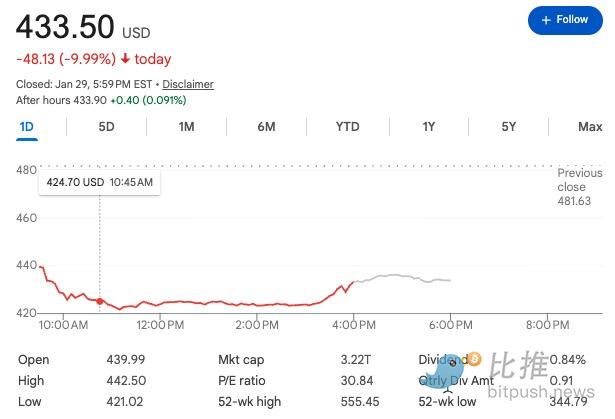

После публикации отчета, превзошедшего рыночные ожидания, Microsoft (Microsoft) столкнулась с самым резким за год рыночным распродажами.

В четверг акции софтверного гиганта Microsoft рухнули на 7% во внеурочных торгах, а рыночная капитализация за один день сократилась на 357 миллиардов долларов — эта сумма эквивалентна тому, как если бы целая компания Coca-Cola исчезла с лица земли. И всё это в тот же день, когда Microsoft представила практически идеальные результаты: прибыль выросла почти на четверть, выручка достигла исторического максимума.

Прибыль растёт, а акции обваливаются. За голосованием ногами Уолл-стрит скрывается молчаливый страх: чем больше считаешь затраты на ИИ, тем страшнее становится. История роста подошла к концу? Когда все гиганты挤在一条赛道上, кто还能真正 заработать?

Красивая "оболочка" и трескающаяся "начинка"

С точки зрения первой строки финансового отчёта, показатели Microsoft были впечатляющими:

-

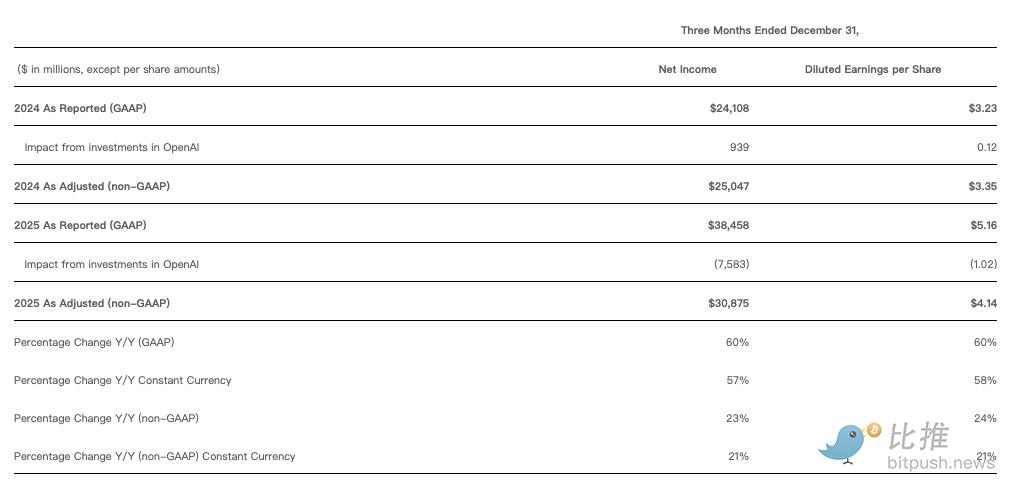

Чистая прибыль: скорректированная чистая прибыль выросла на 23%, достигнув 30,9 миллиарда долларов, что выше ожиданий аналитиков в 28,9 миллиарда долларов.

-

Выручка: рост на 17% до 813 миллиардов долларов, также превысив ожидаемые 803 миллиарда долларов.

-

Облачный бизнес: квартальный доход впервые превысил 500 миллиардов долларов.

