过去三年多,OpenAI几乎定义了大众对大模型的第一印象:4亿级周活、8520亿美元估值、以及AI全民入口ChatGPT。

在公众认知里,它本应该是商业化最先跑通的那家公司。

然而,市场数据却带来了不可能的反转:

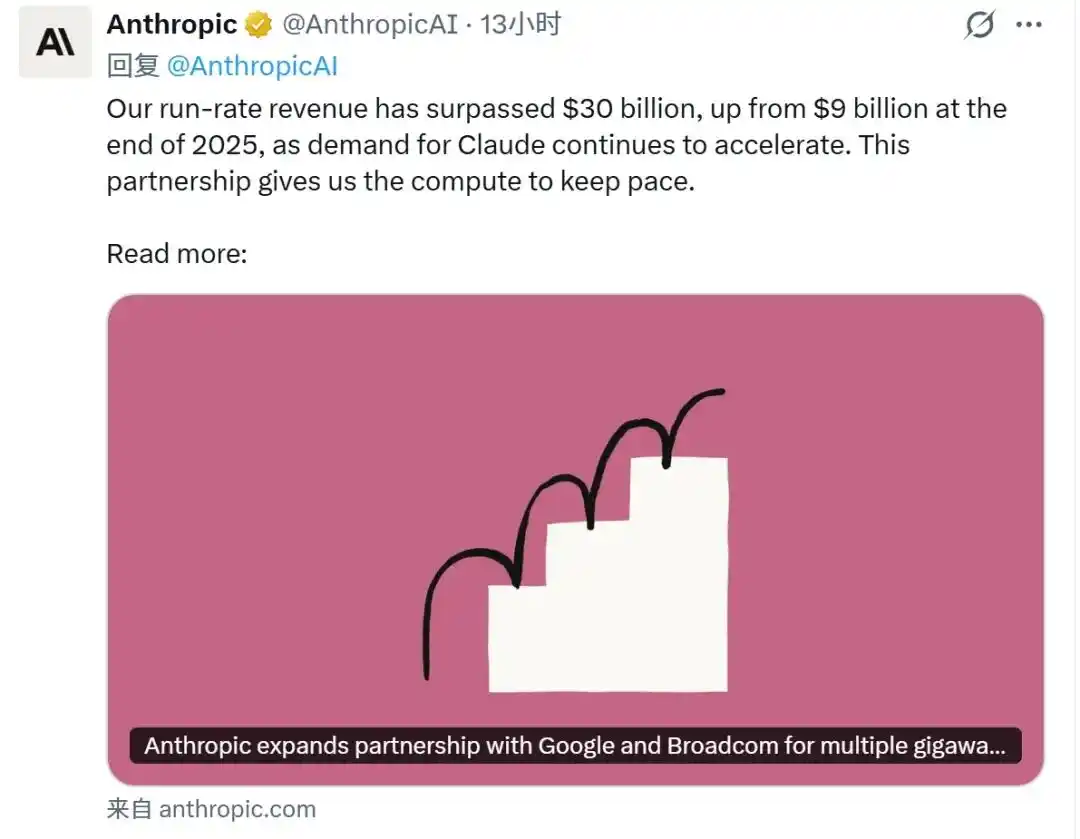

4月7日,美国大模型公司Anthropic对外公布,公司年化收入(ARR)已达到300亿美元。

此金额一举超过OpenAI的250亿美元(截至2026年2月底),Anthropic成为全球收入最高的独立大模型公司。

为什么一家没有ChatGPT入口,也没有OpenAI平台体量的公司,能够在收入上跑得比OpenAI还快?

Anthropic押对了什么?

要理解Anthropic的超越,必须先看懂它与OpenAI的根本分歧。

2022年左右,ChatGPT爆火后,全行业都在复制聊天机器人,但Anthropic却将资源投向了看似枯燥的基础设施——API稳定性、上下文窗口扩展、以及名为Claude的模型。

Anthropic的定位从第一天就不是更好的聊天工具,而是嵌入提升企业生产力的引擎。

这种定位的克制在2023年至2024年显得保守甚至落后。

当时ChatGPT的日活数字是Anthropic的数十倍,OpenAI的估值一骑绝尘。

但当2025年企业级AI支出真正爆发时,Anthropic的提前布局开始兑现。

它的客户名单里出现了Thomson Reuters等专业信息服务商、硅谷的科技独角兽们,还有大量金融、法律、医疗行业的头部机构,这些客户在为生产力的提升买单。

财务数据显示,Anthropic约80%的收入来自企业级客户,而且这些客户很多按消耗量计费。只要某个企业场景开始高频使用,收入就会被迅速推高。

相比之下,OpenAI的收入结构更为多元,目前仍以ChatGPT订阅收入为主,API与授权业务约占15%-20%。

当OpenAI把资源倾向ChatGPT的语音对话、图像生成等消费者功能,Anthropic仍在继续发力企业级能力。

2025年Anthropic推出的Claude Code被开发者群体奉为代码神器,成为企业工程团队的生产力支柱。

不仅如此,两者定价策略的差异同样耐人寻味。

OpenAI的ChatGPT Plus,无论用户使用1次还是1000次,收入封顶20美元。

Anthropic则采用分层定价,从20美元到200美元不等,按Token消耗付费,使用越深、收入越高。

这背后是企业客户对生产力工具的价值认可,远超过个人消费者对聊天娱乐的付费意愿。

一位硅谷风投的观察切中要害:

OpenAI在造一座面向消费者的迪士尼,而Anthropic在修一条通往企业核心系统的收费公路。前者需要持续的创新和营销投入,后者一旦建成,维护成本极低而通行费可以年年涨价。

拉开差距的coding

Anthropic凭借企业级战略实现了对OpenAI的超越,但一个问题随之浮现:

在其庞大的企业级收入版图中,究竟是什么撑起了300亿美元的体量?

答案指向一个看似垂直、实则杀伤力极强的赛道:Coding(编程辅助)。

在Anthropic的企业级业务中,Coding并非唯一的收入来源。

文档分析、客服自动化、法律审查等场景都在贡献收入,但coding无疑是确定性最强、增长最快、且最能体现企业投入意愿的品类。

这种确定性在Claude Code的商业表现中得到了极致验证。

2025年4月,这款面向开发者的AI编程助手年化收入仅为1700万美元;

到了11月,这一数字飙升至10亿美元,创下企业软件史上最快增长纪录。

2026年2月,Claude Code的ARR已突破25亿美元,占Anthropic总收入的18%以上。

更关键的是其收入结构的健康度,企业订阅占比超过一半,且自年初以来增长了四倍。

这意味着,Claude Code不仅贡献了大量收入,更成为Anthropic渗透企业级业务的超级品类。

相比之下,OpenAI在Coding领域的反应显得迟缓而被动。

在OpenAI收入结构中,Coding相关收入在很长一段时间内几乎为零。

数据显示,直到2026年初,OpenAI在代码专项产品上的商业化贡献仍微乎其微。

当OpenAI意识到Coding赛道的战略价值,转而内部开发Codex,并终于在2026年2月以macOS应用形式推出时,市场格局已定。

在企业编码市场份额上,据Menlo Ventures估算,OpenAI仅占21%,远低于Anthropic的54%。

尽管OpenAI模型能力始终强大,但在to B市场,技术领先只是入场券。

找到像Coding这样强确认的场景,以及将技术封装成企业愿意持续付费的生产力基础设施,才是真正的护城河。

而在中国,这场关于企业级的AI战争,正以另一种形态展开。

国内厂商抢占企业级赛道

Anthropic用企业级工作流把收入做大,OpenAI被迫回头补课,这个信号国内厂商当然也看到了。

无论是头部大厂还是创业公司,都各自以不同的切入方式,争夺这块最先商业化的战场。

比如大厂中比较典型的字节,目前正在把底层的云和模型,以及上层的办公、coding等应用,都接到同一个企业级AI底座上。

据IDC数据,2025年上半年,火山引擎的MaaS市场份额达49.2%,排名第一。

豆包大模型调用量更是全球领先,截至2026年4月,累计token使用超过1万亿的企业客户数量已从去年底的100家增至140家。

这表明字节正在把模型调用,做成企业客户持续消耗的基础设施业务。

飞书也已经不再只是一个协作工具,而是把AI直接打包成企业套餐。

飞书官方2026年4月的文档显示,企业可直接购买AI Basic、AI Business、AI Business Plus、AI Enterprise等多层级AI方案。

而Trae作为字节的coding入口,在2025年12月推出企业版,把开发者工作流也纳入这张企业网络里。

再看创业系大模型公司,智谱的企业级路线更为明显。

财报显示,智谱2025年全年营收7.24亿元,其中本地化部署收入占比73.7%,同比增长超100%。同时,API平台ARR过去12个月增长60倍。

这表明智谱的营收,不是单纯来自模型热度,而是来自两类最典型的企业级付费:一类是本地化部署,一类是云API调用。

2026年一季度,API提价83%后,Token调用量仍增长了400%。这种敢于涨价且用户不流失的定价权,在国内厂商中独一无二。

智谱正在证明,即便没有大厂那样完整的生态,也可以先靠企业级部署和调用把收入跑起来。

事实上,Anthropic的超越与国内厂商的集体转向,都指向了一个共同的结论:

在企业级AI市场,模型能力最强已经不再是第一优先级,高频工作流、可量化的生产力提升,才是企业选择AI产品的首要因素。

AI下半场,真正的较量才刚开始。

本文来自微信公众号“世界模型工场”,作者:世界模型工场