Author: Eric, Foresight News

In June 2026, a seemingly promising bottoming rebound for Circle came to a sudden halt. By June 25 US time, the circulating supply of USDC had dropped to 73.6 billion, down approximately 70 billion from its peak. Meanwhile, Circle's stock price plummeted to around $63, effectively halving its value.

On the surface, 70 billion seems like less than 10% of 800 billion. However, for comparison, USDT's circulating supply once reached a high of around 1.91 trillion and currently stands at around 1.863 trillion, a decrease of only 47 billion, or less than 3%.

While there is no direct evidence linking the decline in USDC's circulating supply to the drop in Circle's stock price, their simultaneous movement, along with the coincidence between security incidents in the DeFi space and the timing of Circle's stock decline, inadvertently aligns with a viewpoint expressed by Compass Point analyst Ed Engel back in January:

Circle is a barometer for DeFi activity.

Engel argued at the time that Circle trades similarly to cyclical stocks, noting that from October 2025 to January 2026, the correlation coefficient between USDC's circulating supply curve and ETH's price trend reached 0.66. The core reason is that 75% of USDC circulates within crypto exchanges, DeFi protocols, and similar environments, while the amount actually used for daily consumption, cross-border payments, and other practical scenarios is far lower than imagined.

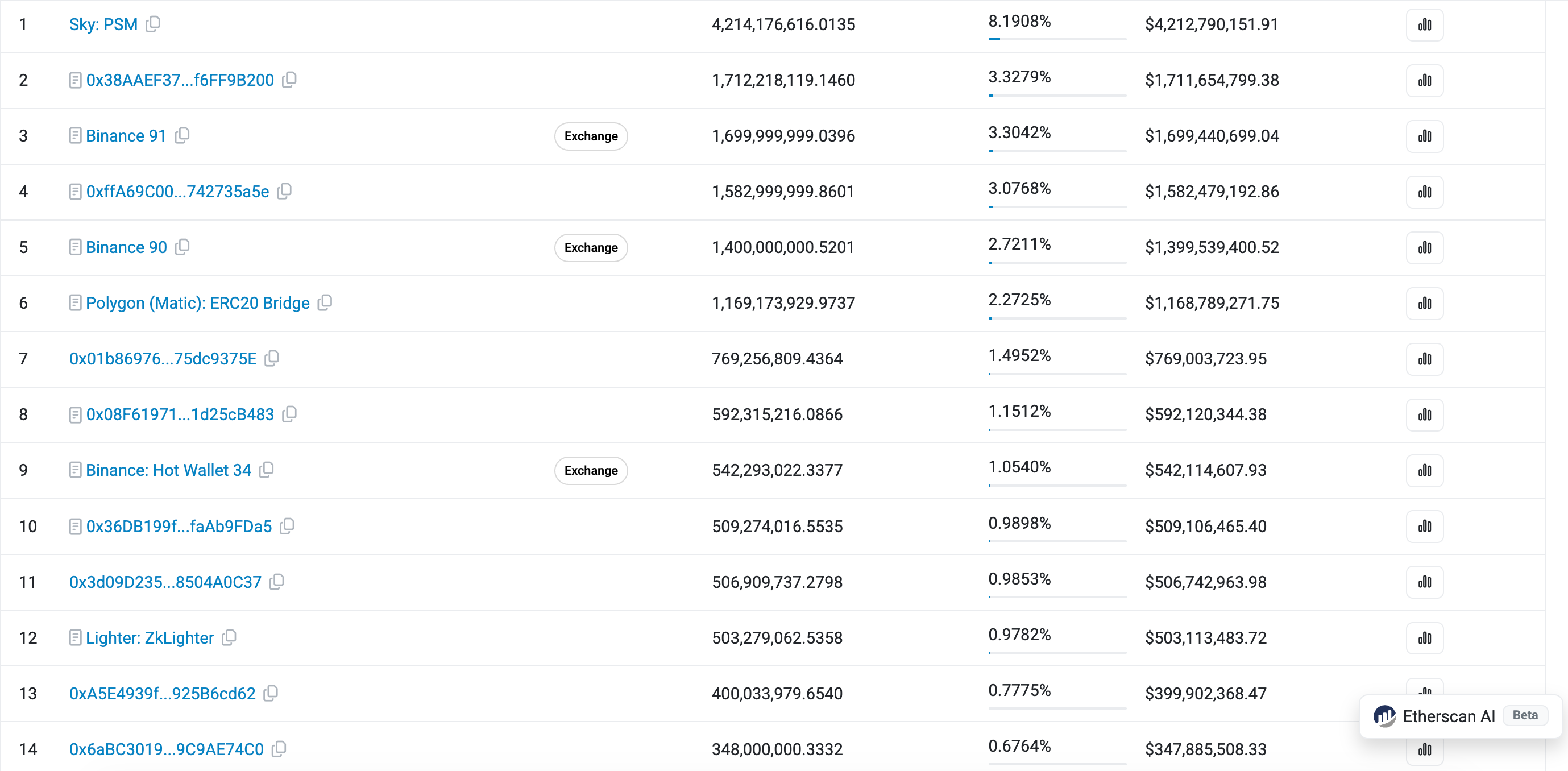

Looking at the Etherscan USDC holding address rankings, the first page is filled with contract holding addresses. These USDC reside in protocols or addresses like DeFi, exchange multi-signature wallets, and cross-chain bridges. Furthermore, the top 100 holding addresses on Ethereum account for over 50% of USDC, with just 0.32% of addresses holding 93.55% of the total supply. A large portion of USDC is parked in protocols, seeking yields higher than bank deposits.

Such high concentration is not characteristic of a "digital dollar" intended for daily circulation. One might counter by pointing out USDT's even higher concentration on Ethereum. However, practical use cases for USDT are very common: the Web3 industry uses it for salary payments, the foreign trade sector settles with it, illicit activities leverage it to evade regulation, and individuals in third-world countries use it to protect savings.

While perhaps not as "glamorous" as USDC, these scenarios form USDT's fundamental user base. This also explains why, despite being the stablecoin most used for crypto trading pairs, USDT has outperformed the more compliant USDC in terms of resilience during the current severe market downturn. The news today about USDT trading at an 8% premium in India further supports this view.

