Author: Jae, PANews

Many regulatory obstacles have emerged on the path to earning interest by holding USDC.

The yield logic of the stablecoin market is undergoing a restructuring from "easy money" to "earned rewards".

The CLARITY Act is taking aim at severing the passive income channels of CEXs (Centralized Exchanges), yet it preserves room for activity rewards for DeFi native stablecoins. According to the draft text disclosed in March, if this bill passes, it could mean: the days of users holding USDC on Coinbase to earn a 4% annualized yield are about to become history.

The old-era dividends of centralized stablecoins may be coming to an end, while DeFi native stablecoins like USDe and USDS have the opportunity to open up growth space in the gaps of regulation, ushering in a further expansion opportunity.

Banking Industry Spends $56.7 Million Lobbying to Block "On-Chain Deposits"

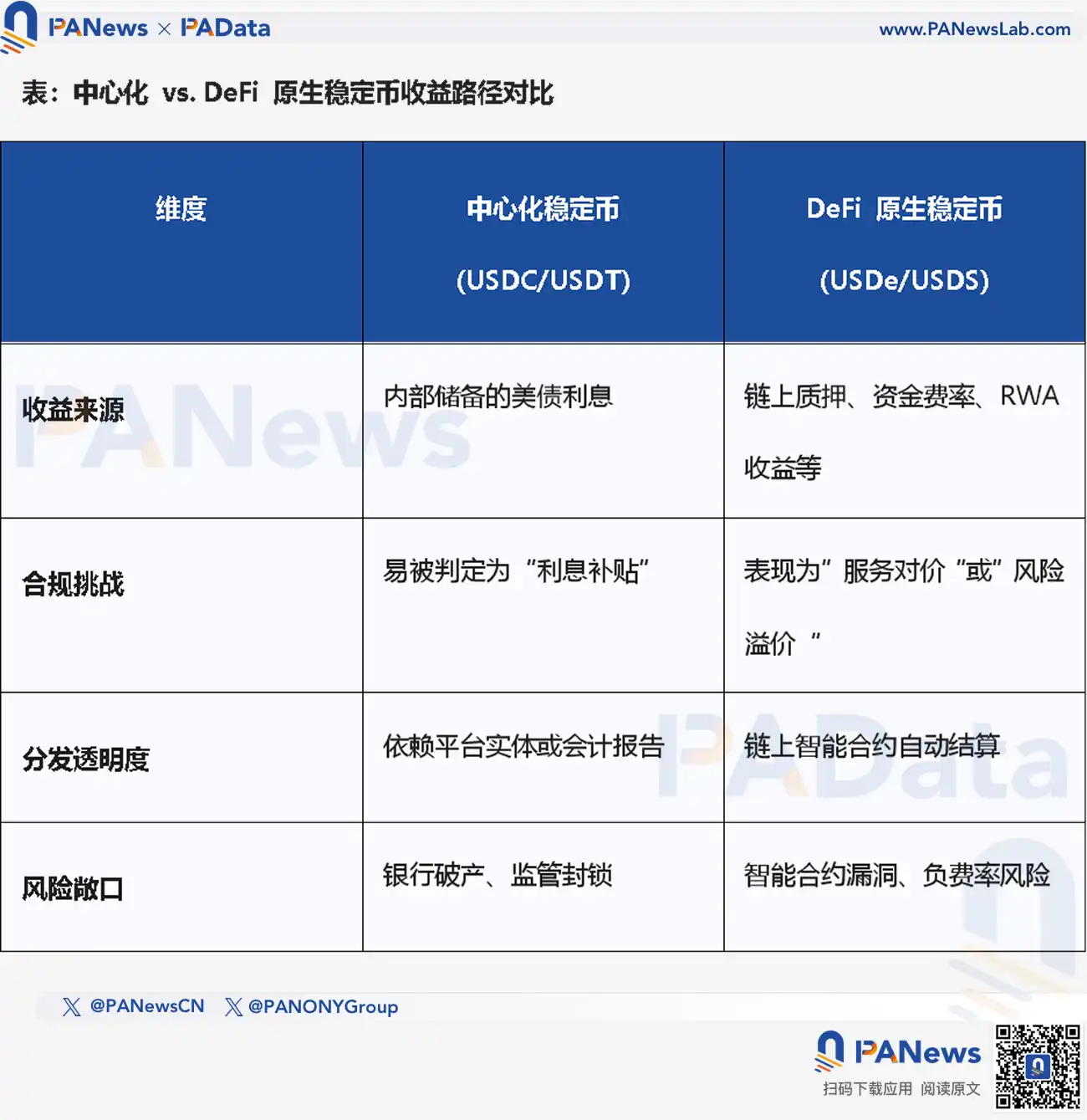

The GENIUS Act, which took effect in July 2025, for the first time established stablecoin issuance rules at the federal level, requiring 1:1 reserves and restricting issuers from directly paying interest, but it left a "distributor loophole": Platforms like Coinbase could, through revenue sharing with issuers like Circle, return U.S. Treasury yield to users in the form of "rewards". This is like banks not being able to directly pay interest on user deposits but being able to give users "red envelopes" through third parties—it's essentially the same thing.

In this gray area, stablecoins quietly broke through their positioning as payment tools, transforming into "on-chain deposits" with built-in yield.

The emergence of the CLARITY Act is precisely to plug this gap. The latest draft text disclosed in March shows that the ban has been extended from issuers to all "digital asset service providers," including CEXs, brokers, and their affiliated companies.

This restrictive trend reflects regulatory considerations regarding the conflict between the "monetary attributes" and "securities attributes" of stablecoins. In regulatory consensus, payment-oriented stablecoins are considered a "Narrow Bank" tool: their functional positioning is for payment and settlement, not as investment products for capital appreciation.

