Author: Sanqing, Foresight News

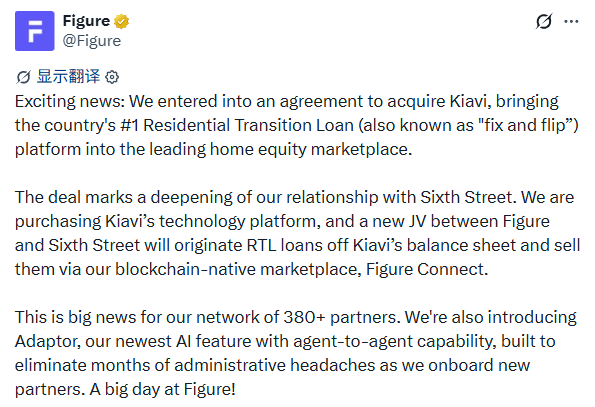

On June 10th, blockchain-native capital markets company Figure Technology Solutions (Nasdaq: FIGR) announced the acquisition of Kiavi for $717 million. Kiavi is a non-bank residential real estate investor lending platform founded in 2013, with cumulative loan origination exceeding $30 billion.

In the deal, Figure acquires Kiavi's technology and operational platform, funding approximately $538 million through the issuance of about $600 million in senior unsecured notes. The remaining roughly $179 million is contributed by global alternative asset manager Sixth Street, with the two parties forming a joint venture to purchase Kiavi's existing loan portfolio on its balance sheet. Sixth Street also provides a $3 billion forward purchase commitment. The two companies have been long-term partners. Kiavi's current CEO, Arvind Mohan, will join Figure as Chief Business Officer after the deal closes, leading the business integration.

Image source: Figure tweet

After the announcement, FIGR's stock price opened higher, briefly touching $30.11 during the session, but later retreated, closing at $28.07, down 0.74%, with an intraday fluctuation of about 9%.

Kiavi

Kiavi's predecessor was LendingHome, founded in San Francisco in 2013 by Matt Humphrey and James Herbert, with backing from investors like Foundation Capital, Ribbit Capital, and Renren.com.

It primarily offers two types of products: short-term transition loans (Residential Transition Loan, RTL) for property renovation investors, and Debt Service Coverage Ratio (DSCR) loans for long-term rental properties.

It rebranded to Kiavi in 2021, and in June 2025 became the first private non-bank institution in the US to reach 100,000 cumulative loans originated.

According to the official announcement, Kiavi achieved revenue of over $250 million and EBITDA of over $100 million in 2025, both record highs; full-year origination volume was approximately $7.8 billion, up about 20% from approximately $6.5 billion in 2024.

First Lien

The origin of Figure dates back to late 2017. After leaving SoFi that year, co-founder Mike Cagney turned his attention to blockchain. In 2018, he and his wife June Ou founded Figure in San Francisco. The following year, they launched their first product on their self-built Provenance Blockchain: a home equity line of credit (HELOC) originated on-chain.

Mike Cagney | Image source: Bloomberg

Subsequently, the company expanded along the same logic—loan origination, financing, secondary market trading...—and gradually migrated these processes on-chain, building the consumer lending marketplace Figure Connect and the on-chain warehouse financing market Democratized Prime.

Following its Nasdaq listing in September 2025, Figure officially stated that it currently accounts for about 75% of the global tokenized RWA volume.

The problem is, HELOCs are second-lien loans.

Second liens rank behind first liens in repayment priority upon borrower default, carrying higher risk and supporting a smaller asset scale. Figure estimates that the market size for first liens is about 25 times that of second liens.

Kiavi's RTL and DSCR products are both first-lien loans, and they operate in the Non-Qualified Mortgage (Non-QM) space, which traditional banks have long avoided due to regulatory concerns—a space with strong demand but highly fragmented supply.

Figure is proactively shifting the focus of its asset classes.

Post-acquisition, Figure expects to add over $7 billion in new first-lien loan volume annually. According to CEO Michael Tannenbaum, Figure's first-lien business proportion had already increased from 10% to 20% in 2025, and the company expects this ratio to reach about 40% by the end of 2027.

AI

Both Figure and Kiavi excel at using AI to process non-standard data that traditional financial institutions are reluctant to touch, building moats in areas where manual processes cannot scale.

Kiavi's core technological asset is a proprietary "after-repair value estimation engine" and an automated document review system. An old, dilapidated property awaiting renovation is nearly impossible for traditional institutions to risk-quantify.

