Original article by Circle Founder Jeremy Allaire

Compiled by| Odaily Planet Daily Qin Xiaofeng(@QinXiaofeng 888 )

Editor's Note: On July 13, Circle founder Jeremy Allaire published a research paper titled "The Agentic Economy," exploring the convergence of AI Agents with future economic systems. Allaire stated that as AI Agents begin to take on corporate work, and value natively flows through open, programmable networks, the Agentic Economy and the Onchain Economy will ultimately become two sides of the same economic system.

"This treatise is the culmination of my decades of work building internet infrastructure, and it crystallizes a question I've focused on from the very beginning: how open software and open networks can reshape not only how we share information but also our social, political, and economic landscape. Many of the ideas in the paper stem from two core beliefs that emerged when I founded Circle. First, money can flow via open protocols just like information flows on the open internet. Second, blockchain is a network computer: it's a foundational platform where autonomous software and machines can store value, exchange value, and coordinate economic activity directly, without human intervention." Allaire explained the motivation behind his research.

He added that these initial ideas have been refined over time, culminating in a deeper understanding of how financial and economic systems merge with software and the internet. As this fusion converges with the emergence of truly powerful AI and agent systems, this theory has expanded further: it not only describes a new type of currency or network, but a fundamentally new mode of economic operation, and the impact of this mode on humanity, labor, capital, ownership, and the new social contract. This is precisely what this book aims to explore.

The original paper is 89 pages long. Those interested can download and read the full text:https://agenticeconomytreatise.com/treatise/index.html; Odaily Planet Daily has compiled a summary of itskey points, enjoy~

——————————————

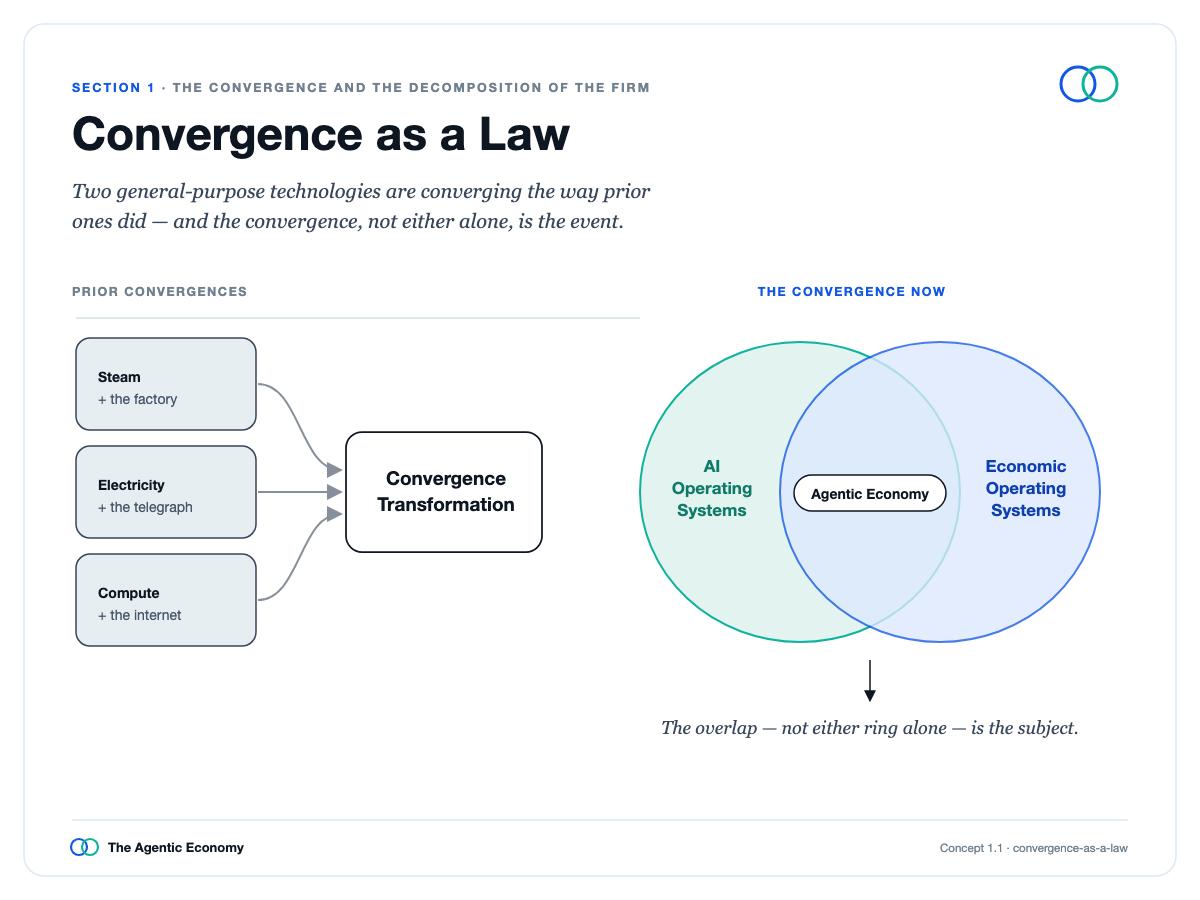

01 The Convergence and Deconstruction of the Firm

Every major shift in the internet era follows the same path: it doesn't stem from a single invention, but from multiple technologies maturing individually and suddenly converging. Networks, mobile, cloud, and social media are all examples of such convergence, repeating the same underlying pattern.

The Law of Convergence

When capabilities converge, things that were once expensive approach zero cost, and once cost is zero, the scale of that activity explodes. This has been true for information with networks, communication with mobile and social, and software with the cloud.

Today, two new systems are converging, directing the same force toward two areas the internet has never fully digitized: intelligence itself and the economy itself. The first is the intelligence system, comprised of AI models and the agents built on them, which is driving the cost of thinking and working toward zero. The second is the economic system, comprised of blockchains, where money, contracts, and coordination run as software, driving the cost of transacting toward zero. They empower each other, and the core thesis of this entire treatise is: these are not two parallel trends, but two sides of the same economy.

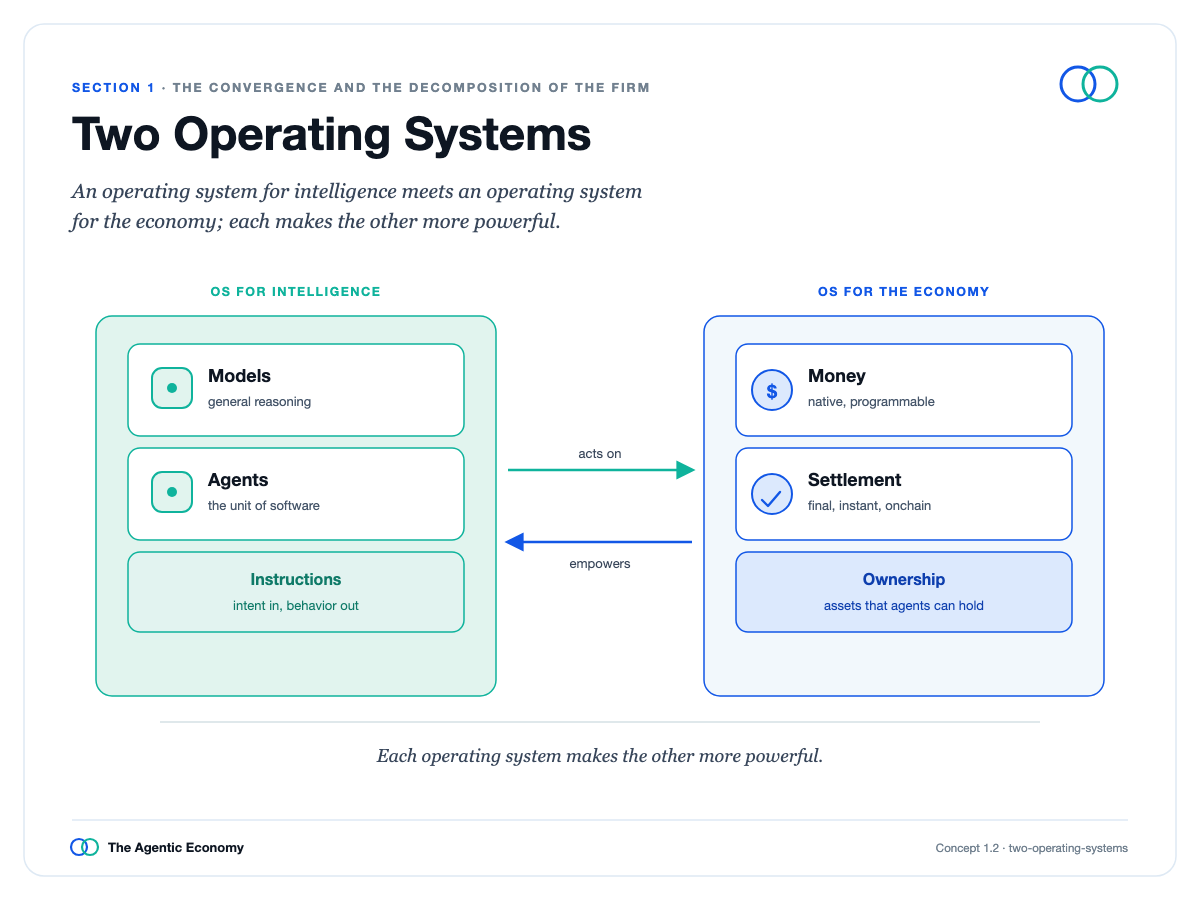

Two Operating Systems

The intelligence system is most critical because it changes the nature of software.

You no longer program; you issue instructions in natural language, and it reasons toward an answer rather than following fixed steps. Its basic unit is the Agent: a reasoning process to which you delegate a task. This shifts software from a program a machine executes verbatim to work you can delegate to a thinking machine, allowing the core tasks of a firm to be decomposed and reconstituted as skills an agent can perform.

Beneath the brand and the building, a company is essentially organized thinking: product, marketing, sales, finance, legal, plus the external firms it hires. These are almost entirely human labor, the largest cost in the economy, and exactly what cheap, powerful intelligence targets.

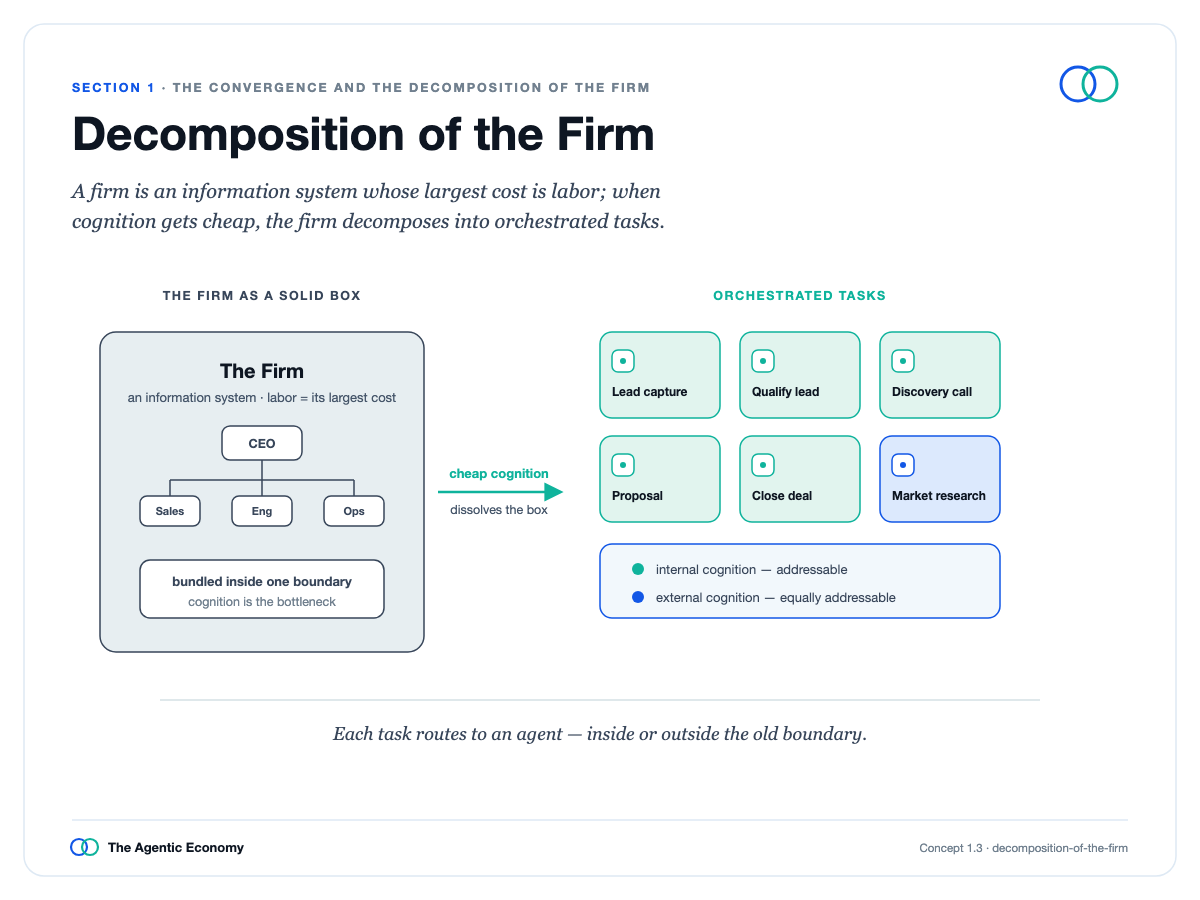

Firm Decomposition

It also upends traditional explanations for why firms exist. Firms grew because coordinating external work was costly, so they internalized it; when any non-physical work can be done by an agent you can find, hire, and pay instantly, that logic is weakened, and one person can do what once took a department.