The stringent restrictions on yield distribution in the CLARITY Act are the result of a carefully orchestrated defense battle by the U.S. banking industry. To prevent stablecoins from offering competitive yields, the ABA (American Bankers Association) spent a whopping $56.7 million on lobbying.

The banking industry argues that if users can earn Treasury-like yields of 4%-5% by holding stablecoins, free from traditional banking regulation and deposit insurance constraints, then up to $1.5 trillion in low-cost retail deposits could flow out of the commercial banking system.

This "Deposit Flight" phenomenon is particularly fatal for U.S. community banks, as they heavily rely on retail deposits to support loans to farms, small and medium-sized businesses, and mortgage housing.

Estimates from Standard Chartered show that if stablecoin yields are not banned, the banking system could face a funding gap of $500 billion by 2028.

However, PANews believes that this calculation is based on several assumptions; the speed and scale of deposit migration will be influenced by multiple factors such as user habits, platform security, and regulatory transparency.

The overlap between stablecoin users and bank retail deposit users is relatively limited. The calculation of $1.5 trillion in deposit outflows is based on extreme assumptions, and the actual impact will likely be far lower.

Furthermore, stablecoins and bank deposits differ fundamentally in risk attributes and usage scenarios; the two may not be perfect substitutes.

Passive Yield Sentenced to "Death," Activity Rewards Leave a Narrow Door Open

The CLARITY Act does not impose a blanket ban on all rewards but sets "Identifiable Activity" screening criteria to legally avoid the "expectation of profit" judgment condition in the Howey Test.

The CLARITY Act explicitly prohibits interest payments based on "idle balances," which severely impacts the sharing model that Coinbase and Circle have maintained for years. For a long time, Coinbase has offered rewards as high as 3.5%-5% to its USDC holders, with the source of funds being the interest income from U.S. Treasuries in Circle's reserves.

Data shows that the correlation between USDC rewards and the 3-month U.S. Treasury yield is as high as 98.7%. By cutting this link, regulators are essentially stripping CEXs of their most attractive user growth weapon.

