Author: Ma He, Foresight News

Even one of the most successful public chains, Solana, has encountered a winter moment.

On February 5th, during the market crash, Solana's token SOL once fell to $67, hitting a new low since December 2023. As of now, SOL is trading at $80, with a 24-hour decline of 3.57%. On a monthly chart, SOL has been declining for five consecutive months since its high in October 2025, with a maximum drop of over 71% during this period. The floor price of its most famous NFT, Mad Lads, once dropped to 22 SOL, approximately $1,760, while at its peak, this NFT was worth over $40,000.

Looking back during this bull market, SOL rose from a low of $8 to $295, performing quite impressively among public chains. Coupled with the explosion of the Meme sector, even U.S. President Donald Trump chose to launch his token first on the Solana network, creating countless wealth stories during this period.

However, as the market turns bearish, with token prices falling, TVL halved, on-chain transaction volume sharply decreasing, and the growth flywheel stalling, Solana also faces its own various problems.

Meme Craze Ends

This cycle, the Meme craze began on Solana. From late 2024 to early 2025, Solana sparked the "Meme Summer" with the Pump.fun platform, with the number of new tokens issued daily once exceeding ten thousand, and transaction volume peaking at over $6 billion. Meme coins like Dogwifhat and Bonk saw their market caps soar, pushing Solana's overall activity to its peak. This reached its zenith when Trump issued TRUMP, creating a historic high of $295. However, as various frauds emerged and the wealth effect diminished, starting from mid-2025, the Meme craze began to cool, with many projects having a graduation rate of less than 2%, and capital began to outflow.