It arrives first in software and other information-intensive work, slowest in physical realms, pending robotics breakthroughs. This isn't just about cutting personnel: one person paired with powerful agents becomes vastly more productive, while judgment, relationships, and ultimate responsibility remain human. This leaves a tension to explore later, addressed through ownership in the argument: even if the proportion of the economy paid to human labor declines, individual capability can be amplified.

Click to read Section 1:https://agenticeconomytreatise.com/treatise/section-1.html

02 Assembly, Coordination, and Why Firms Go Onchain

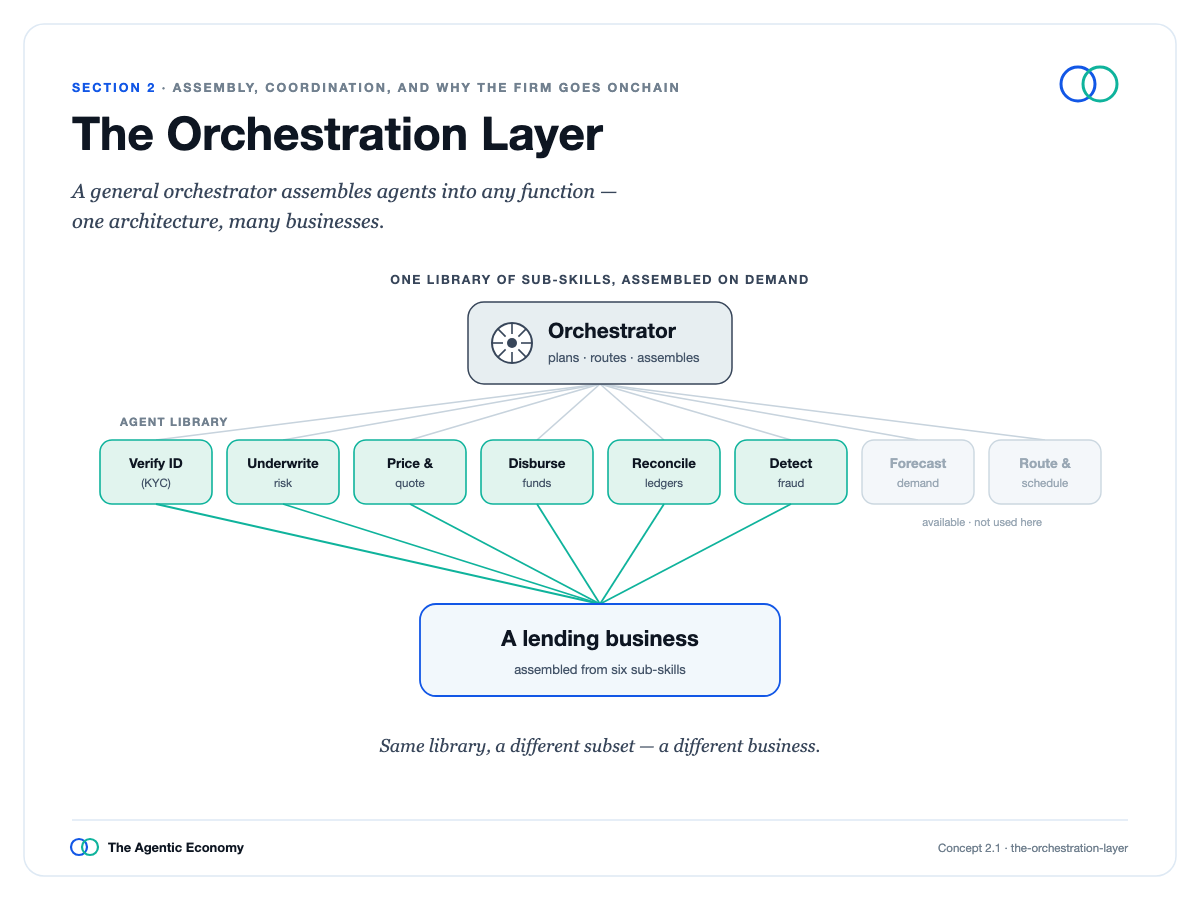

Once a firm is decomposed into skills, the real question isn't which can be automated, but how these pieces are put back together.

The answer is the orchestration layer: a General Manager Agent receives a goal, breaks it into tasks, assigns them to specialized agents, and stitches the results, with companion software passing context and memory between steps. The same mechanism applies to any function, so marketing, finance, sales, and product are essentially the same machine applied to different jobs.

Humans don't disappear. Some remain inside the loop, performing or checking work requiring human judgment. Others rise above the loop, setting goals, defining standards, monitoring quality, and deciding when the machine should stop and ask. This shift from doing work to overseeing work is the real form of human supervision, and the tools are arriving.

Orchestration Layer

When a company structures a task clearly enough to operate it internally, it's clear enough to be hired externally, so an open agent market forms almost as a byproduct.

This market could go two ways. It could evolve into a few large platforms selling intelligence like a utility, or, more likely and more interestingly, into a real labor market of specialized agents because deep expertise still holds value, and durable firms will be agents that specialize in one thing.

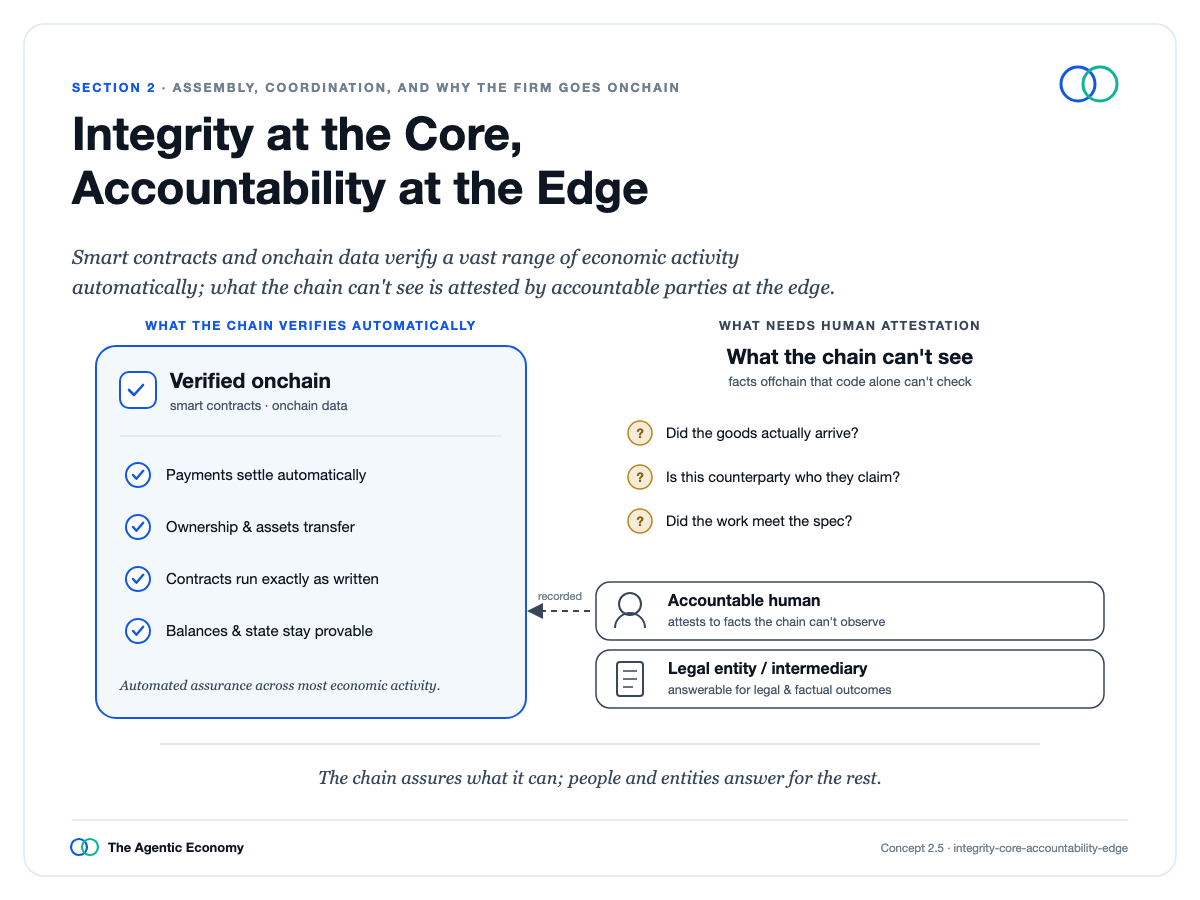

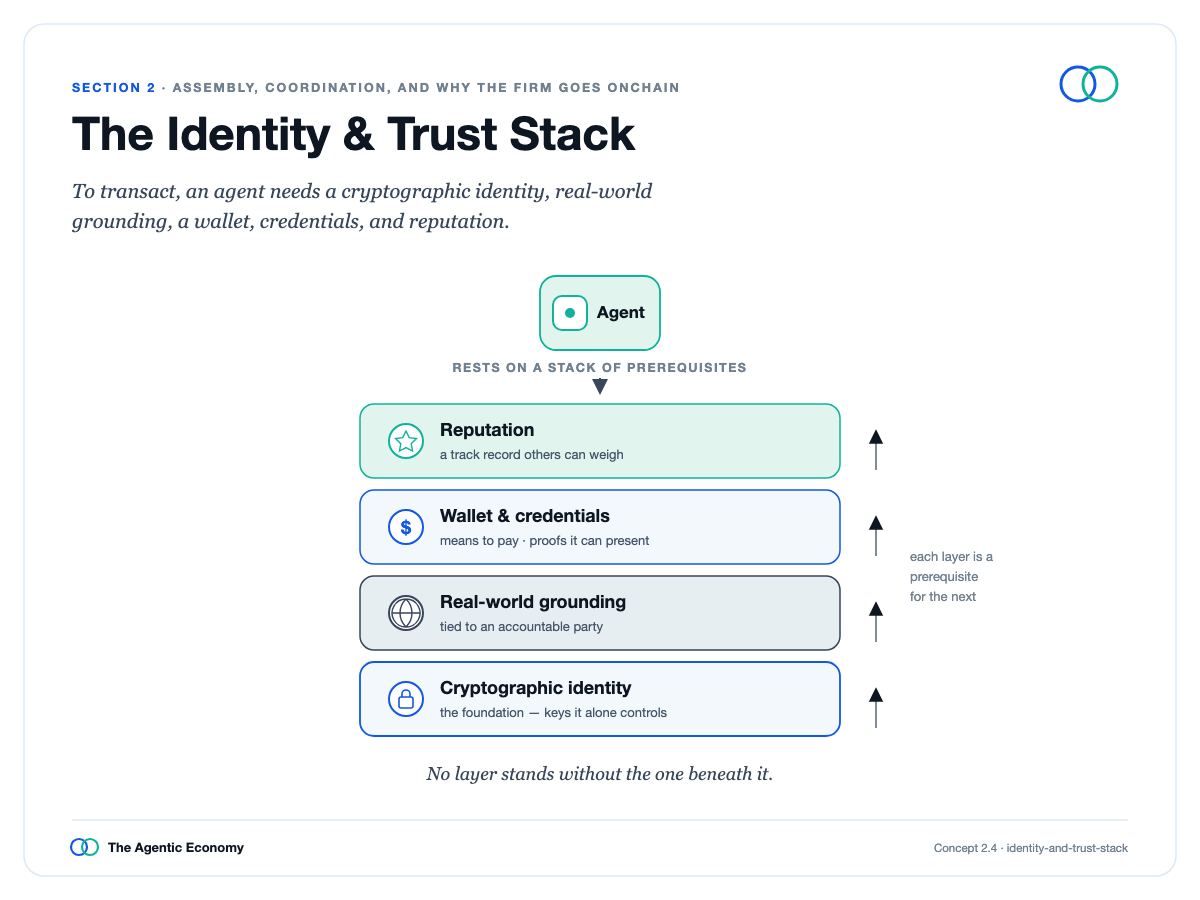

But hiring software assembled from anywhere in the world requires you to be able to trust it, and that's the problem pushing everything onchain.

The solution is layered identity. At the base, public blockchains verifiable by anyone. On top, real-world identity verification, the same run at scale by banks, the agent's own wallet and credentials, and reputation accumulated over time but tied to verified real creators. Together, these form a chain of accountability: every action by an agent can be traced to a real person or company responsible for it.