Kiavi's model can predict the post-renovation market value based on historical transaction data and renovation plans, enabling the scaling of credit decisions for loans like RTLs.

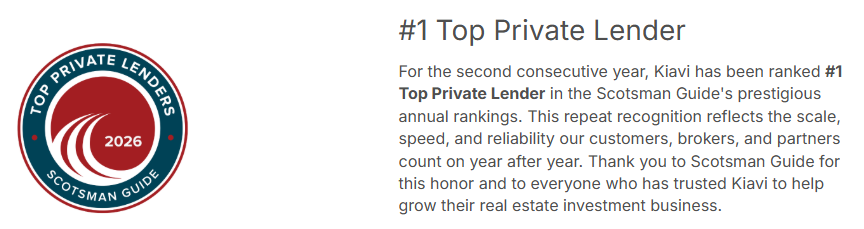

This capability has yielded significant market advantages. According to the Scotsman Guide's "2025 Top Private Lenders" rankings (underlying data from Forecasa), Kiavi's fix-and-flip loan origination volume in 2024 was approximately $5.5 billion, more than three times that of the second-place lender, and it continued to expand its lead in 2025.

Image source: Kiavi

Figure aims to solve the problem of what happens to assets after they leave Kiavi: how to put them on-chain, how to circulate them, and how to attract institutional capital. Figure's newly unveiled product in this deal, Adaptor, is designed precisely for this purpose.

It supports "Agent to Agent" automated integration, standardizing the diverse data formats from different originating institutions, thereby compressing the onboarding cycle for new partners.

Kiavi's assets will become the first real-world validation scenario for Adaptor after its launch. According to Figure's investor presentation materials, the company expects this transaction to achieve approximately $35 million in cost synergies within 24 months.

Two AI systems are being stitched together, pointing towards the same goal: making non-standard real estate loans priceable, tradable, and scalable on-chain.

Integration

Figure employs a dual-class share structure. According to the IPO prospectus, Cagney and his affiliates hold Class B shares, controlling about 69% of the total voting power at the time of the IPO; as of the latest proxy statement in April 2026, he still controls the majority of voting power, and Figure continues to be designated a "controlled company" by Nasdaq.

As a growth-stage company undertaking a major acquisition less than a year after its IPO, Figure also disclosed in its S-1 filing that previously existing material weaknesses in internal controls were yet to be remediated. The large-scale integration poses a non-negligible test for the execution team.

On Kiavi's side, its assets are sensitive to interest rate cycles. During the 2022 hiking cycle, lacking the backing of government-sponsored enterprises (GSEs) like Fannie Mae and Freddie Mac, the liquidity of Kiavi's assets in capital markets tightened, leading the company to make corresponding cost and personnel adjustments.

This vulnerability has already been validated during the high-interest-rate phase, and future interest rate changes will remain a significant external variable for RTL/DSCR origination volume.

Furthermore, Figure's existing assets are still heavily concentrated in HELOCs. Kiavi's asset types, data formats, and customer base are significantly different. It remains to be seen whether Adaptor can truly reduce integration costs and whether Kiavi's non-standard assets can be smoothly absorbed by institutional investors on Democratized Prime.

The good news is that Figure stated the deal will be accretive to earnings per share, with an unlevered cash payback period not exceeding 4 years, and reaffirmed its medium-term EBITDA margin target of around 60%; Kiavi's monthly loan flow exceeding $100 million will be directly fed into Democratized Prime.

Sixth Street's managed and committed capital scale of over $130 billion, along with its $3 billion forward purchase commitment, provides considerable capital buffer for the joint venture; Mohan's entry into the executive team means Kiavi's customer relationships and industry resources are retained within Figure's management structure.

The RWA narrative has been around for several years. This time, Figure is using $717 million to migrate an institution that has operated for 13 years and processes billions of dollars in real loans annually entirely onto the blockchain. This is one of the most structurally significant acquisitions in the RWA tokenization space to date.

The potential market space Figure points to is its estimated approximately $200 billion annual RTL/DSCR origination opportunity, underpinned by the long-term renovation and rental demand generated by the roughly $25 trillion stock of aging housing in the US.

If the integration proceeds smoothly, this could be a landmark node marking the transition of blockchain capital markets from "proof-of-concept" to "scale operations." Not just for Figure, but for the entire RWA credit asset market.