Author: Damir Tokic, Finance Professor, Seeking Alpha Analyst

Led by technology stocks, the S&P 500 is approaching its highest historical valuation, signaling the formation of a massive bubble. Simultaneously, the war in Iran is highly likely to trigger an inflationary shock, leading to a surge in oil prices and higher U.S. Treasury yields. The escalating situation seems to be increasing the probability of this pessimistic prediction becoming a reality. Despite the Fed maintaining a dovish official bias for now, the market has already begun pricing in rate hikes. Therefore, the Fed's official shift to a hawkish stance in June could very well serve as the catalyst that pricks this bubble.

President Trump attending the swearing-in ceremony for the new Federal Reserve Chair

Does the Ceasefire Only Benefit Tech Stocks?

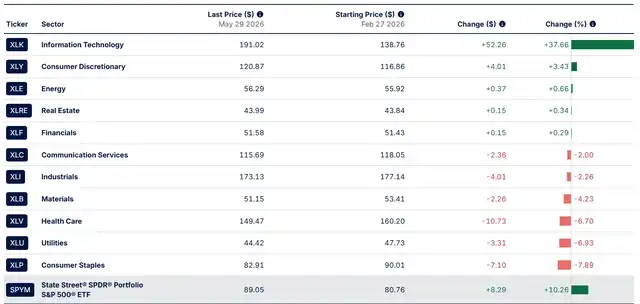

The following shows the performance of the S&P 500 Index (SPY) over the past three months since the outbreak of the Iran war:

-

Since February 27, the S&P 500 has risen by 10%.

-

The Technology sector (XLK) has gained over 37%.

-

The second-best performer is the Consumer Discretionary sector (XLY), which rose only 3%. It's important to note that Amazon (AMZN) constitutes 27% of XLY's weighting, and its stock price has increased by 28%; Tesla (TSLA) constitutes 20% of XLY's weighting, and its stock price has risen by 8%. Both companies are essentially tech firms and members of the "Magnificent 7" (Mag 7).

So, what is the core issue now? Did the ceasefire in the Iran war provide an absolute benefit only to the tech sector, especially semiconductors (SMH)?

In my view, the answer is no. The market has blindly assumed the war is over. More importantly, it assumed we could escape an inflationary shock and the demand-destroying recession that would follow. Therefore, this became a green light for speculators to go on a rampage, re-inflating the bubble.

However, it must be pointed out that the current bubble is not like the 2000 dot-com bubble. That bubble was driven entirely by expectations and the uncontrolled expansion of P/E multiples. The 2026 bubble is much worse! It is built on "backward-looking" realized profits and the naive expectation that these profits will continue indefinitely. Specifically, the mega-cap companies have poured $770 billion into AI capital expenditures. Clearly, these profits are concentrated in the primary beneficiaries of this spending, mainly semiconductor companies like Micron Technology (MU).

However, the Shiller P/E (CAPE) ratios for 2000 and 2026 are almost neck and neck, both remaining above 40x. This means the severity of the 2026 bubble is already on par with that of 2000.

But, the profits of the tech giants cannot be sustained indefinitely. AI capital expenditure growth is likely to slow and eventually decline. When will this tipping point occur?

In my opinion, this $770 billion in AI capital expenditure can be traced back to that meeting between tech executives and President Trump early in his second term. At that meeting, President Trump, sitting next to Mark Zuckerberg, asked him how much Meta planned to spend on AI capex. Zuckerberg replied, "Sorry, I'm not prepared... I'm not sure which number you want."

Therefore, I believe that this $770 billion AI capital expenditure is essentially a 'Trump stimulus' imposed on the private sector, and it is unsustainable. If Democrats win the upcoming midterm elections, this trend is likely to reverse.

Thus, the market's euphoric reaction after the Iran war ceasefire is just part of the 'Trump stimulus' and likely represents a final blow-off rally. The question now is, where is the peak of this surge, and what will trigger the crash?

SPY Sector Performance (Data Source: SSGA.COM)

Iran War Escalation and Inflationary Shock

Now let's shift our focus back to the Iran war. This is a crucial variable because it has a high potential to trigger a classic systemic shock that could completely pop the bubble.

A classic bubble burst typically follows this trajectory: 1) Inflation accelerates, 2) The Fed raises interest rates, 3) A recession triggers a bear market.

Let's first examine inflation. Inflation can be demand-driven or supply-driven.

