On March 17, the U.S. Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC) jointly issued a document titled "Application of the Federal Securities Laws to Certain Types of Crypto Assets and Certain Transactions Involving Crypto Assets." This 68-page regulatory document systematically addresses core issues such as crypto asset classification, securities qualification, and the compliance of typical transactions, marking a shift in U.S. crypto asset regulation from the long-standing "regulation by enforcement" model to a rule-based, transparent regulatory framework. This article by Beosin will interpret the core content of the report to help industry participants gain an in-depth understanding of the latest U.S. regulatory policies and compliance guidelines.

I. Regulatory Background

For a long time, U.S. crypto asset regulation has lacked clear rules. The SEC primarily used enforcement actions rather than a dedicated regulatory framework to define the securities attributes of crypto assets, leading to extremely high compliance uncertainty for participants in the crypto market. To change this situation, the SEC established the Crypto Task Force in 2025 and launched "Project Crypto," aiming to collaborate with the CFTC to unify federal regulatory standards and provide clear legal boundaries for crypto assets.

The core goal of this document is to provide the crypto market with a set of clear classification standards and legal interpretations. The document clearly classifies crypto assets, delineates the boundaries between securities and non-securities assets, qualifies common on-chain activities (PoW mining, PoS staking, liquid staking, token wrapping, airdrops), and indicates that the core principle of regulation should be "economic substance" rather than the name or form of the asset.

Original Content

II. Five Major Classifications of Crypto Assets

The document divides all crypto assets into five major categories, each subject to different regulatory rules, fundamentally changing the previous ambiguous qualification model.

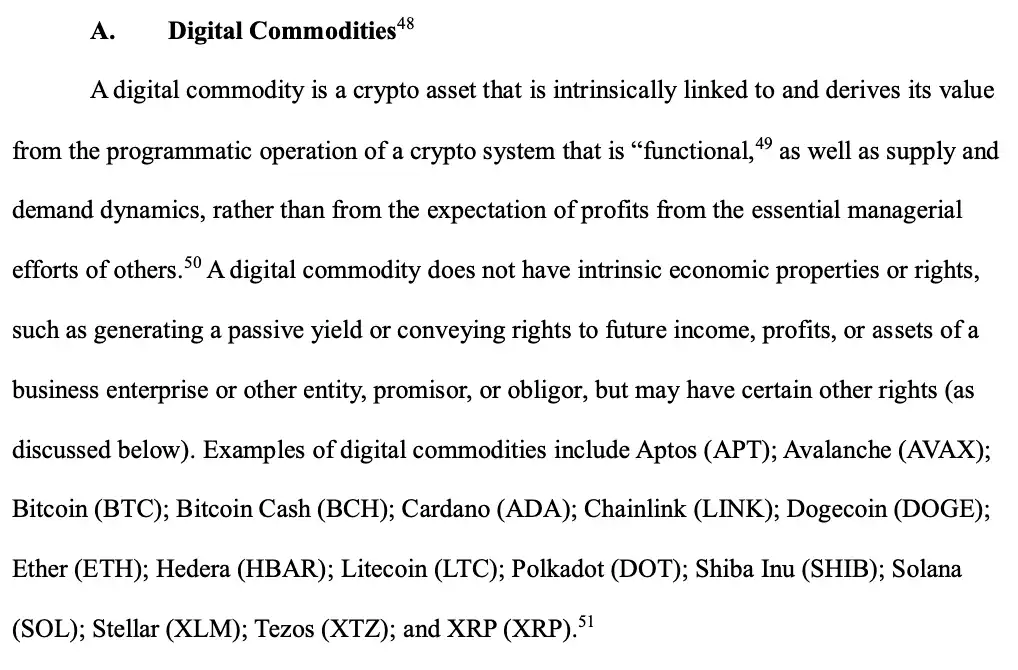

1. Digital Commodities

Digital commodities themselves are not securities. Their value derives from the programmatic operation of a decentralized system and market supply and demand, rather than relying on the managerial efforts of others.

