Source: New York Times

Original Title: The S.E.C. Was Tough on Crypto. It Pulled Back After Trump Returned to Office.

Authors: Ben Protess, Andrea Fuller, Sharon LaFraniere, Seamus Hughes, Elena Shao

Compiled and Edited by: BitPushNews

The New York Times conducted a systematic analysis of thousands of government documents and court records from the last three U.S. administrations and interviewed more than twenty current and former government officials.

A cryptocurrency company operated by the billionaire Winklevoss twins was facing a severe federal lawsuit. After Trump returned to the White House, the U.S. Securities and Exchange Commission (SEC) moved to freeze the case.

The SEC had also sued the world's largest cryptocurrency exchange, Binance (Binance), but after the new administration took office, the SEC completely dropped its lawsuit against the company.

Furthermore, after a years-long legal battle with Ripple Labs (Ripple Labs), the new SEC attempted to reduce the fine imposed by the court, easing the penalty on the crypto company.

An investigation by The New York Times found that the SEC's leniency in these cases reflects a comprehensive shift in the federal government's attitude toward the cryptocurrency industry during President Trump's second term.

The SEC's collective retreat from a batch of lawsuits targeting a single industry is unprecedented.

However, The New York Times found that when Trump returned to the White House, the SEC slowed down more than 60% of ongoing cryptocurrency cases, including pausing lawsuits, reducing penalties, or directly dismissing cases.

The investigation pointed out that the dismissal of these cases is particularly abnormal. During Trump's tenure, the dismissal rate of SEC cases against cryptocurrency companies was significantly higher than that of other types of cases.

Although the specific details of these crypto lawsuits vary, the companies involved often share a common trait: they all have financial ties to Trump, who calls himself the "crypto president."

As the top federal agency regulating U.S. financial markets, the Securities and Exchange Commission (SEC) is no longer actively pursuing any company with public connections to Trump. The New York Times investigation found that the agency has taken a step back for all companies linked to the Trump family's crypto business or those that have funded his political endeavors. The only remaining crypto cases pursued by the SEC are against obscure defendants with no apparent connection to Trump.

Case Handling Statistics

-

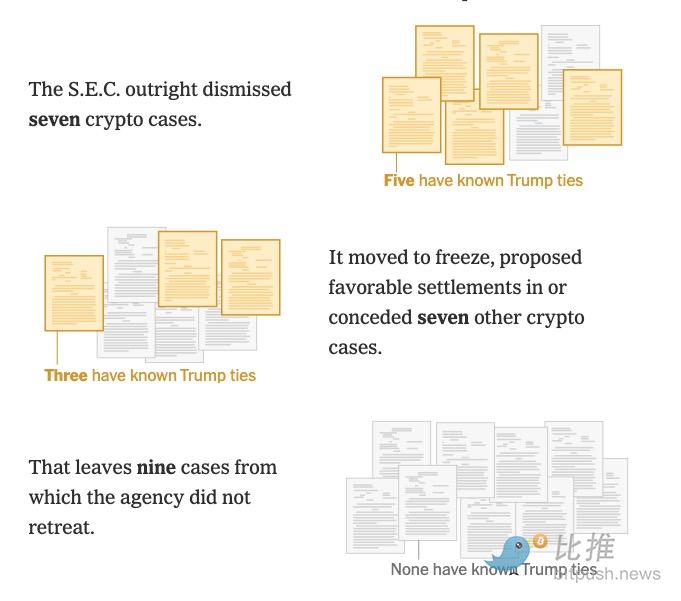

Cases directly dismissed: 7

└ 5 of these involved defendants with public connections to Trump -

Cases with mitigating measures: 7

└ Including suspending asset freezes, offering favorable settlements, or making substantial concessions

└ 3 of these involved defendants with public connections to Trump -

Cases maintaining original litigation stance: 9

└ No public connection to Trump has been found in any of these so far

The SEC stated in a declaration that political favoritism "has nothing to do" with their approach to crypto enforcement, claiming the agency's shift was due to legal and policy reasons, including concerns about its authority to regulate the industry. The SEC noted that long before Trump embraced the industry, its current Republican commissioners fundamentally disagreed with bringing most crypto cases and emphasized that they "take securities fraud and investor protection seriously."

