Author: Sanqing, Foresight News

On June 16, HYPE reached 76.965 USDT, once again hitting a new all-time high, with a daily increase of about 10%, triggering over $11.5 million in short liquidations. Meanwhile, according to SoSoValue data, three US spot HYPE ETFs have attracted a cumulative net inflow of approximately $180 million in their first month of trading, indicating sustained institutional capital inflow.

However, the scene on the Hyperliquid ecosystem side is completely different. From May to June, several protocols across multiple sectors including lending, NFT, stablecoin, and DEX have successively announced their shutdown.

HYPE is an "Application Stock"

Hyperliquid injects about 97% of protocol fees into the Assistance Fund, continuously buys back HYPE in the open market and permanently burns it. According to buildix data, the current daily buyback is about 34,000 HYPE (approximately $2.57 million), with an annualized buyback scale of about $940 million, annualized protocol revenue of about $976 million, a P/E ratio of about 73x, and a buyback yield of about 5.6%.

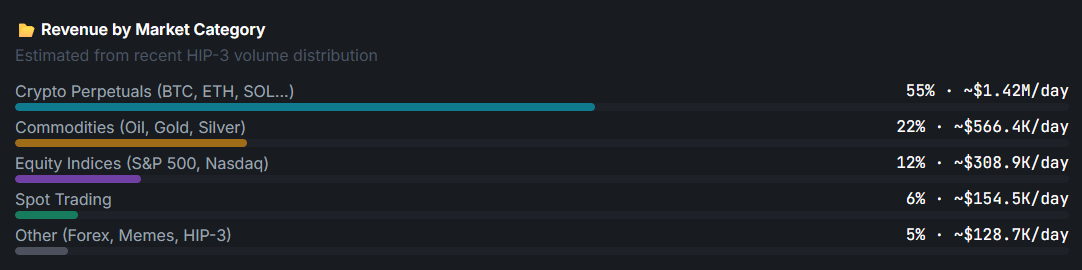

According to DefiLlama data, Hyperliquid's trading volume in the last 30 days exceeds $240 billion. This is precisely the fuel driving the buyback machine: the highly diversified revenue structure of the HyperCore perpetual contract trading layer. Crypto perpetual contracts (BTC, ETH, SOL, etc.) contribute about 55% of daily fees, commodities (crude oil, gold, silver) about 22%, stock indices (S&P 500, Nasdaq) about 12%, and spot trading about 6%.

This means HYPE resembles more of an "application-type stock" rather than a traditional "ecosystem token." Its value capture is anchored to HyperCore's trading fees and has almost no direct relationship with HyperEVM's TVL scale or the survival count of DeFi protocols.

This is fundamentally different from ETH's value logic. ETH's pricing premise is that ecosystem prosperity drives Gas consumption, which in turn pulls the token price. Therefore, the death of any ecosystem project is a negative signal for ETH.

But HYPE's fee source is almost unrelated to HyperEVM. Whether HyperEVM projects live or die does not change HyperCore's trading volume, nor does it affect the Assistance Fund's buyback pace. Investors holding HYPE are exposed to the operational risk of "the business of Hyperliquid's perpetual contract trading," not the risk of a particular DeFi protocol.

Five Announcements

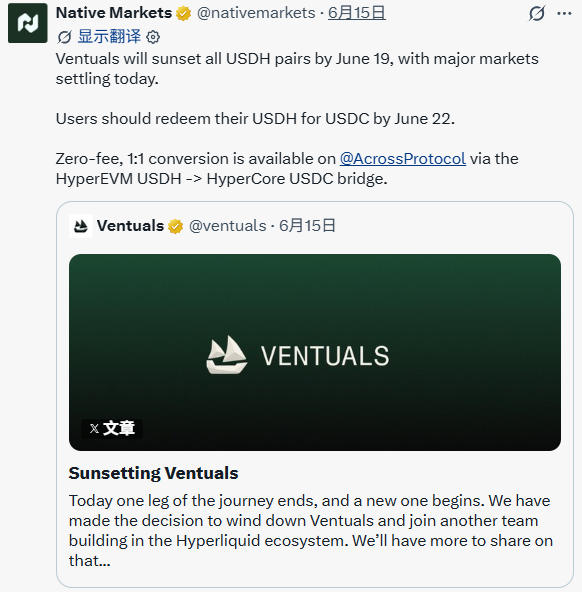

Ventuals (June 15): Cumulative trading volume exceeded $650 million, serving over 11,000 traders, with the announcement receiving 47,000 views. The team wrote: "Today, one segment of the journey ends, and a new one begins." The shutdown process was extremely orderly, listing settlement times and price mechanisms for 11 markets including OpenAI and Anthropic one by one, with user HYPE refunded in full at a 1:1 ratio.