Integrity First, Accountability Throughout

A single company's private database can't do this because trust locked inside a single operator doesn't transfer, while identity rooted in public chains and real-world verification does. Thus, autonomy here is not anonymity. Behind an agent acting autonomously, there is always a person accountable for it.

Chain of Accountability

Click to read Section 2:https://agenticeconomytreatise.com/treatise/section-2.html

03 The Monetary Base: Speed, Safety, and Finality

Agents need money they can hold and move at machine speed, in any size, without stopping to verify the money itself is reliable with each payment. The last point is key, pointing to a classical answer: fully backed, settlement-final, money running on an open network.

Speed Replaces Leverage

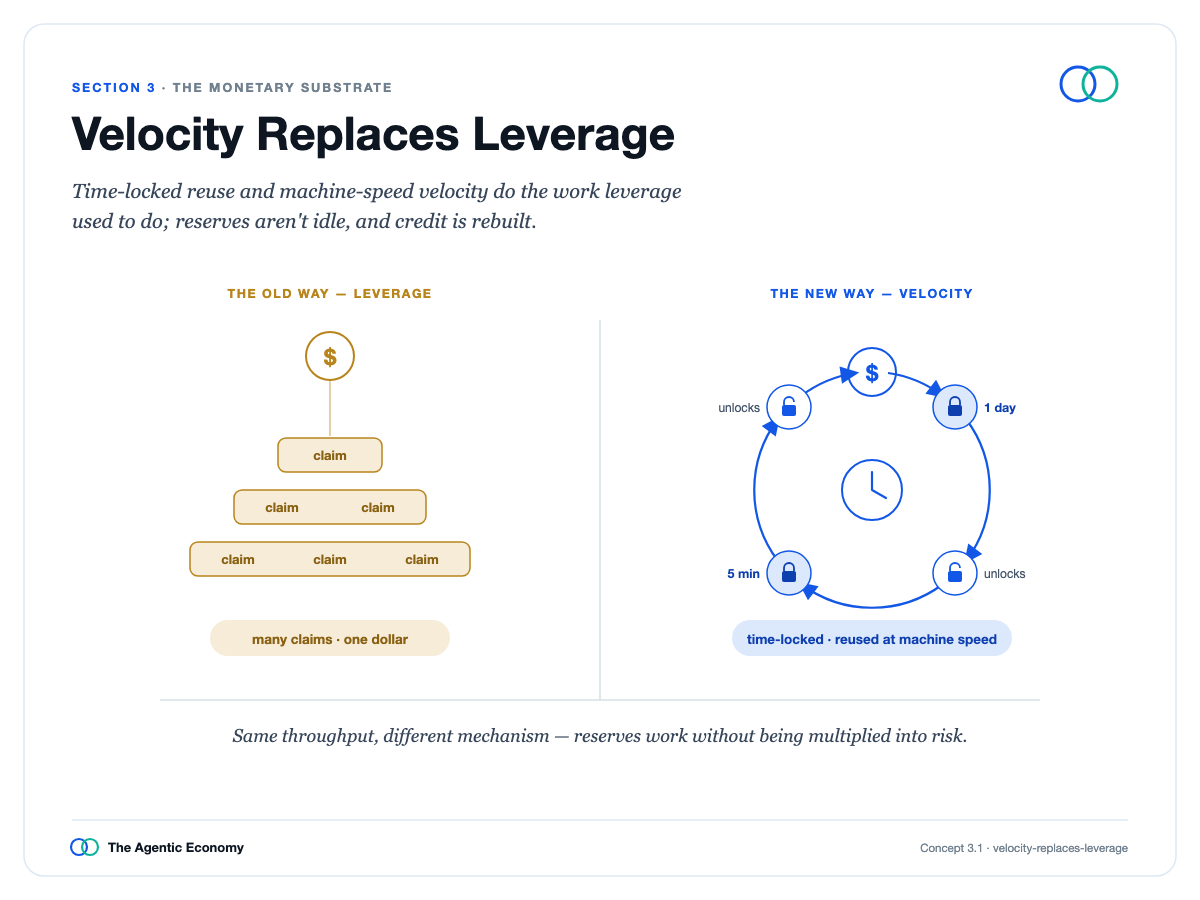

Start with speed because it reshuffles everything else.

When moving money costs nearly zero, settles instantly, and can be controlled by software, the same dollar can be reused many times in a short period, any amount can be spent the moment it arrives, and tiny payments between agents finally become viable. This is exactly the pattern information and software already follow on the internet, now extended to money.

Each part of the answer exists for a reason.

A natural objection is that banks create speed by lending out the same deposit repeatedly, so wouldn't full backing kill credit? No: when money turns over fast enough, a dollar can be locked for seconds and then lent, so speed plays the role leverage once did, and credit rebuilds on top, not canceled.

Why Base Money Should Not Take Risk

Why insist base money can't have any risk? Because speed makes risky money dangerous in proportion to how fast it moves. A bank run that once took weeks can now happen in minutes, and agents settling instantly cannot stop to judge if each dollar is sound.

Fully backed money is the only money worth exactly one dollar to everyone, everywhere, without relying on national safety nets that can't cover a global system. Settlement must be equally certain: not final after some time, but final within a second; settlement is settlement.

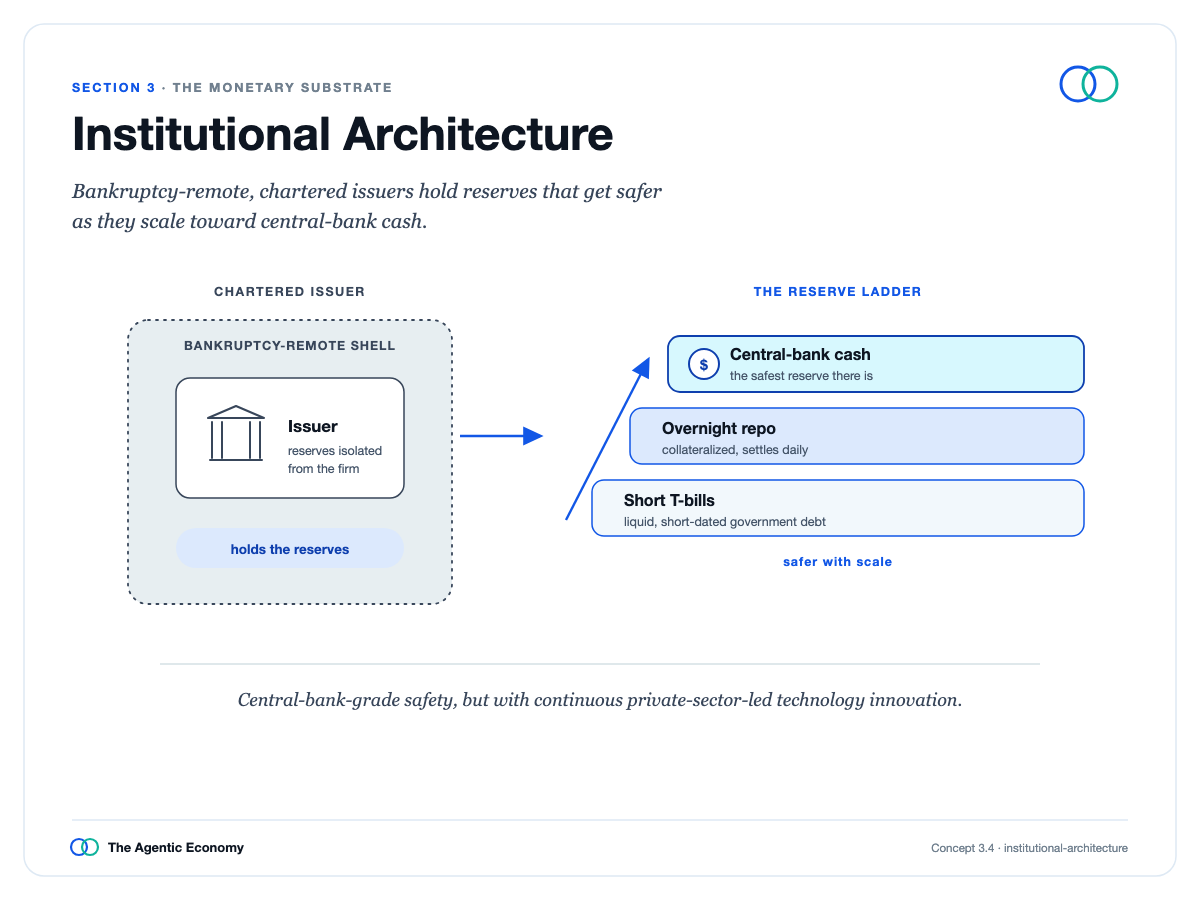

Institutional Architecture

Refunds and fraud protection still exist, but as optional layers built on top, like custody, refund pools, and insurance, not baked into the money itself. These safeguards don't apply automatically; they rely on real institutions being built, large regulated issuers with bankruptcy-remote structures and reserves secured in increasingly safe ways.

One line must be sharp: holding money earns no yield. Reserve earnings go to the issuer and flow into the ecosystem, but when you seek yield, you are no longer holding money but lending it and taking risk. Blurring the two collapses the entire safety argument.

Click to read Section 3:https://agenticeconomytreatise.com/treatise/section-3.html

04 Credit Markets: Machine Underwriting, Agent Working Capital, and the Prudential Layer

When base money is fully backed, credit doesn't vanish; it moves to the other side of that line and returns stronger, reaching more people, priced more precisely, and failing more visibly than the system it replaces.

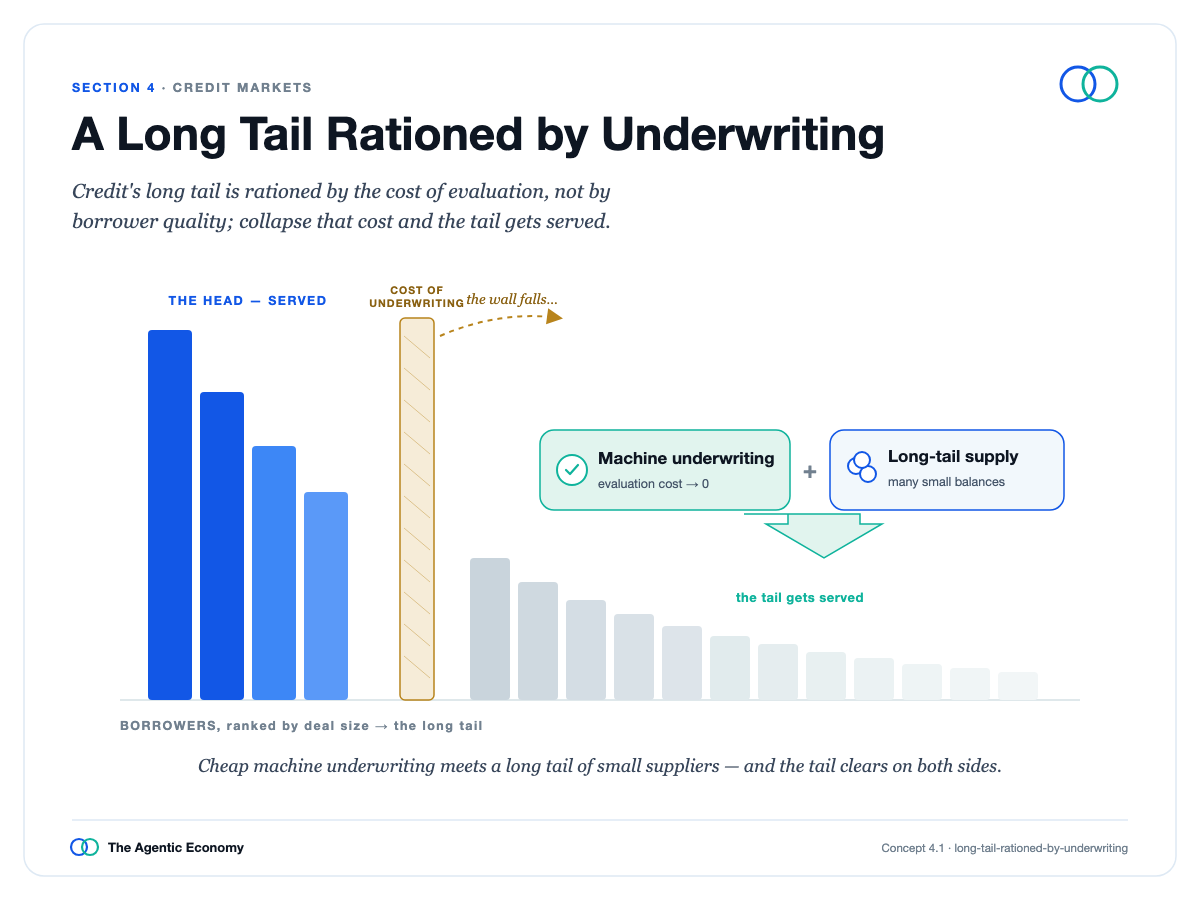

The Long Tail Under Underwriting Constraints

The key is reframing the problem. A huge number of borrowers—small businesses, gig workers, households, and now agents—are underserved not because they are risky, but because the cost of underwriting each tiny loan exceeds the loan's value. Credit rationing is driven by underwriting cost, not borrower quality. Lower that cost, and a whole population of creditworthy but neglected borrowers becomes servable.

