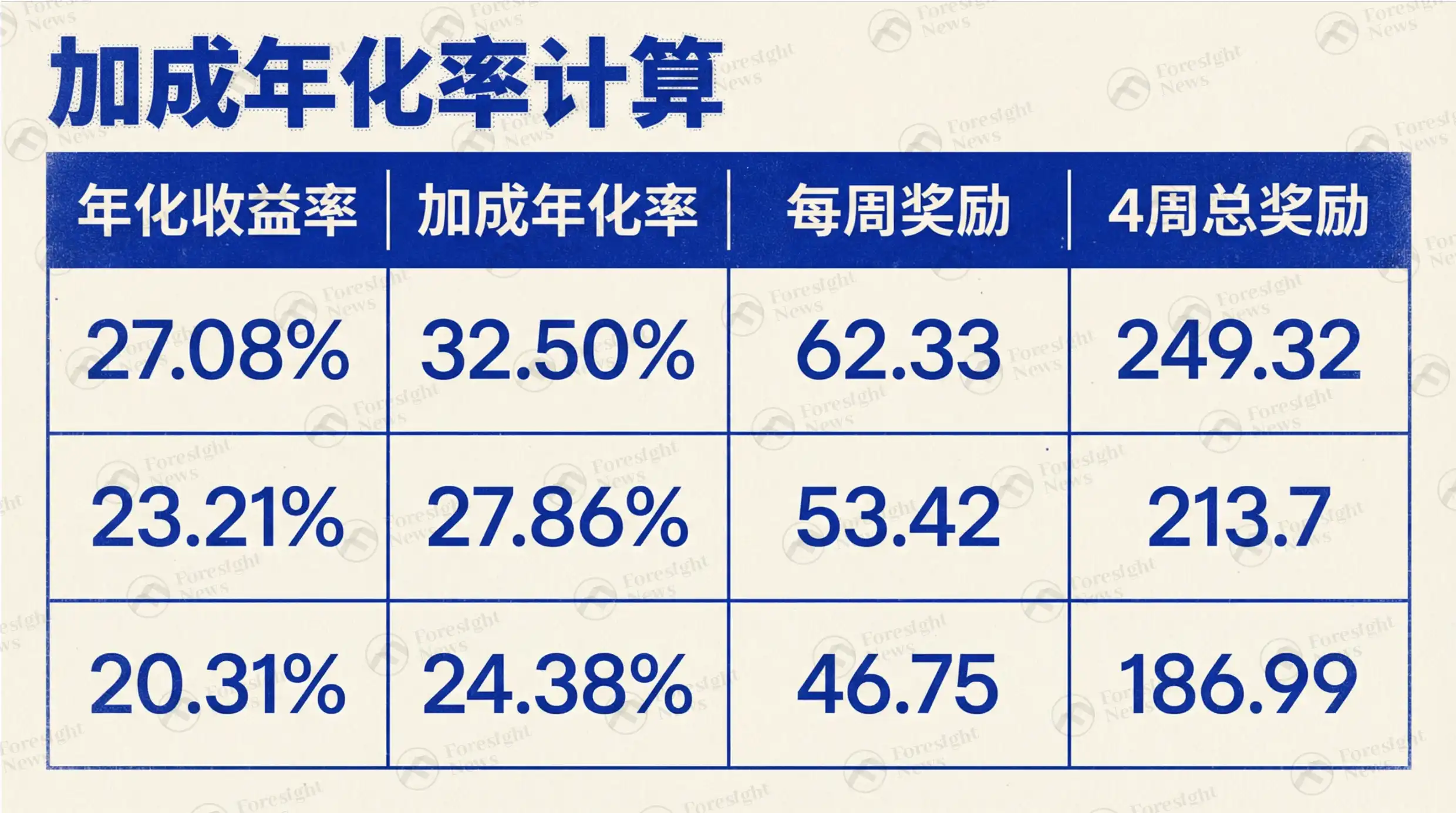

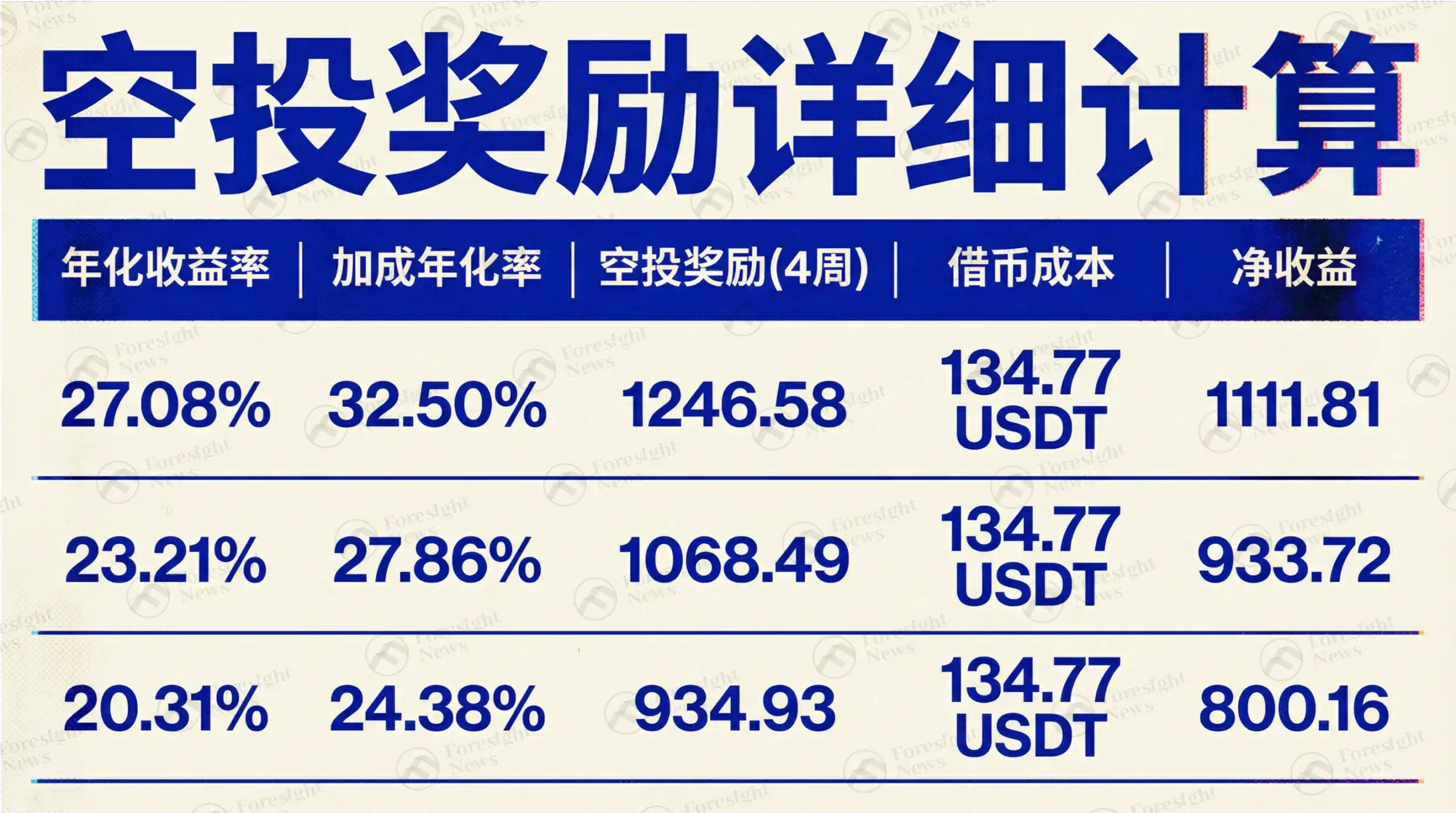

Моделирование доходности

На данный момент общий объем USD1 составляет около 3.2 миллиарда. Еженедельное вознаграждение эквивалентно 10 миллионам долларов США в WLFI. Оценка годовой доходности based on предположении о存量 USD1 на Binance (если бы все участвовали в акции):

Оценка годовой процентной доходности (APY)

Вознаграждение для спотового и Funding-счета (холдинг 10,000 USD1)

Вознаграждение для маржинального и фьючерсного счета (холдинг 10,000 USD1, коэффициент 1.2)

Вознаграждение для счета с 5-кратным плечом (холдинг 10,000 USDT, покупка USD1 с плечом, коэффициент 1.2)

Примечание: Часовая процентная ставка по маржинальному продукту Binance USD1/USDT составляет примерно 0.0005%. Стоимость займа за 4 недели估算руется на основе этой ставки.

Сравнение трех сценариев

Примечание: В расчетах не учтена премия USD1. Кроме того, объем холдингов USD1 на Binance не является публичной информацией, приведенные данные являются оценочными.