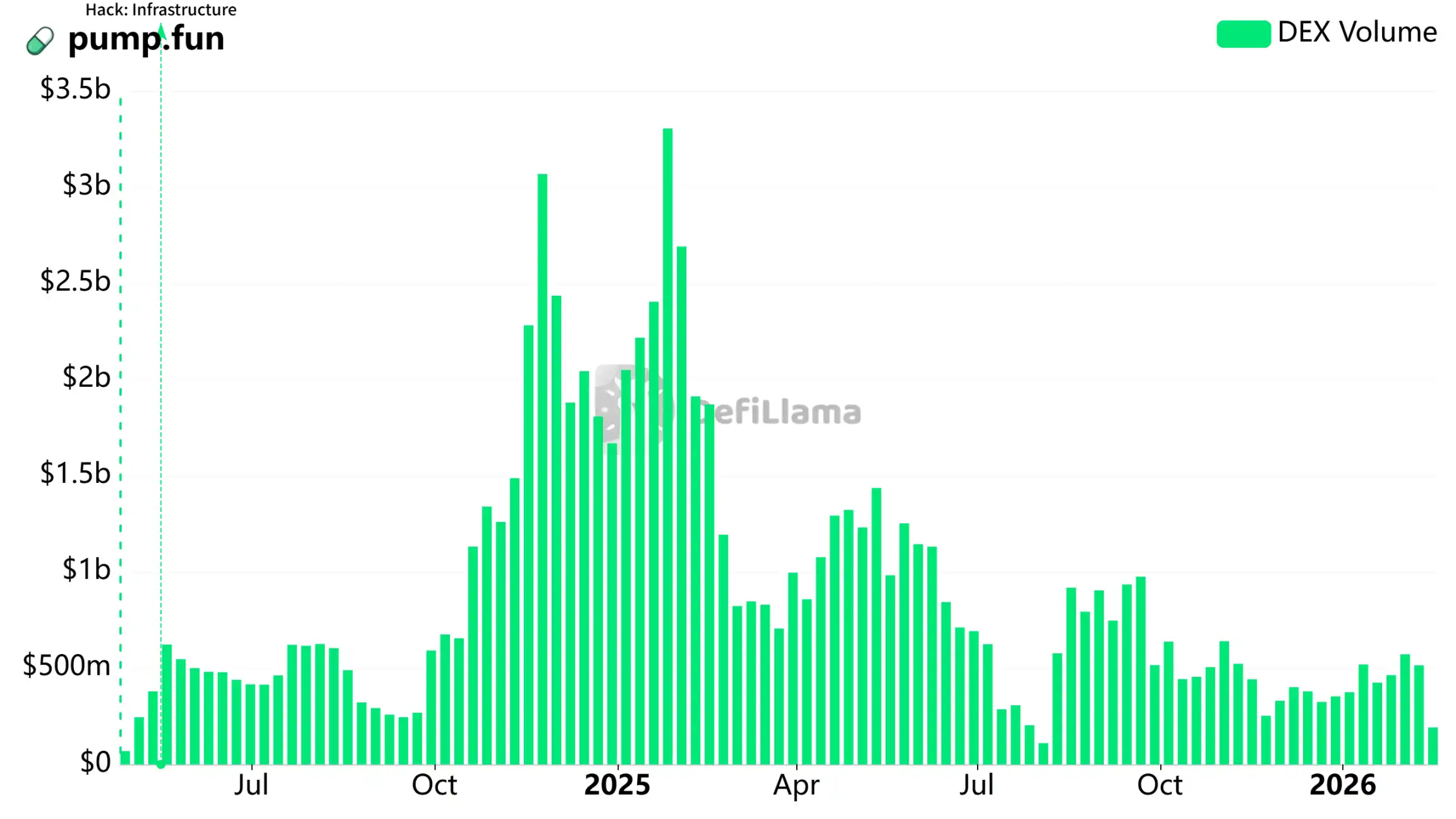

Defilama data shows that around the beginning of 2025, the trading volume of the Meme platform pump.fun reached a historical high. Weekly trading volume exceeded $3 billion twice, followed by a continuous decline. In early 2026, its trading volume hovered around $500 million, only one-sixth of its peak.

At the same time, some Meme traffic shifted to BNB Chain. BNB Chain rapidly rose through the Four.Meme platform. In the second half of 2025, Chinese-themed Memes like "Binance Life" and "I'm F*cking Coming" sparked FOMO sentiment. BNB Chain's Meme market cap grew from almost zero to hundreds of millions of dollars, with a 24-hour trading volume reaching $460 million. In comparison, although Solana's Meme market cap still amounts to billions of dollars, its growth has stagnated, with many projects falling over 95% from their peaks.

In October 2025, BNB Chain once replaced Solana on the trending Meme list, showing obvious capital rotation: when BNB Chain Memes surged, Solana's capital contracted; after BNB Chain receded, capital partially flowed back, but the momentum had weakened. Furthermore, under the influence of key figures like CZ/He Yi, BNB Chain saw short-term traction, while Solana's Pump.fun, despite its first-mover advantage, weakened due to narrative exhaustion and a lack of incremental funds.

The end of the Meme wave means that the demand for its public chain token has also decreased simultaneously.

Public Chain Narrative Cools

Additionally, the overall cooling of the public chain narrative has further weakened Solana's ecosystem expansion plans. Between 2025 and 2026, the crypto market retreated from early high leverage and excessive narrative expansion. Many weak narratives, such as celebrity tokens and the Meme craze, quickly faded, shifting focus to areas with more practicality and institutional support. Solana's narrative as a "high-speed public chain" once attracted developers, but as the market entered the "deep water of value," investors tended to prefer mainstream assets like Bitcoin and Ethereum for their "digital gold" or "settlement layer" positioning, leading to a continued overall bear market and intensified capital outflows from Solana.

This narrative fatigue reflects that public chain competition has shifted from pure TPS competition to ecosystem maturity and regulatory adaptability. Solana's previous TPS and ecosystem advantages have been diluted. Whether in terms of Memes or airdrop incentives, Solana's appeal to new users has weakened.