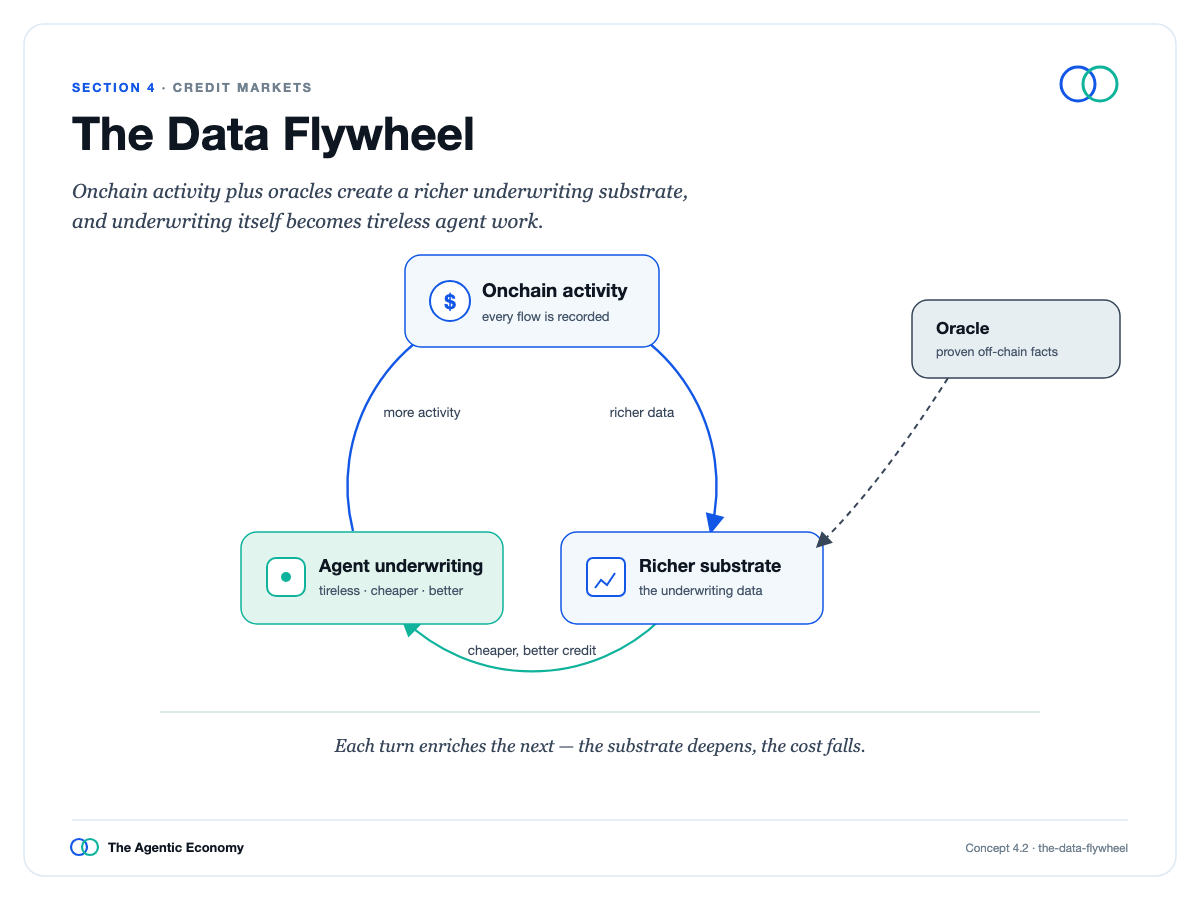

The Data Flywheel

What pushes the cost down is a data flywheel: onchain activity is structured, verifiable, and real-time, allowing risk models far better than the patchy records of the past; better data leads to better loans, which attracts more activity and more data.

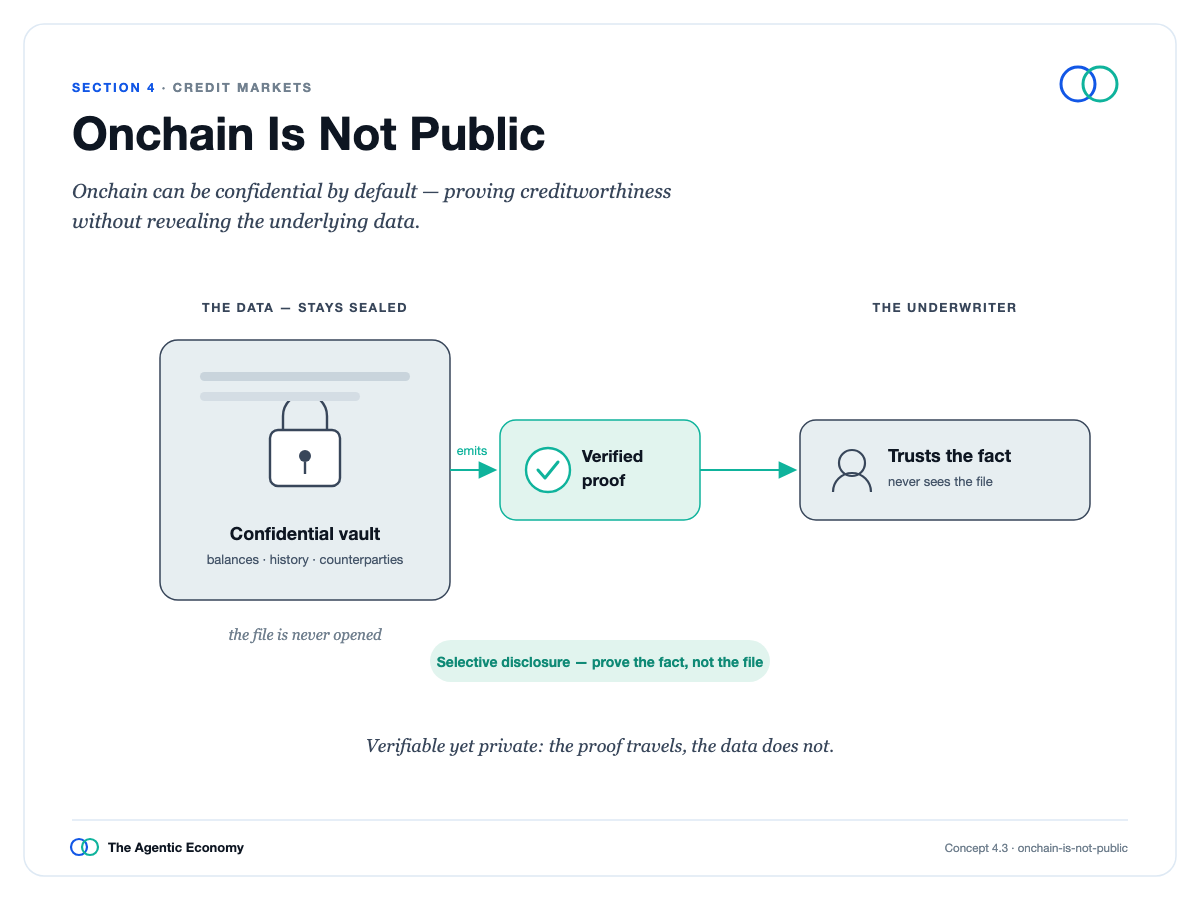

One naturally worries this puts everyone's finances on a public ledger, to which the answer is simple: onchain does not mean public. New privacy tech lets people prove what a lender needs to know—say, their credit standing or loan balance—without revealing the specifics.

Onchain Is Not Public

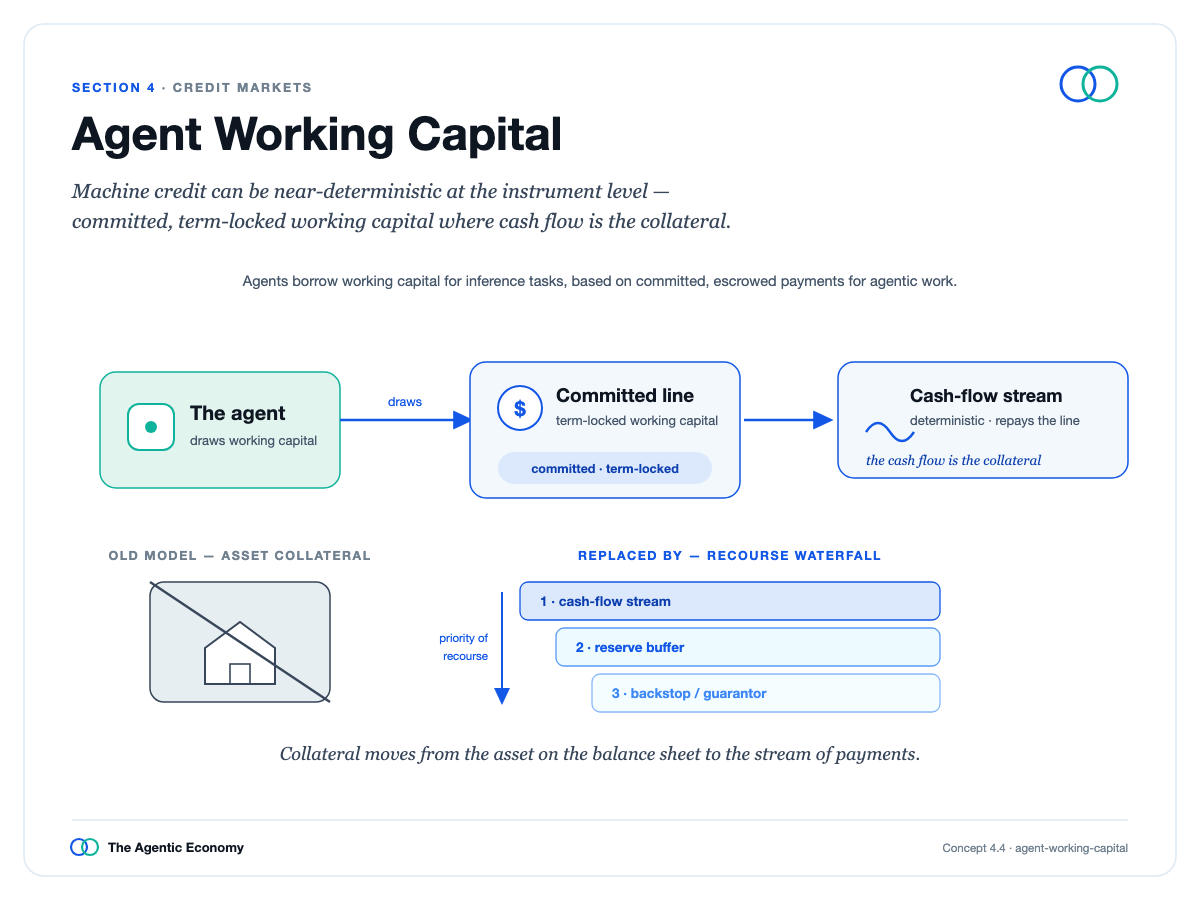

At the core is a genuinely new kind of loan: working capital for agents. It is exceptionally predictable because it removes the biggest variable in human lending—whether the borrower will choose to repay—collapsing risk to a short-cycle, bounded question about a specific piece of work.

Agent Working Capital

Imagine an agent borrowing four dollars of compute to finish a ten-dollar job it has already been hired for. The lender isn't guessing character; it is pricing the probability the work is accepted. Collateral flips the usual model: instead of slowly seizing unrelated assets through courts, the loan is first secured by the payment for the work itself, claimed automatically, backed by a deposit from the agent, its reputation, and ultimately the real person behind it.

The result is credit that is cheaper, more available, and simultaneously safer, which seems impossible until you realize the gain comes from better information, not more lending.

The honesty the claim requires is that this predictability wears off over time: tasks done in seconds are nearly mechanical, while financing over months reverts to ordinary risk.

Thus, machine credit does not replace human credit; it becomes a new low-risk baseline against which human loans are priced.

And, all of it is monitored: risk becomes visible as it accumulates, automatic brakes make piling into the same pattern or provider steadily more expensive, and insurance is priced on actuals, not stale averages.

Click to read Section 4:https://agenticeconomytreatise.com/treatise/section-4.html

05 Natively Global

The architecture comes in exactly three layers.

The bottom is money: stablecoins as unit of account and final settlement. The middle is the economic operating system: coordination, contracts, and value exchange run as programmable smart contracts with final settlement. The top is the agent execution layer: the actual work happens here, powered by AI and the cloud.

What matters about these three is where they live. Each is software; each runs on the internet. Each also displaces something once bound to nations: software money displaces national banking systems stitched together by slow correspondent banks; the middle layer moves contract enforcement from national courts to code that runs the same everywhere; agent execution replaces local labor with work that has no hometown.