Demand-driven inflation is initially favorable for the market because businesses have pricing power, often accompanied by an "overheating" economy where companies initially see revenue and profit growth. The Fed then curbs demand by raising rates, but this ultimately leads to higher unemployment and a recession.

In contrast, supply-driven inflation is significantly negative for the market from the outset because businesses lose pricing power—this often occurs in a weak or stagflationary economic environment. The Fed is forced to raise rates even as the economy is weak, inevitably leading to a deeper recession.

The Iran war is triggering a destructive supply-side inflation because it is causing a global energy shortage, as well as food shortages due to fertilizer shortages and many other derivative product and chemical shortages.

Fundamentally, Iran has closed the Strait of Hormuz, and this closure has persisted for three months. During these three months, the global economy has been tapping strategic petroleum reserves to fill the lost oil gap. These reserves are expected to reach critical operational levels in June.

If Iran does not immediately reopen the Strait of Hormuz, the global economy will face its most severe energy shock ever. Due to the very real physical shortage, crude oil prices could surge to over $200 per barrel until demand is completely destroyed, leading prices to fall back down. The destruction of demand directly corresponds to a recession.

This is precisely why Trump is acutely aware of the severity of the situation. For the past two months, he has been trying to negotiate with Iran to reopen the Strait of Hormuz but to no avail.

Currently, reaching a deal with Iran seems almost impossible for three reasons:

-

First, Iran wants to retain control of the Strait of Hormuz even after reopening it, which crosses a U.S. red line;

-

Second, Iran refuses to negotiate on the nuclear issue and most likely does not want any nuclear deal, which is another U.S. red line;

-

Third, even if Trump compromises on Iran's terms to reopen the strait and reaches some deal, Israel would likely block it, as Israel sees a nuclear-armed Iran as an existential threat.

So, what is the actual situation on the ground now?

My take is that Trump's likelihood of striking a last-minute deal with Iran to prevent an inflationary shock is becoming increasingly higher.

However, Israel absolutely does not approve of such a deal. Because part of an Iran deal would involve a ceasefire on all fronts, including Lebanon. Israel could outright veto this deal by directly attacking Lebanon. For Israel, this is also an existential issue, given the very real threat posed by its neighbor, Hezbollah.

Currently, we are facing a potential for major escalation.

Reports indicate Iran has now severed all contact with the U.S., meaning all negotiations have stalled. Not only that, but Iran has also completely blockaded the Strait of Hormuz and is threatening to further close the Bab al-Mandab Strait. If this happens, over 30% of the world's energy supply would simply vanish—a true disaster.

Although Trump claims he has spoken with both Israel and Hezbollah, and even suggests negotiations with Iran are still ongoing—and just these statements have been enough to push tech stocks to new all-time highs—there has been no official confirmation of these claims to date.

The June Crash

Therefore, the probability of a crash erupting in June is becoming increasingly high. Global oil inventories will hit critical levels in June. Once they fall below that line, crude oil (CL1:COM) prices will skyrocket due to a real supply shortage, and it will become very difficult to "talk down" prices with mere words.

The consequence will be that bond yields will also soar as inflation expectations rise and fiscal concerns drive real rates higher. Moreover, when inflation spikes, trying to 'jawbone' the bond market sell-off will become futile.

Most crucially, the Federal Reserve will have to respond at its June FOMC meeting. This could very well be the final trigger that pops the bubble. Specifically, the Fed's official stance in its Summary of Economic Projections (SEP) still signals that the next move will be a rate cut, maintaining a dovish policy bias.

However, the federal funds futures market has already priced in a tightening bias. Currently, the market is pricing in over a 50% probability of one rate hike by December 2026, and potentially even two hikes.

The Fed will then be forced to align with market expectations, making an official hawkish shift at the June meeting. This alone could burst the bubble instantly. Furthermore, even if the Fed insists on maintaining a dovish bias, as it would completely lose market credibility, the 10-year Treasury yield could skyrocket, triggering an even greater systemic shock.

Investment Implications

The S&P 500's Shiller P/E ratio is approaching a new all-time high, well above 40x, forming a mega-bubble. An inflationary shock triggered by the Iran war could pop it at any moment, and the Fed's official pivot to hawkishness in June might be the fatal bullet. Investors should prepare for a major pullback, potentially as severe as the bear markets of 2000 and 2008. Remember, all bubbles eventually burst.