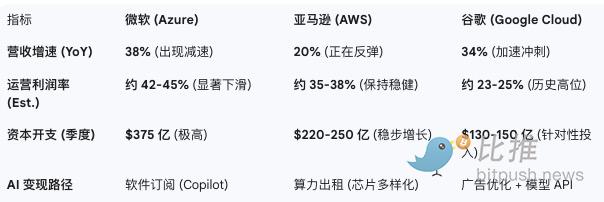

Однако внимание рынка быстро сосредоточилось на двух деталях: темпе роста Azure и скорости расширения капитальных затрат.

Отчёт показал, что годовой темп роста Azure составил 38%, что по-прежнему сильно, но на один процентный пункт ниже, чем 39% в предыдущем квартале.

На фоне исторически высоких оценок это замедление на 1% было воспринято как сигнал о "достижении пика роста". Аналитик Barclays прямо заявил: "Даже несмотря на здоровые общие цифры, покупатели-инвесторы явно хотят видеть больше".

Microsoft стала "рабочим по железу"?

В этой золотой лихорадке ИИ Microsoft, хотя и является лидером, больше похожа на "высококлассного подрядчика".

За астрономическими инвестициями скрывается чрезвычайно жёсткое давление цен на аппаратное обеспечение. Согласно последнему отраслевому отчёту TrendForce по состоянию на январь 2026 года, HBM (память с высокой пропускной способностью), являющаяся ключевым компонентом для серии NVIDIA B200, переживает беспрецедентный "захват мощностей".

Мониторинг данных показывает, что поскольку заказы на HBM от Micron и SK Hynix уже расписаны в основном до начала 2027 года, средняя цена чипов HBM за последние два квартала выросла примерно на 30%. Для Microsoft это равносильно "структурному шантажу". Чтобы вычислительная мощность Azure AI не отставала, Microsoft вынуждена принимать надбавку в тысячи долларов за каждый чип.

Сравнение ключевых данных облачных гигантов (2025 Q4 – 2026 Q1)

Что это значит?

Сотни миллиардов долларов, которые Microsoft инвестирует ежеквартально, в основном уходят к поставщикам аппаратного обеспечения. Это означает, что деньги, которые зарабатывает Microsoft, не успевают осесть на счетах, как уже передаются NVIDIA за видеокарты и Micron за память. Хотя Microsoft также разрабатывает собственные чипы Maia, на данный момент она по-прежнему сильно зависит от внешних закупок. Результат жесток: валовая маржа облачного бизнеса Microsoft снизилась с отметки выше 70% до примерно 67%.

Для сравнения, конкурент Amazon AWS, благодаря собственным чипам (серия Trainium), разработанным ранее, снизил зависимость от дорогого оборудования, и его операционная маржа по-прежнему стабильно держится на уровне 38%. А Meta, хотя и также делает крупные инвестиции, но поскольку ИИ напрямую повышает конверсию рекламы, её акции, наоборот, выросли на 10%, так как "увидели квитанции". По сравнению с ними, Microsoft больше похожа на "рабочего" для производителей оборудования.

Такие "кровоточащие" инвестиции не только не смогли удовлетворить аппетиты рынка, но и спровоцировали внутреннее "поглощение" вычислительных мощностей, характерное для Microsoft. Из-за ограниченности поставок Microsoft вынуждена faced с жестоким балансом: сдавать в аренду внешним облачным клиентам самые передовые вычислительные мощности для получения мгновенной прибыли или оставлять их собственному Copilot для будущего экосистемы? Microsoft выбрала последнее. Эта стратегия "пожертвовать внешним ради внутреннего" хотя и стабилизировала пользовательский опыт, но серьёзно снизила рентабельность Azure как pure-play облачной платформы в краткосрочной перспективе.

Тревога концентрации: кризис "зависимости от одной точки" OpenAI

В этом отчёте Microsoft впервые раскрыла ошеломляющие данные: около 45% из её будущей балансовой стоимости облачных контрактов в 6,25 триллиона долларов приходится на OpenAI.

