Author:Zhou, ChainCatcher

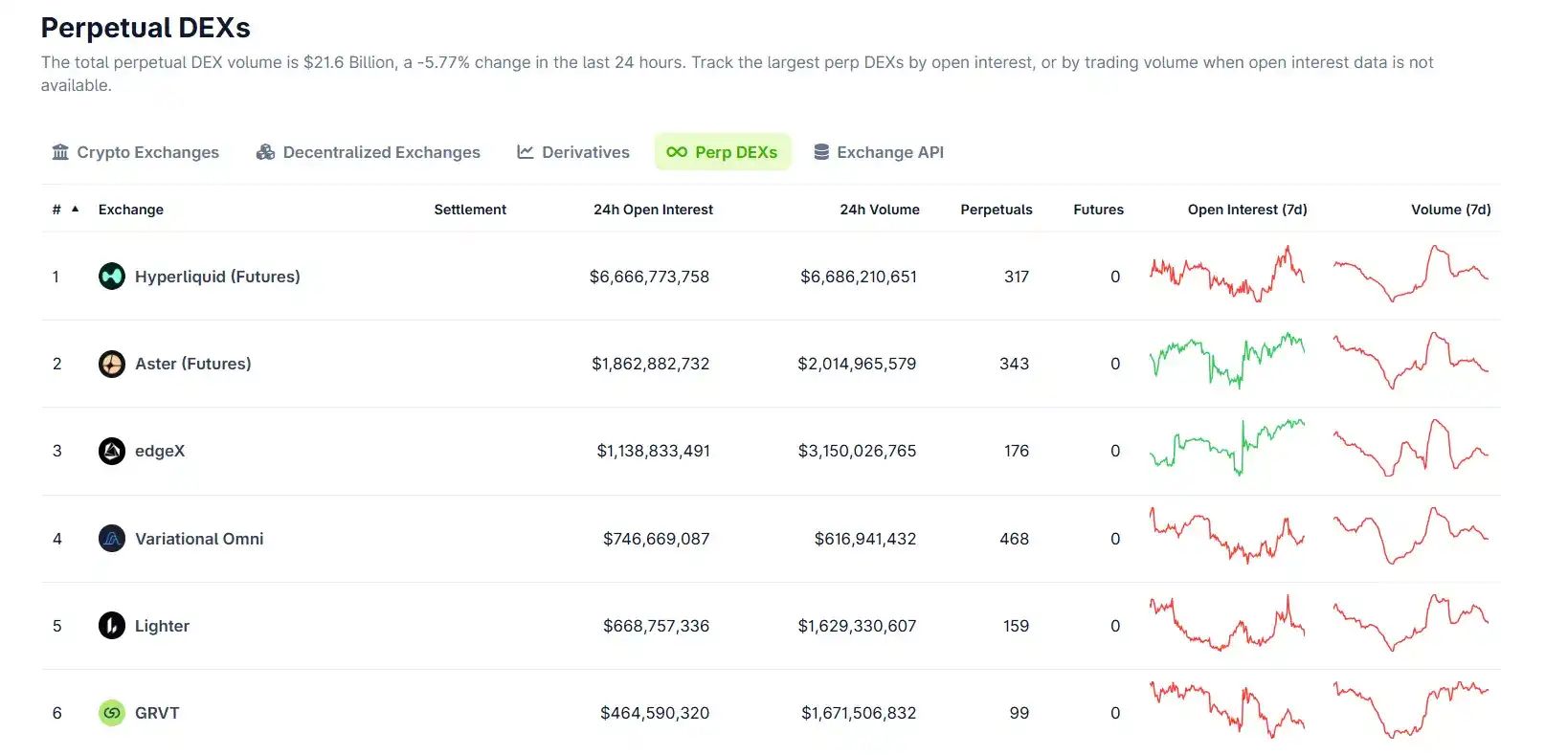

Last week, Hyperliquid's trading volume reached approximately 15 billion USD, with commodity-related contracts such as crude oil, gold, and silver becoming the main drivers.

As oil prices fluctuated sharply, the daily trading volume of crude oil perpetual contracts on Hyperliquid exceeded 2.2 billion USD, second only to Bitcoin.

