撰文:Ruthy

编译:Chopper,Foresight News

大多数 Web3 项目完全忽视了搜索引擎优化(SEO)。它们想当然认为用户和合作伙伴不会主动去谷歌搜索,觉得有了 Discord 和 Twitter,自然流量就无关紧要。

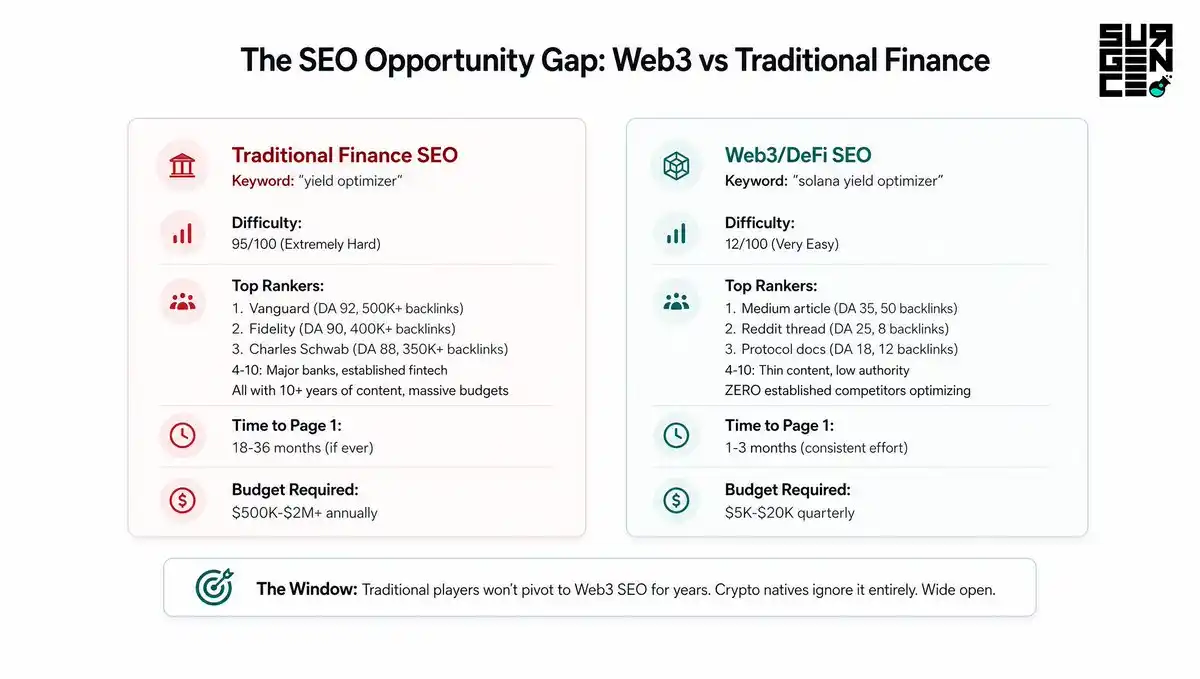

但现实数据摆在眼前:「Solana 收益优化」 月搜索量达 8000 次,「最佳加密预测市场」 月搜索 1.2 万次,「杠杆代币交易」 月搜索 1.5 万次。

这些关键词的竞争程度如何?很弱。关键词难度评分在 10 到 25 之间。传统金融机构不愿涉足这类赛道,加密从业者也尚未意识到 SEO 的价值。

眼下有 12–18 个月的窗口期,谁先入局,谁就能垄断 Web3 自然搜索流量。以下是具体做法。

为什么 Web3 项目普遍忽视自然搜索流量

Web3 公司放弃 SEO 主要有三个原因:

原因一:误以为目标用户不会主动搜索

固有认知认为加密用户都是从推特、社群发现新项目,不会用谷歌。现实真相是早期原生玩家确实不靠搜索,但未来千万级增量新用户一定会搜。

新手想找 DeFi 收益工具,第一反应就是谷歌;听说预测市场想深入了解,也会主动搜索。谷歌首页排名,直接决定用户最终选择哪一个协议。

原因二:误以为 SEO 见效太慢

传统金融赛道,竞争激烈的关键词往往要 18–36 个月才能做上排名。但 Web3 完全不同,只需 1–3 个月。行业竞争极弱,只要持续稳定输出内容,一个季度就能冲上谷歌首页。

原因三:不懂区块链产品该怎么做 SEO

加密行业 SEO 和普通 SaaS 行业完全不一样:关键词逻辑不同、内容结构不同、技术优化要求也不同。绝大多数 Web3 团队内部没有 SEO 专业人才,索性直接放弃。

如何提前抢占赛道

当前行业窗口期巨大,完整落地步骤如下:

第一步:挖掘关键词

借助 Ahrefs、SEMrush 等工具,搜索「某公链 + 收益优化器」「最佳某类型加密协议」「如何在 DeFi 进行某类操作」之类关键词。

筛选标准:月搜索量 1000+、关键词难度低于 30、具备商业转化意图。

例如:Solana 质押收益、加密杠杆交易、预测市场平台、DeFi 流动性挖矿。这类词既有稳定搜索量,又几乎没有强势竞品。

第二步:快速搭建权威内容壁垒

只需 30–50 篇优质文章,就能建立网站域名权威度。每周发布 3–5 篇,持续 8–12 周即可。内容聚焦实操教程、竞品对比、行业科普、协议深度解析、市场行情分析四种类型。

以「Solana 收益优化器」关键字的示例结构:

- 文章 1:「什么是 Solana 收益优化器?完整指南」

- 文章 2:「五大 Solana 收益优化器对比」

- 文章 3:「如何最大限度地提高 Solana 链上收益」

每篇文章瞄准一组相关长尾关键词,自然植入自家产品链接,同时累积行业主题权威度。

第三步:获取高质量外链

Web3 最高价值外链来自项目生态合作、行业博客、加密新闻媒体、研究平台、社区论坛。

有效实操方式是在 CoinDesk、Decrypt、The Defiant 等媒体发布客座稿件,与其他项目官宣生态合作,发布生态集成指南,输出原创行业研究报告并被加密分析师引用转载。

目标:每月发布 5–10 条优质外链,优先选择域名权重 40 以上的权威站点。

第四步:针对加密货币搜索进行优化

加密用户的搜索话术和传统金融完全不同。他们搜 APY,而不会输全称年化收益率;搜 TVL,而不会完整拼写锁仓总价值;用 Degen 指代高风险投机玩家。

写内容要贴合圈内术语,用用户的语言,回答用户真正关心的问题。

区块链产品的专属技术 SEO 优化

区块链项目有很多专属技术 SEO 要点,绝大多数团队都会忽略。

定制化 Web3 结构化数据标记

通用搜索引擎结构化数据无法适配加密产品,需要自定义 Schema 标记。需包含:协议类型、支持公链、TVL、APY 区间、安全审计状态、智能合约地址。这些可以帮助谷歌精准识别项目业务属性,在相关搜索中获得更多曝光。

DApp 页面提速优化

Web3 原生 DApp 普遍加载缓慢,钱包连接、链上数据查询、实时行情都会增加延迟。

解决方案:官网营销页与 DApp 应用页拆分。营销宣传页保证极速加载、抢占排名、承接流量;DApp 页面可以适当放宽速度要求,用户已经认可品牌后再进入使用。

目标:营销页面加载时长控制在 2 秒内。

内容持续更新策略

加密行业行情变化极快,内容必须保持时效性。核心页面每周更新:TVL 数据、APY 收益率、支持资产列表、协议关键指标。谷歌对高速迭代行业格外青睐新鲜内容。

文章标注「最新更新时间」,爆款内容每 90 天更新迭代一次。

内链架构布局

采用中心页面 + 分支页面架构搭建全站逻辑。

例如:中心页面:「Solana 链上收益优化全」》(主攻核心大关键词)分支页面:各类收益策略指南、协议对比、技术文档。所有分支页面链回枢纽页,中心页面反向内链辐射所有分支页面。

这种架构可以高效传递页面权重,也便于谷歌识别全站主题关联。

时间表:90 天冲上谷歌首页

以下是一个比较实际的 Web3 SEO 落地时间表:

第一个月:第 1–2 周,关键词调研、竞品分析、网站技术审计、制定内容策略;第 3–4 周,核心页面上线、首发 10 篇文章、部署结构化标记。

第二个月:第 5–6 周,再更新 20 篇文章、行业媒体客座稿、项目合作官宣;第 7–8 周,首批优质外链落地、完善全站内链,关键词逐步冲到谷歌第二、三页。

第三个月:第 9–10 周,爆款内容精细化优化、加码外链布局、冲刺精选摘要位;第 11–12 周,5–10 个核心关键词稳定在谷歌首页、自然流量持续上涨,开始进入维护模式。

结语

当下,SEO 是 Web3 最容易搭建的一条护城河。

传统金融机构未来数年都不会入局加密关键词,加密原生团队普遍轻视 SEO、不懂玩法。行业窗口期完全敞开。

只需 90 天稳定深耕,就能拿下多个核心关键词的谷歌首页排名;整体投入成本 1.5 万–2.5 万美元,换来的是长年复利增长的稳定自然流量。趁成本还低、竞争还弱,尽早筑起你的 SEO 护城河。