An economy built on these layers is therefore borderless by default. This is what "natively global" means: not an added feature, but an inherent property of its materials. Historically, economic activity was national first, crossing borders took extra work; now, economic activity is global first, and the national frame is what gets added afterward.

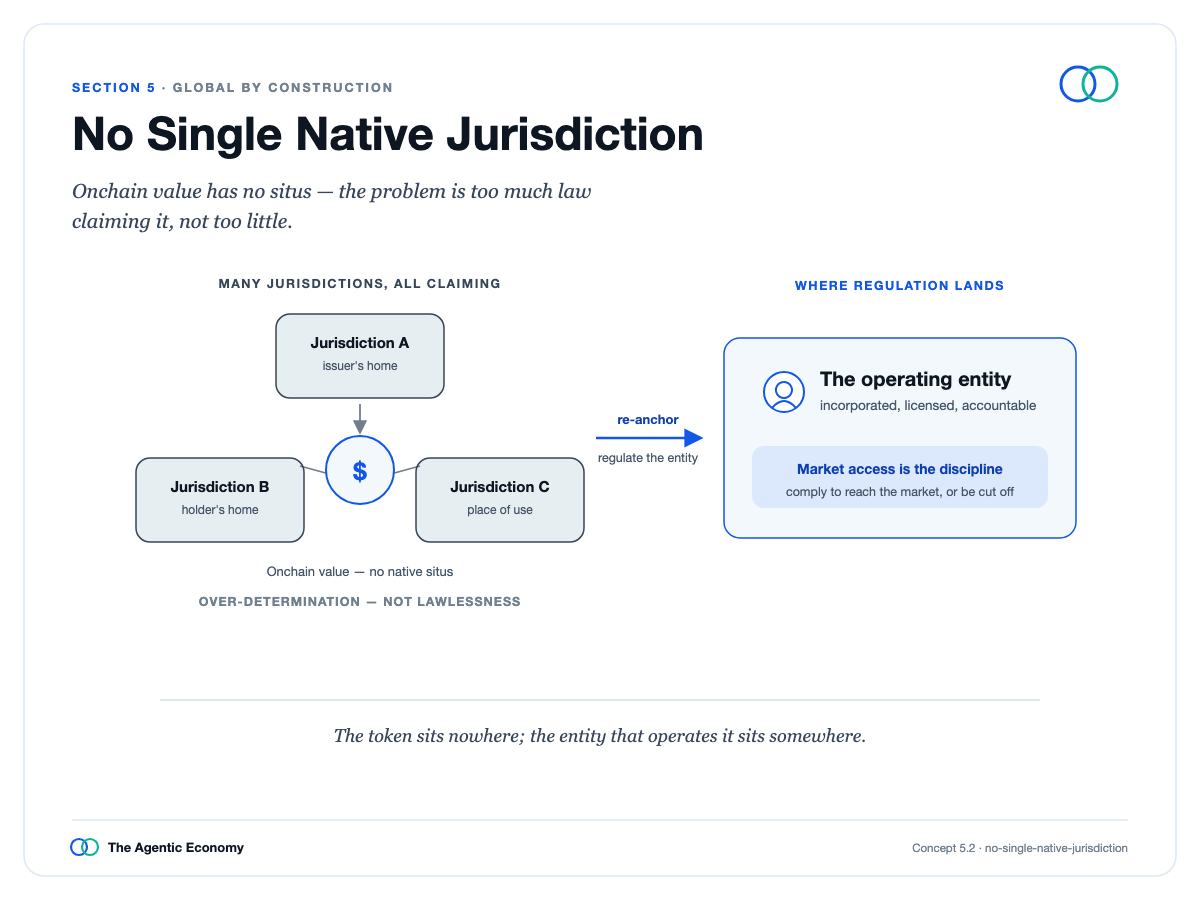

No Single Native Jurisdiction

An economy without a homeland does not escape law; it is subject to too many laws, with rules from many jurisdictions in conflict and no single place to decide which applies. The resolution shifts the question from "where did something happen" to "who is behind it," regulating the accountable entity each agent traces back to, while the country where the user actually lives sets conditions for market access.

Enforcement moves to the edge, where money and identity cross between the open world, the regulated world, and the private world, checking before payment settles, not reporting after clearing. This doesn't require a public ledger of everyone's finances: disclosure stays private by default, shared only with permission.

A healthy system also preserves a genuinely private space, the digital equivalent of cash, so control resides at the regulated edge, not the core. The most powerful tool—the ability to freeze or claw back funds—is only legitimate under real due process: recorded, time-bound, multi-party, and with appeal.

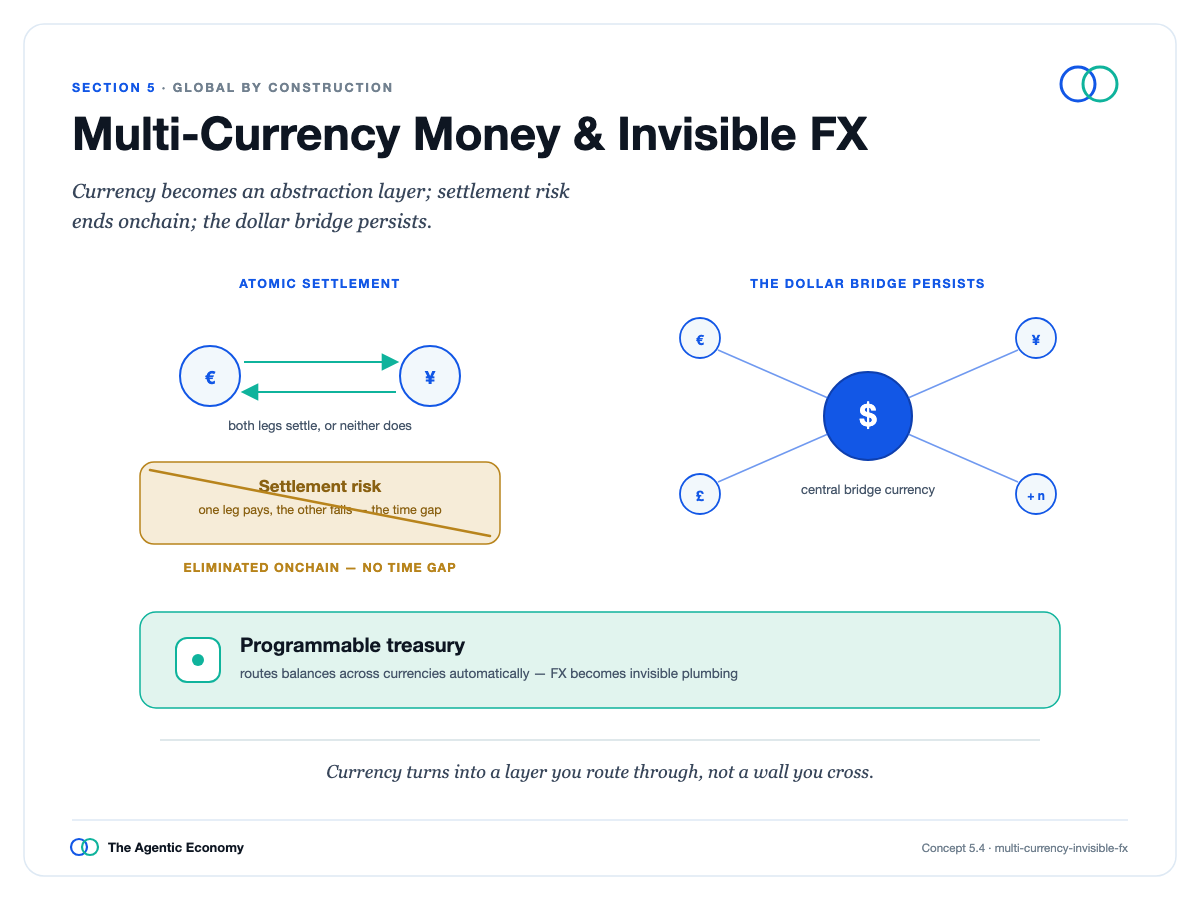

Multi-Currency Money and Invisible FX

Currency exchange also becomes invisible because as each major currency goes onchain, you hold yours, the other party gets theirs, and the conversion happens at the best rate underneath. Sovereignty is reshaped, not lost: a neutral network precisely lets a nation issue its own currency on the same rails, rather than depending on someone else's.

The real danger lies in the transition, not the endpoint, because people can flee weak currencies faster than ever, so it must be managed.

This economy has both equalizing and centralizing tendencies, concentration is the default, and broad sharing is the harder, buildable alternative. The same machine that can enforce accountability can also enforce censorship; the choice is ours.

Click to read Section 5:https://agenticeconomytreatise.com/treatise/section-5.html

06 The Supply Side: From Subscriptions to Consumption

The agent economy needs a supply side—services that agents can call, hire, and pay for—and it forms in two waves.

First, existing software and data wrap themselves for machines to use, priced for agents, not people. Second, new specialized agents are built, going deep in one domain and selling their work. The deeper shift is in pricing: value shifts from access to work output, resetting software businesses.

For three decades, software sold by the seat, charging periodic fees to people who log in. But the customer now is an agent performing tasks, so the purchase is the work itself, not the login. The seat dies as a billing unit, though subscriptions won't vanish; pricing reshapes around new units of work in multiple forms, from pay-as-you-go to committed budgets to pricing on delivered outcomes.

The same logic goes one layer down, and that's where the money flows.

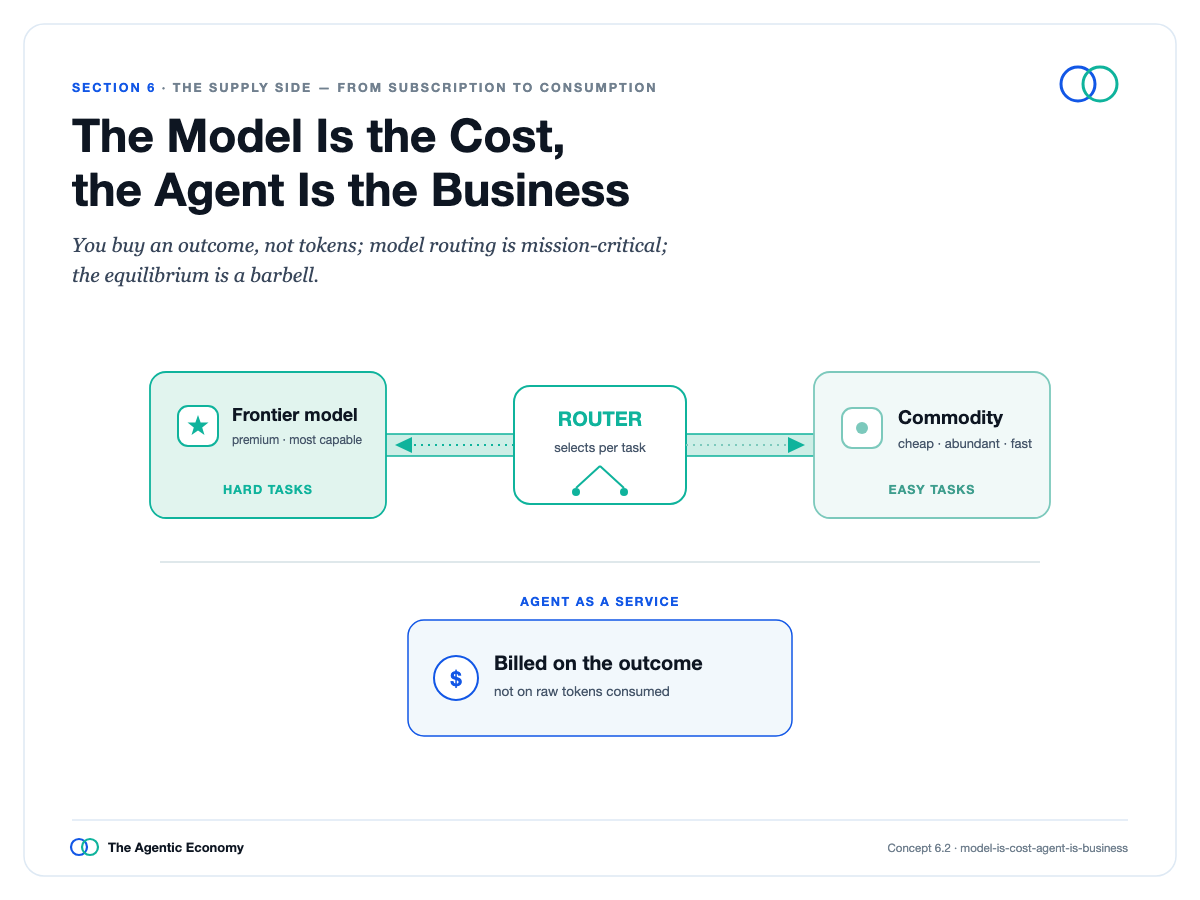

As specialized agents proliferate, what buyers purchase from agents is outcomes, not raw output from models, and agents will shop among competing models to complete jobs as cheaply as quality allows.

