Editor's Note: The simultaneous rise in gold and Japan's 10-year yield contrasts sharply with the weakness in Bitcoin. This article points out that this divergence reflects a market shift from 'tightening trades' to 'risk pricing,' and every move by the Bank of Japan could become a key variable in breaking the current pattern.

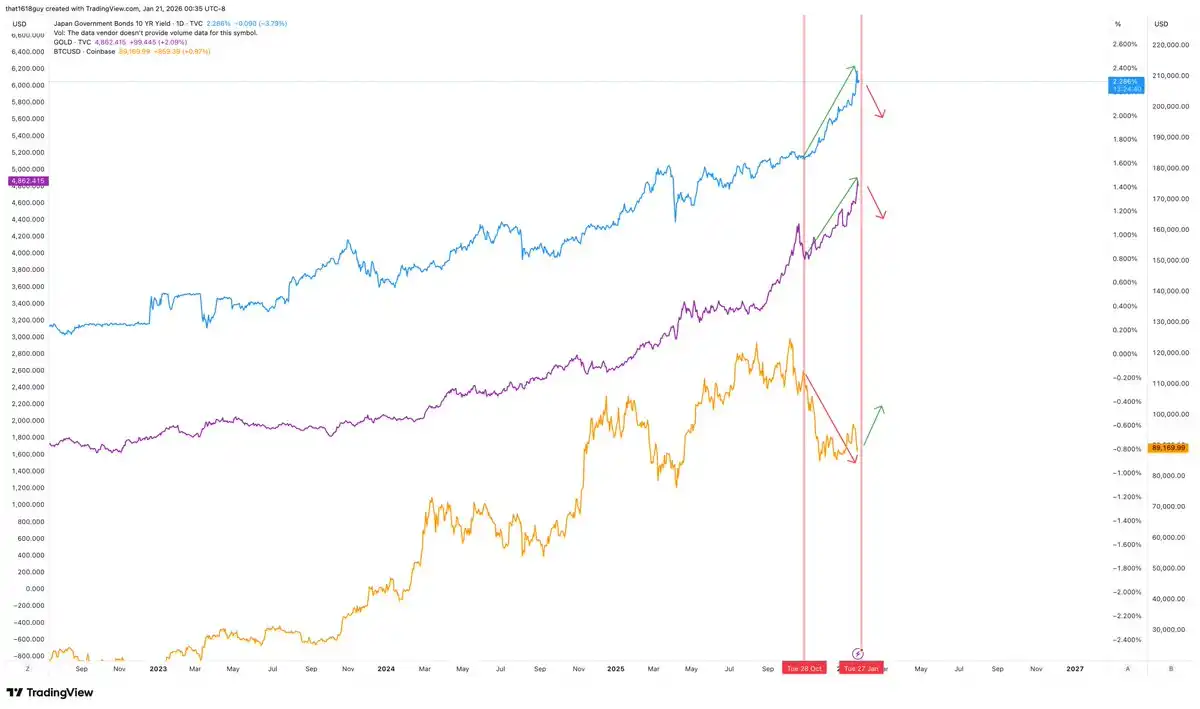

One of the most intriguing macro trends currently is the联动 relationship between gold and Japan's 10-year government bond yield. These two assets are moving in sync, which defies the norm in a typical monetary policy tightening cycle.

The following will analyze why gold is following the movement of Japanese yields, why Japan has become a key pressure point in the market, and the potential impact on Bitcoin if the Bank of Japan intervenes.

Gold and Japanese Bonds Climb Together... While Bitcoin Moves in the Opposite Direction

In a常规 environment, rising long-term yields suppress gold prices by increasing the opportunity cost of holding non-yielding assets. This negative correlation only breaks when yields deviate from the market's normal development and instead signal policy pressure. The current sharp surge in Japan's 10-year yield, with gold rising同步, precisely confirms the latter scenario.

