Author: Curry, Deep Tide TechFlow

How frenzied has the South Korean stock market become recently?

The KOSPI rose from around 4,000 points to nearly 8,000 points in six months. According to a report in the "JoongAng Ilbo," the employee restrooms in a department store in Seoul's Gangnam District are completely full every day at 3:30 p.m., the market close time, with employees hiding inside to check stock prices.

By mid-May, the balance of loans taken by Korean retail investors from securities firms for stock trading had surged to a historic high of 36.47 trillion won (approximately 170 billion yuan), doubling within a year.

But in this carnival, the source of the money is a bit odd.

According to a report in the "Korea Herald," the three major life insurance companies in South Korea saw policy surrenders totaling 4.9 trillion won (approximately 230 billion yuan) in the first quarter, a year-on-year increase of 16.3%. Savings-type life insurance policies were surrendered the most aggressively, up 23.2%.

Savings-type life insurance is inherently a product for leaving money to family. Surrendering a policy guarantees a loss, as the surrender value is lower than the premiums paid. Yet, more and more people are choosing to take a loss and surrender their policies.

Where does the withdrawn money go? Most likely, into another stock trading account.

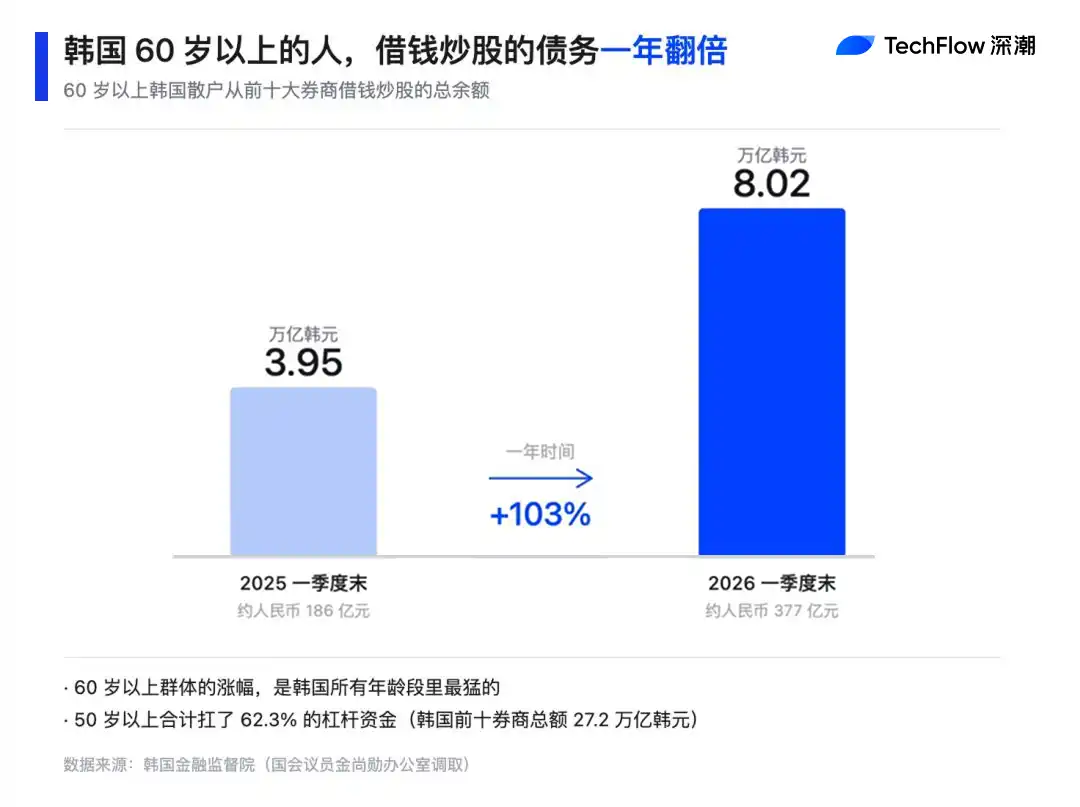

Data obtained by a South Korean lawmaker from the Financial Supervisory Service shows that as of the end of the first quarter, retail investors borrowed 27 trillion won from the top ten securities firms for stock trading. Of this amount, over sixty percent (62.3%) was borrowed by people aged 50 and above.