With the escalation of the situation in Iran and the Strait of Hormuz in crisis, and the CME closed over the weekend, global traders flocked to an on-chain decentralized exchange for price discovery.

At the same time, GMX Labs, which once held nearly a quarter of the decentralized perpetual contract market share, is publicly recruiting a CEO, admitting that the early founder-driven model is unsustainable and seeking to transition to a traditional leadership structure.

One is capturing the overflow demand from traditional finance, while the other is still rebuilding its foundation.

GMX and dYdX Why Did They Fail?

Looking closely at this announcement from GMX Labs, the candidate pool for CEO covers DeFi, CeFi, traditional finance, and the tech industry, with a base salary of 150,000 to 200,000 USD paid in stablecoins, and performance directly tied to protocol fee growth. This proposal passed in the DAO governance vote with 96.42% approval.

A decentralized protocol, with overwhelming community consensus, decides to introduce a traditional professional manager. This means the community has realized that the original makeshift model can no longer hold up, and the solution they can think of is to move closer to traditional enterprise management.

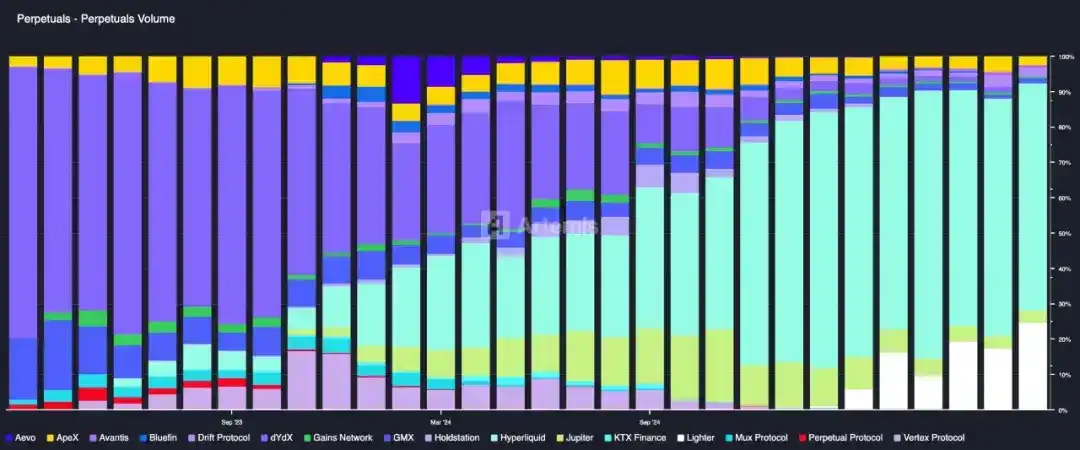

dYdX's situation is even more dire. At the beginning of 2023, dYdX held 73% of the decentralized perpetual contract market share, almost monopolizing it; by the end of 2024, this number had dropped to single digits, and its token price fell by over 90%.

Now, the news about these two protocols in the media is not about product updates or market share, but token buybacks. When a protocol focuses its main energy on maintaining token value rather than winning market share, its strategic focus has fundamentally shifted.

First is the starting point problem. An OKX Ventures report shows that in 2021, dYdX pushed its daily trading volume to about 9 billion USD through trading mining, once surpassing Coinbase. This number was built on token incentives, with users刷量ing for rewards, not real trading.

The more serious consequence is not the虚假 data itself, but the team treating虚假 user feedback as real product signals to respond to, so the iteration direction was off from the start.

Second is the architecture problem. GMX adopted a multi-asset liquidity pool plus oracle pricing model. This design had its合理性 in 2021, when the Ethereum chain couldn't handle order books, and the AMM model was a viable choice.

But this architecture has a quantifiable ceiling; the total open interest the protocol can carry is approximately 5 times the TVL, and the上限 of TVL locks the上限 of trading scale.

LPs are naturally at an information disadvantage in this model, acting as the collective counterparty for all traders but without the ability to actively manage risks. Professional market makers are unwilling to enter under these conditions, so liquidity depth is always limited.

dYdX saw the direction of order books and decided to migrate to Cosmos to build its own app chain. The technical judgment was correct, but there were problems in execution. After the migration, users needed to readapt to new wallets and cross-chain asset bridging, significantly increasing friction costs. More critically, in the v4 version, protocol fees flowed to validators instead of token holders, and the community's perception of growth红利归零.