Это означает, что рост облачного бизнеса Microsoft сильно привязан к одной стартап-компании. Хотя финансовый директор Эми Худ подчеркнула, что ещё 3,5 триллиона долларов поступило от клиентов из других отраслей, инвесторы по-прежнему обеспокоены: если OpenAI замедлится в конкурентной борьбе или в будущем перейдёт на собственное оборудование, эта дорогостоящая система Microsoft столкнётся с серьёзным "риском простоя".

Размывание рва: снижающий измерение удар открытого кода и низких затрат

Кроме того, тесная привязка к OpenAI сталкивается с снижающим измерение ударом "революции性价比" (соотношения цена/качество).

С появлением таких недорогих или открытых моделей, как китайский DeepSeek, на рынке ИИ началась "ценовая война". Когда корпоративные клиенты обнаруживают, что модели с открытым исходным кодом стоимостью в несколько центов могут решить 90% проблем, модель подписки на Copilot от Microsoft с высокой надбавкой сталкивается с challenges.

Эта неопределённость бизнес-модели делает высокий коэффициент P/E (цена/прибыль) Microsoft шатким. Если Microsoft не сможет доказать, что её высокие затраты на вычислительные мощности могут трансформироваться в столь же высокий доход с надбавкой, то ров, который она построила, может быть незаметно сровнен с землёй волной open source.

Перед лицом падения акций Наделла остаётся непоколебимым. На телеконференции с аналитиками он активно продвигал своё видение "полного стека ИИ": "Когда вы думаете о наших капитальных затратах, думайте не только об Azure, думайте о Copilot. Мы не хотим максимизировать только один бизнес, мы хотим распределять мощности для создания лучшего портфеля активов".

Заключение

Несмотря на панические распродажи на рынке, этот гигант стабилизирует ситуацию с помощью серии сложных капитальных операций.

Microsoft в этом квартале disclosed бухгалтерскую прибыль в размере 7,6 миллиарда долларов, полностью обеспеченную её ранними инвестициями в OpenAI. После реорганизации OpenAI в октябре из некоммерческой организации в традиционную коммерческую компанию, её баланс резко вырос благодаря нескольким раундам крупного финансирования. В настоящее время Microsoft владеет 27% акций этой компании-лидера в области ИИ. Поскольку OpenAI ищет новое финансирование с оценкой более 7500 миллиардов долларов, первоначальные инвестиции Microsoft в 14 миллиардов долларов принесли ошеломляющую бумажную прибыль.

Это "экосистемное маховичное колесо, где левая нога наступает на правую", становится всё сложнее: конкурент Anthropic только что пообещал в будущем закупить вычислительные мощности Azure на сумму 30 миллиардов долларов, а Microsoft сразу же планирует инвестировать в него 5 миллиардов долларов. В этой потенциальной сделке оценка стартапа уже взвинчена до 3500 миллиардов долларов.

В итоге, испарившаяся рыночная капитализация Microsoft в 3570 миллиардов долларов — это коррекция рынка её модели "тяжёлого капитала, медленной монетизации". Хотя бухгалтерская инвестиционная прибыль (Paper Gain)极其丰厚, Уолл-стрит на самом деле волнует не то, сколько Microsoft заработала на оценке как "венчурная компания", а то, сможет ли её核心云业务 в условиях подрыва затрат на оборудование真正从全球企业身上收回真金白银 (получить реальные деньги от глобального бизнеса).

В данный момент индустрия ИИ похожа на高速行驶的列车 (поезд, движущийся на высокой скорости):一旦铺开便难以停下 (инфраструктуру,一旦развёрнутую, трудноостановить), а能否在保持速度的同时逐步实现商业闭环 (возможностьпостепеннореализоватькоммерческоезамыкание, сохраняяскорость),将决定下一阶段的市场定价逻辑 (определитлогикурыночногоценообразованиянаследующемэтапе).

Автор: Bootly

Twitter:https://twitter.com/BitpushNewsCN

比推 TG 交流群:https://t.me/BitPushCommunity

比推 TG 订阅: https://t.me/bitpush