Author: Nancy, PANews

While the storage sector is going crazy, with Micron and SK Hynix both surpassing the trillion-dollar market capitalization mark, Elon Musk is personally accelerating the myth of creating a trillion-dollar fortune.

SpaceX, with its sky-high valuation, is accelerating towards the capital market. This super IPO, which may rewrite wealth history, is pushing Musk towards becoming the world's first trillionaire, while also delivering astounding returns of hundreds or even thousands of times to early allies.

However, for humanity's most expensive space narrative to continue, new buyers are ultimately needed. As massive pension funds will be 'forced to buy in,' Americans' retirement savings become the fuel for Musk's space dream.

Elon Musk is making American retirees 'pay up.'

Countdown to History's Largest IPO, Early Allies Reap Huge Profits

Wall Street has been waiting for SpaceX's IPO for many years.

Over the past decade, the company has grown from a startup valued at just $27 million into today's super unicorn valued at nearly $1.75 to $2 trillion, becoming one of the world's highest-valued private companies.

Now, this super IPO is finally set to list as early as June 12. This is not only the largest IPO event in human history but also means the wealth feast is entering its cash-out moment. Musk's long-term followers have finally waited for substantial returns.

For example, Google, through early investment, may become the biggest external winner. As of the end of 2025, it holds about 6.11% of SpaceX shares. An investment of just $900 million back then is now worth close to $120 billion; Valor Equity Partners, as a major shareholder second only to Musk, holds over 500 million SpaceX Class A shares, with equity value ranging roughly between $90 billion and $140 billion; Peter Thiel's Founders Fund, through multiple rounds of follow-on investments, holds about 3.5% of the shares, with paper gains exceeding $60 billion; Fidelity, as a major institutional investor in a 2015 co-investment round, holds shares worth about $35 billion; even Sequoia Capital, which entered relatively late, sees considerable returns, expected to be over $20 billion.

As for Musk himself, he is also poised to become the world's first trillion-dollar billionaire.

Bank of America strategist Michael Hartnett warns in a recent report that once super IPOs like SpaceX and OpenAI materialize, the weight of tech stocks in equity benchmark indices could easily surpass about 48%, exceeding the market concentration levels of all major bubble periods in history such as the 'Roaring Twenties' of the 1920s, the 'Nifty Fifty' of the 1970s, the Japanese bubble of the 1980s, and the dot-com bubble of the 1990s.

However, who will ultimately take on such a massive valuation?

To reduce selling pressure after listing and maintain stock price stability, SpaceX has made some adjustments. For instance, insider shares will use a phased unlocking mechanism instead of the traditional unified 6-month lock-up period common in IPOs. Additionally, the company approved a 5-for-1 stock split for common shares to lower the psychological barrier for retail investors and enhance liquidity. Musk has also publicly stated that he will not sell any SpaceX shares.