There is no indication that the president pressured the agency to go easy on specific crypto companies. We also found no evidence that these companies attempted to influence the cases against them through donations or business ties to Trump, some of which were established after the SEC's policy shift.

However, Trump is both a participant in the crypto industry and its top decision-maker, profiting from companies regulated by his own administration. The fact that many companies sued by the SEC have connections to him highlights the conflict of interest inherent in a president pushing policies that serve his own interests.

At the start of his second term, the White House announced the president would "halt the radical enforcement actions and regulatory overreach that are stifling crypto innovation."

Although the SEC's abandonment of some individual crypto cases had previously drawn public attention, The New York Times' analysis of thousands of court records and dozens of interviews reveals the unprecedented scale of this year's regulatory retreat and the enormous benefits it has brought to Trump's industry allies.

All defendants named in The New York Times investigation denied any wrongdoing, with many companies insisting they were only accused of technical violations. Some companies whose cases were dismissed by the agency had no apparent connection to the president.

Crypto companies welcomed what Trump's newly appointed SEC chairman, Paul S. Atkins, called a "new day" for the industry.

White House press secretary Karoline Leavitt dismissed any suggestion of a conflict of interest for Trump or his family. She said Trump's policies were "fulfilling the president's promise to make America the crypto capital of the world, bringing innovation and economic opportunity to all Americans."

The Trump administration has broadly relaxed crypto regulations, including the Justice Department shutting down a crypto enforcement unit. But this year's changes at the SEC mark a particularly sharp reversal.

According to The New York Times' analysis, during the Biden administration, the SEC initiated more than two crypto cases per month on average (whether in federal court or its internal legal system). Even during Trump's first term, the agency brought about one case per month on average, including the high-profile case against Ripple.

In contrast, since Trump returned to the White House, the SEC has not initiated a single crypto case (as defined by The New York Times), although it has continued to file dozens of lawsuits against other types of defendants.

Number of Cryptocurrency Enforcement Cases Initiated by the U.S. SEC Under Different Administrations

-

Trump's First Term: 50 cases

-

Biden Administration: 105 cases

-

Trump's Second Term (Current): 0 cases

Trump's newly appointed SEC chairman, Paul S. Atkins, argued in a statement that his agency was merely reining in the previous administration's overzealous approach to the crypto industry. He insisted that the Biden-era SEC used its enforcement power to create new policy.

Atkins said: "I have been clear that we will end regulation by enforcement."

Although crypto companies welcomed what Atkins called a "new day" for the industry, career SEC lawyers responsible for bringing some of these cases expressed concern about the pullback. They worry that the agency, created during the Great Depression to protect investors and oversee markets, is emboldening the crypto industry in ways that could harm consumers and threaten the broader financial system.

Christopher E. Martin, a senior SEC litigation attorney who led a case against a crypto company, chose to retire after the agency dropped the lawsuit this year.

He described the SEC's broad retreat as "total surrender," saying: "They really threw investors to the wolves."

The End of Tough Regulation

Inside the glass-walled Washington headquarters of the SEC, the agency's crackdown on cryptocurrency was running out of steam by the end of last year.

Then-Chairman Gary Gensler (Gary Gensler, appointed by the Biden administration) wanted to advance multiple cryptocurrency investigations, but he was out of time.

Trump had won re-election, having just announced a cryptocurrency venture involving him and his family—"World Liberty Financial" (World Liberty Financial)—and vowed to rein in the SEC.

Trump had not always been pro-crypto. During his first term, he tweeted that cryptocurrency was based on "thin air" and could facilitate drug deals and other illegal activities.

His first SEC also took a hard line. The agency established a unit dedicated to combating cyber and cryptocurrency misconduct and filed dozens of cases.

