Author: Prathik Desai

Compiled by: Saoirse, Foresight News

If you are overseas and want to buy SpaceX or NVIDIA stock, it's not easy. You need a brokerage that supports account opening for residents of your country, compliant cross-border transfer channels, and often must meet the qualifications of an accredited investor. The vast majority of ordinary people cannot directly trade US stocks.

Blockchain offers an alternative: you can now gain exposure to US companies through tokenized stocks. But 'tokenized stock' is just an umbrella term; it actually includes three completely different products.

The first is native equity registered on-chain by the stock issuer itself. The second is a backed token representing real shares held 1:1 by an offshore entity. The third is a perpetual futures contract with no underlying stock support whatsoever. The ownership, voting rights, and price appreciation rights enjoyed by holders of these three types of products are vastly different.

Currently, NVIDIA has all three types of token products. The first two types combined have over 650,000 real shares as underlying backing. Yet the trading volume of the perpetual contracts, which are completely unbacked by stock, is 4 to 5 times that of the other two spot token types.

Last week, Vaidik outlined some industry background: since 1973, most stocks (whether tokenized or not) have operated under the same custodial structure. He also explained a core fact—most people who nominally 'hold stocks' do not actually own the corresponding shares. For details, see "Who Really Holds Your US Stocks? 83% of the Market's Stocks Are Nominally Held by This Institution".

In this article, I will deconstruct the ownership structures of different on-chain stock tokens and analyze the underlying logic of why the market is still willing to trade these tokens, even when investors are completely detached from real equity.

What Are Tokenized Stocks

Tokenized stocks are a digital representation of corporate shares on the blockchain. These tokens are programmable, can be freely transferred between wallets, traded 24/7, and integrated into various DeFi protocols. The economic attributes of stocks—such as share price, dividends, and corporate payouts—are embedded within the token's mechanisms.

The market size for tokenized stocks is no longer what it used to be: over the past year, the total market capitalization of the sector has surged nearly fivefold, from $327 million to $1.5 billion.

One of the most noteworthy aspects of this tokenization wave is the participation of traditional giants in experimentation. DTCC, the clearing, settlement, and custodian institution for the vast majority of US and global securities trading, announced last month that it will launch a tokenized securities pilot project in October 2026. The New York Stock Exchange also revealed earlier this year that it is building a 24/7 tokenized stock trading platform. These established institutions, with decades of experience in securities infrastructure, are reevaluating the existing trading system.

