Curve 并非靠运气挺过每一次熊市。

它之所以能存活下来,是因为它专为一件事而打造:可持续性。

从 2019 年的一个数学实验到 2025 年成为全球流动性支柱,Curve 的发展历程就是真实收益、激励协调一致和社区韧性的演进。

下面一起逐年回顾:

2019 年:StableSwap(一种新的 AMM 理念)的诞生

当时 DeFi 还处于萌芽阶段。像 DAI、USDC 和 USDT 这样的稳定币很受欢迎,但交易者面临高滑点,流动性提供者(LP)的收益也很低。

Michael Egorov 发现了这一缺陷,并推出了 StableSwap,这是一种新的 AMM 模型,结合了常和函数(constant-sum)与常积函数(constant-product),使稳定资产的滑点接近于零。

这并非只是另一个 DEX 概念。

这是一个数学上的突破,为 LP 带来了深度流动性与真实收益。

StableSwap 成为了 Curve Finance 的基因:首个真正为稳定币效率而优化的 AMM。

2020 年:Curve Finance 与 veTokenomics 的曙光

2020 年初,Curve Finance 正式上线,其使命明确:

通过高效的稳定币流动性提供稳定的收益。但其真正的创新出现在 2020 年 8 月,推出了 CurveDAO 和 veCRV 模型(投票锁仓机制),这是一种重新定义 DeFi 治理的代币经济设计。

Curve 不再奖励短期参与者,而是激励长期合作:

- 锁定 CRV --> 获得 veCRV

- 投票决定哪些资金池获得奖励

- 获得更高的收益

这种结构构建了一个良性飞轮,将 LP 转变为利益相关者,并开启了传奇的 “Curve 之战”,Convex、StakeDAO 和 Yearn 等 DAO 为争夺 veCRV 权力而展开激烈竞争。

到年底,Curve 的 TVL 超 10 亿美元,巩固了其作为 DeFi 流动性支柱的地位。

2021 年:扩大流动性,深化社区

2021 年,Curve 证明了其可扩展性。

- 其日交易量达到 10 亿美元,每天产生 40 万美元的费用,全部分配给 veCRV 持有者。

- Tricrypto(USDT/WBTC/WETH)的推出使 Curve 超越了稳定币的范畴。

当其他项目追求不可持续的收益时,Curve 则专注于真正的收益和流动性深度。

每次交易都创造了价值,每个 LP 都获得了真实的收益。

与此同时,社区逐渐成熟,治理投票增加、贿选(bribes)行为加剧,“Curve 之战”将治理变成了一场经济与博弈论交织的杰作。

Curve 不再仅仅是一个协议,而是一个经济生态系统。

2022 年:熊市压力测试

随着 2022 年熊市重创“DeFi 2.0”,Curve 的基本面受到考验,但表现坚挺。

即便 DeFi 领域的流动性普遍枯竭,Curve 的 StableSwap 不变系统和 veCRV 结构仍使激励机制保持一致:

- 2022 年 1 月 TVL 超过 240 亿美元达到峰值,到 2022 年年中,Curve 仍有超过 57 亿美元的 TVL

- LP 从稳定的交易量中获得稳定的费用

- 由于长期锁定,CRV 的抛售压力保持在低位

Curve 还通过 Aurora、Arbitrum 和 Optimism 扩展了跨链业务,巩固了其作为多链流动性标准的地位。

在其他项目纷纷消失之际,Curve 用实际行动展示了经济韧性。

2023 年:危机与社区韧性

2023 年 8 月,Curve Finance 因 Vyper 编译器漏洞被攻击,损失约 7300 万美元,多个稳定币池受到影响。对大多数协议来说,这无疑是致命的打击。

但 Curve 却挺了过来。

几周内,白帽黑客、合作伙伴和 veCRV 持有者迅速行动。通过社区协调和谈判,73% 的被盗资金得以追回,这在 DeFi 历史上实属罕见。

与此同时,Curve 推出了 crvUSD,这是一种去中心化的超额抵押稳定币,为 veCRV 持有者带来了真正的实用价值和新的收益来源。

Curve 的社区证明了它不仅活跃,而且经过了实战考验。

2024 年:扩展生态系统飞轮

Curve 从自动做市商(AMM)发展成为一个完整的 DeFi 生态系统:

- LlamaLend:无需许可的借贷服务,支持 ETH 和 WBTC 作为抵押品。

- Savings crvUSD (scrvUSD):一种产生收益的稳定币,连接了 DeFi 和 TradFi。

- CRV 的通胀率降至 6.35%,巩固了代币长期价值。

- 与贝莱德支持的 BUIDL 基金建立的合作关系,将 Curve 的流动性与机构资本相连接。

veCRV 系统继续支撑着这一增长:将用户、DAO 乃至机构围绕 Curve 的流动性引擎进行整合。

2025 年:流动性、收益与传承

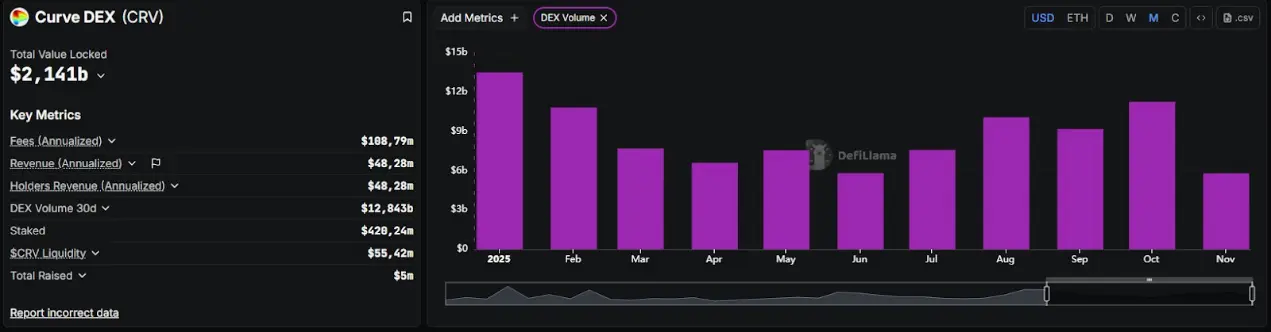

到 2025 年,Curve 不再仅仅是一个 DEX,它已成为 DeFi 流动性的支柱。

第一季度交易量达到 346 亿美元(同比增长 13%),超过 550 万笔交易,日均交易量 1.15 亿美元,该协议继续为 veCRV 持有者每年产生 1940 万美元的费用。

crvUSD 达到 1.78 亿美元的历史最高市值,而 Curve 则在全球 DEX 中排名第二,TVL 达 19 亿美元。

最初作为稳定币自动做市商(AMM)的项目,现已发展成为一个基于数学(StableSwap)、经济学(veTokenomics)和社区信念的自给自足的流动性网络。

经受住周期考验的秘诀

Curve 的三大支柱是:StableSwap 提供的流动性深度;veTokenomics 提供的激励机制;社区的韧性。

当热门项目兴衰更迭之际,Curve 始终坚守其核心优势:将流动性转化为基础设施,将收益转化为持久价值。

Curve 的创立并非为了昙花一现,而是为长久发展而建。