Under Biden, the agency's efforts intensified severalfold. By 2022 (the year the giant crypto exchange FTX collapsed), the SEC's crypto unit had nearly doubled to about 50 lawyers and industry experts.

Under both presidents, the SEC argued that since investors could put their life savings into cryptocurrency, they deserved to understand the risks.

But a thorny legal question always loomed over the agency: Did it even have the authority to bring these cases? The answer depended on whether cryptocurrencies were securities, a modern variation of stocks and other financial instruments.

The SEC argued that many cryptocurrencies were effectively securities, so companies like crypto exchanges and brokers had to register with the agency, submit extensive public disclosures, and in some cases undergo independent reviews. Failure to register meant the agency could sue them for violating securities laws.

The industry countered that most cryptocurrencies were not securities but another asset class requiring a specialized set of rules the agency had not established.

Blockchain Association CEO Summer Mersinger said: "We are not seeking to be unregulated; we are seeking clear regulation we can operate under."

Last year, the tide began to turn for the crypto industry as Trump transformed from a crypto skeptic to an evangelist.

In a July 2024 speech, he promised crypto enthusiasts the "persecution" of their industry would end, saying "on my first day in office, I will fire Gary Gensler."

The SEC is an independent agency with five presidentially appointed commissioners, including a chair, whose views often reflect the administration that appointed him. Commissioners vote on whether to bring, settle, or dismiss cases, but career enforcement officials handle the actual investigations. This system allows for shifts in regulatory focus but has traditionally avoided wild swings based on political whims.

But when Trump won the election a second time, a sobering reality set in at the SEC. Gensler announced his departure shortly after the election.

And the cryptocurrency enforcement unit, once seen as a career springboard, suddenly became a "liability" overnight.

According to people familiar with the matter, during the presidential transition, Sanjay Wadhwa, the enforcement director under Gensler, pleaded with the enforcement team in internal meetings to "finish the work the people pay us to do." (The people spoke on the condition of anonymity because they were discussing internal meetings.)

Nonetheless, some staff members pulled back.

A senior leader in the crypto team took a previously unannounced multi-week vacation and did not respond to emails about cases, the people said.

Another senior official refused to sign off on one of the few crypto cases the agency brought after the election.

Other officials simply stopped working on their crypto cases, thwarting Gensler's final efforts.

Victor Suthammanont, who worked at the agency for a decade, most recently as an enforcement adviser to Gensler, said staff had persevered through the previous two transitions.

"But this transition was unlike any I've seen," said Suthammanont, who declined to discuss specific cases. "The atmosphere changed immediately."

Once Trump was sworn in, there was no turning back. He appointed one of the SEC's Republican commissioners, Mark T. Uyeda, as acting chairman until the president's nominee, Atkins, was confirmed by the Senate.

Uyeda had long opposed the agency's approach to crypto cases. In a statement to The New York Times, he said Gensler was using novel theories "not supported by existing law."

But in a 2022 speech, Gensler made clear he held the opposite view. "When a new technology comes along, our existing laws don't just disappear," he said.

By early February, Uyeda had sidelined Jorge G. Tenreiro, who had helped lead the crypto unit and supervised many of the cases, as the litigation chief. Tenreiro was reassigned to the information technology division, a move seen within the SEC as a demotion.

Without Tenreiro, the agency began dropping investigations into crypto companies facing potential lawsuits. While some investigations continued, at least 10 companies announced they were no longer under scrutiny, including one just last week.

"Nothing to Negotiate"

Uyeda soon faced a tougher decision: what to do with the Biden-era lawsuits the agency was still pursuing in court.

While the SEC often drops investigations, dismissing ongoing cases is rare and requires approval from the agency's commissioners.

In one of the most prominent crypto cases, the SEC sued the largest U.S. crypto exchange, Coinbase, accusing it of failing to register with the agency. The company mounted an aggressive defense during the Biden administration, persuading the presiding judge to let a higher court review the case before trial.