Models as Cost, Agents as Business

This is already happening: tools that route each request to the best model went from optional to essential within a year, price gaps between models are so large that using an expensive model for simple tasks is pure waste. Thus, models become cost items, agents become the business itself, and value flows to the party that owns the customer, the context, and the responsibility for results.

This is a tendency, not a law, because the makers of the very best models hold real pricing power on the hardest tasks and can move up into the agent layer themselves; the likely outcome is a barbell structure, with a large middle commoditized and the frontiers holding value.

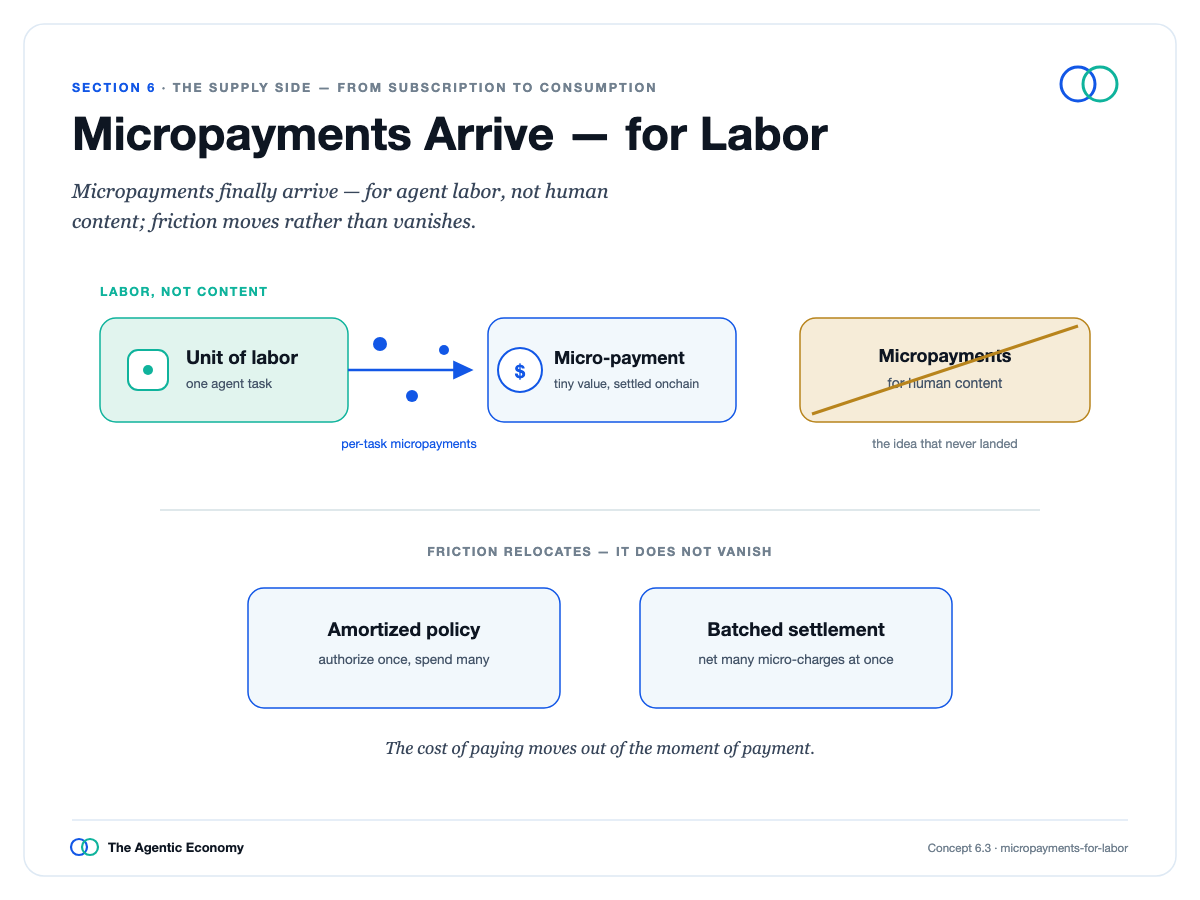

The Age of Micropayments for Labor Arrives

Below this, an old dream finally comes true: micropayments. They never took off on the consumer internet partly because settlement was expensive, but mostly because people hated deciding if every little thing was worth a penny.

Machines have no such hesitation, settlement is now near-free, so micropayments finally arrive, not for content, but for tiny units of work between agents.

The optimistic narrative misses one problem: if agents can hire other agents and tools on their own, spending can spiral out of control quickly, so the economy needs a spending control layer with caps, budgets, and approvals, itself becoming a product category, completing the vision rather than undermining it.

Click to read Section 6:https://agenticeconomytreatise.com/treatise/section-6.html

07 The Onchain Firm

As agents take on more and more of a firm's work, the firm itself needs a new home.

A company whose work is done by agents holding money, signing contracts, and acting 24/7 needs a place where that can actually happen: where money moves programmatically, rules run as software, and external transactions settle at machine speed. That place is the onchain economy.

Two Parallel Paths

Therefore, the agentic firm and the onchain firm are actually two sides of the same thing, one describing who does the work, the other describing the form the work takes. This is the core of the entire treatise: an economy run by software agents must run on software money, software contracts, and software governance, or it cannot function at all.

This does not mean—and this distinction matters more than any other—that every firm dissolves into a token-governed collective.

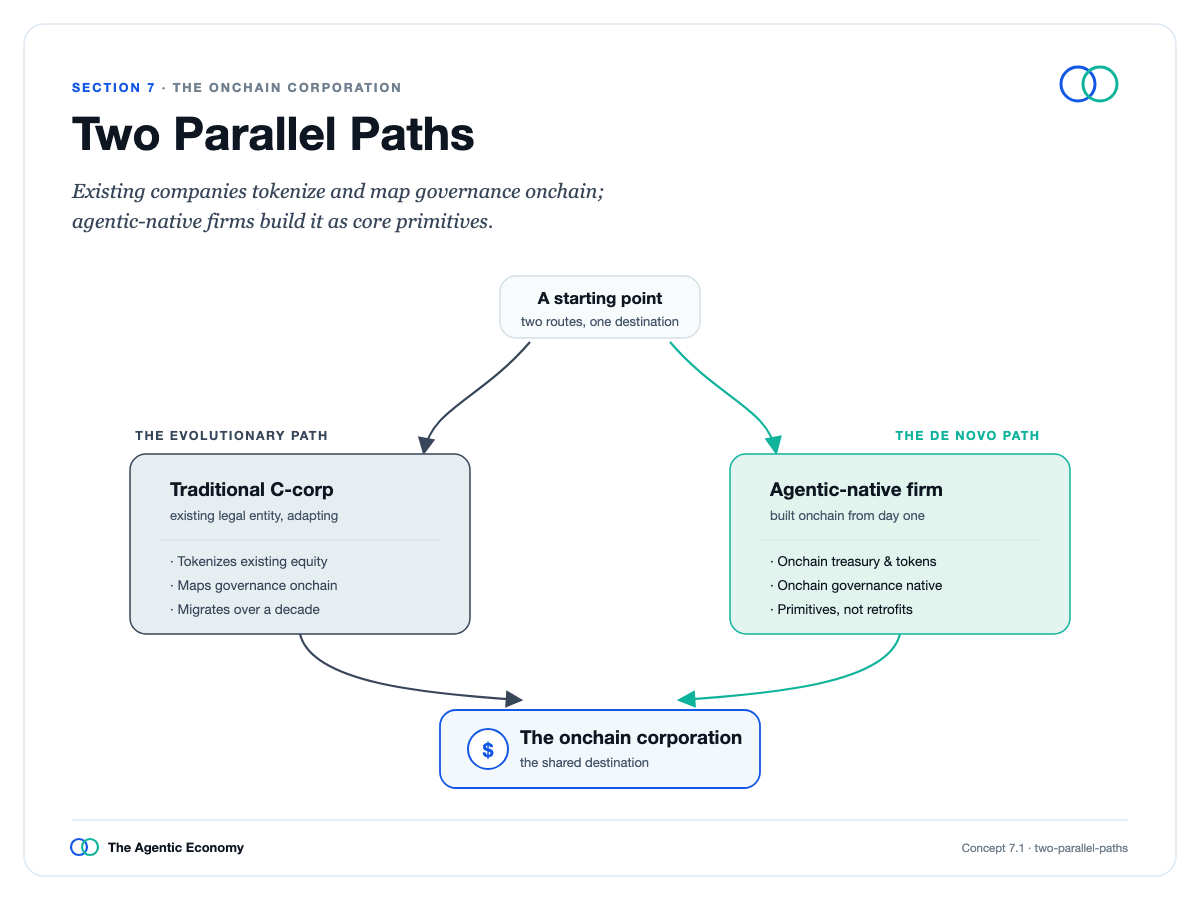

The future is a hybrid, advancing along two tracks.

On one track, existing firms gradually bring their shares and governance onchain while keeping their familiar legal forms, a slow change driven by the most cautious institutions in finance.

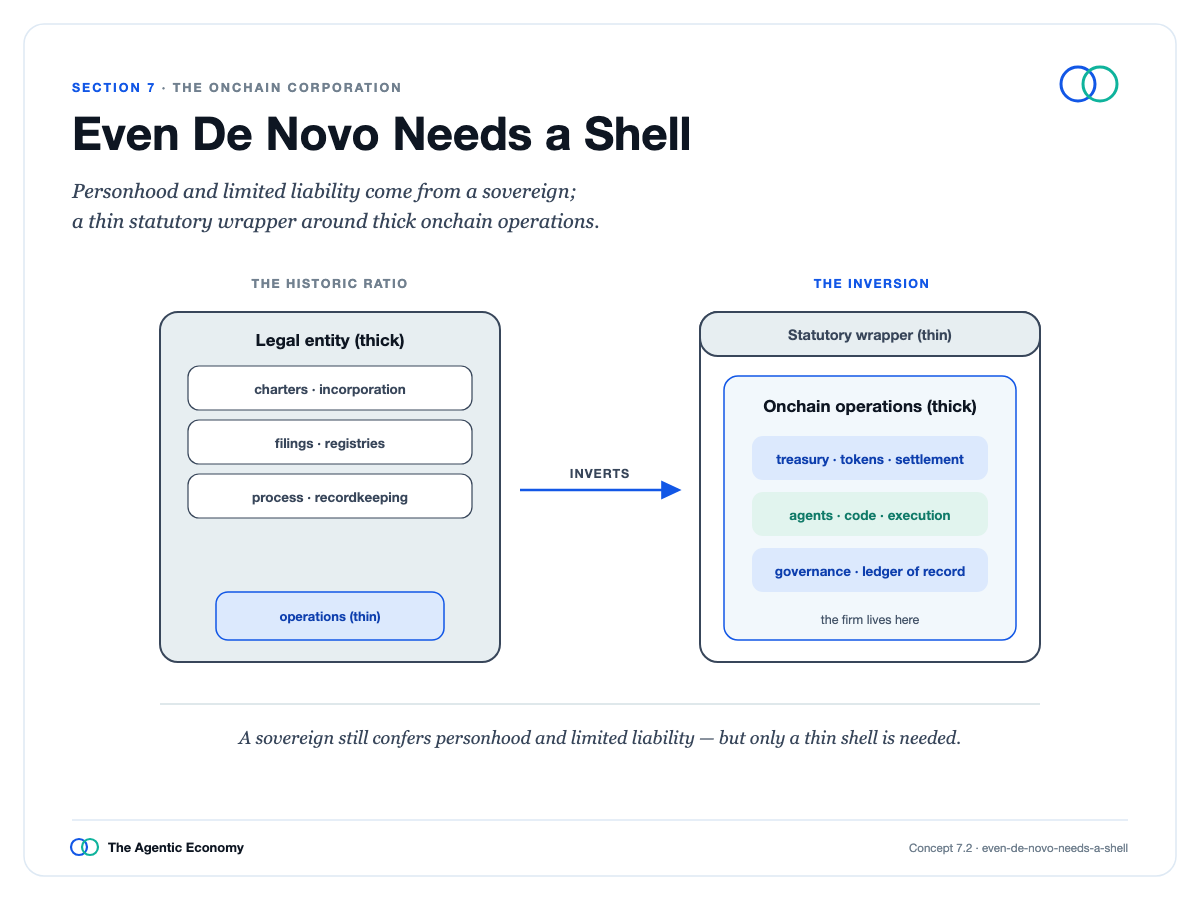

On the other track, new, highly agentic firms build onchain from day one, pulling everyone else forward. Even these new firms don't escape law by being born in software: legal existence and limited liability come from governments, not lines of code, so they still need a thin legal wrapper. What flips is the proportion: the legal wrapper becomes thin, and the onchain working entity becomes thick.

Even De Novo Needs a Wrapper

Two caveats keep this honest. First, shared ledgers can prove what happened, in what order, by whom—a real advance—but they cannot prove whether an action was authorized, wise, or loyal; a perfect record of self-interested trades is still self-interested trading. The ledger is a better witness, not a better conscience, so responsibility still falls on the humans who designed the agent and are meant to oversee it.

Second, contracts become programs in how they execute, running automatically in common, clear cases, but remain legal documents in how they are adjudicated, because code runs verbatim while law makes room for intent, mistakes, and fraud.