The debt of the group aged 60 and above doubled in one year, from 3.95 trillion won to 8.02 trillion won, the sharpest increase among all age groups.

Withdrawing insurance to buy stocks—an entire generation of South Koreans is using future money to chase the current bottom.

Borrowing Because of the Crazy Bull Market?

Adding leverage in a bull market is called "amplifying returns"; adding leverage in a bear market is called "accelerating to zero." Korean seniors have already experienced this roller coaster once.

In early March of this year, joint U.S.-Israel airstrikes on Iran caused panic in global capital markets. The South Korean stock market triggered circuit breakers for two consecutive trading days, with the KOSPI plunging nearly 13%.

According to a late March report by the Financial Supervisory Service of South Korea, during that downturn, among the nation's 4.6 million retail investor accounts, those who used margin loans lost an average of 19%, while those who didn't lost 8.2%. Those who borrowed to trade stocks lost 2.3 times more than those who didn't borrow.

Breaking it down by age group, the leveraged account holders aged 60 and above suffered the worst, with an average return rate of -19.8%, the lowest among all age groups.

What's even harsher is what comes next: forced liquidation.

Leveraged accounts have a liquidation line. If the market value of the stocks in the account falls below this line, the securities firm won't consult with you; they will directly sell your positions. The Financial Supervisory Service received numerous complaints from retail investors at the time, such as "My stocks were sold without my knowledge" and "I was charged exorbitant interest rates."

A significant portion of these complaints came from the elderly, who were already unfamiliar with trading rules. However, it must be said, the retail investors who held on during the March circuit breakers ultimately won.

The Korean stock market recovered all those losses in just over two months and has been rising ever since. Those who held on through March have seen their accounts fully recover, with some possibly even making money.

There was volatility, there was room for an uptrend, so this became a successful experience of "getting on board," even if it meant getting on board with borrowed money.

Thus, this success story becomes the excuse for the next, bolder move. After the March circuit breakers, margin lending to South Korean retail investors not only didn't shrink but kept rising. Public data shows that the total margin loan balance hit a record high of 25 trillion won by the end of April; by mid-May, it had surged further to 36.47 trillion won.

In just a month and a half, South Korean retail investors collectively borrowed an additional 11 trillion won (approximately 52 billion yuan).

Looking at individual cases. In early May, a South Korean civil servant posted a screenshot on the Korean workplace community Blind:

Their account showed 2.3 billion won (approximately $1.7 million) all-in on SK Hynix, with 1.7 billion of that borrowed from a securities firm. In other words, their own capital was 600 million won, leveraged by 1.7 billion in borrowed funds.

Four days later, they updated that they had already made 267 million won.

On the same day, another post from a woman in her 20s working for Seoul Metro said she would rather "go completely bust" than miss this wave, going all-in on SK Hynix with 150% margin financing. Borrowed money was used as principal to borrow yet again.

Such posts are discussed daily on the Korean Blind community.

The regulators are not unaware of this FOMO frenzy. At the end of March, the Financial Supervisory Service summoned major securities firms to strengthen risk controls, and some brokerages temporarily restricted new margin loans for overheated stocks. But the money already lent out remains there, accruing interest daily at annual rates ranging from 7% to 9%.

Calculating at an 8% interest rate, South Korean retail investors collectively pay nearly 3 trillion won (approximately 14 billion yuan) in interest to securities firms annually.