Now, with the SEC under Trump's administration, Coinbase was among the first to seek dismissal.

Traditionally, the SEC chairman's office would stay out of such negotiations, leaving them to career officials overseeing the cases. But an official from Uyeda's office attended some negotiations with Coinbase, as well as meetings with enforcement lawyers.

Coinbase's chief legal officer, Paul Grewal (Paul Grewal), said in an interview: "We were very careful to ensure the acting chairman's office was kept fully apprised and informed of everything that was happening."

Uyeda said his staff's attendance at these meetings was "entirely appropriate."

The SEC under Uyeda was initially reluctant to drop the case. They initially offered Coinbase only a pause in the litigation, according to a person familiar with the matter.

But Coinbase rejected a delay.

The SEC then made a more generous offer: It would dismiss the case on the condition that the agency retained the right to revive the lawsuit if leadership changed its mind.

Coinbase wouldn't settle for that, either.

Grewal, a former federal judge, said: "We were very clear—either they surrender or we litigate, because we had nothing to negotiate."

The SEC ultimately conceded. By then, with Gensler and another Democratic commissioner gone, the agency was down to two Republican commissioners and one Democrat.

Uyeda, speaking without referencing any specific decision, said, "these cases should not be continued, particularly if the S.E.C. is going to disavow their underlying theory in the near future."

But the remaining Democratic commissioner, Caroline A. Crenshaw, said in an interview that the agency had given the crypto industry a pass across the board.

She said: "They can essentially do whatever they want."

Shift in Attitude

The crypto industry viewed the Coinbase dismissal as a white flag of surrender.

Lawyers for other crypto companies sought similar settlements. By the end of May, the agency had dismissed six more cases.

The New York Times' analysis of court records highlights how unusual this was.

During the Biden administration, the SEC did not voluntarily dismiss a single pending crypto case from Trump's first term, although it did dismiss a case against a deceased defendant and part of another case after unfavorable court rulings.

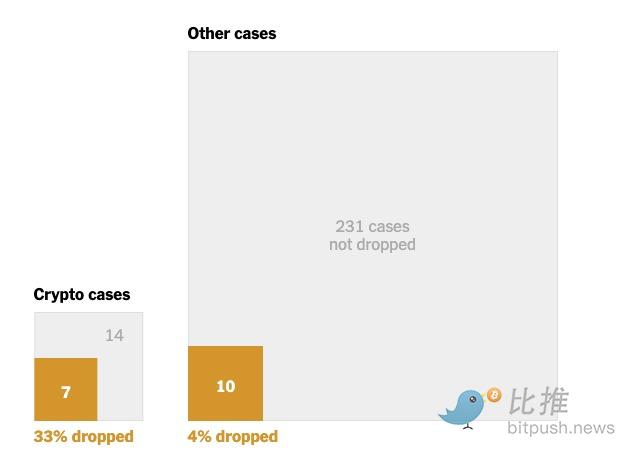

Yet, during Trump's second term, the agency dismissed 33% of the Biden-era crypto cases it inherited. For cases in other industries, the dismissal rate was just 4%.

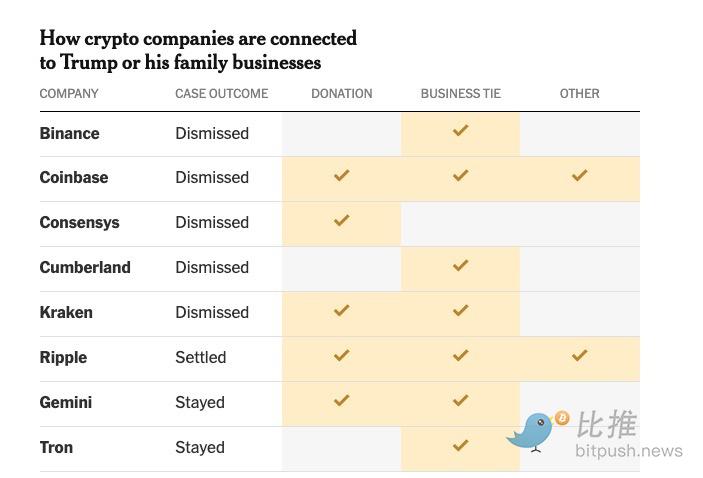

Despite vowing to continue pursuing fraud, the SEC still dropped its lawsuit against Binance. In that case, the SEC accused two related entities of fraudulently misleading customers about their efforts to prevent manipulative trading.