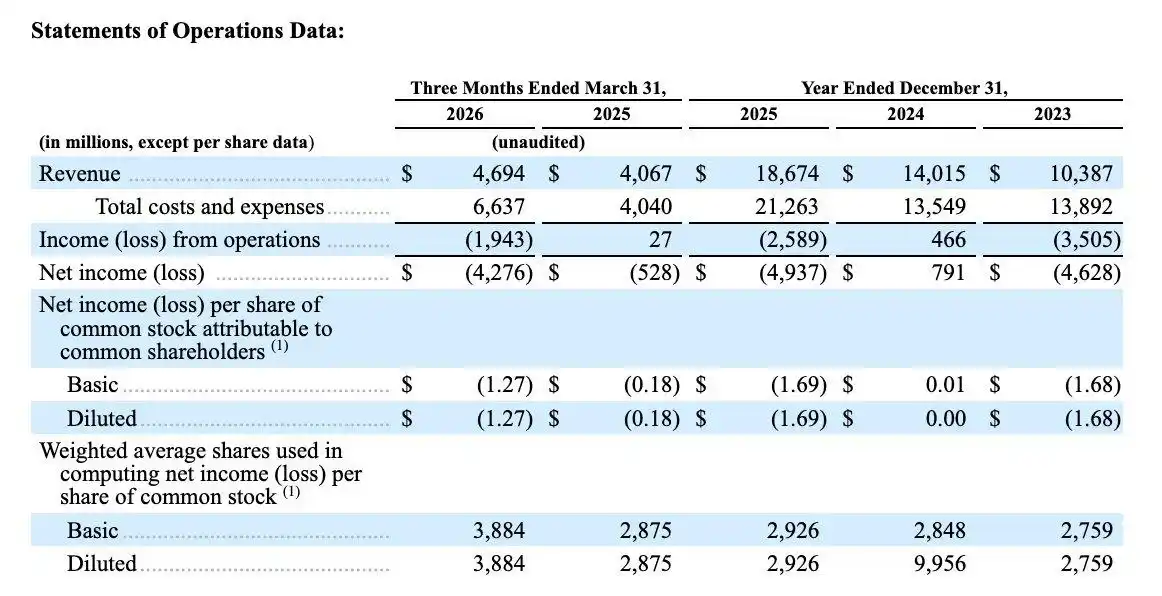

But market concerns haven't disappeared. Putting aside the uncertainty of the grand Mars narrative and looking just at financial data, SpaceX remains a fast-burning company. The prospectus shows that in the first quarter of 2026 alone, SpaceX's net loss was nearly $4.3 billion, almost equivalent to the full-year loss of the previous year. Meanwhile, Musk controls an absolute 85% of the voting rights, meaning the board can hardly fire him, and external shareholders can almost never push through any major business decisions.

To some extent, SpaceX is a highly Musk-ified company. Its valuation, governance, and future expectations are deeply tied to Musk personally.

After all early investors have made a fortune, who is still willing to buy this already outrageously expensive space ticket at a high price?

Wall Street Paves an Index Fast Lane, U.S. Pensions Become the 'Bag Holders'

Americans' retirement savings may become the potential fuel for Musk's space dream.

Wall Street has already started opening express lanes for super IPOs. On May 1 this year, new Nasdaq rules officially took effect. Newly listed companies ranking in the top 40 of the Nasdaq-100 index by market cap can be included in the index after just 15 trading days, compared to the usual wait of about three months previously.

S&P also launched a consultation in May, proposing to shorten the minimum listing time required for inclusion from 12 months to 6 months and considering exempting extremely large companies from profitability requirements. FTSE Russell similarly relaxed restrictions, allowing large IPOs to be assessed for inclusion in the Russell U.S. Equity Indexes (including Russell 1000, Top 200, etc.) as early as the 5th trading day after listing, without waiting for quarterly reviews.

Major U.S. indices quietly relaxing rules is undoubtedly paving a dedicated runway for SpaceX.

According to Business Insider disclosures, after SpaceX goes public, it may quickly enter mainstream indices and ETFs. The speed of passive fund allocation could far exceed that of previous large IPOs. For example, the CRSP indices tracked by Vanguard's VTI and Growth ETF VUG could include SpaceX as early as 5 trading days post-listing; the Nasdaq-100 index tracked by QQQ could include SpaceX after 15 trading days; and the S&P 500 index tracked by SPY might include SpaceX in 2027 after rule changes, among others.

Within the U.S. retirement system, a vast number of 401(k) plans, pension funds, and long-term savings accounts employ passive index investment strategies. Funds typically automatically allocate assets according to index constituents and their market cap weightings.