● Core Characteristics: Intrinsically related to a functional crypto system

● Examples: The document explicitly lists assets that are digital commodities, including: Bitcoin (BTC), Ether (ETH), Solana (SOL), XRP (XRP), Cardano (ADA), Avalanche (AVAX), Dogecoin (DOGE), Polkadot (DOT), etc.

● Regulatory Authority: CFTC

● Compliance Requirements: Meet the commodity definition under the Commodity Exchange Act and must comply with the Commodity Exchange Act

Original Content

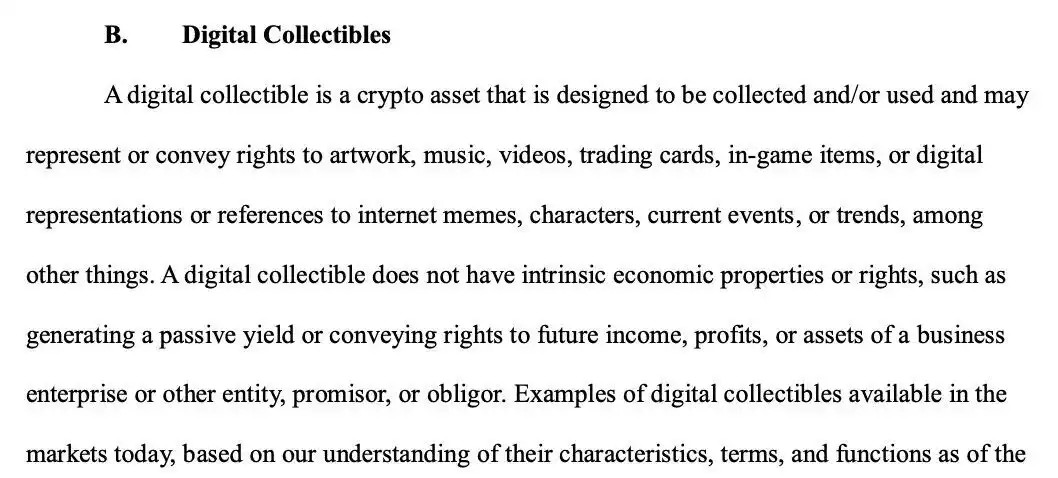

2. Digital Collectibles

Includes NFTs and Memecoins. Since their value primarily stems from artistic, entertainment, or social significance and lacks the characteristics of a security, they are not securities.

● Core Characteristics: Intended for collection or use, representing rights to artworks, game items, etc., with no correlation to corporate profits

● Examples: The document explicitly lists CryptoPunks, Chromie Squiggles, FanTokens, and Memecoins

● Regulatory Authority: No specific regulation

Initial issuance does not require securities registration, but if it involves the fractionalization of digital collectibles, it may constitute a security and be subject to SEC regulation.

Original Content

3. Digital Tools

Refers to assets used to obtain services or functions within specific applications; they are not securities themselves.

● Core Characteristics: Voucher-like assets with practical functions, such as memberships, tickets, domain names, etc.; value derives from functionality

● Examples: Ethereum Name Service (ENS), CoinDesk conference NFT tickets

● Regulatory Authority: No specific regulation

Original Content

4. Stablecoins

According to the GENIUS Act, "regulated payment stablecoins" that meet specific conditions are not considered securities. The issuance and redemption of such stablecoins do not require registration with the SEC. However, it is important to note that payment stablecoins must meet the requirements of the GENIUS Act, while non-payment stablecoins need to be judged based on economic substance to determine if they constitute securities.

5. Digital Securities

i.e., "tokenized securities," which are digital representations of traditional securities and legally qualify as securities.