The third point lies in the judgment of the decisive point. GMX bet on the liquidity model, dYdX bet on building its own chain, but the real decisive points in this赛道 are only two: performance, and the density of the market maker ecosystem.

OKX Ventures pointed out that most perpetual DEXs merely shift centralized risk from the custody layer to the less visible execution and liquidation layers. Decentralization is treated as a narrative, not a real product problem to be solved.

dYdX's turn to synthetic stock perpetual contracts and opening up to US users is about trading compliance for survival space, avoiding正面竞争. GMX recruiting a CEO is about using organizational upgrade to make up for strategic judgment欠账. These are correct self-rescue actions, but they are still dealing with the results, not the causes.

The Logic of the Latecomers

Hyperliquid launched in 2023, when GMX and dYdX were still the dominant players in this赛道. It had no financing, no VC backing, and no large-scale launch event.

On the technical route, founder Jeff chose from the beginning to build his own L1 and create a fully on-chain order book. The logic behind this was that through a fully transparent on-chain environment, market makers could identify different types of trading flows and adjust their quoting strategies accordingly.

This line of thinking determined that it could not take the path of dYdX's migration to an app chain, nor could it follow GMX's reliance on oracle pricing; it had to rebuild from the ground up. Although this theory is still controversial in the industry, it provided a clear主线 for Hyperliquid's product direction.

In terms of布局 traditional assets, HIP-3 was launched in October 2025, first accumulating a market maker ecosystem with crypto assets, then依次 launching gold, silver, and crude oil.

The report points out that when dYdX launched permissionless traditional asset markets in 2024, the daily trading volume of Tesla synthetic stock was 4000 USD, and the Turkish Lira was 0. Without market makers present, asset listing is zero.

而Hyperliquid's approach was to wait for the market maker ecosystem to mature before expanding asset categories, so when the Iran crisis broke out, it caught this wave of trading volume.

Aster CEO Leonard said in an interview, "When dYdX appeared, we started trying to build our own thing on-chain, and the first version of Aster appeared, which was Apollo X. Since then, perpetual contract DEXs have gone through several cycles, with projects like GMX representing an era. We have always tried to build what the market really needs, so now we have Aster."

From his words, it can be seen that Aster's path is渐进. Starting from the AMM model, it gradually iterated, adding order books, and then adding private order functions to address the limitations of transparent markets. Each step responds to market feedback, and each step is a reasonable product decision.

Simply put, it has always been following the evolution of the赛道, not defining the evolution of the赛道.

Don't Release Your Product Too Early

In the crypto industry, the speed of technological paradigm shifts is too fast, and渐进 iteration means you are always chasing the decisive points of the previous era.

There have always been people in this赛道重新 looking for answers, and this is still the case now.

The crypto industry is not viewed favorably now, and a large amount of talent and capital is withdrawing. But precisely because people are leaving, the technology window will not be quickly filled, leaving builders with more time. Every infrastructure iteration, L2 maturity, app chain feasibility, and on-chain order book viability open up new product possibility spaces.

First-mover advantage is much more fragile in this industry than in traditional industries, which is both a risk for old players and a real opportunity for new players. Especially in the era where AI tools level the productivity gap, homogeneous competition is intensifying, and just-good-enough products are increasingly difficult to stand on their own.

Particle's founder, summarizing the lessons of the past year's entrepreneurship, quoted Google founder Sergey Brin's words at Stanford: Don't release your product too early. He meant that once you release a signal too early, you are tied to a delivery timeline and have no time to truly finish what needs to be done.

So, the real problem for entrepreneurship is not how fast you run, but figuring out where the endgame of this赛道 is.

Conclusion

GMX recruiting a CEO is not a big deal, but it may be looked back upon as a footnote at some point.

The entrepreneurial红利 period of the first generation of perpetual DEXs has ended. The era of makeshift teams, founder-driven, rapid iteration has reached a node that requires professional management.

The new window is elsewhere, just as Hyperliquid caught this wave of geopolitical行情 with commodity contracts. Decentralized exchanges are moving from internal competition within the crypto industry towards real替代 of traditional financial infrastructure, and this direction has just begun.