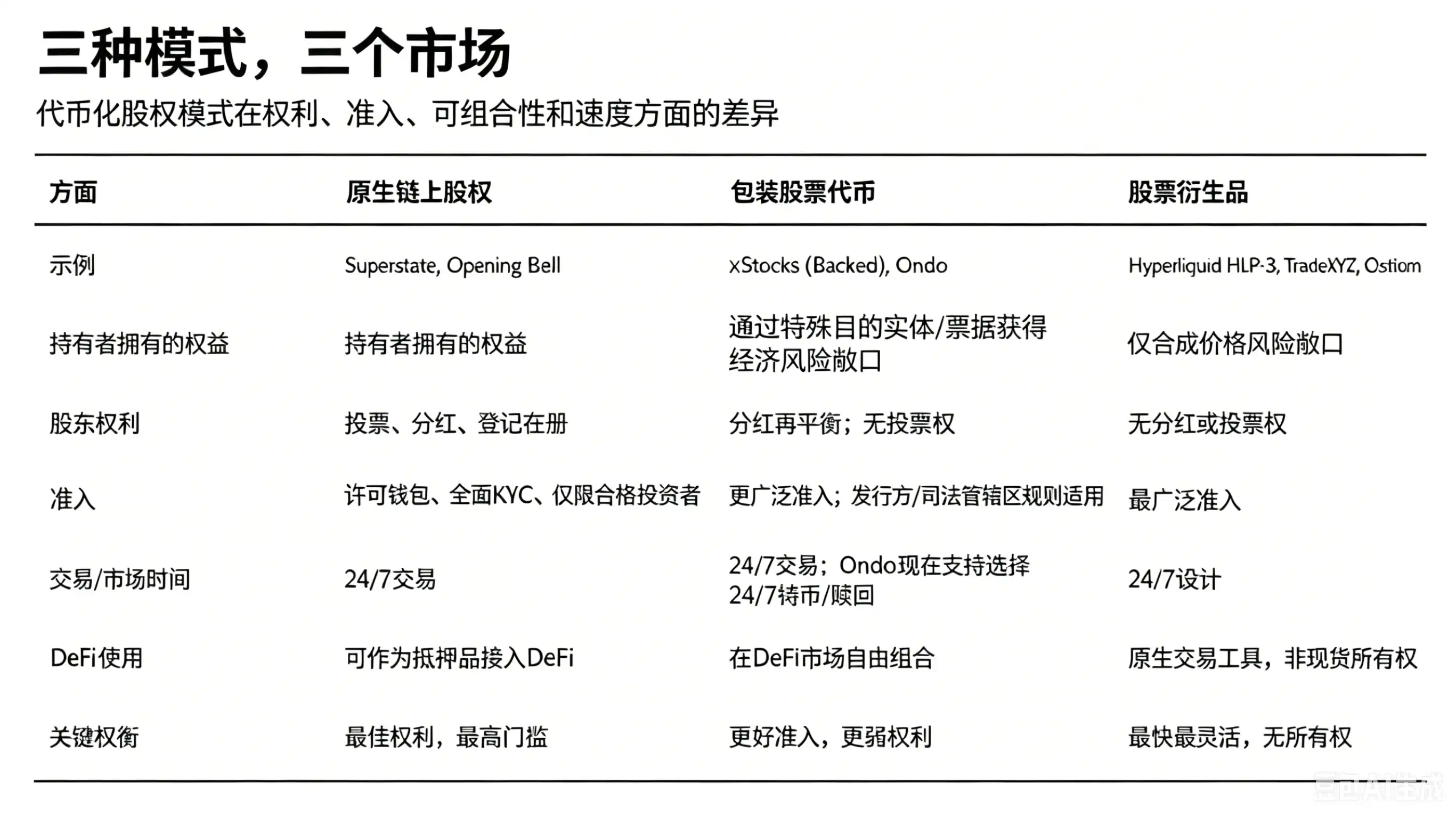

Currently, various stock tokenization solutions have emerged. Different on-chain products make trade-offs in terms of ownership, redemption mechanisms, DeFi composability, and price appreciation rights. Let's break them down one by one.

