Author: Ma He, Foresight News

On May 29th, the U.S. Commodity Futures Trading Commission (CFTC) announced two landmark actions on the same day: it formally approved the Bitcoin perpetual contract submitted by KalshiEX, LLC (Kalshi). Additionally, the CFTC issued a no-action letter to Coinbase, allowing Coinbase to offer certain perpetual futures products to U.S. customers through its subsidiary.

The CFTC also released a "Policy Statement on the Listing of Perpetual Contracts," providing a clear guidance framework for the listing of perpetual products on regulated markets. This combination of actions signifies a crucial step away from the longstanding regulatory gray area for U.S. crypto derivatives, moving toward a compliant path for genuine perpetual contracts.

Kalshi and Coinbase Both Receive Regulatory Approval

The CFTC's review determined that Kalshi's Bitcoin perpetual contract complies with the core principles of the Commodity Exchange Act and Designated Contract Market (DCM) regulations, including the depth and liquidity of the underlying Bitcoin spot market, contract design, and risk management capabilities. The approval order requires Kalshi to maintain ongoing compliance and clarifies that the perpetual contract design "may not be suitable for all asset classes," encouraging other market participants to engage with regulators and submit formal applications for perpetual products based on different underlying assets.

Furthermore, the CFTC's Division of Market Participants issued an interpretive letter and a no-action letter to the registered futures commission merchant Coinbase Financial Markets (CFM), permitting it to offer crypto options and perpetual contracts listed on Deribit to U.S. users. The letter confirms that these perpetual contracts can be classified as foreign futures under CFTC Regulation 30.1. Under specified conditions, the CFTC stated it would not recommend enforcement action against CFM for transferring customer-held digital commodities and payment stablecoins to its foreign broker affiliate for margin purposes, where the affiliate may exercise rehypothecation rights over such customer assets.

Previously, the U.S. market lacked genuine perpetual contracts (with no expiration date). Coinbase Derivatives had self-certified and launched "perpetual-style" futures in July 2025 (with contract terms up to 5 years), designed to mimic perpetual economic characteristics but still retaining an expiration date. Today's approval and no-action letters provide a dual compliance pathway for "true perpetuals": Kalshi follows the standard DCM futures route, while Coinbase reaches U.S. customers via the foreign futures + crypto collateral route.

Mike Selig

CFTC Chairman Mike Selig emphasized in his statement that perpetual contracts are important tools for risk management and price discovery in the global crypto asset market. Introducing true perpetual contracts in the U.S. is a significant step toward establishing the U.S. as a global crypto hub. He noted that the CFTC has established a workable regulatory framework for crypto asset perpetual contracts and will maintain market integrity by limiting excessive leverage, market volatility, and systemic risk.

Selig also acknowledged that the CFTC's current regulatory stance has not yet been formalized into a permanent rule, and future policies may adjust as the regulatory environment evolves.

The Trillion-Dollar Market Opportunity

So, why had the CFTC not approved true Bitcoin perpetual contracts until now?

Perpetual contracts were considered a "novel" product within the traditional commodity futures framework. They lack an expiration date and final settlement, which conflicts with the conventional understanding under the Commodity Exchange Act that traditional futures "must have an expiration date and a convergence mechanism." The CFTC internally debated whether to classify them as futures or swaps, as different classifications entail entirely different regulatory requirements (including clearing, margin, reporting obligations, etc.). This legal ambiguity made it difficult for platforms to secure a solid compliance path.

Furthermore, concerns about their high leverage and speculative nature, along with fears of market manipulation, have kept the CFTC's approach cautious.

BTCPERP, as a perpetual contract tracking the Bitcoin spot price, has no fixed expiration date. It uses a funding rate mechanism for periodic settlements between long and short positions to maintain a tight peg between the contract price and the spot price.

