作者:0xNatalie来源:ChainFeeds

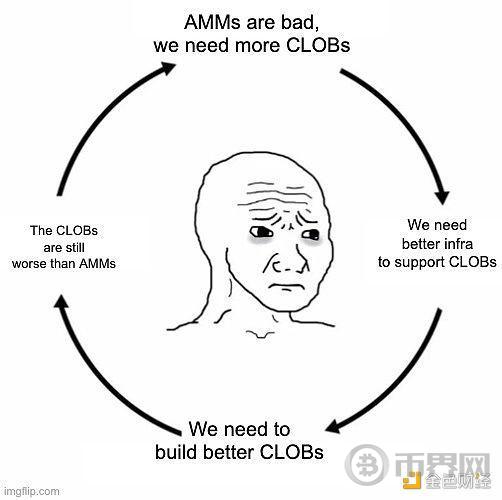

近日,Flashbots 战略主管Hasu指出:在 Solana 链上,大部分交易量实际上是通过自动做市商(AMM)完成的,而不是通过中央限价订单簿(CLOB,或简称为订单簿模式)。这一结论令人意外,因为不少人曾认为 Solana 赢得市场的的重要原因之一其能够支持 CLOB。如Feng Liu所说:「当初 Solana 的一个核心卖点,就是终于可以在上面搞订单簿 dex 了,以及,『订单簿交易才是 dex 的未来』。」

值得注意的是,AMM 和 CLOB 之间的争论并非始于近日,这场较量早已持续多时。自 DeFi Summer 以来,AMM 凭借其算法驱动的资产定价方式迅速成为去中心化交易的核心,而 CLOB 则因其在传统金融和中心化交易所中的主导地位,被认为是更成熟的市场机制。这场较量推动了它们在各类区块链平台上的不断创新。尤其是在以快速和低成本为核心的 Solana 上,Phoenix成功让 CLOB 一度成为焦点。

AMM 主导市场的原因仅在于长尾资产?

Hasu 的这一发现在社区内迅速引发了广泛讨论。对此,Multicoin Capital 合伙人 Kyle Samani解释道,在长尾资产的市场中,缺少真正的做市商(MM)来提供流动性,而 AMM 的出现弥补了这一不足,从而形成了当前 AMM 主导的局面。Solana 的成功不仅仅依赖于 CLOB,而是因为它能够提供始终如一的快速和低成本的交易体验,能够为各种类型的资产提供支持。此外,Solana 的无桥接机制(no bridging)也是其成功的一个重要因素,因为用户普遍对跨链桥接持负面态度。

Taproot Wizards 创始人 Udi Wertheimer 也认为AMM 在支持长尾资产方面具有独特优势,能够帮助小型社区为长尾资产快速启动流动性。Solana 上有大量的 memecoin,对于这些资产来说,AMM 是非常合适的选择。

Krane 则进一步将市场划分为三种类型:memecoin、主要资产(如 SOL/USDC)和稳定币。他指出,AMM 在 memecoin 市场中表现突出,因为这些资产需要良好的被动流动性,而 CLOB 在这方面表现较差。对于主要资产,虽然 CLOB 在一些情况下占据了一定地位,但 AMM 仍然具有竞争力。在稳定币市场中,CLOB 的应用尚未广泛普及。

然而,Ambient 创始人 Doug Colkitt 提出了不同的看法,并通过数据进行了反驳。他指出,许多人误认为 Solana 上的 AMM 交易量主要来自一些不活跃的长尾资产。然而,他提供的数据表明,即使在主要交易对(如 SOL/USDC)中,AMM 的交易量也远远超过了 CLOB。例如,Orca在 24 小时内的交易量高达 2.5 亿美元,而 Phoenix 的交易量仅为 1400 万美元。即使采用最有利于 CLOB 的假设(使用 Phoenix 的 7 天平均每日交易量而不是当天的较低交易量,并尽可能多地计入 CLOB 的交易量),AMM 在主要交易对上的交易量也比 CLOB 高出 50%,如果不采用这些假设,差距甚至会扩大到 10 倍。

社区观点:CLOB 的发展受到区块链性能的限制

AMM 在 Solana 上占主导地位的原因不仅仅在于长尾资产,更深层次的原因在于区块链性能的限制。许多社区成员认为,CLOB 的发展受限于区块链的性能瓶颈。Sam觉得区块链面临的固有挑战(高延迟、Gas 费高、隐私保护不佳等)使得 CLOB 不适合在当前的区块链环境中有效运行。相比之下,AMM 更能适应区块链的特点,尤其是在价格发现和流动性提供方面。

Enzo也持类似观点,他认为 CLOB 在 Layer 1 上面临高延迟、昂贵的 Gas 费用和较低吞吐量的局限性,但在 Layer 2 解决方案中,这些局限性可以被克服,从而使 CLOB 在这些环境中更具竞争力。在当前的 Layer 1 链上,AMM 仍然是更为实际的选择。

实际上,在 Reforge Research 4月发布的《Death, Taxes, and EVM Parallelization》一文中也提到过类似观点。文章里指出:在以太坊等区块链平台上实现 CLOB 时,由于平台处理能力和速度的限制,往往会导致高延迟和高交易成本。然而,随着并行 EVM 的推出,网络的处理能力和效率得到极大提升,CLOB 的可行性也随之增加,并预计 DeFi 活动将显著增加。