Trade-offs in Rights for Tokenized Products

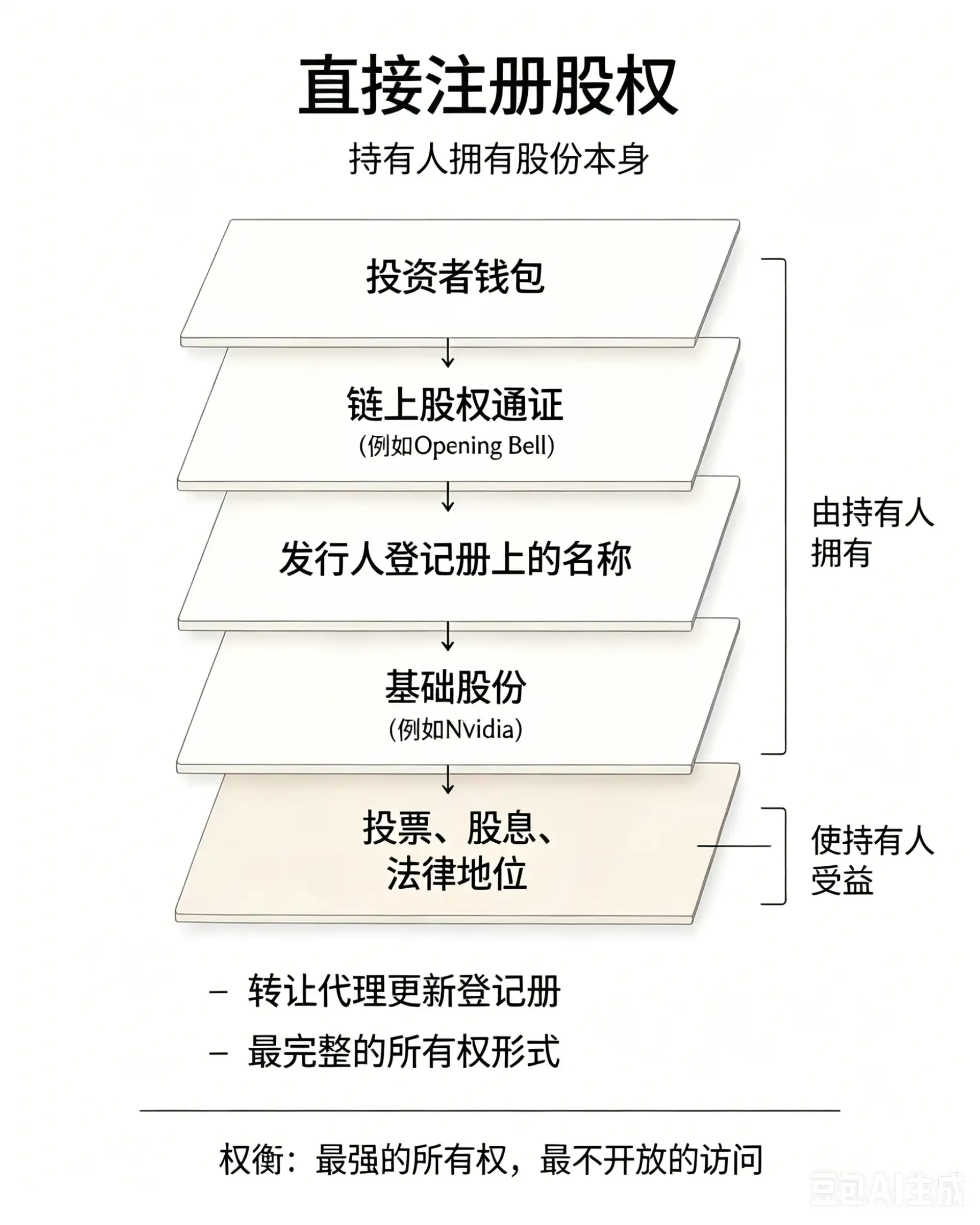

Model 1: Complete Real Equity, Holders Enjoy Full Ownership

The SEC-registered transfer agent Superstate registers equity directly on the Solana public blockchain. The holder's name is recorded in the company's official shareholder register, granting full voting rights, dividend eligibility, and legal shareholder status.

In May 2026, Galaxy adopted this model to complete equity tokenization and achieved on-chain proxy voting through Broadridge. As early as December 2025, Superstate's compliant equity tokens were listed on Kamino, becoming the first registered equity usable as collateral in DeFi protocols.

