排名第一的智能合约网络的交易成本已达到九个多月以来的最低水平。

关键要点

自1月以来,处理交易需要消耗的的以太坊下降了94%。

以太坊的低gas费是由于对区块空间的需求减少。

历史模式表明,当使用以太坊网络的中位成本达到创纪录的低点时,以太坊的价格通常会上涨。

以太坊的Gas费已达到九个多月以来的最低点。

虽然网络活动减少是下降的主要原因,但以太坊上的唯一活跃用户数量保持稳定。

以太坊活动减少

使用以太坊的成本正在创历史新低。

根据数据分析网站Nansen的数据,今天的gas费用达到了10gwei的低点。

过去几天的平均交易成本12gwei,相当于点对点ETH转账大约需要0.67美元。

从这个数字来看,1月份,以太坊的平均gas成本高达218gwei,这表明处理交易所需的以太坊数量下降了94%。

网络上Gas费的下降是由于对以太坊区块空间的需求减少。

由于区块只包含有限的交易空间,因此在高度拥塞期间,用户会提高他们愿意支付的价格,以便在下一个区块中处理他们的交易。

然而,当活动减少时,网络会降低反映需求所需的Gas fee。

NFT市场OpenSea近几个月来一直是以太坊网络上最大的gas用户之一,但最近几周的活动有所下降。

根据token terminal的数据,OpenSea在3月13日处理了价值6750万美元的交易,比2月份的峰值水平下降了70%。

OpenSea并不是唯一一个活动减少的以太坊应用程序。

Uniswap是以太坊上最受欢迎的去中心化交易所,自去年11月以来,交易量一直在稳步下降。

3月12日,该交易所的交易量创下了7.99亿美元的数月新低。

相比之下,该交易所在11月10日达到高峰时,在24小时内处理了价值88亿美元的巨额交易。

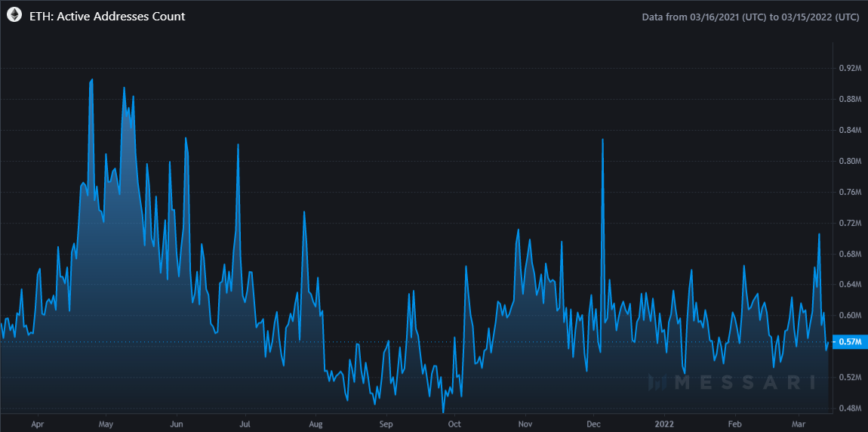

尽管对以太坊区块空间的需求在减少,但积极使用网络的钱包数量似乎并没有减少。

根据Messari的数据,唯一活跃的以太坊地址的数量一直保持在500,000以上,并且没有达到2021年夏季观察到的低点。

以太坊唯一活跃地址(来源:Messari)

由于以太坊上唯一活跃用户的数量保持不变,这意味着用户仍在该网络上进行交易,只是比以前少了。

对于许多以太坊高级用户来说,低gas费可能是一件好事。

由于网络交易现在更便宜,交易者能够利用较小的套利机会,从而提高资本效率。

较低的gas费对更多临时用户来说也是一种友好,在OpenSea等平台上购买和上架NFT的成本也变得非常便宜。

那些正在等待空投或需要获得奖励的用户将能够不像在费用达到历史新高时那样消耗他们的利润。

虽然Gas费很低,但不一定会长期保持这种状态。

从历史模式来看,每当使用以太坊的成本中位数达到创纪录的低点时,由于以太坊的价格上涨,它通常会回升,类似事件是否会很快上演还有待观察。