● Core Definition: Tokenized financial instruments possessing the core characteristics of securities

● Examples: Tokenized stocks

● Regulatory Authority: SEC

● Compliance Requirements: Must comply with the registration requirements of the Securities Act of 1933; rules on信息披露 (information disclosure) and investor protection apply

III. Key Interpretation of "Investment Contract": Separation of Crypto Assets and Investment Contracts

(1) Refined Application of the Howey Test

This document does not replace the classic Howey test but provides more refined guidance tailored to the characteristics of crypto assets: A crypto asset transaction constitutes an "investment contract" (security) only if it simultaneously satisfies three elements:

● Investment of Money: The investor invests money or valuable consideration (including crypto assets)

● Common Enterprise: The investor's profits are highly intertwined with the operational efforts of the issuer or a third party

● Expectation of Profit: The investor reasonably expects profits derived primarily from the "essential managerial efforts" of the issuer, rather than their own labor or changes in market supply and demand

The document specifically clarifies the criteria for judging "essential managerial efforts": including but not limited to project development, technological upgrades, business promotion, and other key activities affecting the project's success; purely administrative or ministerial tasks (such as node maintenance, transaction settlement) do not constitute this element.

(2) "Securitization" Risk and De-securitization of Non-Security Crypto Assets

This is the most innovative interpretation in this document: Non-security assets (e.g., digital commodities) can be sold as part of an investment contract, but the asset itself does not thereby become a security:

Original Content

1. Securitization Triggering Conditions

When an issuer, through whitepapers, social media, or other channels, explicitly promises to undertake essential managerial efforts to increase the asset's value and induces investors to purchase based on this promise, the non-security crypto asset will be deemed the vehicle of an "investment contract" and must comply with securities regulations.

2. Three Scenarios for De-securitization

● Promise Fulfilled: The issuer completes the promised essential managerial efforts (e.g., decentralized deployment of the project, completion of功能开发 (function development)) and publicly discloses this;

Original Content

● Lapse of Time: Long-term failure to fulfill promises with no clear plan for advancement, causing the investor's reasonable expectation to disappear;

● Inability to Fulfill: The issuer publicly and widely announces the abandonment of the promised essential managerial efforts, and the market is fully aware of this.

Original Content

This rule provides a clear compliance path for project teams in the crypto industry, allowing a project to start from a "securitized" financing stage and, through diligent development, achieve a transformation of its issued crypto asset from a security attribute to a non-security attribute.

IV. Qualification of Common Activities in the Crypto Industry

The policy clearly defines the compliance boundaries for common activities in the crypto asset market, such as mining, staking, token wrapping, and airdrops:

1. PoW Mining

● Activity Description: Miners provide computing power to maintain the network in a PoW network and receive rewards.

● Regulatory Determination: Does not involve the issuance or sale of securities.

● Analysis: Miners receive rewards through their own "administrative or ministerial" work (providing computing power), not passively from the "essential managerial efforts of others." Even joining a mining pool does not change this, as the pool operator's role is ministerial and does not constitute "essential managerial efforts."

Original Content

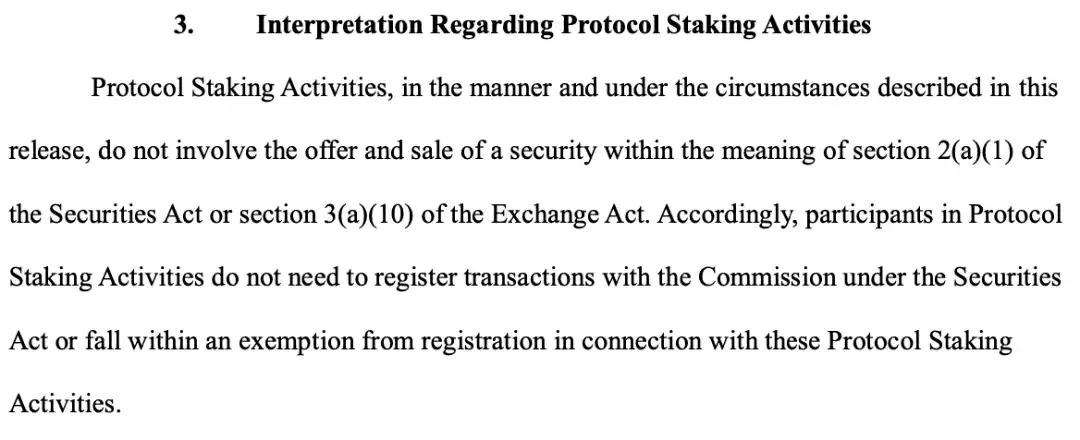

2. Protocol Staking

● Activity Description: In a PoS network, users stake tokens to run validation nodes or delegate to validation nodes, receiving staking rewards.