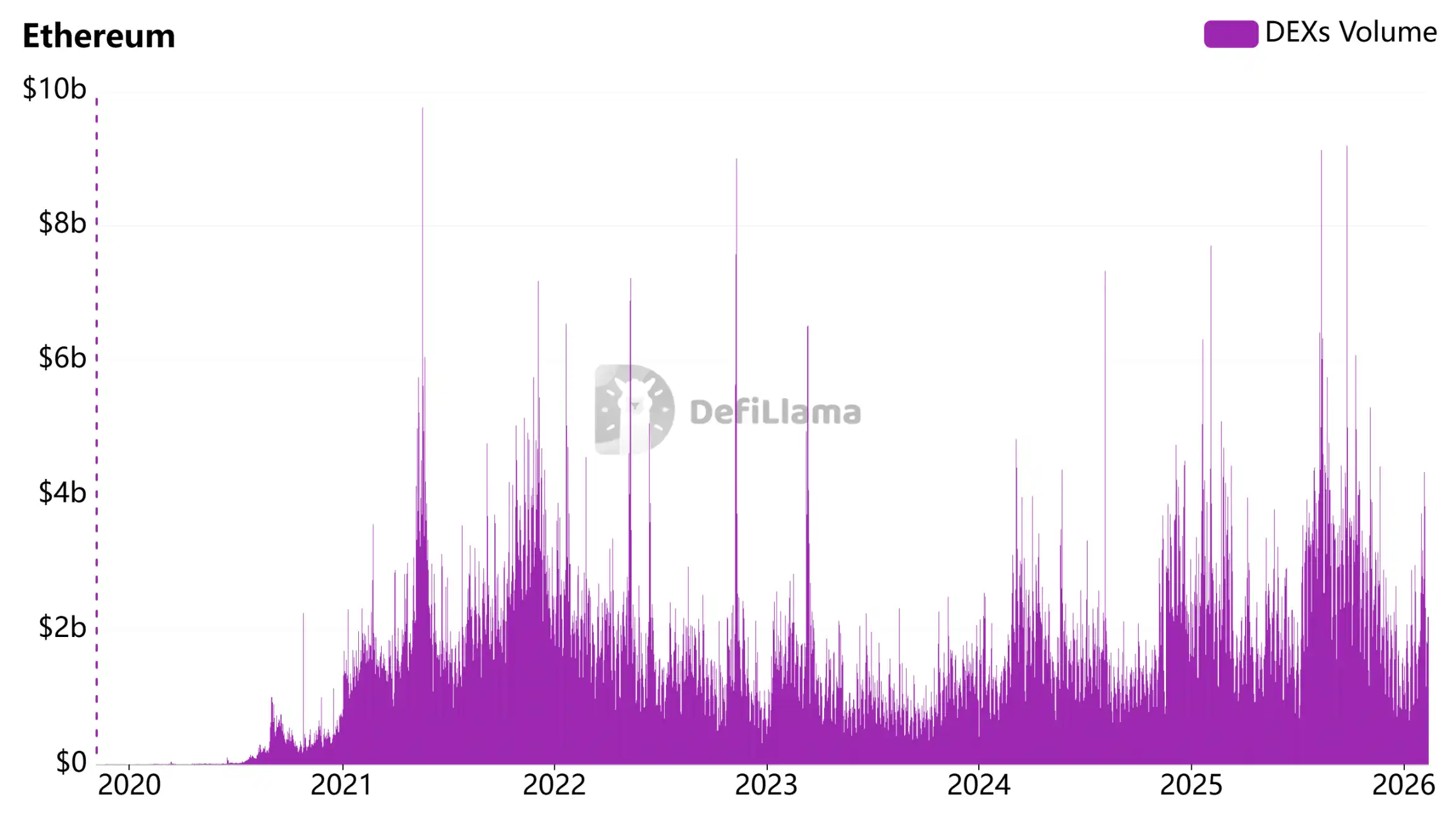

Meanwhile, the significant speed improvement of the Ethereum mainnet has also weakened Solana's core advantage. Through the Fusaka upgrade in 2025, Ethereum increased data blob capacity from 3 to 6-9 and introduced the PeerDAS mechanism, significantly reducing transaction fees and increasing throughput. Transaction volume and active addresses subsequently rebounded.

Data shows that DEX trading volume on Ethereum overall rose at the end of 2025. Entering 2026, the Glamsterdam upgrade will achieve near-perfect parallel processing, further accelerating block verification and reducing fees, bringing the mainnet closer to an "operating system" level. These improvements have brought Ethereum mainnet's TPS and cost close to Solana's levels, while retaining higher security and decentralization, reducing the necessity for users to switch to Solana.

Another rising competitor, Base, is also growing rapidly, particularly attracting many users with AI tokens. According to DefiLlama data, its TVL is still maintained at a high level of $4 billion.

Under the tokenization热潮, RWA (Real World Assets) activities occur more on Ethereum, further marginalizing Solana's ecosystem. As of February 12, 2026, data from rwa.xyz shows that RWA assets on the Ethereum mainnet amount to $14.9 billion, while Solana has only $1.7 billion, still a significant gap. The tokenization trend of RWA emphasizes stability and compliance, and Ethereum's leading position makes it difficult for Solana to get a share.