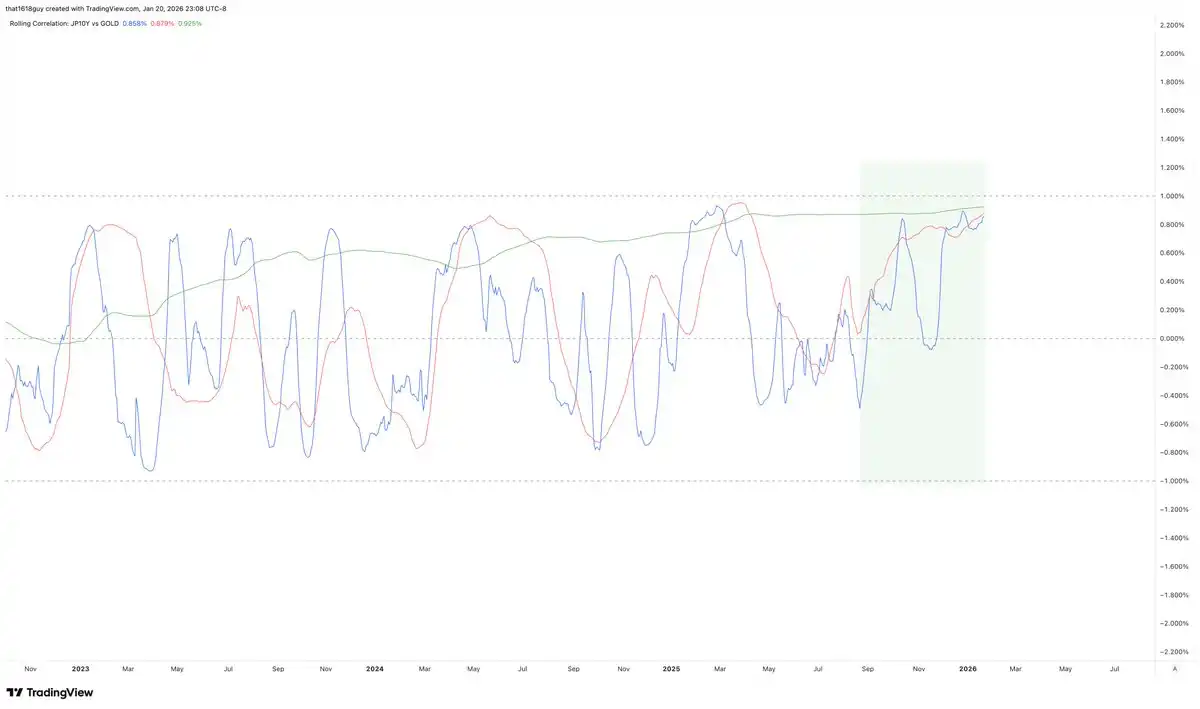

This correlation chart clearly reveals this shift.

The blue line in the chart shows the 30-day correlation between Japan's 10-year yield and gold. Although it still has fluctuations, the duration it stays in positive territory has significantly increased, rather than quickly falling into negative territory. This alone indicates that the traditional inverse relationship is weakening.

More importantly, the red line representing the 90-day correlation has followed suit and risen, indicating this is not short-term noise. Most convincing is the green line representing the 1-year correlation: it has steadily climbed and stabilized in positive territory.

When long-term correlations turn positive and remain high, it often signals a fundamental change in market logic. Rising Japanese bond yields no longer pose阻力 to gold but are instead interpreted by the market as a stress signal that gold is absorbing. This suggests the market views yield increases as a risk signal, not merely a tightening signal.