● Regulatory Determination: Does not involve the issuance or sale of securities.

● Analysis: Whether self-staking, delegating to a third party, or custody staking through a centralized institution, the essence is that users provide "staking services" to maintain network security and receive service compensation, rather than investing in a common enterprise. The document特别指出 (specifically points out) that providing additional services like slashing insurance or early unstaking does not affect its non-security nature.

Original Content

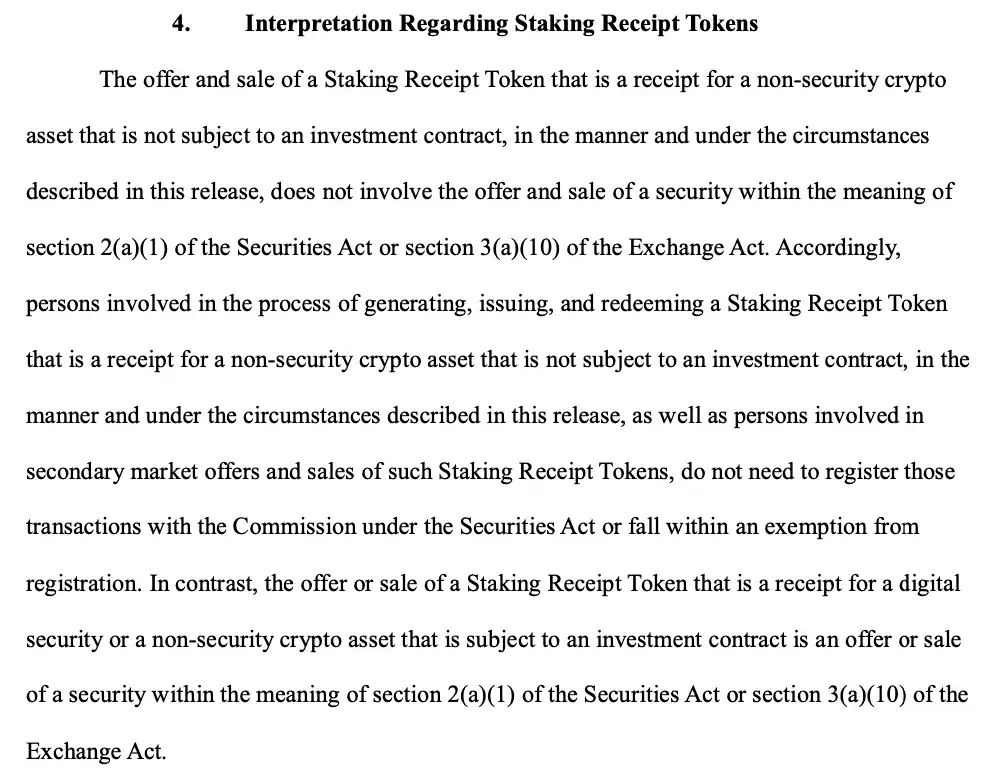

3. Staking Derivative Tokens

● Activity Description: Users deposit tokens into liquid staking platforms like Lido and receive tokens representing their staked assets and rewards (e.g., stETH).

● Regulatory Determination: As long as the underlying asset is a non-security digital commodity and the derivative token represents only the ownership and收益权 (profit rights) of the underlying asset, then the issuance and trading of this derivative token itself do not involve securities transactions. If the staking derivative token is for a digital security or a non-security crypto asset subject to an investment contract, it needs to be regulated by the SEC.

● Analysis: It is被视为 (considered) a "receipt," its value derived from the underlying asset, not the managerial efforts of the issuer.