However, leveraging at 60 is a different matter from leveraging at 30. A 30-year-old who gets wiped out still has decades of salary to slowly recover. A 60-year-old who gets wiped out potentially loses their entire pension, with only exhausted physical strength and the reality of being unable to earn more left.

If another circuit breaker hits, the outcome might not be "a full recovery in just over two months."

In Tapgol Park, the Flowing Intelligence Among the Elderly

Like all Korean retail investors, the elderly in Korea are borrowing and betting on Samsung Electronics and SK Hynix.

Samsung Electronics is up 138% year-to-date, SK Hynix is up 189%. The KOSPI as a whole is up about 80%, but excluding these two companies, the remaining stocks have gained only about 30%.

These two companies together account for over 43% of the weighting in the KOSPI index. This means that as long as these two rise, the entire Korean stock market rises.

Most of the money borrowed by the elderly flows here. A quarter of the net purchases by Korean retail investors this year went into these two companies. The remaining three-quarters are scattered across other stocks, but the overall gain for those other stocks this year is only 30%.

There's Tapgol Park in Jongno District, Seoul, one of the city's oldest public parks. Young people rarely visit. Its regulars are a group of retired seniors who come to the park every morning, drink free coffee, chat, play board games—time seems to flow as slowly as if it were standing still.

According to a report by the "Kyunghyang Shinmun," the topics of conversation in Tapgol Park have changed this year.

Amidst coffee drinking, someone might say, "My Samsung stocks went up again." During a board game, someone might ask, "Did you buy Hynix?" A 77-year-old gentleman told his middle school classmates that Samsung and Hynix have been performing well lately and that he had made a bit in his account.

A corner of Tapgol Park, gathering many elderly people playing board games

Source: Seoul News

However, he didn't mention whether he borrowed money or how much he borrowed.

Topics popular among seniors in the park don't come out of thin air; they resemble intelligence exchanged at the village entrance station. For instance, an elderly person hears another senior made money in the park and checks their own account the next day. Then they start trying to borrow a little. And then potentially borrow more and more.

But if you ask why South Korean seniors are appearing in leveraged stock trading accounts, this is actually related to their retirement security.

According to OECD data, the relative poverty rate among South Korea's population aged 65 and above is about 40%, the highest among OECD member countries. The replacement rate of the National Pension (South Korea's version of a pension) has long been low. The OECD average is around 50%, while South Korea's is only about 31%.

Conversely, the labor force participation rate of those aged 65 and above is the highest among OECD countries, meaning a significant portion of South Korean seniors have to continue working after retirement.

Therefore, the availability of free coffee in places like Tapgol Park is essentially a form of social relief in South Korea. A cup of coffee costs less than 500 won. For seniors with a monthly pension of less than a thousand dollars, this is part of daily life.

But the elderly in Tapgol Park are no longer just there for free coffee and board games. They might also have the KOSPI行情 open on their phones.

After taking office, South Korean President Lee Jae-myung has been vigorously promoting全民炒股 (全民炒股 - mass participation in stock trading). He has publicly called himself the "Great Ant," where "ant" is a common nickname for retail investors in Korea. He set a KOSPI突破 5000点 as an administrative goal.

In other words, to some extent, the elderly borrowing to buy stocks is officially encouraged in South Korea.

What the elderly are truly betting on is an anxiety. If they don't get on board now, they will miss out.

This is their last chance before retirement. The South Korean semiconductor industry is cyclical, having experienced more than one boom-to-bust roller coaster over the past three decades.

SK Hynix reported a loss of 4.26 trillion won in 2023, its worst performance in a decade. Switching from massive losses one year to an operating profit margin of 72% in a single quarter two years later (surpassing Nvidia)—the speed of this cyclical shift itself serves as a reminder that the cycle might switch back again.

And time, perhaps, is the most precious thing for these elderly individuals borrowing to trade stocks.

The elderly in Tapgol Park are striving to seize the红利 of this era. The coffee is still free. The行情 on their phones hasn't stopped for a moment.