Felix (announced June 8, terminated June 20): Announcement: "In light of the deactivation of USDH, the Felix HIP-3 DEX and all active markets will begin deactivation on June 19 and conclude on June 20."

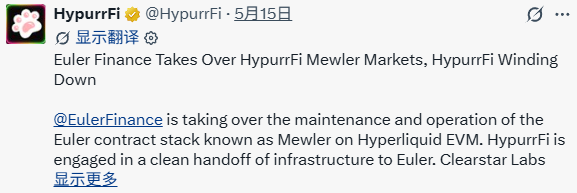

HypurrFi (May 15): Once a top lending protocol on HyperEVM, with a peak TVL exceeding $300 million. The announcement stated: "No security breach. No exploit. No emergency. This is a considered operational decision." The brand is exiting, infrastructure is being handed over to Euler Finance, and Pooled markets will complete final settlement on July 15.

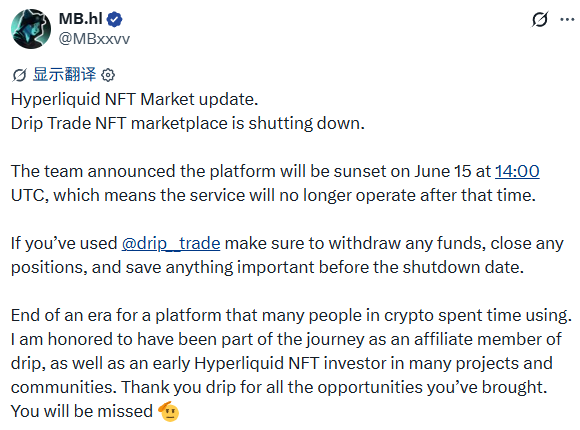

Drip.Trade (June 15): The only NFT marketplace on HyperEVM. Hyperliquid ecosystem KOL @MBxxvv relayed official news: "The platform will go offline at 22:00 on June 15, and services will no longer operate thereafter."

USDH / Native Markets (May 14): Announcement by Native Markets stated it would transfer the stablecoin brand rights of USDH to Coinbase, making Coinbase the official USDC deployer on Hyperliquid.

These five projects cover five sectors: lending, NFT, stablecoin, RWA private markets, and DEX, almost representing the main categories of DeFi infrastructure on HyperEVM. They were not marginal projects but protocols with real users and trading volume within the ecosystem at the time.

The Stronger the Core, the Harder the Ecosystem Lives

If HYPE's rise and the death of ecosystem projects were merely two independent trajectories, then this crisis would just be "the failure of peripheral projects themselves," not worth in-depth examination. But looking closely, these two events are not just happening in parallel.

Hyperliquid's design philosophy is minimalism: provide the chain and infrastructure, do not get involved in operations.

Since its launch in February 2025, HyperEVM has attracted over 170 project deployments, but from the start, there were no official grants, no coordinated market-making arrangements, no launch liquidity support. Projects faced the fully competitive secondary market head-on from day one. The core team hardly publicly participates in collaborative interactions with HyperEVM project parties; protocol projects are expected to be self-sufficient by default.

When on-chain products were scarce, any functioning protocol brought its own traffic. But the market in 2026 is already saturated. The survival of new protocols is not a technical problem; it's a cold start problem. Without official endorsement and liquidity guidance, the vast majority of projects simply cannot survive the cold start phase.

Furthermore, the HIP-3 mechanism allows anyone to directly deploy perpetual contract markets on HyperCore. It was originally an outlet for liquidity overflow, but it simultaneously diverts attention and user traffic away from protocol projects.

The leading project on HIP-3, TradeXYZ, already occupies about 97% of the market share in its category, leaving almost no room for latecomers. This means protocol projects are not only competing with external competitors but also competing with Hyperliquid's own liquidity siphon effect.

The more successful HyperCore is, the more traffic and capital it attracts, the harder it is for projects on HyperEVM to get a share. This is not HyperEVM's technical failure, but Hyperliquid's business model inherently reserves the highest-quality resources for the core layer, structurally compressing the peripheral survival space.