Bitfarms grows revenue 72%, but losses widen – Here’s why!

ambcryptoPublished on 2026-04-02Last updated on 2026-04-02

Abstract

Bitcoin mining faces significant pressure as hashprice drops to $30–$35, well below production costs of $80,000–$88,000 per BTC, leading to losses of $17,000–$19,000 per coin. Despite this, miners like Bitfarms continue expanding hashrate. Bitfarms reported a 72% revenue increase to $229 million, but net losses widened to $209 million due to non-cash accounting charges, including depreciation and Bitcoin price volatility. In response, the company is pivoting to high-performance computing (HPC) and AI infrastructure, with 2.2 GW of power capacity in development, aiming for more predictable revenue streams. This strategic shift may reposition Bitfarms as an infrastructure-focused business, reducing reliance on Bitcoin's cyclical volatility.

A clear tension is building in Bitcoin’s mining sector, where growth in activity no longer translates into financial stability.

According to CoinShares Q1 2026 report on Bitcoin mining, Hashrate held near 1,020 EH/s after peaking around 1,160 EH/s, showing miners continue expanding despite pressure.

However, hashprice has dropped to $30–$35 from over $60, cutting revenue per unit sharply. This happens because the halving reduced block rewards while the price has not risen enough to offset costs.

As a result, production costs near $80,000–$88,000 exceed current prices, leaving losses of $17,000–$19,000 per BTC.

Meanwhile, accounting rules amplify these losses through asset revaluation. This implies weaker miners may exit, while stronger players consolidate, tightening supply and influencing future price stability.