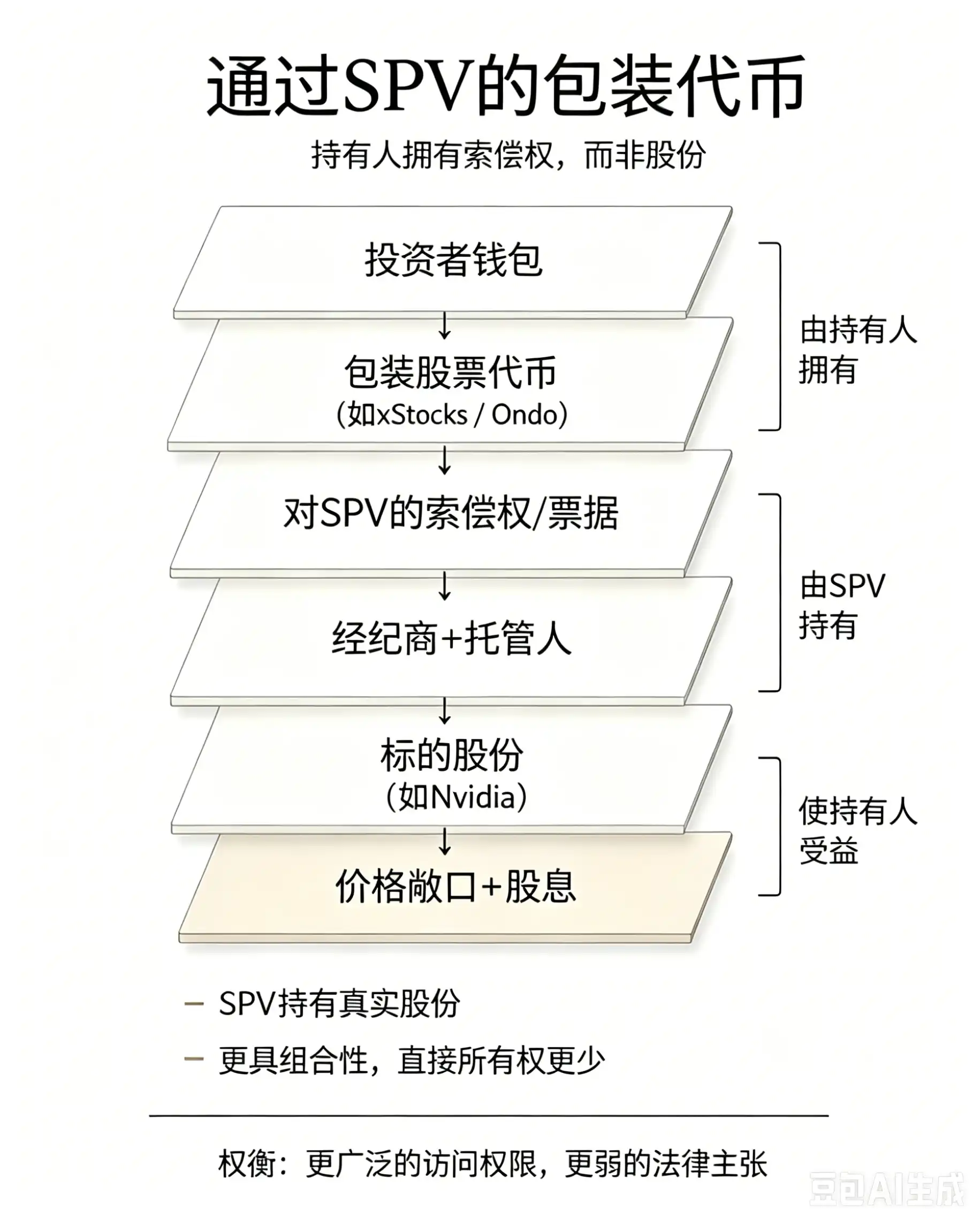

Model 2: Surrendering Full Ownership for DeFi Composability

Backed's xStocks issues tracking certificates through a Jersey special purpose vehicle (SPV), covering over 160 stocks, with underlying shares matched 1:1. Ondo issues total return notes through a British Virgin Islands SPV, supporting over 200 types of tokenized stocks, with the total value locked surpassing $1 billion in just 8 months after launch. Both products allow investors to benefit from stock price appreciation and dividends, but dividends are not paid in cash; they are automatically added to your token balance.

The biggest advantage of this model is its high composability: xStocks can be used as collateral for lending on Kamino and Morpho. Less than 24 hours before this article's publication, Ondo opened round-the-clock minting and redemption channels for its mainstream tokenized stocks, enabling a 24/7 primary market.

But the risks are equally prominent: you only hold a claim against the SPV, not direct ownership of the underlying shares. The PreStocks crash serves as a cautionary tale: in May 2026, the transfer of its underlying shares was deemed invalid. With only $23 million in real stock backing tokens valued at $1.3 trillion, the product ultimately collapsed. Although Backed and Ondo mitigate risks through segregated custody and proof-of-reserves, the risk is not eliminated; it's merely transferred from the corporate entity to the SPV wrapper layer.