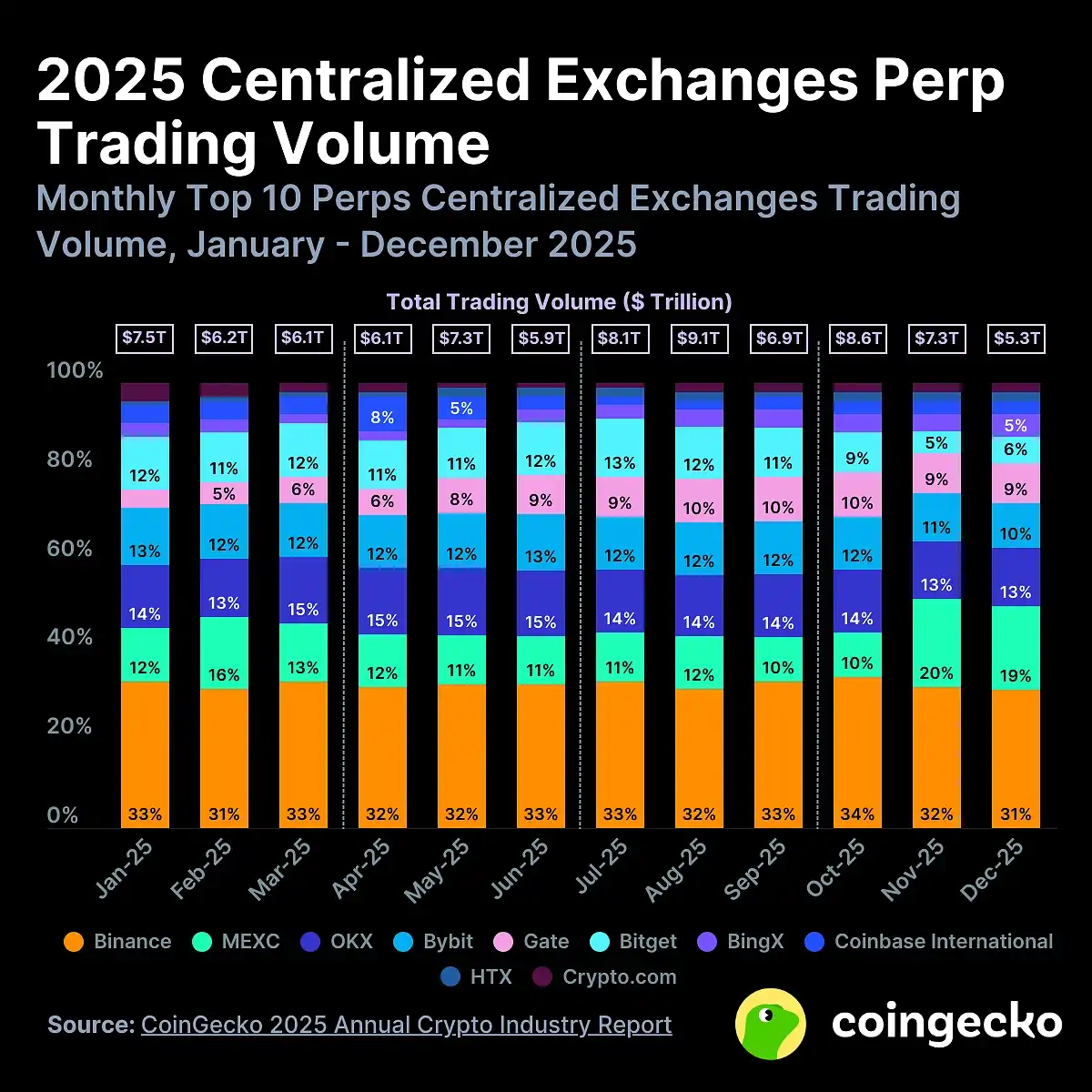

Perpetual contracts have long dominated the global crypto derivatives market. According to CoinGecko's 2025 annual report, the cumulative trading volume of crypto derivatives on centralized exchanges globally was approximately $85.7 trillion, with perpetual contracts accounting for about 78%. In 2025, the cumulative volume of perpetual contracts on decentralized exchanges reached about $6.7 trillion (a 346% year-over-year increase).