The SEC also asked a judge to freeze a fraud case against crypto billionaire Justin Sun and his Tron Foundation (Tron), one of four cases the agency handled on its way to a settlement. Agency officials have yet to announce a resolution in that case.

In total, the Trump administration inherited 23 cryptocurrency-related cases from the SEC: 21 from the Biden era and 2 dating back to Trump's first term. The agency has taken a lenient approach to 14 of these 23 cases.

In eight of these cases, the defendants established connections with the president or his family before or shortly after the cases were resolved.

For example, Justin Sun purchased $75 million worth of "World Liberty Financial" digital tokens. His company, Tron, did not respond to multiple requests for comment. In court filings, Sun and Tron said the SEC lacked evidence of fraud and jurisdiction to sue.

Just weeks before the Binance case was dropped, the company participated in a $2 billion business deal using "World Liberty Financial's" digital currency. The deal is expected to generate tens of millions of dollars in annual revenue for the Trump family.

A spokesperson for "World Liberty Financial" said, "There is not the slightest connection between World Liberty Financial and the U.S. government," adding that the company "has no influence over the policies or decisions of the executive branch."

Binance said in a statement that the SEC's action against it was "a product of the war on crypto."

In March, the SEC abandoned a case accusing crypto trading firm Cumberland of acting as an unregistered securities dealer.

About two months later, its parent company, DRW, invested nearly $100 million in Trump's family media company.

DRW officials said the company only learned of the investment opportunity after the case concluded and that the dismissal was solely because the allegations were unfounded.

In the case against Ripple (which donated nearly $5 million to Trump's inauguration), the SEC tried to undo its own efforts.

During Trump's first term, the SEC accused Ripple of depriving investors of important information when selling its crypto tokens. Last year, after dismissing some of the SEC's claims, a federal judge ordered Ripple to pay a $125 million fine for some securities violations.

However, after Trump returned to the White House, the SEC sought to reduce the fine to just $50 million. The judge chastised the government's change of heart and rejected the new settlement.

Ripple had argued to the judge that it deserved a lower fine, partly because the SEC had moved to dismiss complaints against other similar crypto companies. Ripple ultimately paid the full fine.

The president's media company said in July it plans to include Ripple's cryptocurrency in an investment fund open to the public.

In an interview, Republican commissioner Hester M. Peirce, who leads the SEC's newly established crypto task force, said retreating from many cases was about correcting errors. She said these cases should never have been brought.

"I would say the radical action was in the last few years, bringing cases where we didn't have the legal basis," she added, saying she believed the cases stifled legitimate innovation.

Peirce said politics or financial considerations played no role. She said: "We are making decisions based on the facts and the specifics of the situation, not based on 'who knows whom.'"

"Plenty of Cash"