In contrast, the CLARITY Act preserves the legitimacy of incentives for "active behavior." According to Section 404(b)(2) of the bill, rewards generated from three types of activities are deemed compliant:

- Platform Activities: Loyalty programs, promotional lotteries, subscription discounts, etc.;

- Transactions and Consumption: Payments, transfers, cross-border remittance settlements, etc., made using stablecoins;

- On-Chain Infrastructure Contribution: Participating in protocol validation, staking, governance voting, or providing liquidity.

This classification creates a new legal logic: If the yield is not "given for free" but is earned by the user through undertaking specific risks or performing specific labor, then it is no longer a "deposit" but a form of "Payment for Service."

Strictly speaking, the path to earning yield with USDC is not completely blocked; users can still earn rewards by participating in activities using USDC. However, since participating in activities involves certain costs, compared to the previous "easy money" model, the yield obtained will inevitably incur损耗 (loss/wear and tear). The utility of USDC will also revert more to payment, settlement, and consumption.

This恰好 (precisely) creates a clear compliance path and growth opportunity for DeFi native stablecoins.

Derivatives Hedging and Protocol Profit-Sharing, DeFi Native Stablecoins Step on the Compliant "Escape Hatch"

While CEXs tread carefully in the "regulatory minefield," DeFi native stablecoins like USDe and USDS,凭借 (relying on) their截然不同的 (entirely different) yield logic, have stepped into the regulatory gap for compliance.

Taking USDe as an example, it抛弃 (abandons) bank dollar reserves and is supported by a "synthetic dollar" derivatives architecture, with the underlying logic being Delta neutral hedging.

USDe's yield comes from two separate activities, both of which can be interpreted under the CLARITY Act as "activity-based rewards":

-

Staking Layer Yield (Staking Yield): Earned by holding staking tokens like stETH, obtaining consensus layer rewards from the Ethereum network, which is explicitly listed in the bill as a compliant activity for "participating in validation or staking";

-

Derivatives Layer Yield (Funding Rates): By opening equivalent perpetual contract positions on exchanges. In a market with strong bullish sentiment, the funding fees paid by long positions to short positions constitute the main source of yield for USDe.

Under the framework of the CLARITY Act, the yield obtained by USDe holders is essentially a reward for users participating in the specific activity of "risk management and hedging operations," not interest paid by the protocol based on deposit balance.

Because USDe's yield is volatile and bears counterparty risk and smart contract risk, it will legally depart from the category of "bank deposit equivalents."

USDS represents another DeFi native force adapting to regulation.

Users deposit USDS into the Sky protocol, which deploys the deposits to other lending protocols or liquidity pools. In this process, the revenue or fees generated on Sky, as well as RWA (Real World Asset) yields, are distributed to users as returns.

Therefore, USDS incentivizes users through "protocol profit-sharing" rather than "interest payments." The provision in the CLARITY Act draft regarding rewards for "providing liquidity" also, to some extent, provides a legal shield for DeFi protocols adopting models similar to USDS.

The advancement of the CLARITY Act宣告着 (declares) the impending end of the era of wild growth for stablecoins. Under the spotlight of regulation, the market is moving towards a clear dual-track structure. There are no absolute winners, only survivors who adapt to the rules.

Centralized stablecoins like USDC will inevitably become "instrumentalized," returning to their本源 (origin) of payment and settlement.凭借 (Relying on) compliance, liquidity, ecosystem coverage, and cross-border transfer experience, they will become the preferred digital cash for most ordinary users and enterprises, with yield no longer being their competitive barrier.

DeFi native stablecoins like USDe may承接起 (take on) wealth management needs, becoming the "yield engine" of the crypto market. By deeply anchoring asset value to complex on-chain activities like Delta neutral hedging and liquidity mining, they巧妙地 (cleverly) circumvent the regulatory狙击 (sniper fire) aimed at "bank deposits."

The differentiation in the stablecoin track is an inevitable result of the market seeking optimal solutions within the compliance framework. For investors, understanding the deep logic behind this migration is more important than chasing high yields: future stablecoin yields will no longer belong to passive "holders" but to active "contributors" who participate in protocol activities.

This transformation is both a result of regulatory constraints and an opportunity for DeFi innovation to adapt to regulation.