Bitcoin’s price has lately struggled to generate sufficient demand to push itself higher. Especially since bearish sentiment has continued to dominate.

However, shifting dynamics among short-term holders may be emerging. These could influence Bitcoin’s [BTC] trajectory, particularly if a near-term bullish scenario unfolds.

Bitcoin to $64,000 may trigger bulls

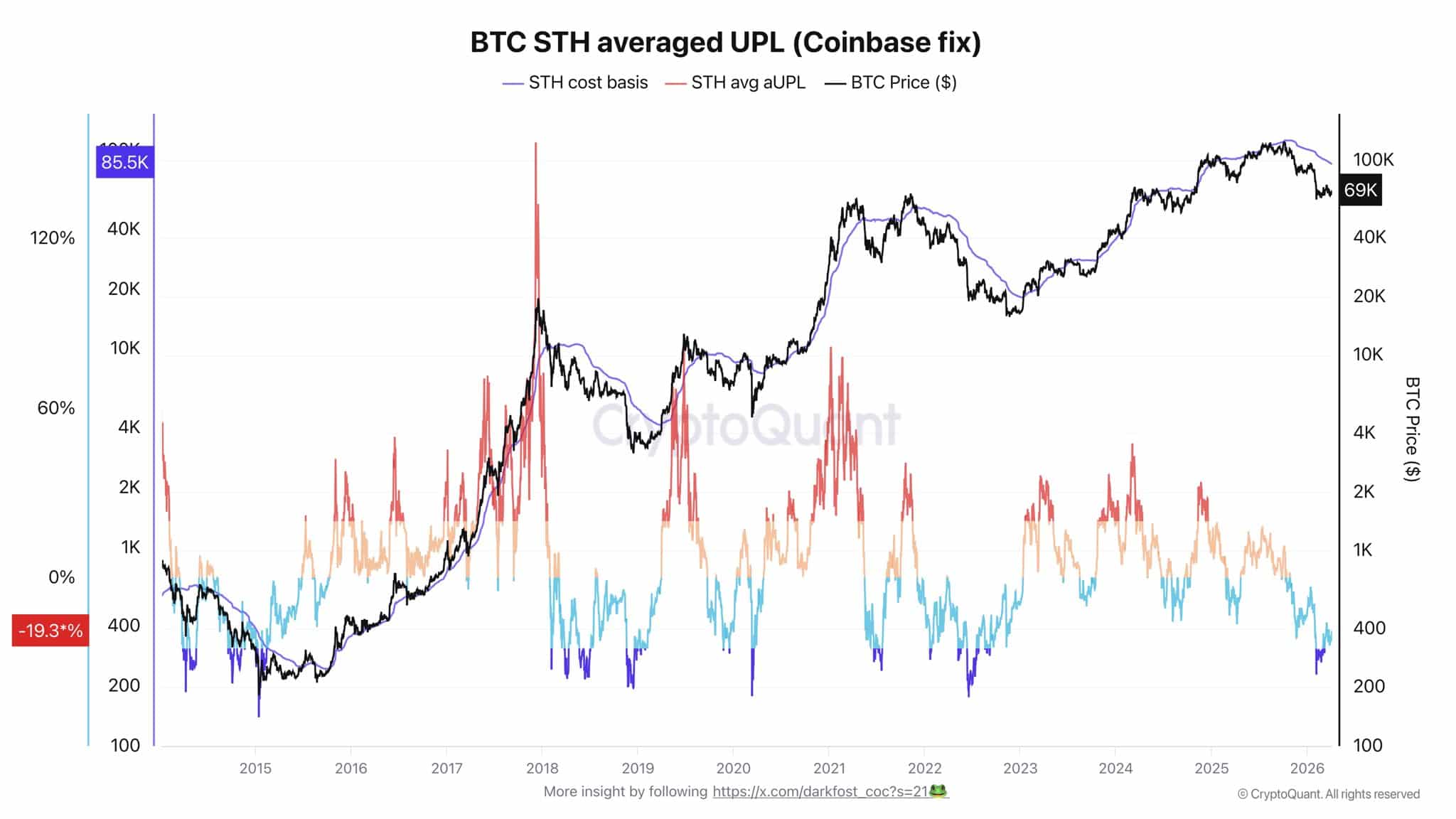

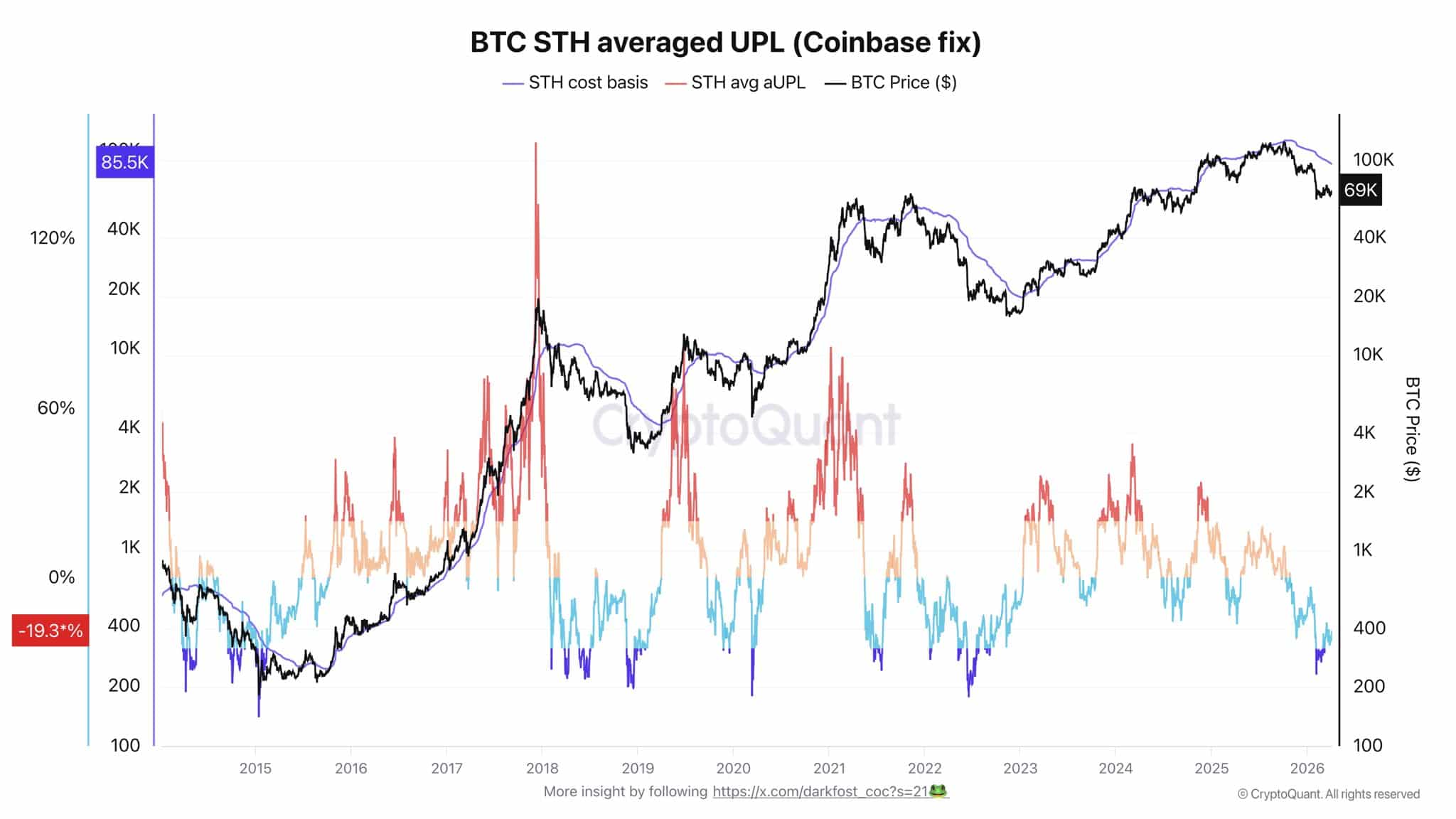

Data from CryptoQuant highlighted the cost basis of short-term holders—the average price at which they purchased Bitcoin—revealing a potential market pattern.

STHs who bought within the last month have an average cost basis of approximately $85,450. At Bitcoin’s press time price, this puts them at a 19% unrealized loss – A significant drawdown.

Historically, when the STH cost basis drops to 25% or lower, it often marks a market bottom. At a 19% loss, Bitcoin would need an additional 6% decline—bringing it to roughly $64,000—before conditions for a rebound may emerge.

At these levels, two behaviors typically occur – Some STHs hold longer, while others sell, unable to bear further losses. For Bitcoin to reach a historical low and potentially repeat past fractal patterns, the selling from the latter group is usually required.