The best way to think about it is a reliable core, with human judgment at the edges, handling the few disputed cases with external data feeds, arbitration, and shared, time-bound, recorded override mechanisms, because ultimately, who holds the override key holds the firm.

Click to read Section 7:https://agenticeconomytreatise.com/treatise/section-7.html

08 Impact and Power Concentration

The agent economy holds this era's greatest opportunity and its sharpest risk in the same hand; they are not two futures to choose between but joint outcomes of the same machine, their balance undecided.

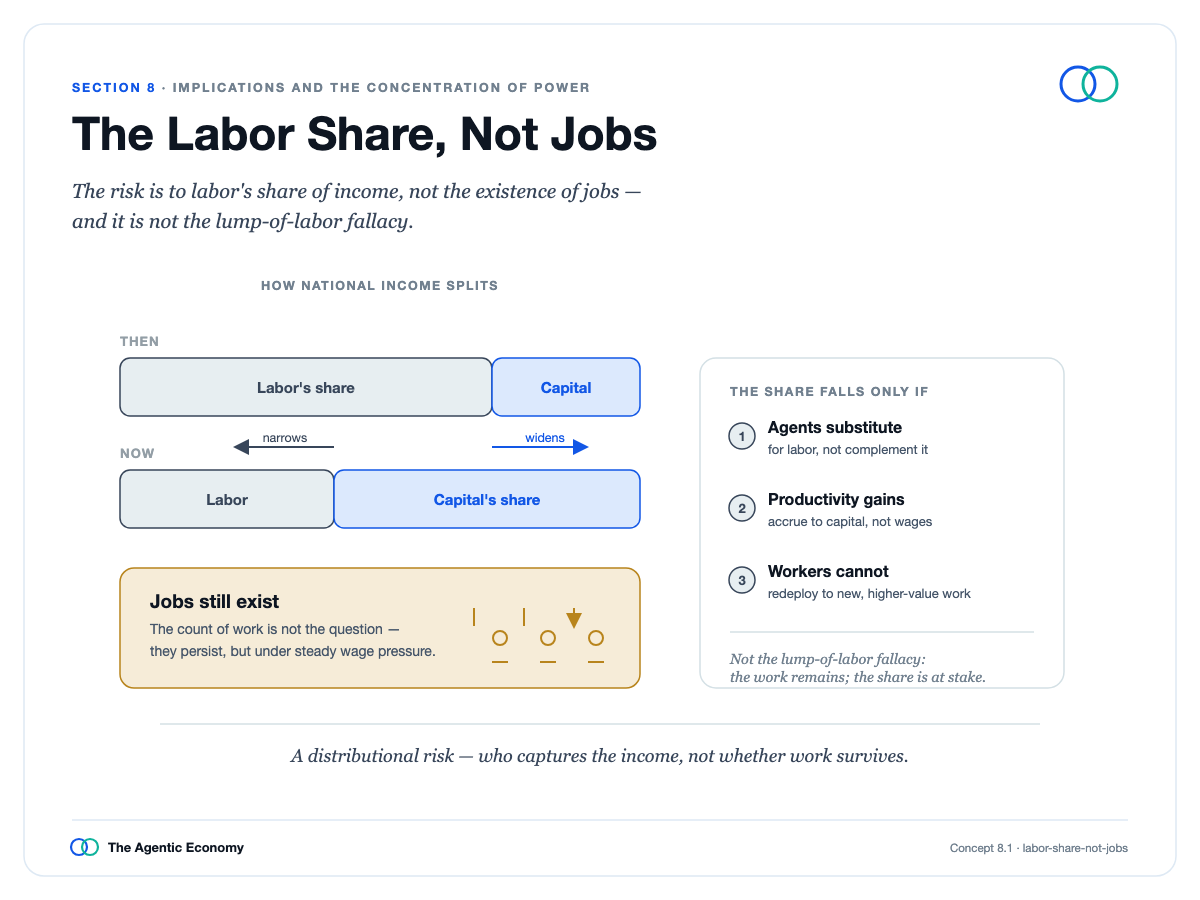

Start with labor, stating it carefully enough to withstand the oldest objection in economics. The claim is not that automation destroys jobs overall—an assumption disproven for two centuries. The real issue is the share of national income going to human labor and the wages human work can command. People may still be employed on tasks where machines are weakest, but the pay for those jobs drops below what sustains a household, which is full employment on paper, crisis in practice.

Labor Share, Not Employment

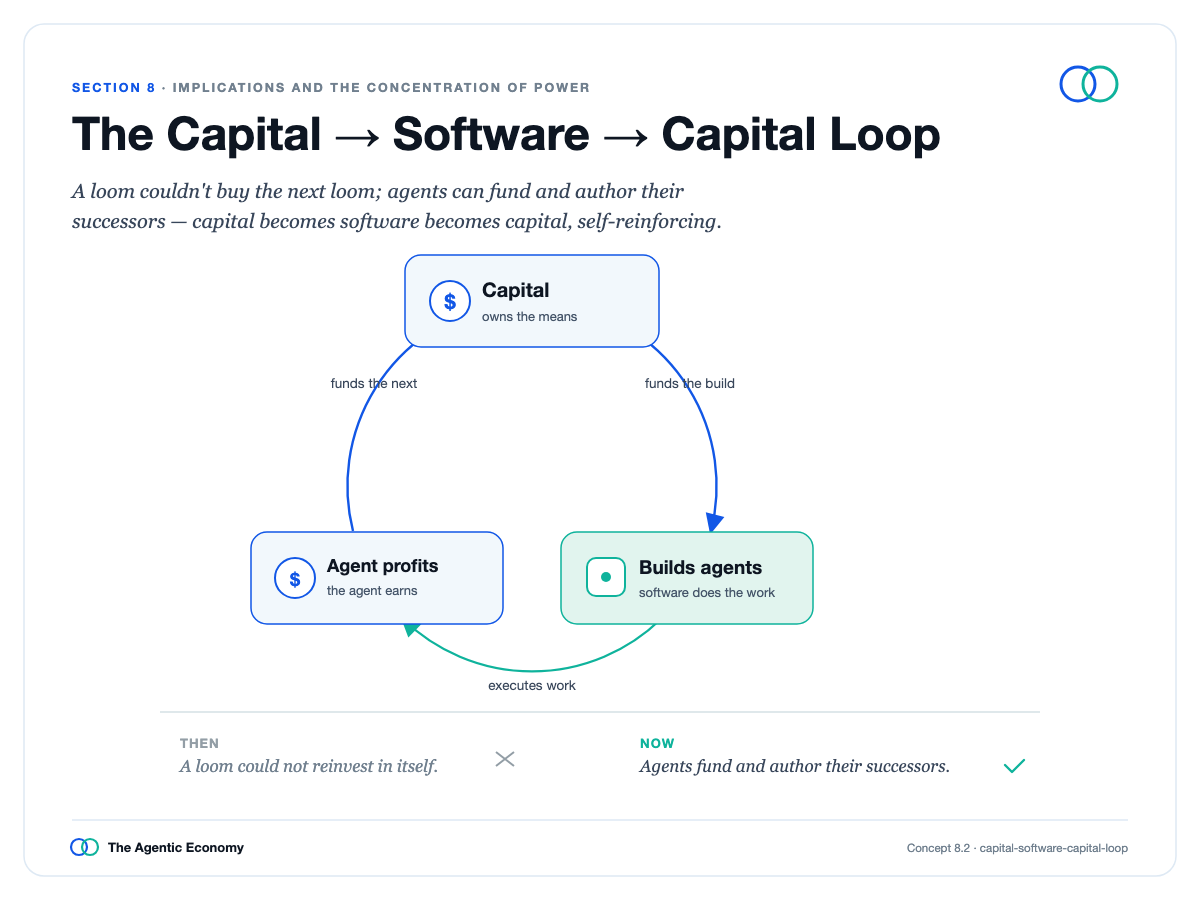

This holds if software takes new tasks faster than people can retrain; if the price of agent labor falls with computing costs, pulling wages down; and if—the break from all past waves—capital can finance its own growth, money earned by agents used to build more agents. A loom never earned the money to buy the next loom; an agent can.

Capital → Software → Capital Loop

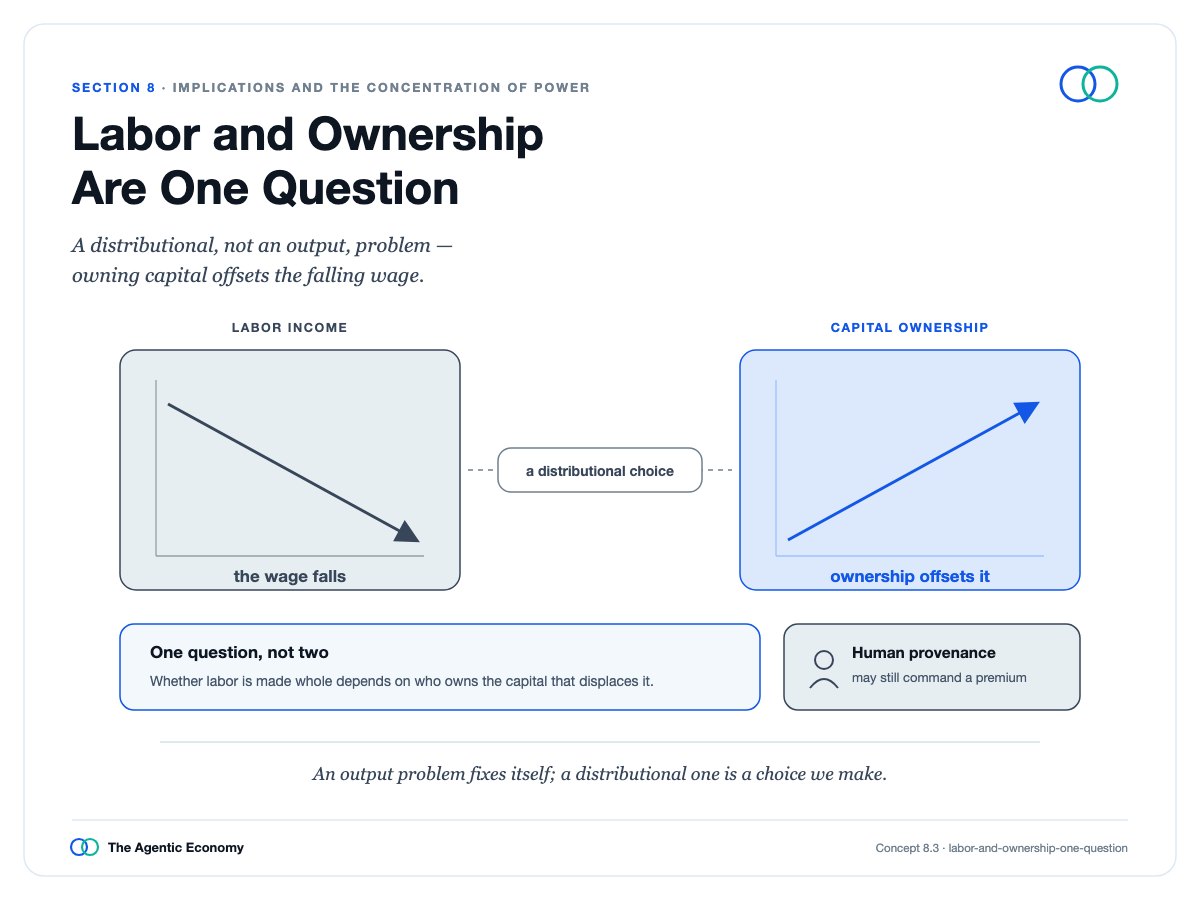

Two honest caveats keep this from fatalism. Even if all the above holds, the result is a distribution problem, not a scarcity problem, because output could be enormous—this is the abundance thesis. And the pessimistic view secretly assumes humans hold no advantage and own nothing, neither of which is foreordained: human work may command a premium for care, status, and authenticity, and if displaced workers own capital, a falling labor share can be offset by their share of the capital they are part of.

This is the crux and should be said plainly: the labor problem and the ownership problem are the same problem. A falling labor share is only a disaster if ownership is concentrated; if ownership is widely shared, the same automation is just shared abundance. That makes concentration the decisive issue, and it deserves analysis, not assertion.

Labor and Ownership Are the Same Problem

Concentration is not a law of nature; open standards and forks have a long record of dispersing power. It wins only when strong network effects meet an unforkable bottleneck: you can copy open-source code, but you cannot fork the dominant currency, license, deep liquidity pool, or override key.

Where power most likely aggregates is not AI models—they tend to commoditize—but the identity layer, the override key, and the dominant currency issuer, which earns the yield on the money it intermediates. The author sits in the last of these and says so, and he argues against his own interest: that yield is a policy choice, and what policy creates, policy can redistribute.

The same choke points that gather profit can also become weapons, history is sobering, so the dense connections that raise the cost of conflict can also be its instruments. Which way it goes depends on whether those points stay open or are captured.