Digital Asset Treasury Buyers Fail to Offset Overall Bearish Selling Pressure

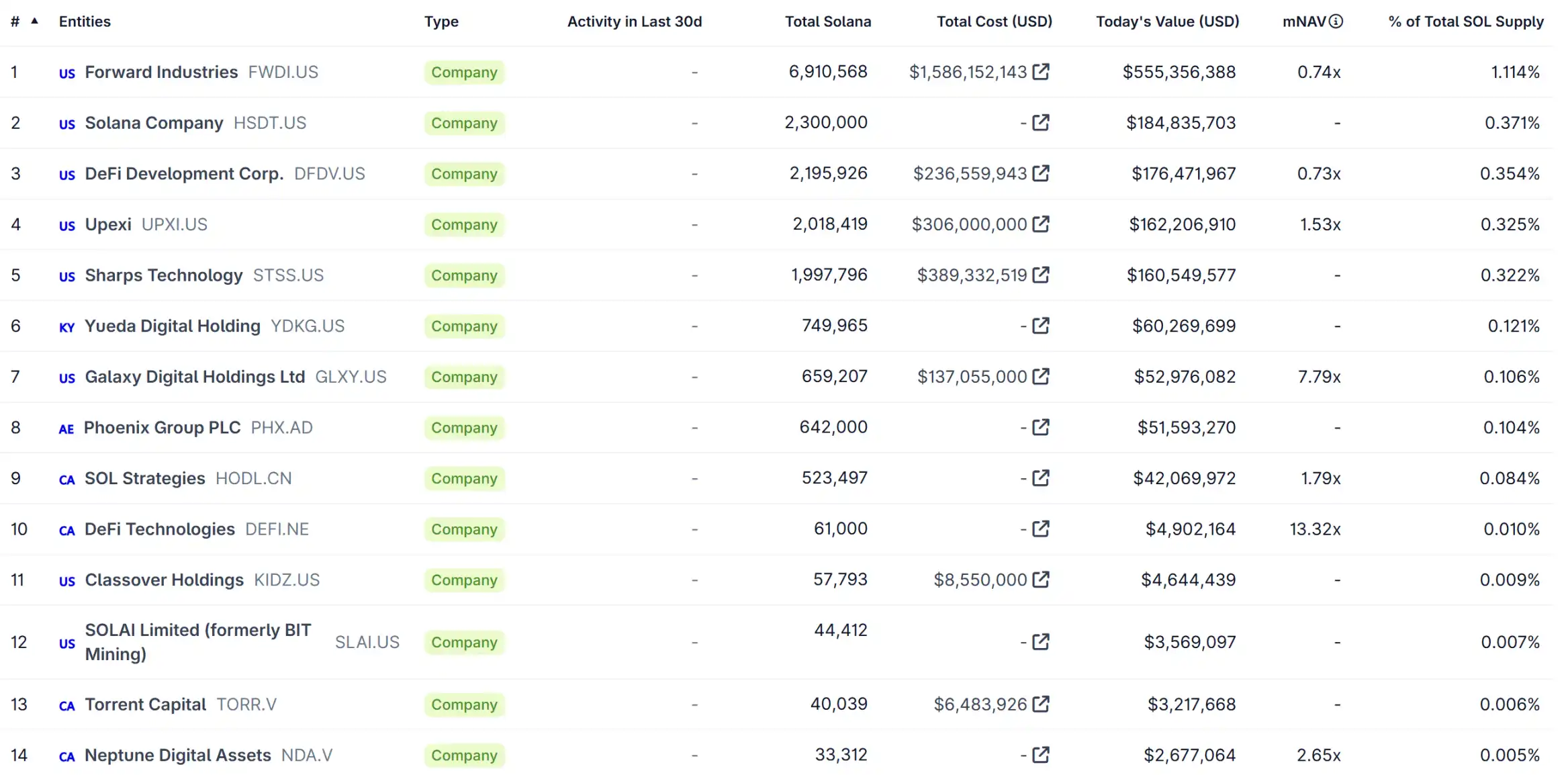

From the perspective of Digital Asset Treasuries (DAT), in 2025, the DAT model was once popular. Many publicly traded companies like Forward Industries, Upexi, and Sharps Technology purchased large amounts of SOL as treasury assets through private financing or debt issuance.

Entering 2026, as the price of SOL fell from its 2025 peak of around $200 to about $80, the market capitalization of these DAT companies shrank significantly. For example, Forward Industries spent $158 million to purchase SOL, now worth only $55.5 million, shaking the confidence of some investors.

Furthermore, the DAT purchasing热潮 has weakened, with fewer new companies joining. Although the early purchased locked SOL reduces circulating supply, it has failed to offset the overall bearish market pressure.

Bitcoin and Ethereum prices have also been severely hit in the bearish market of recent months. BTC fell from $126,000 to the current $67,000, and ETH dropped from $4,900 to the current $2,000.

In January 2026, Solana founder toly once asked on X in Chinese: What do you think is the biggest challenge for Solana now? The comments section received a variety of feedback and answers, including: no direct exchange, users have less perception of other product ecosystems besides Memes, etc.

Perhaps Solana will find its own solutions.