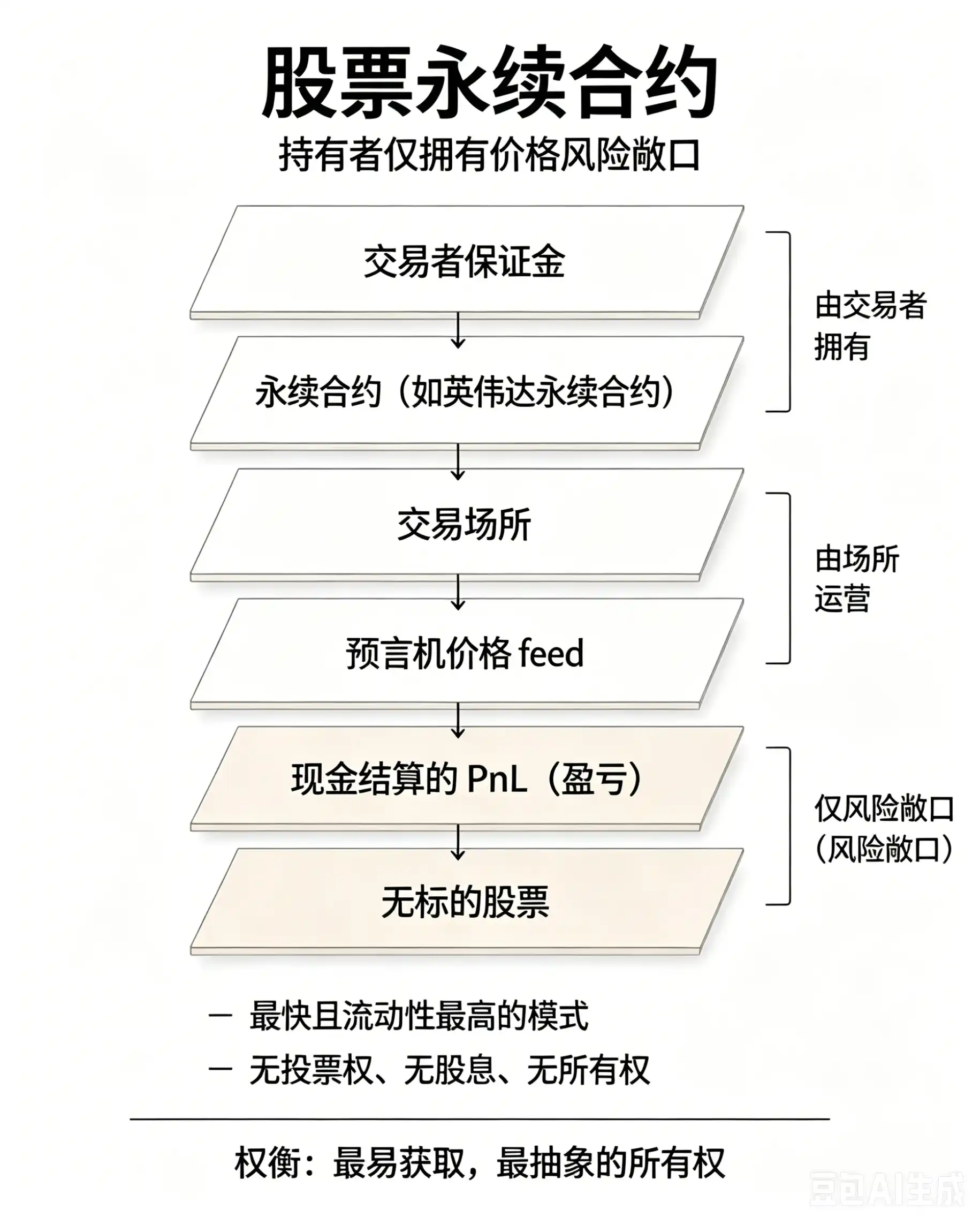

Model 3: Completely Abandoning Equity Ownership, a Pure Price Speculation Tool

Hyperliquid's HIP-3 framework allows anyone to build perpetual contract markets, requiring only a price oracle and a liquidity pool to operate. The leading project, TradeXYZ, accounts for over 90% of the open interest within the HIP-3 framework, offering perpetuals for NVIDIA, Tesla, Google, Amazon, and the Nasdaq 100 index. Ostium, deployed on Arbitrum, has also launched similar products.

The platform charges a funding rate hourly to balance long and short positions, thereby anchoring the perpetual contract price to the stock's spot price.

The trading volume of perpetual contracts far exceeds that of spot tokens for a practical reason: building a spot token market requires a complete supporting system including SPVs, brokerages, custodians, and proof-of-reserves. Launching a perpetual contract only requires connecting to a price data source. TradeXYZ even launched a SpaceX perpetual contract *before* the company filed its S-1 IPO prospectus, with open interest directly reaching $50 million. Spot tokens relying on SPVs simply cannot achieve this speed, as physical institutions cannot quickly and sufficiently purchase the corresponding underlying shares.

The Core Value of Tokens: They Don't Need to Be Tied to Real Shares

The vast majority of retail investors never exercise their voting rights. Research data from the Harvard Law School Forum shows that, on average, only about 12% of retail accounts in a company participate in shareholder meeting votes. For global traders looking to gain exposure to blue-chip stocks like NVIDIA, Google, SpaceX, and Tesla, giving up a voting right they will never use is largely inconsequential.

Tokens themselves possess independent asset value; they do not need to be completely equivalent to native shares. The three types of tokenized products cater to three types of investment needs: institutional long-term capital seeking full shareholder rights, on-chain users valuing DeFi collateral and liquidity, and short-term speculators preferring high leverage and round-the-clock trading. Tokenization is not a replacement for traditional stocks; it is a new type of financial instrument that adapts to different needs across various layers.