Click to read Section 8:https://agenticeconomytreatise.com/treatise/section-8.html

09 The Civic Vision

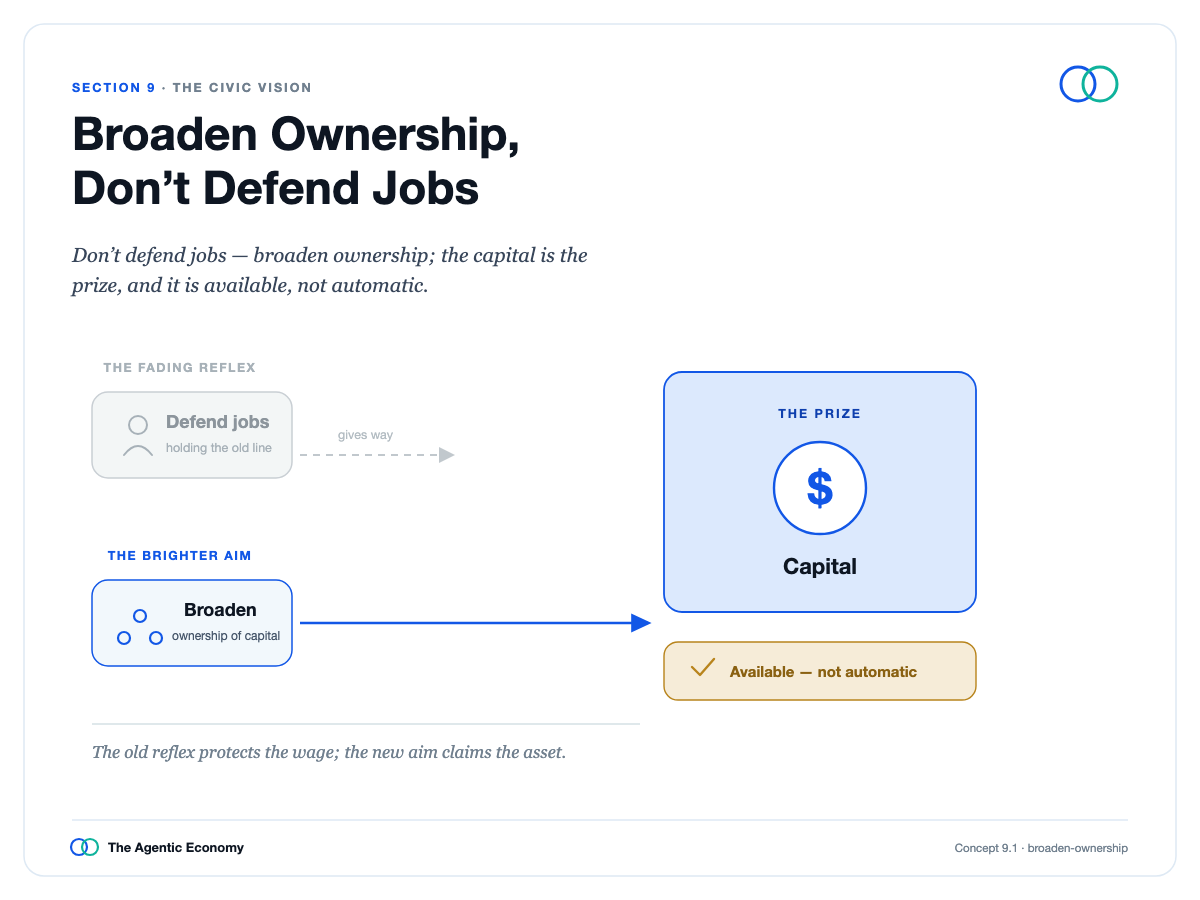

If the agent economy breaks the link between labor and the share of output, the answer isn't to defend old jobs but to broaden ownership of the capital—agents, models, infrastructure, firms—now capturing value. The same architecture that, left alone, concentrates on a few choke points can distribute ownership, returns, and governance more widely than any prior system.

Expand Ownership, Not Defend Jobs

The inheritance determines scale: the joint-stock company once let strangers pool capital and share in an enterprise's success, expanding participation beyond the wealthy and royalty. The onchain economy can stretch it further because, for the first time, there are tools to grant not just ownership but governance and upside to vast numbers at near-zero administrative cost.

The idea isn't new; what's new is that the cost to act on it has become trivial. But capability is not outcome, and this section holds itself to a strict standard: list the mechanisms that actually work, including ones that cost the author himself.

Real history refuses to be whitewashed. Early movements for broad ownership failed not on the paperwork blockchain now solves, but on power.

Onchain mechanisms lower the cost of sharing ownership and remove some gatekeepers, true, but they do nothing for the power imbalances that truly killed those movements.

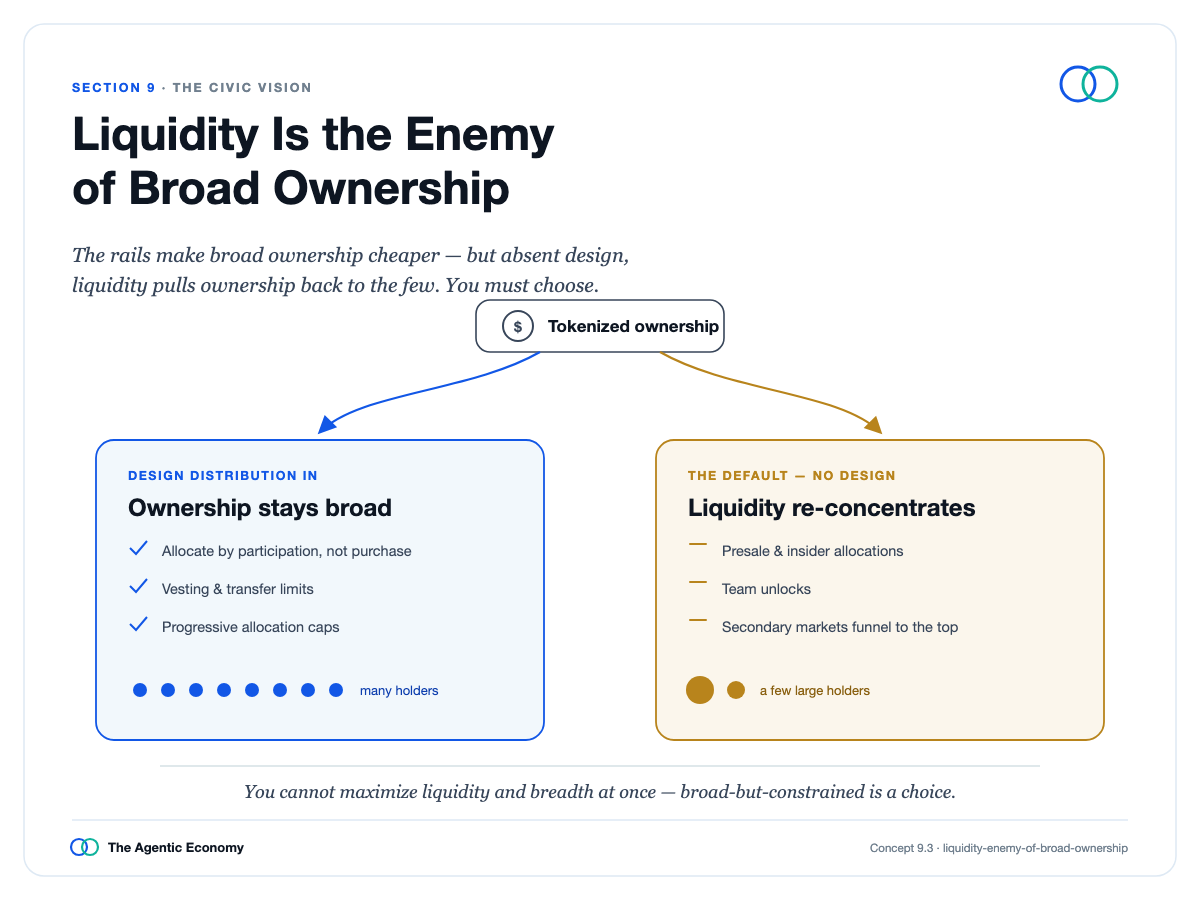

Worse, the default setting is recentralization: insider distributions, especially with open secondary markets, pull tokens back to the largest holders as soon as they have value; and “one-token-one-vote” is plutocracy by design. Liquidity ends up the enemy of broad ownership.

Liquidity Is the Enemy of Broad Ownership

So, the pull must be designed against with vesting through participation, limits on transfer, and caps, accepting that liquidity and breadth cannot be maximized together.

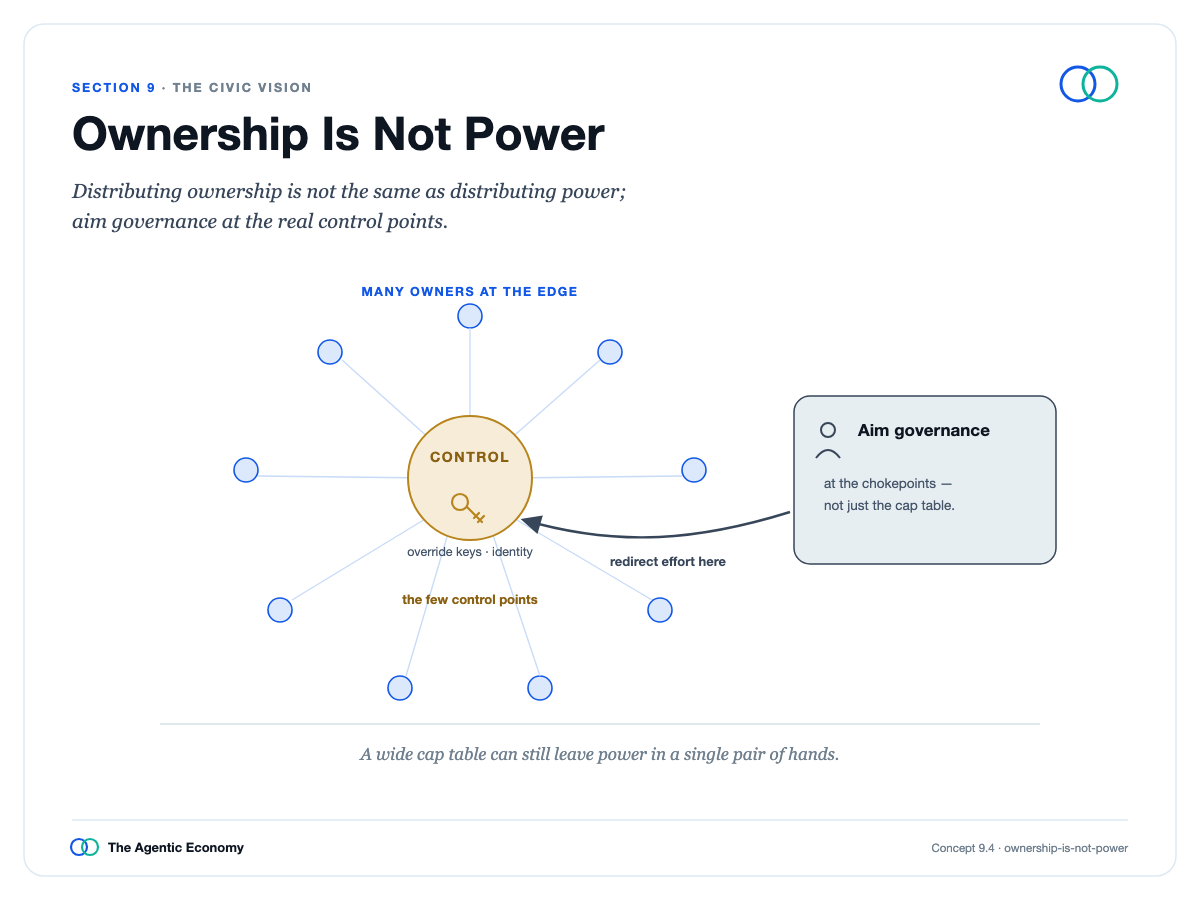

And there is a deeper trap: shared ownership is not shared power. You can give a billion people a stake in an economy, but whoever holds the final override key still controls the firm. Therefore, dispersing the override key is a separate and hard task, targeting those choke points directly.

Ownership Is Not Power

The stance is this: design for expanded ownership, and combine it with equitable capital and automation taxes, public provision of the abundance that should be universal, and a stake for the public in the value these infrastructures create. The clearest measure the author applies to his own interest is the yield on stablecoin reserves: it is a policy creation, should be competed down, and ultimately returned to the people holding that money, including issuers he is associated with.

None of this works on its own merits because the beneficiaries write the rules, so it needs countervailing force: open standards make rent-seeking unblockable, public mandates on the control layer, and a constituency of broad owners with real stakes to defend.

All of it points to a core question: if labor is no longer the path through which people gain standing and voice, perhaps ownership must become that path. Infrastructure is not fate. Whether this becomes the most balanced economy ever or the most concentrated is not a prophecy to wait for but a design problem to solve and a political fight to win. The test of whether we mean it is whether we would constrain ourselves first.

Click to read Section 9:https://agenticeconomytreatise.com/treatise/section-9.html