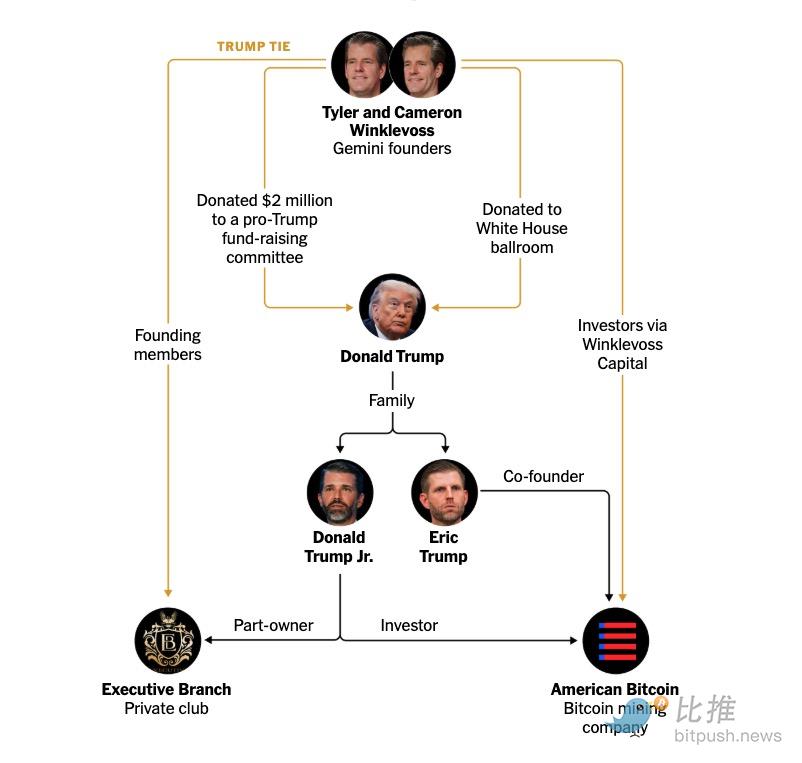

Few players in the crypto industry are closer to Trump than twins Tyler and Cameron Winklevoss.

The twins founded and operate Gemini Trust, and they donated to fundraising committees supporting Trump's re-election campaign and other Republican organizations.

They also provided funding for the construction of the White House ballroom (a private project of the president's).

They also supported a new exclusive club in Washington—"Executive Branch"—partly owned by the president's eldest son, Donald Trump Jr.

Furthermore, the twins' investment company recently invested in a new crypto mining company called "American Bitcoin";

The president's second son, Eric Trump, is a co-founder and chief strategy officer of the company, and Donald Trump Jr. is also an investor.

The president has repeatedly praised the twins, describing them as high-IQ smart male models.

Trump said at a White House event: "They've got the looks, they've got the talent, and they've got plenty of cash."

But Gemini Trust had legal troubles.

In December 2020, Gemini and another company, Genesis Global Capital, agreed to offer Gemini customers the opportunity to lend their crypto assets to Genesis. In turn, Genesis lent these assets to larger players.

Genesis paid interest to customers, who were promised they could withdraw their assets at any time, while Gemini received a cut for acting as the intermediary. Gemini promoted the program as a way for account holders to earn up to 8% interest.

San Diego data scientist Peter Chen said in an interview that he trusted Gemini enough to hand over more than $70,000. He said: "They gave me the impression they were clean, followed the rules, and were one of the most heavily regulated of all the crypto companies."

Then, in late 2022, Genesis, facing bankruptcy, froze the accounts of 230,000 customers, including Peter Chen's.

A 73-year-old grandmother pleaded with Gemini to return her $199,000 life savings. "I am finished without that money," she wrote.

Genesis reached a $2 billion settlement with New York in May 2024, and customers eventually got their money back. Gemini also reached its own agreement with the state, agreeing to pay up to $50 million if needed to cover any remaining losses. It denied any wrongdoing, blaming the disaster on Genesis, and pointed out that ultimately no customer lost money.

But the SEC also sued both companies, accusing them of selling cryptocurrency without registration. On social media, Tyler Winklevoss called the lawsuit a "made-up parking ticket."

Genesis settled, but Gemini fought on until this April, when the SEC moved to freeze the case to pursue a settlement. The agency disclosed in September that it had reached a deal with Gemini, but it still needed a vote by the commissioners.

The SEC told the presiding federal judge the agreement would "fully resolve this litigation."

Twitter:https://twitter.com/BitpushNewsCN

BitPush TG Discussion Group:https://t.me/BitPushCommunity

BitPush TG Subscription: https://t.me/bitpush