Original Content

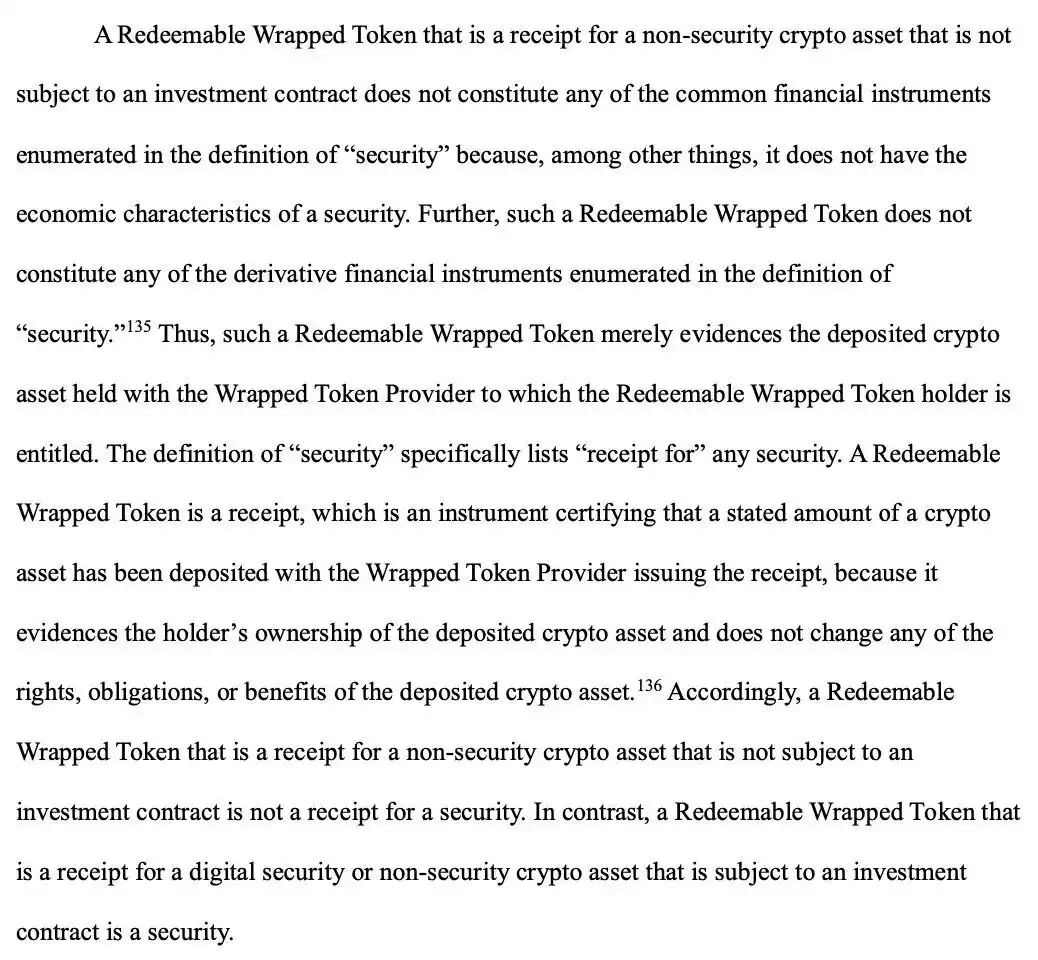

4. Token Wrapping

● Activity Description: Generating tokens on another blockchain (e.g., WBTC) that represent ownership of an asset from one blockchain (e.g., BTC) through a cross-chain bridge or custodian.

● Regulatory Determination: Similar to the judgment for liquid staking, as long as the underlying asset is a non-security digital commodity and is redeemable, without any promise of profit, then the issuance and trading of this wrapped token do not involve securities transactions. If the underlying asset is a digital security or a non-security crypto asset subject to an investment contract, it needs to be regulated by the SEC.