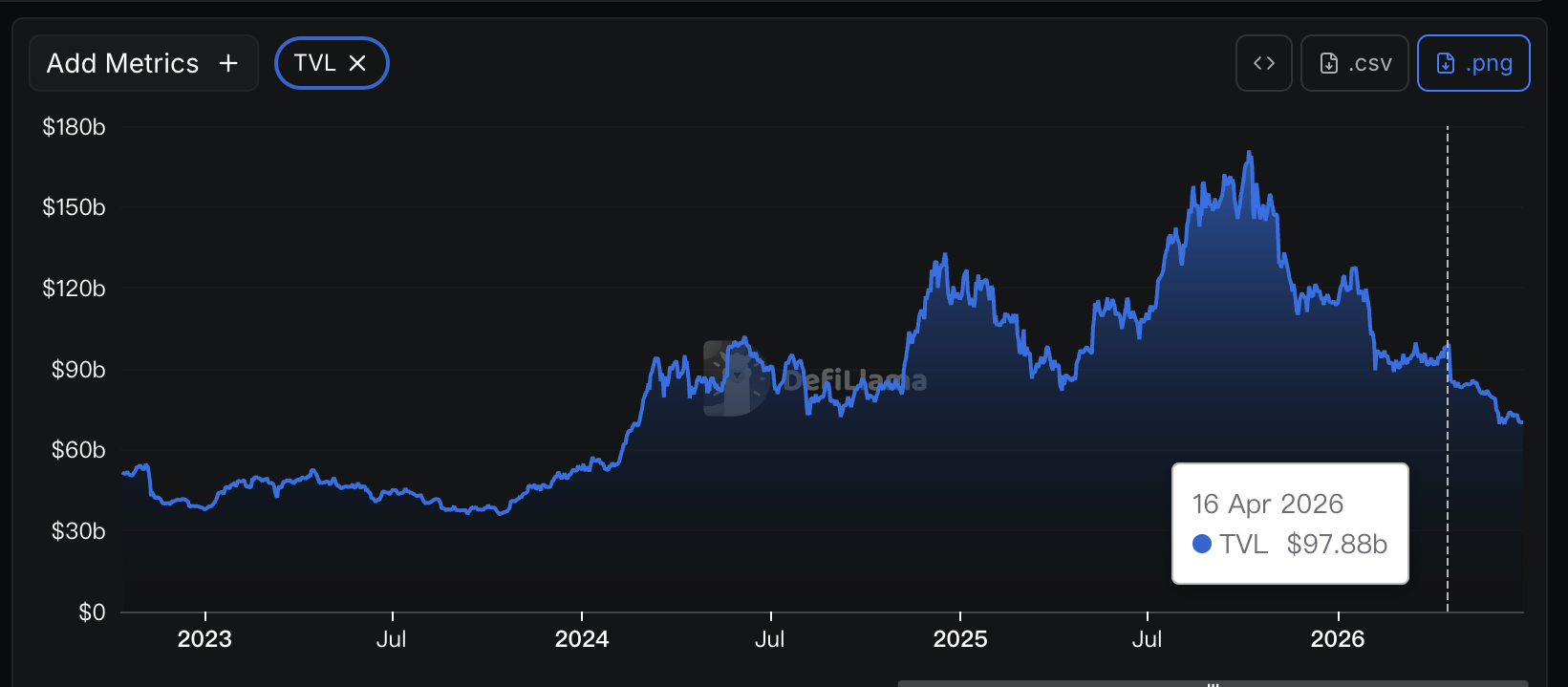

The overall TVL of DeFi began to decline in mid-April, coinciding with the start of the Kelp DAO attack incident. Circle's stock price started its descent in mid-May. Although the starting points differed, their subsequent trajectories have been largely similar.

Just last month, Circle and Coinbase collaborated to elevate USDC to the status of settlement stablecoin on Hyperliquid. The cost involved not only staking 500,000 HYPE tokens each but also conceding 90% of the yield generated by the reserve assets backing USDC on Hyperliquid. Behind this seemingly "win-win-win" situation lies Circle's predicament: its main battlefield, DeFi, is rapidly shrinking. The Kelp DAO incident severely damaged DeFi's credibility. Relying on DeFi's natural growth to boost USDC supply has hit a bottleneck, forcing Circle to "fend for itself."

Upon closer observation, one finds that USDC serves not only as the settlement asset for Hyperliquid but also for platforms like Lighter. Beyond the cryptocurrency sphere, Circle has been relentlessly promoting the use of USDC "as digital dollars." According to Artemis data, USDC's "organic transfer volume" (excluding wash trading, high-frequency trading, exchange wallet consolidation, etc.) in 2025 was $18.3 trillion, compared to USDT's $13.2 trillion.

It is an undeniable fact that USDC is widely used in institutional and compliant payment scenarios. However, the amount of USDC required for these scenarios is not as high as one might think. The flow of funds might not consistently remain in USDC form; instead, USDC acts as an "intermediate state," reducing the time and capital costs of transfers between banks or financial institutions.

In other words, to increase USDC supply by 100 billion tokens might require trillions of dollars in real-world capital flow. On-chain, however, it could simply involve a few large DeFi protocols, meme coin trading platforms, or prediction markets. No matter how fast USDC circulates or how high its adoption rate is in the real world, if the issuance volume of USDC doesn't increase, neither will revenue nor profits.

Of course, none of this is enough to "sentence Circle to death." If Circle can break free from its reliance on DeFi in the future, or demonstrate that real-world usage significantly drives the growth of USDC's issuance volume, its investment thesis might be rewritten. In the short term, however, the focus likely remains on whether DeFi can break free from the shackles of "mismatched returns and risks" and restore more market confidence.