Примечание редактора: пока Майкл Сейлор продолжает увеличивать экспозицию компании к биткоину с помощью таких инструментов, как STRC, финансовая структура, кажущаяся эффективной, одновременно накапливает дивидендные обязательства и потенциальные риски. В краткосрочной перспективе это стимулирует приток капитала и рост цен; но как только рынок развернется, этот механизм, зависящий от постоянного финансирования, может быстро обернуться против самой компании. Данная статья исследует эту структуру, пытаясь определить её пределы в экстремальных сценариях и возможные каскадные эффекты.

Далее следует оригинальный текст:

С помощью STRC Сейлор создал «монстра Франкенштейна».

Виктор Франкенштейн создал этого монстра из-за собственного высокомерия — он был уверен, что может играть роль Бога и бросить вызов смерти. Но после того, как монстр уничтожил его семью и друзей, он в конечном итоге погубил и его самого.

С помощью STRC Сейлор разработал «идеализированный» инструмент, привязанный к BTC, позволяющий розничным инвесторам получать сверхдоходность от биткоина почти как «безрисковую ставку». Именно эти способности в области финансового инжиниринга позволили ему заявить о беспрецедентном коэффициенте Шарпа и доходности в 11,5% при волатильности всего в 1 пункт — но в конечном счете этот механизм может также обрушить и MSTR.

Примечание: следующий анализ основан на предпосылке — BTC движется в боковом тренде или снижается. Если BTC сможет достичь сложного темпора роста в 20–25% и более, заложенного во внутренних расчетах Strategy, то многие из этих предположений станут недействительными (но не все).

Только за последние две недели STRC привлек почти $3,5 млрд притоков, а общий объем эмиссии достиг $8,5 млрд. Вместе с другими привилегированными инструментами Strategy, текущий объем находящихся в обращении средств составляет около $13,5 млрд (здесь не учитываются конвертируемые облигации). Эти средства от финансирования, с одной стороны, поддерживают соответствующий объем покупок BTC, и, вероятно, были основной движущей силой роста цены до $78 000 на прошлой неделе; но в то же время они создают ежегодные дивидендные обязательства в размере около $400 млн.

Ранее у Сейлора был дивидендный резерв в размере около $2,25 млрд. До апрельского раунда эмиссии этого резерва хватало примерно на 25 месяцев выплат. Но только新增发行 за последние две недели сократило этот период покрытия до 18 месяцев. Чтобы вернуться к 25 месяцам, ему потребуется привлечь еще около $500 млн через ATM-эмиссию (дополнительную эмиссию по рыночной цене).

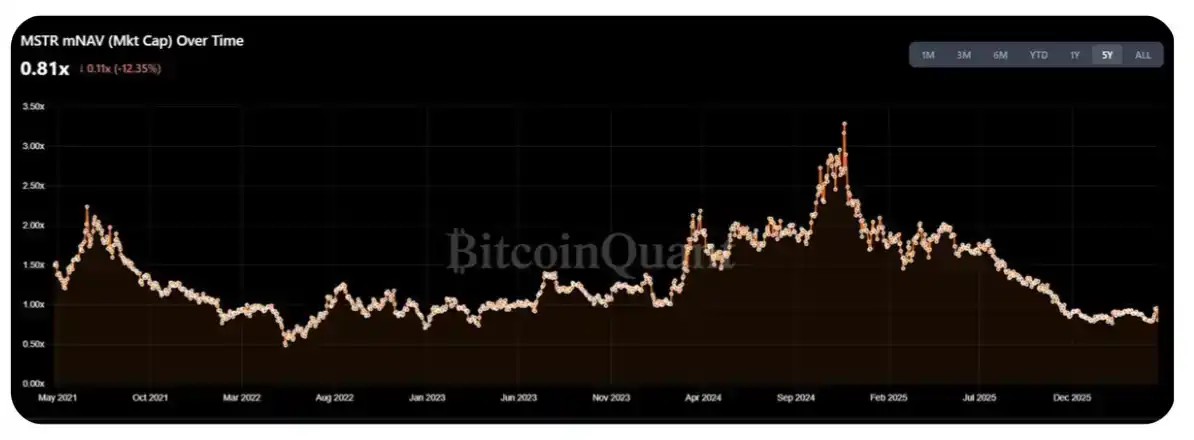

В настоящее время mNAV (скорректированная чистая стоимость активов) MSTR откатилась до уровня 1,25–1,30 от годовых максимумов, что на этой неделе вновь побудило сообщество криптоэнтузиастов (CT) призвать к масштабным покупкам BTC. Однако проблема заключается в том, что, по моему мнению, около 50–70% от новой эмиссии на этой неделе будет направлено на пополнение дивидендного резерва, а не напрямую на покупку BTC.