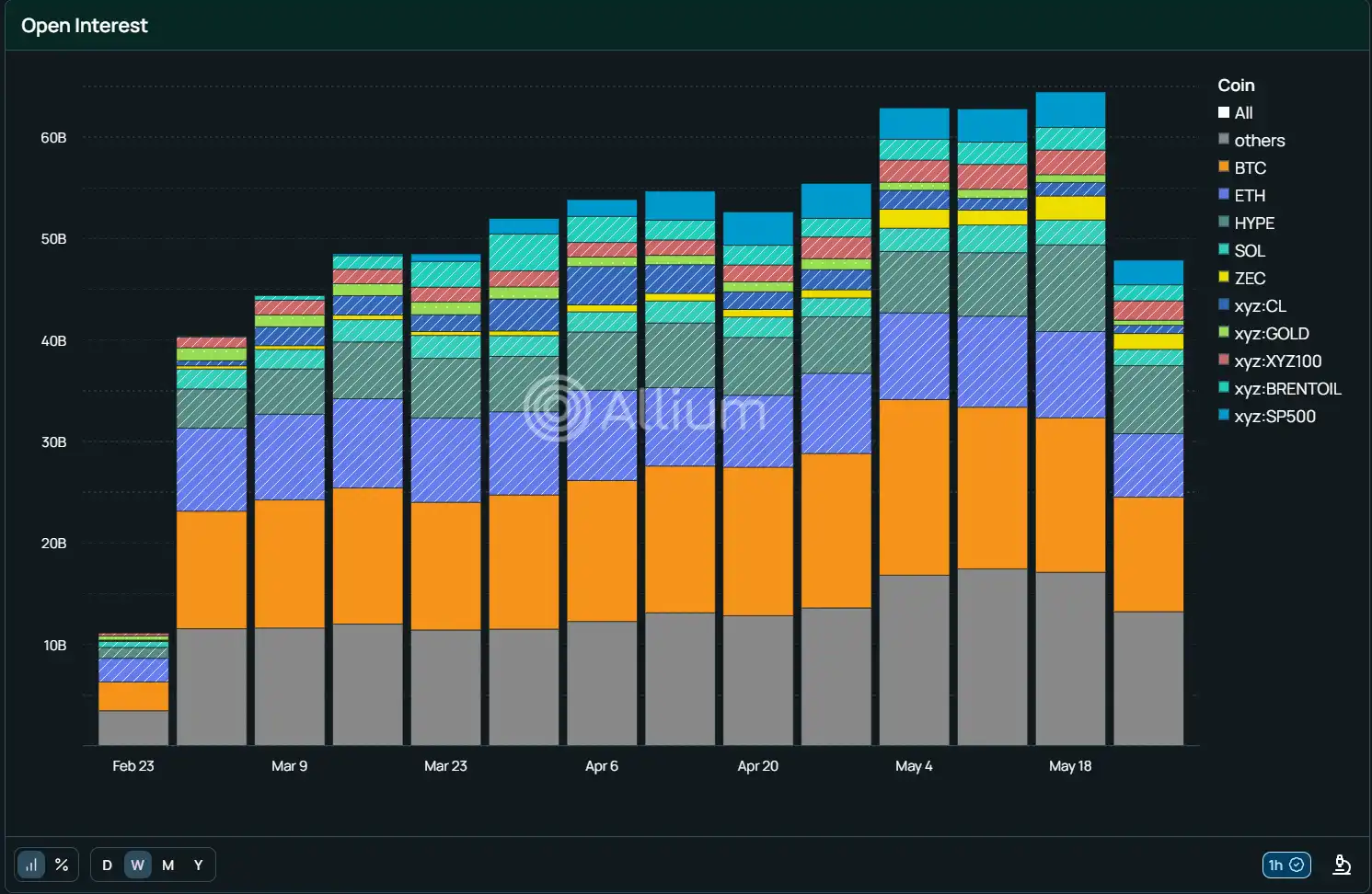

Ironically, while traditionalist regulators in Washington debated compliance, offshore decentralized perpetual platforms like Hyperliquid had already extended their reach to S&P 500, crude oil, and gold through on-chain synthetic assets. By the end of May 2026, Hyperliquid's perpetual trading volume had risen to $586.12 billion, and according to Allium on-chain data, the total open interest for Hyperliquid's network-wide derivatives also hit a record high of nearly $60 billion at the end of May. An increasing number of individuals and institutions are choosing to trade on its platform.

Hyperliquid Latest Open Interest

This unprecedented approval by the CFTC is not just an accommodation to the crypto market; it is a necessary "onshore defense battle" forced upon the compliant world by the innovative pressure from offshore "everything-as-a-perpetual-asset."

In contrast, while regulated Bitcoin futures like those on CME provide stable hedging tools for institutions, their leverage and trading characteristics differ from the perpetual products favored by retail/professional traders.

This approval by the CFTC undoubtedly opens a new battleground for Kalshi in the prediction market. The boundary between prediction markets and traditional crypto derivatives markets has completely blurred; Kalshi can leverage its compliant event-settlement logic to tap into the perpetual capital pool originally belonging to centralized exchanges. For Coinbase, the trading volume and revenue from its perpetual contracts will likely be reflected concretely in its next financial report.

U.S. traders previously relied heavily on offshore platforms, facing custody risks, regulatory uncertainty, and barriers to institutional access. The release of this regulatory policy, which supports crypto collateral, will attract traditional institutions like hedge funds and family offices to participate. Traders can hold leveraged positions long-term to hedge spot exposure without frequent operations; it will also attract some offshore traffic back to U.S. compliant channels.

Simultaneously, the approval for Kalshi and Coinbase will stimulate the accelerated launch of other products like ETH perpetuals, forming a more complete crypto derivatives matrix. In the long term, this policy may enhance the U.S.'s competitiveness in the global crypto derivatives ecosystem, attracting more capital, talent, and infrastructure, creating favorable conditions for deeper integration between crypto assets and traditional finance.

Now may indeed be the most regulation-friendly era for the crypto industry.