Bitfarms growth rises as accounting losses widen

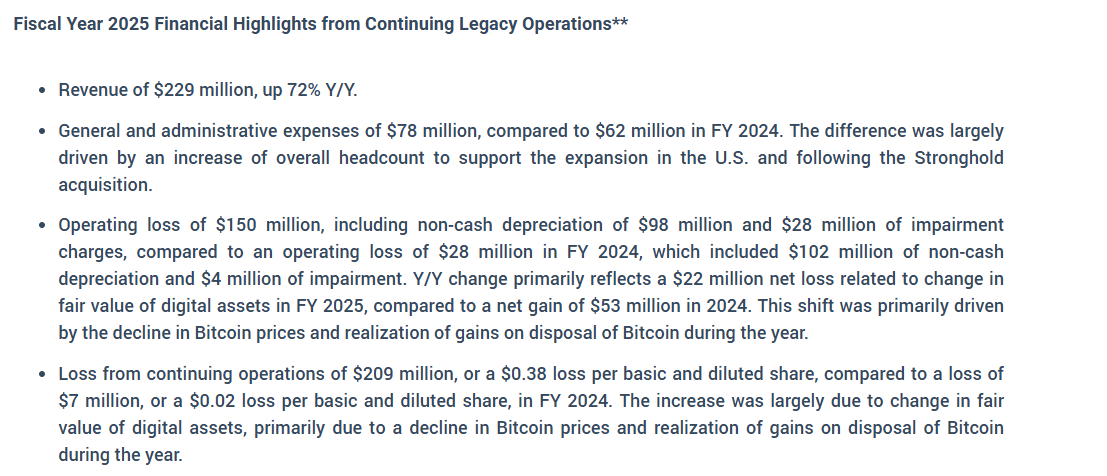

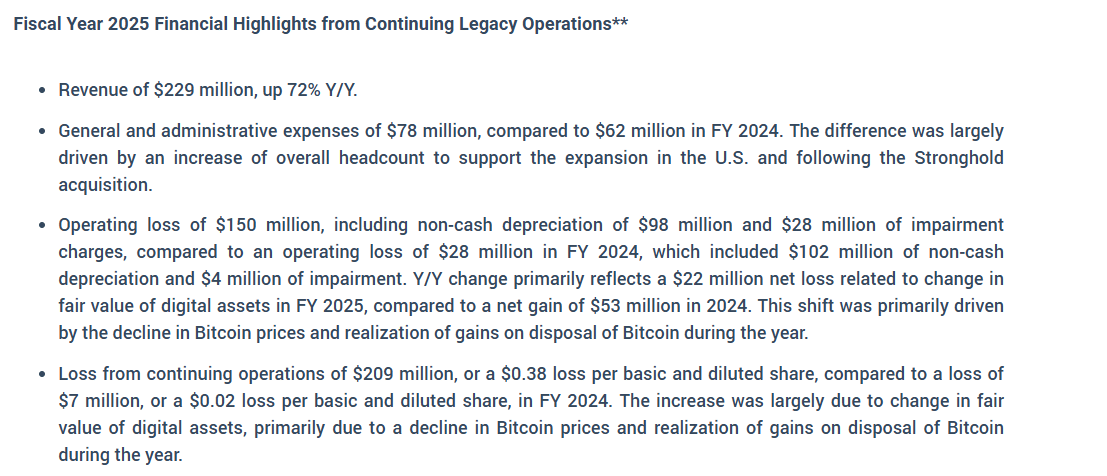

As mining margins tighten across the sector, Bitfarms’ report results reveal how operational growth clashes with financial outcomes. Revenue rose 72% to $229 million, showing stronger output from expanded hashrate.

Source: Bitfarms

However, net losses widened to around $209 million, not from weak operations but from accounting pressure.

Depreciation hit $98 million, impairments reached $28 million, while $22 million reflected BTC price swings. This happens because fair-value accounting captures past volatility, even as current production improves.

Yet shares rose about 6%, showing investors’ focus on future positioning. This implies markets expect miners to evolve beyond BTC exposure, where diversification could reshape long-term valuation.