Более важно задуматься о поведении STRC в «экстремальном сценарии». Текущая рыночная капитализация MSTR составляет около $55–60 млрд. Тогда возникает практический вопрос: какой объем STRC Сейлор еще может выпустить до того, как дивидендная нагрузка окажет существенное давление на mNAV?

Простой способ оценки: годовой объем эмиссии можно контролировать на уровне 1–2% от среднедневного объема торгов (ADV) MSTR. При текущем дневном объеме около $2–3 млрд и 252 торговых днях в году это примерно соответствует пространству для эмиссии в $5–15 млрд — что эквивалентно 3–10-кратному размеру текущих годовых дивидендных/купонных выплат.

Но я скорее склонен считать, что этот интервал представляет собой «верхний предел», а не обычный уровень. На самом деле, для акционеров, владеющих только обыкновенными акциями, структурная стоимость этой сделки уже начинает проявляться: успех STRC, по иронии, давит на mNAV MSTR — тогда как в рамках бокового тренда с 2023 года этот показатель был ближе к 1,5 (конечно, можно возразить, что текущая среда больше напоминает первую половину 2022 года).

На поверхности кажется, что для акционеров обыкновенных акций продолжать поддерживать эти «доходности», которые не преобразуются в их собственный апсайд, является нерациональным поведением — при постоянной эмиссии количество BTC на акцию не увеличивается существенно (хотя это во многом также связано с тем, что сама Strategy уже стала слишком большой).

Как бы то ни было, акционеры DAT сами по себе являются довольно «особой» группой, и я могу представить, что они еще способны выдерживать такое давление, по крайней мере, в течение следующего года они могут не поменять свое мнение.

Кроме того, приведенный выше анализ подразумевает ключевую предпосылку: MSTR в обозримом будущем сможет удерживаться выше отметки в 1x mNAV. Если она упадет ниже 1x, то продажа BTC Сейлором будет разбавлять акционеров меньше, чем прямая эмиссия акций. Это откроет шлюзы для предложения и приведет рынок в фазу, где доминирует «рефлексивность DAT в нисходящем тренде» —这一点 я обсуждал еще в прошлом году (см. оригинальный пост).

Кратко резюмирую эту логическую цепочку:

STRC продолжает расширяться;

По мере роста объема Сейлору нужно выплачивать все больше дивидендов;

Покупатели MSTR постепенно осознают, что они покупают акции, которые фактически финансируют выплату дивидендов, а не用于 увеличения позиции в BTC;

Покупатели понимают, что это не та структура сделки, которую они изначально ожидали, и начинают выходить;

Как только не станет новых покупателей, mNAV падает ниже 1x;

mNAV < 1x → Сейлор вынужден продавать BTC, а не продолжать эмиссию акций;

Рынок впадает в панику.

На мой взгляд, правильный способ определить максимальный объем предложения STRC — это найти «переломный момент»: когда дивидендное бремя от новой эмиссии начинает превышать предельную выгоду от роста количества BTC на акцию. Согласно粗略ной оценке, этот переломный момент примерно соответствует годовым дивидендным выплатам в $3–4 млрд, что эквивалентно дополнительной эмиссии STRC на $10–20 млрд. При текущих темпах этого можно достичь в течение 6 месяцев.

Конечно, у Сейлора еще есть пространство для маневра. Дивидендный резерв действительно помогает стабилизировать цену и доверие рынка, но если боковой или нисходящий тренд сохранится, держатели, по сути, играют в «горячую картошку». Когда дивидендный резерв останется на 6–9 месяцев, рациональным выбором может стать досрочный выход в ценовом диапазоне 90–95, а не принятие на себя риска снижения из-за возможной приостановки выплат дивидендов Сейлором (это еще один его вариант).

Хотя дивиденды по STRC являются «кумулятивными», в экстремальной ситуации я считаю, что Сейлор скорее выберет «полную потерю кредитоспособности привилегированных акций», чем будет вынужден проводить масштабные продажи BTC. По сути, он сталкивается с следующей арифметической задачей: «Если выполнять обязательства по привилегированным акциям, отказавшись от будущего пространства для эмиссии, сколько еще BTC я смогу купить» - «Количество BTC, которое придется продать для поддержания привилегированных акций» = Результат

Если результат положительный, то выбрать продажу BTC; в противном случае — «пожертвовать» держателями привилегированных акций.

Основной контраргумент против этого суждения заключается в том, что если дело действительно дойдет до необходимости решать эту задачу, рынок, скорее всего, уже развернется, а mNAV MSTR с большой вероятностью упадет ниже 1x.

Спасибо за чтение, даже если начало было несколько «сенсационным». Также приветствуются любые иные мнения или критика. (Благодарность @TraderBot888, первому, с кем я обсуждал эту идею.)