Original Content

5. Airdrops

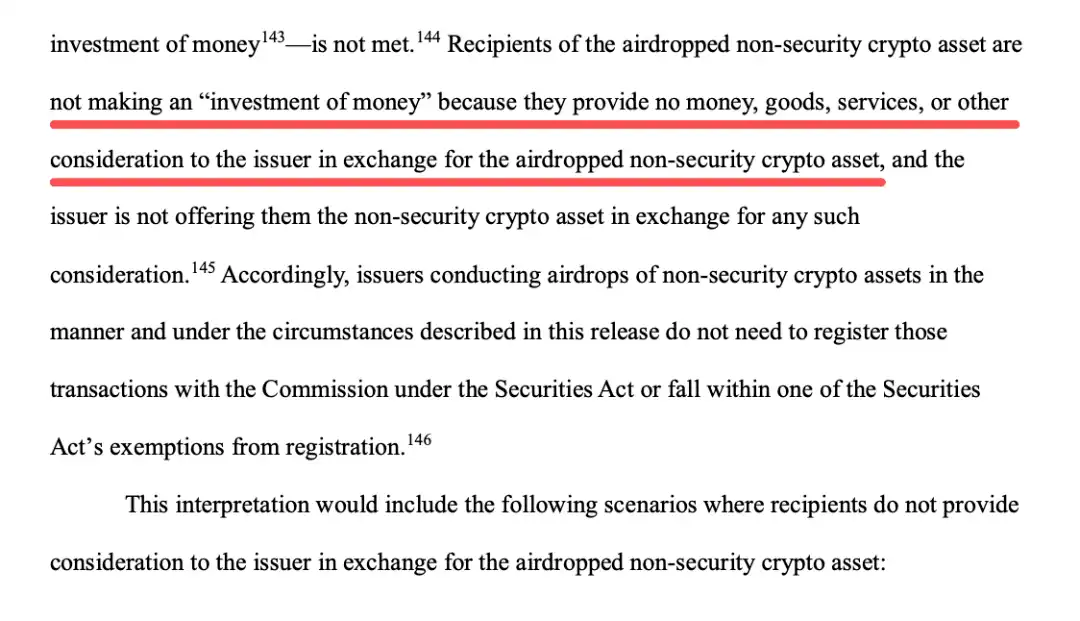

● Activity Description: A method where crypto asset issuers distribute their crypto assets to the market for free or for nominal consideration.

● Regulatory Determination: If the issuer airdrops non-security crypto assets to recipients, and the recipients have not paid money, provided goods or services, or given other consideration to the issuer in exchange for these airdropped assets, then such non-security crypto assets do not constitute an investment contract.

● Analysis: Airdrop activities do not satisfy the first element of the Howey test, "investment of money," even if airdropped to active users (as a reward for past actions). The core point is that the recipient did not provide any consideration to the issuer in exchange for the airdropped non-security crypto asset. The issuer may not need to register the transaction with the SEC under the Securities Act of 1933. However, this determination does not apply to airdrops of digital securities.

Original Content

It is important to note the policy's界定 (delineation) of "gray areas": If mining pools promise fixed returns, staking services provide capital preservation guarantees, or airdrops require recipients to complete specific promotional tasks, these may cross the compliance boundary and be deemed securities offerings.

Conclusion

The issuance of this document marks the completion of a key shift in U.S. crypto asset regulation from "regulation by enforcement" to "providing clear rules." Its core logic is: by clarifying classification standards and compliance boundaries, it reserves space for innovation in the crypto market. This U.S. regulatory interpretation and guidance place more emphasis on "functional regulation" and "substance regulation," stressing that regardless of the technological form, whatever economic function is具备 (possessed) will be subject to the corresponding regulatory rules. For market participants, this policy provides a clear compliance path,彻底厘清 (thoroughly clarifying) the long-standing debate over "assets versus securities." In the future, with the full生效 (effectiveness) of the GENIUS Act and the introduction of subsequent supplementary rules, the U.S. crypto asset regulatory framework will be further完善 (perfected) to achieve compliant operation of the crypto industry.