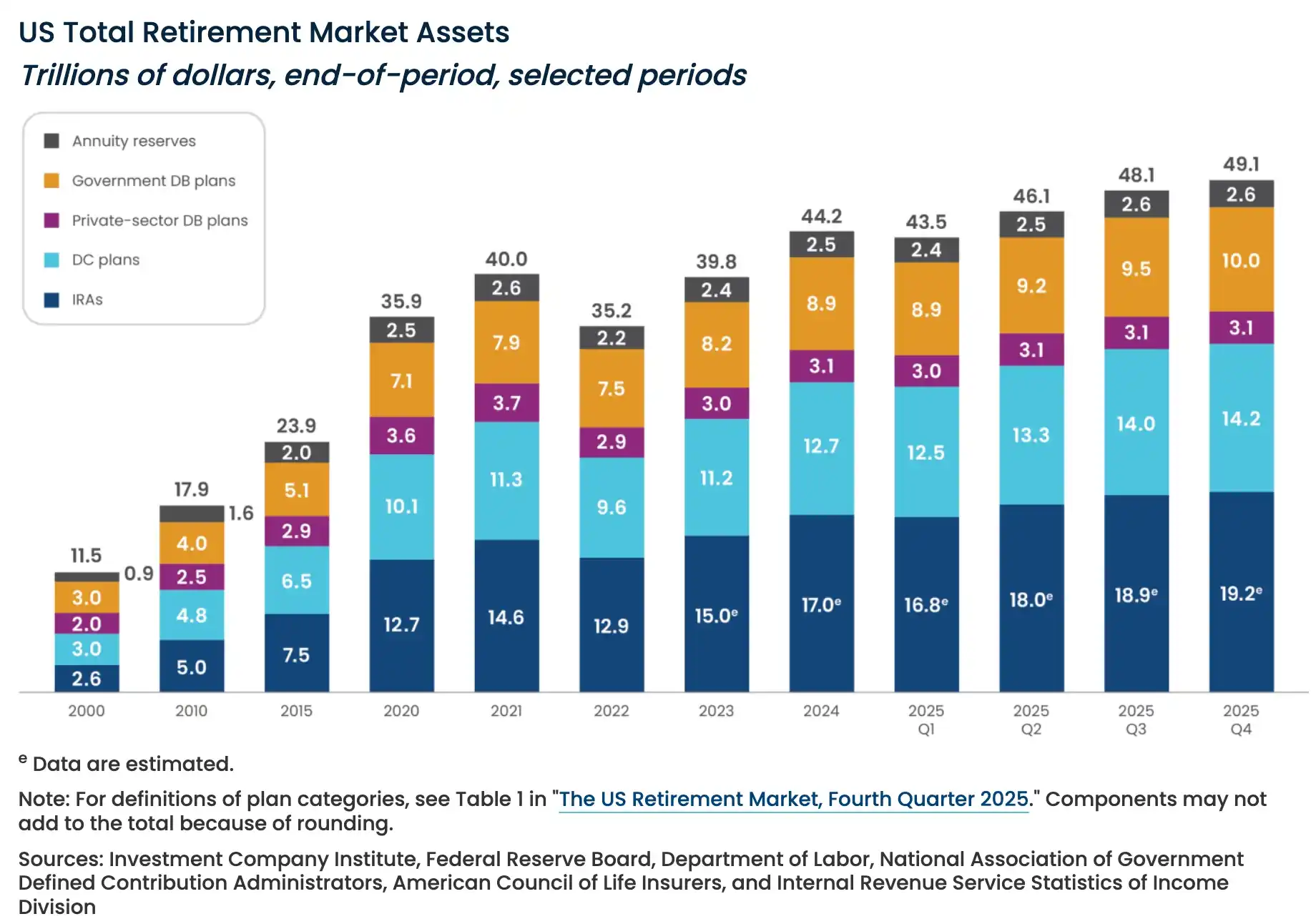

This strategy originated from the first index fund for ordinary investors launched in 1976 by index fund pioneer John Bogle. The core philosophy is to 'replicate the market, not beat it.' With extremely low management fees and high diversification, it became the preferred allocation method for pensions and 401(k) accounts. To date, total U.S. retirement assets exceed $49 trillion.

This means that once SpaceX is included in an index, all funds tracking that benchmark, without analyzing valuation, judging bubbles, or even caring if the company is profitable, are forced to buy according to the weight.

However, this game has sparked strong dissatisfaction within the pension system.

Recently, the American Federation of Teachers sent a letter to the SEC urging strengthened scrutiny of SpaceX's listing, warning that workers' lifetime savings could be controlled by a company that resembles a Musk family business more than a transparent public company.

Simultaneously, three major U.S. public pension funds managing over $1 trillion in assets (CalPERS, New York State, and New York City pension systems) also co-signed a letter to Musk, strongly opposing SpaceX's extreme governance structure. This includes super-voting rights, veto power over his own removal as CEO, and immunity from lawsuits.

They pointed out that Musk simultaneously leads SpaceX, Tesla, xAI, Neuralink, and other companies, posing significant risks due to divided attention. The letter demanded that SpaceX transition to a one-share-one-vote structure within seven years, establish a board with a majority of external shareholders, separate the CEO and Chairman roles, and remove Musk's self-veto rights.

This rule change, tailored by Wall Street for super IPOs, ultimately tightly binds the retirement savings of tens of millions of Americans to Musk's grand space dream. After early investors enjoy hundred-fold returns, the remaining 'bag-holding' cost is shifted onto passive investors incapable of making a choice.

The largest 'Granny Drain' game in history, under the guise of indexing, is officially beginning.