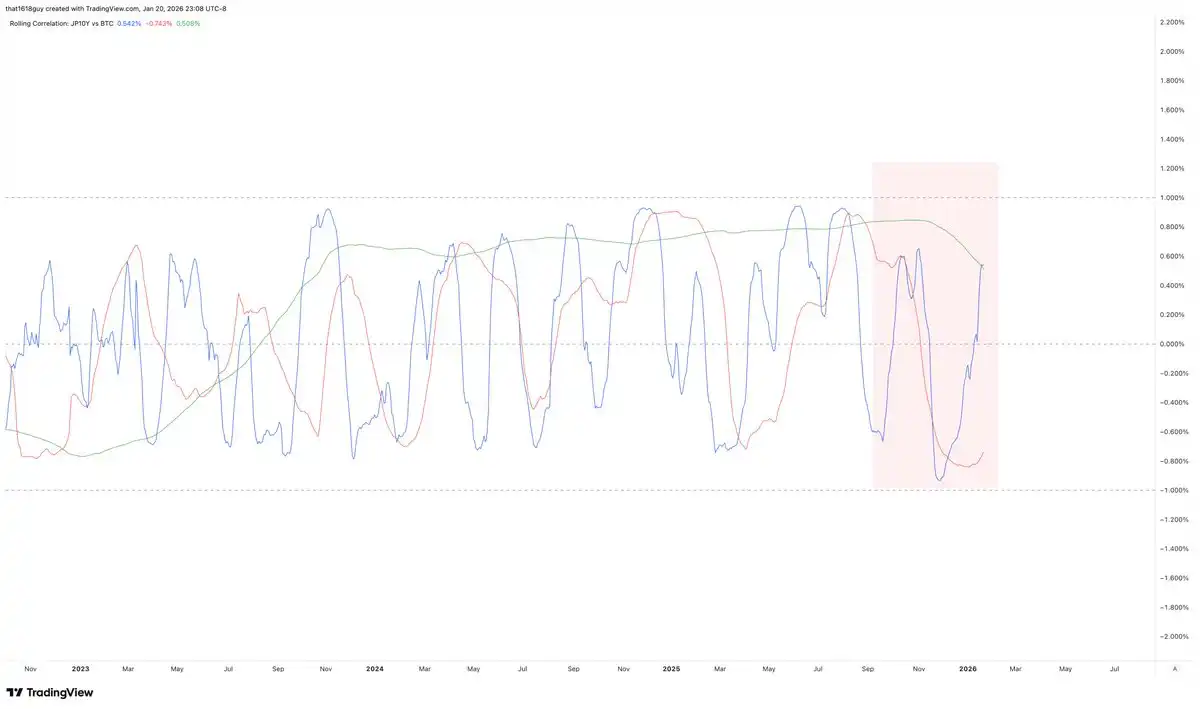

Even more interesting is that other markets haven't shown a similar phenomenon. During the same period, Bitcoin and Japan's 10-year yield have maintained a negative correlation.

A second correlation chart highlights this contrast.

The 30-day and 90-day correlations between Japan's 10-year yield and Bitcoin, while volatile as expected, primarily operate below the zero axis, reflecting Bitcoin's sensitivity to short-term macro pressures. Most crucially, the green 1-year correlation line has turned downward and remains negative, indicating that over a longer time horizon, Bitcoin consistently faces pressure when Japanese yields rise.

In other words, to see sustainable signs of a rebound, we need Japan's 10-year yield to start cooling down—theoretically, this would also be reflected in the gold price.

How to Interpret the Current Market Logic

When gold and sovereign bond yields rise together, the market is pricing not economic growth or enhanced monetary policy discipline, but credit risk and balance sheet fragility.

This pattern typically emerges under the following circumstances: hedging demand overpowers arbitrage logic, policy control capabilities are questioned, and rising yields expose duration mismatches rather than抑制 economic activity. In this environment, gold acts less like an inflation hedge and more like a balance sheet hedge.

The inverse relationship between Bitcoin and Japanese yields reinforces this interpretation. The market views rising Japanese yields as a tightening shock. Gold benefits from this while Bitcoin does not. This current divergence is a key signal.