Bitfarms pivots to HPC and AI as mining margins compress

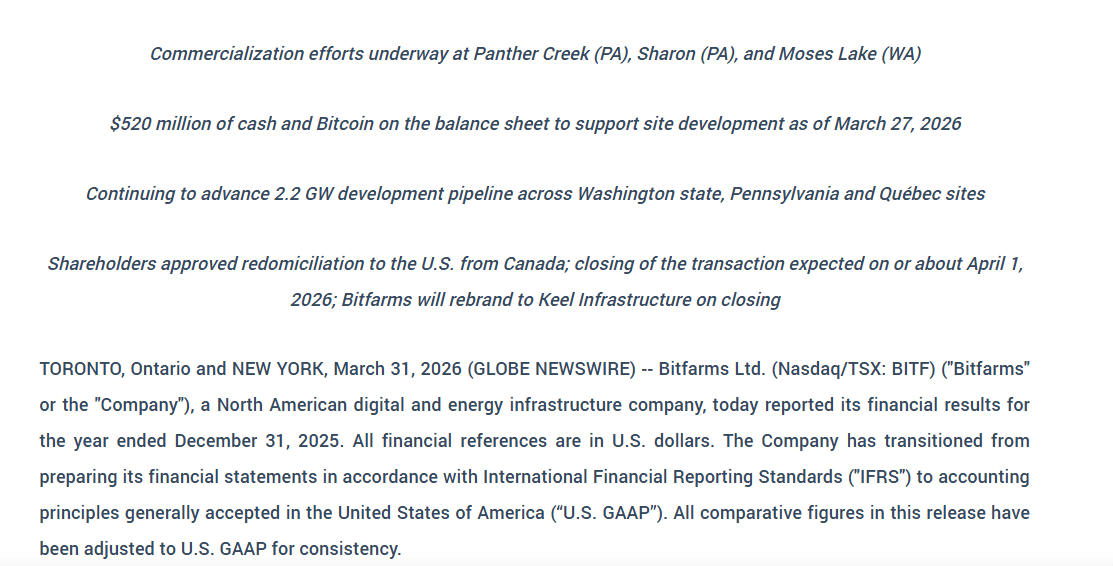

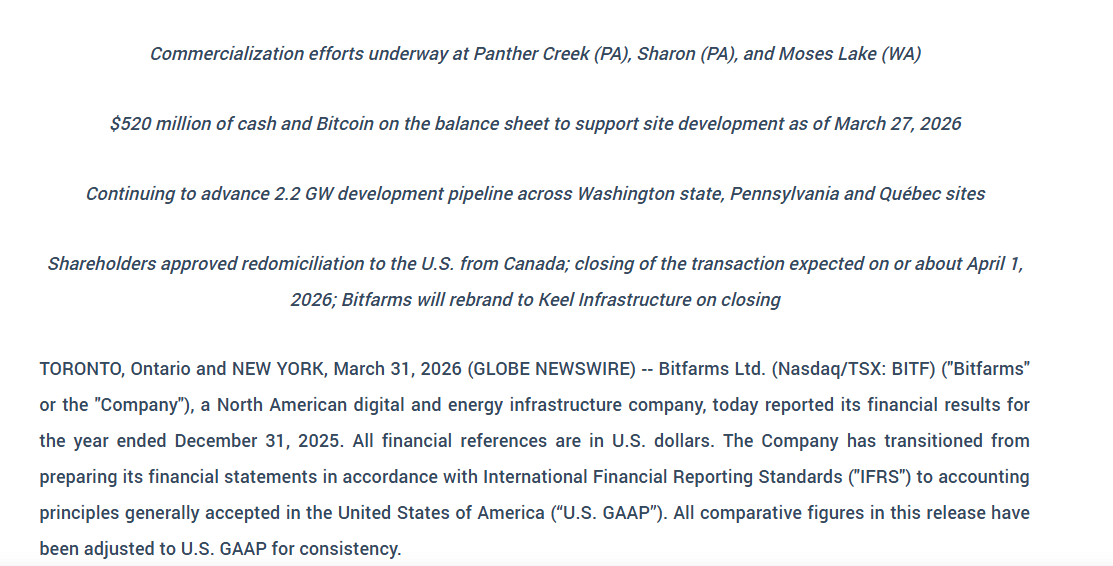

As mining margins remain under pressure, Bitfarms is actively repositioning its business toward HPC and AI infrastructure to secure more stable revenue. The company is building a 2.2 GW pipeline, with 341 MW already active and 1.5 GW in expansion, targeting high-demand data markets.

Source: Bitfarms

This shift is happening because hashprice stays compressed, making mining returns less predictable.

In response, Bitfarms is redirecting power capacity toward AI workloads, where long-term contracts offer higher margins and steady cash flow.

Industry trends support this move, with HPC revenue projected to reach 70% of miner income by 2026. The rebrand to Keel Infrastructure reinforces this transition.

This implies Bitfarms is evolving beyond Bitcoin exposure, positioning for more resilient, infrastructure-driven growth.

All this together, Bitfarms may reprice as an infrastructure play if HPC and AI drive stable revenue growth. However, if mining remains dominant, BTC volatility will continue shaping earnings, keeping the stock tied to cyclical crypto movements.

Final Summary

Bitcoin [BTC] mining margins compress as hashprice falls below costs, forcing weaker miners out while efficient players consolidate supply dynamics.

Bitcoin volatility still drives Bitfarms’ performance, but the HPC and AI pivot may shift valuation toward stable, infrastructure-led growth.

QWhy did Bitfarms' revenue grow by 72% despite widening losses?

ABitfarms' revenue grew 72% to $229 million due to increased output from expanded hashrate, but net losses widened to $209 million primarily due to non-cash accounting pressures including $98 million in depreciation, $28 million in impairments, and $22 million from BTC price volatility.

QWhat is the current hashprice range and how does it compare to previous levels?

AHashprice has dropped to $30–$35 per exahash from over $60 previously, representing a sharp decline in revenue per unit of computing power.

QHow are production costs comparing to Bitcoin's current price according to the article?

AProduction costs are near $80,000–$88,000 per Bitcoin, which exceeds current market prices, resulting in losses of $17,000–$19,000 per BTC mined.

QWhat strategic shift is Bitfarms making to address compressed mining margins?

ABitfarms is pivoting to High Performance Computing (HPC) and AI infrastructure, building a 2.2 GW pipeline with 341 MW already active, targeting high-demand data markets with long-term contracts that offer higher margins and steady cash flow.

QWhat percentage of miner income is HPC revenue projected to reach by 2026?

AHPC revenue is projected to reach 70% of miner income by 2026 according to industry trends mentioned in the article.

Recently, Robinhood Chain adopted Chainlink as its official oracle and CCIP provider.

43.7k Total ViewsPublished 2026.07.22Updated 2026.07.24

Discussions

Welcome to the HTX Community. Here, you can stay informed about the latest platform developments and gain access to professional market insights. Users' opinions on the price of S (S) are presented below.