Foundations for a rally

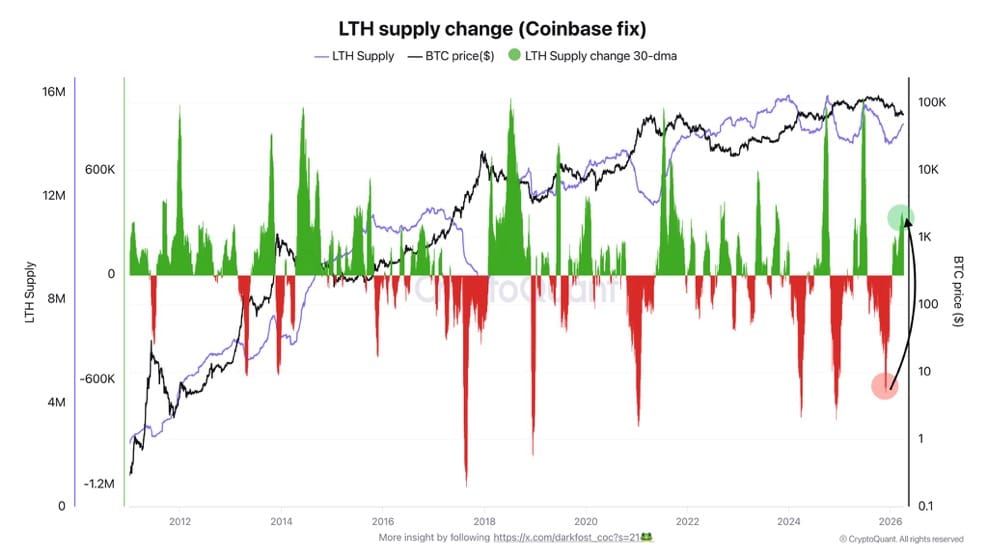

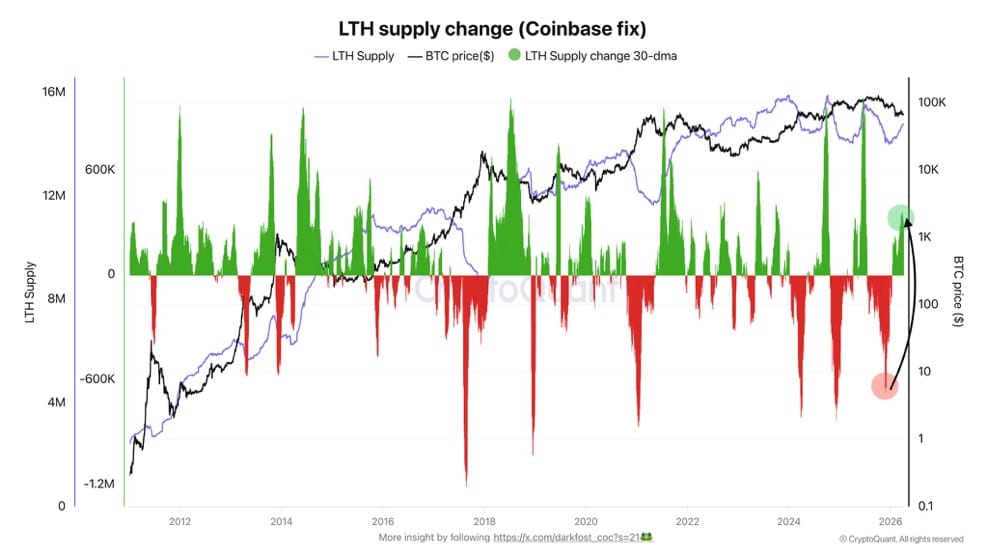

Signs of a foundational shift may be forming too. In fact, some short-term holders are already taking actions that could tighten Bitcoin’s supply dynamics.

At the time of writing, reports from CryptoQuant hinted at an ongoing transition from STHs to LTHs – Generally positive for Bitcoin. Long-term holders, investors who have held Bitcoin for at least six months, tend to reduce the likelihood of sudden sell-offs.

In fact, approximately 300,000 BTC have recently moved from STHs to LTHs, representing around $27 billion removed from the liquid market.

This reduced supply can support price stability, especially during downtrends, as LTHs are less likely to sell under pressure.

Exchange reserve dynamics

Another critical metric is the availability of Bitcoin on exchanges, reflected in the exchange reserves. High reserves can increase selling pressure as more Bitcoin is readily available for trading.

At the time of writing, exchange reserves stood at 2.45 million BTC, declining slightly from a high of 2.46 million on 02 April.

A sustained decline in exchange reserves would indicate tightening supply, which could reduce the risk of major price drops. Nevertheless, exchange flow dynamics will remain crucial for any rebound to levels historically associated with market bottoms.

Final Summary

- Short-term holders are at a 19% unrealized loss and a further 6% decline could push Bitcoin towards levels historically associated with market bottoms.

- Over 300,000 BTC previously held by STHs have not yet transitioned to long-term holders.