Why Japan is the Key Pressure Point

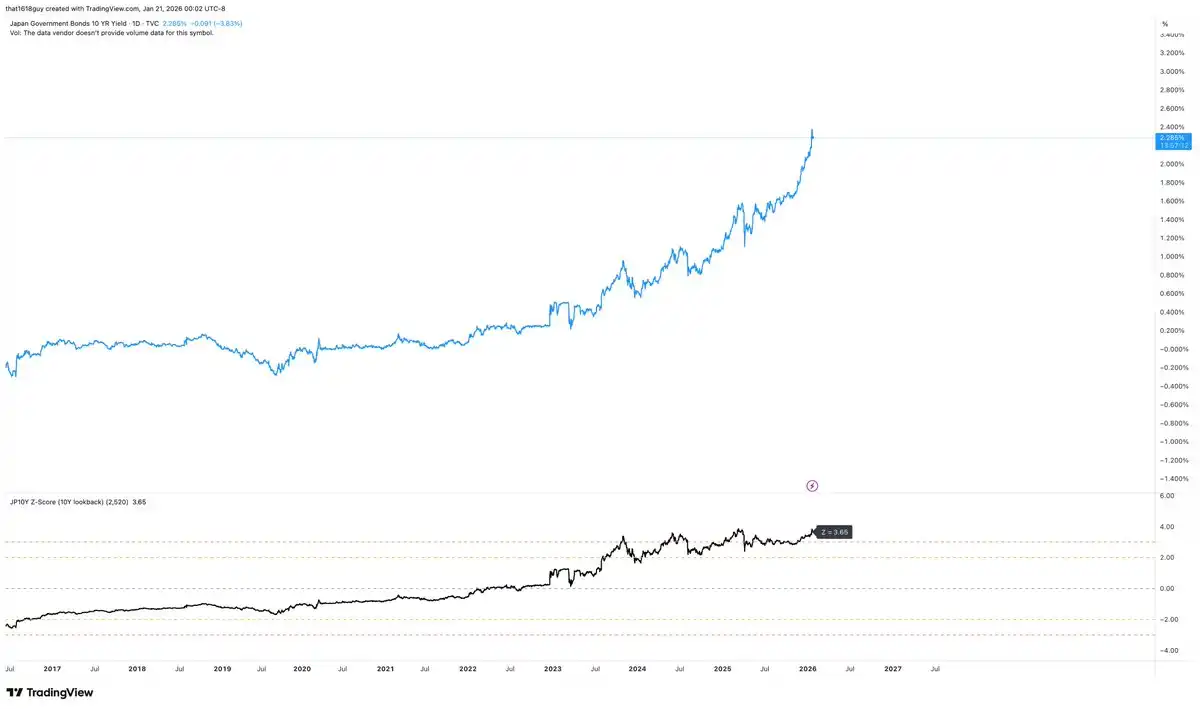

Japan has a unique sensitivity to this dynamic. The straight-line rise in Japan's 10-year government bond yield shown in the chart above is by no means a neutral event for its domestic financial system. The key is not just that yields are rising, but that the magnitude of the increase has reached statistically extreme values relative to Japan's own policy framework.

Calculated on a rolling 10-year window, the current Japan 10-year yield is about 3.65 standard deviations above its long-term average. This is equivalent to flipping a coin 13 times in a row and getting heads every time.

This is noteworthy in any market. But in Japan, where long-term yields have been strictly controlled for the past decade, a fluctuation of this magnitude clearly signals that the policy anchor is loosening. This is a classic特征 of the old order unraveling.

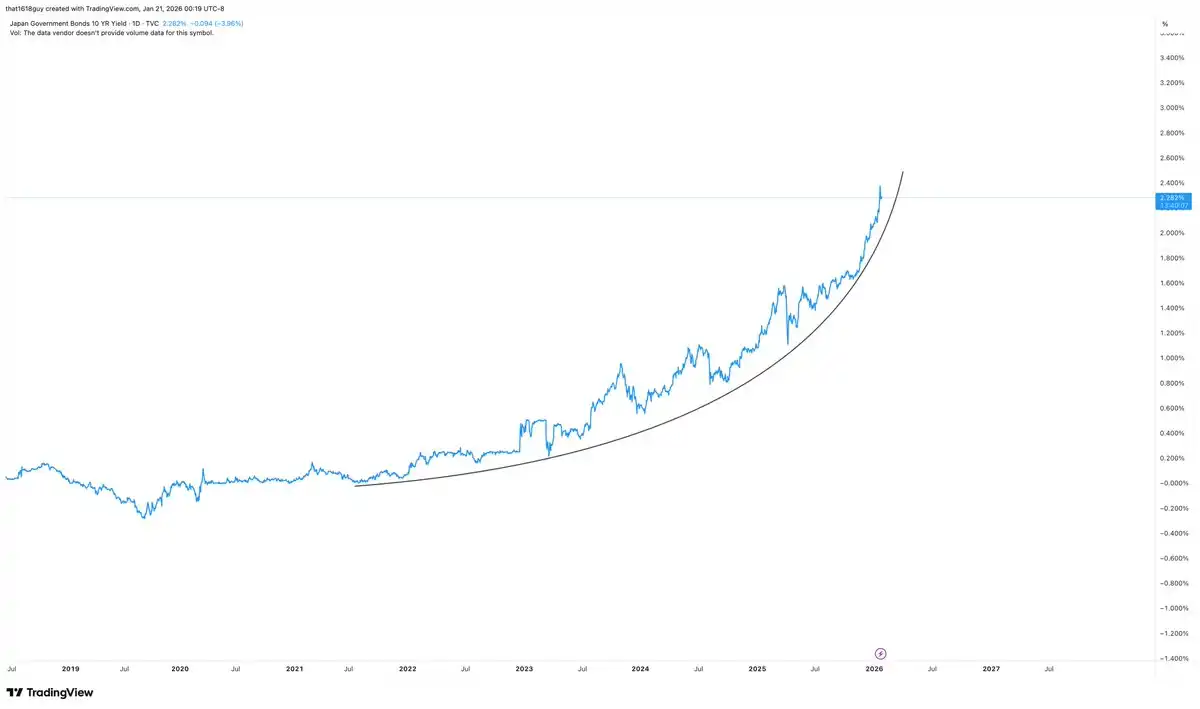

As important as the absolute level is the speed of the increase.

The steep slope of the recent yield surge has turned an interest rate move into a balance sheet event. Japan can gradually digest higher yields, but it struggles to cope calmly with a rapid duration repricing occurring abruptly within a financial system explicitly designed around yield suppression.

When yields shoot up vertically, the market is not just finding a new equilibrium; it is stress-testing all participants betting on the 'unchanged Japan model.'

Japanese banking institutions are structurally long duration and deeply hold JGBs as assets and collateral. This makes rapid yield increases inherently destabilizing, not merely restrictive. As yields spike sharply, bond portfolio market values shrink, collateral quality deteriorates, and financing conditions tighten within a system explicitly designed for yield suppression.

This is why the Bank of Japan has historically intervened when stress manifests in the data, not after the market has normalized. The BOJ doesn't need to wait for yields to hit an absolute threshold; accelerating moves of multiple standard deviations are often enough to trigger action.

Therefore, yield normalization in Japan is not a simple market adjustment but a balance sheet变动 that poses tangible transmission risks to the banking system, especially if market volatility is disorderly or one-way.

The current trajectory of Japan's 10-year government bonds significantly increases the motivation for the Bank of Japan to intervene. Such intervention does not necessarily require explicitly reinstating hard Yield Curve Control. Verbal guidance, targeted yield-smoothing operations, or more moderate control over the long-term bond market might be sufficient to slow the volatility in the yield curve and stabilize market conditions.

The Impact of BOJ Intervention on Gold

If the BOJ conducts credible intervention and regains control over long-end yields, this specific stress signal should weaken. This does not mean gold suddenly turns bearish, but it would likely remove a key catalyst for the current rally.

Combined with the analysis in the author's article 'Commodities Lead, Bitcoin Follows' published last week at Delphi Digital, the gold chart hints at this dynamic.

Although the overall uptrend remains intact, the upward momentum is no longer expanding at the same rate. The recent rally pushed the price to the upper edge of the rising channel but lacked the momentum confirmation seen in the early stages of the rise. Even as prices gradually move higher, the RSI indicator struggles to break previous highs, suggesting marginal buyers are becoming more cautious.

This aligns with a market that is structurally bullish but increasingly relies on policy stress rather than broad participation. Gold benefits from the vertical rise in Japan's 10-year yield, but this benefit manifests more in price persistence than acceleration. When the main catalyst is expected to be resolved, price action often shifts from impulsive to digestive.

Decisive intervention by the BOJ would likely break the link between gold and Japanese yields, reduce the pricing of policy stress, and perfectly match the signals already emitted by the chart——the market is forming a local top or entering a consolidation phase, not a trend reversal. Such an outcome would allow gold to work off excess momentum through time rather than price, cooling the pace of advance while preserving the larger trend.

Structurally, gold's support does not rely on Japanese stress, but marginally it clearly benefits from it. If that pressure is contained, the chart shows the market is prepared to pause the commodity trade.

The Impact of BOJ Intervention on Bitcoin

Given that Bitcoin's movement is inversely related to Japanese yields and gold, this relationship should also manifest when the BOJ finally decides to step in.

The chart already hints at this asymmetry: even as gold and Japanese yields continued to climb, Bitcoin, while weak, showed signs of stabilization rather than accelerated decline. This pattern fits an asset finding a bottom under macro pressure, remaining highly sensitive to any credible suppression measures.

If BOJ intervention materializes, Bitcoin's reaction is likely to differ from gold's. With global liquidity conditions stabilizing and the tightening shock from Japanese long-end yields easing, Bitcoin could experience a recovery rather than a pullback. In this sense, Bitcoin is not competing with gold in this mode; it's more like 'digital gold' waiting for the stress signal to be lifted.

Conclusion

The key insight is not that gold has peaked or that Japanese intervention is imminent, but that the market has already begun to treat Japanese yields as a global stress signal, and asset price behavior is adjusting accordingly.

Gold is absorbing this stress, while Bitcoin is reacting to it. The divergence between the two is revealing. As long as Japan's 10-year yield continues to rise unimpeded, gold's strength is logical. If the BOJ intervenes and regains control, the stress premium in gold should ease, and price action may shift from accelerating gains to choppy consolidation.

Regardless, the Japanese government bond market currently serves as the clearest window into how the market is pricing policy risk and balance sheet fragility. Until Japan's 10-year yield shows signs of softening, gold may continue its upward march, while Bitcoin's price performance may remain weak.