Original | Odaily Planet Daily (@OdailyChina)

Author | Mandy (@mandywangETH), Azuma (@azuma_eth)

This weekend, amid internal and external troubles, the crypto market was once again bloodied. BTC is currently hovering around the Strategy's cost basis of $76,000, while altcoins are so dismal that one might want to poke their own eyes out just looking at the prices.

Behind the current bleak scene, after recent conversations with projects, funds, and exchanges, a question keeps recurring in my mind: A year from now, what exactly will the crypto market be trading?

And the more fundamental question behind it is: If the primary market stops producing "the secondary market of the future," what will the secondary market be trading a year from now? What changes will happen to exchanges?

Although the death of altcoins has long been a cliché, the market hasn't been short of projects over the past year. Projects are still lining up for TGE every day. As media, we are still frequently coordinating market promotions with project teams.

(Note: In this context, when we say "projects," we mostly refer narrowly to "project teams"—simply put, those benchmarking against Ethereum and the Ethereum ecosystem—underlying infrastructure and various decentralized applications, and specifically "token-issuing projects." This is the cornerstone of so-called native innovation and entrepreneurship in our industry. So let's temporarily set aside Memes and platforms emerging from traditional industries venturing into crypto.)

If we pull the timeline back a bit, we'll find a fact we've all been avoiding: These projects about to TGE are all 'legacy projects,' most of which raised funds 1–3 years ago and are only now finally reaching token generation, or even being forced to issue tokens due to internal and external pressures.

This seems like a kind of "industry destocking," or, to put it more harshly, queuing up to complete their lifecycle: issue the token, give the team and investors an交代 (explanation/account), then lie down and await death, or spend the money on the books hoping for a miraculous turnaround.

The Primary Market is Dead

For "old-timers" like us who entered the industry during the ICO era or even earlier, have experienced several bull and bear cycles, and witnessed industry红利 (dividends) empowering countless individuals, there's a subconscious belief: Given enough time, new cycles, new projects, new narratives, and new TGEs will always emerge.

However, the reality is that we are far from our comfort zone.

Let's look at the data directly. Over the recent four-year cycle (2022 -2025), excluding special primary market activities like M&A, IPO, and public fundraising, the number of fundraising deals in the crypto industry has shown a clear downward trend (1639 ➡️ 1071 ➡️1050➡️829).

The reality is uglier than the data suggests. The change in the primary market is not just an overall shrinkage in amount but a structural collapse.

Over the past four years, the number of early-stage rounds (including pre-seed and seed rounds), representing the industry's fresh blood, (825 ➡️ 298 over four years, a 63.9% drop) has shown a greater decline than the overall figure (49.4% drop). The primary market's ability to supply blood to the industry has been shrinking.

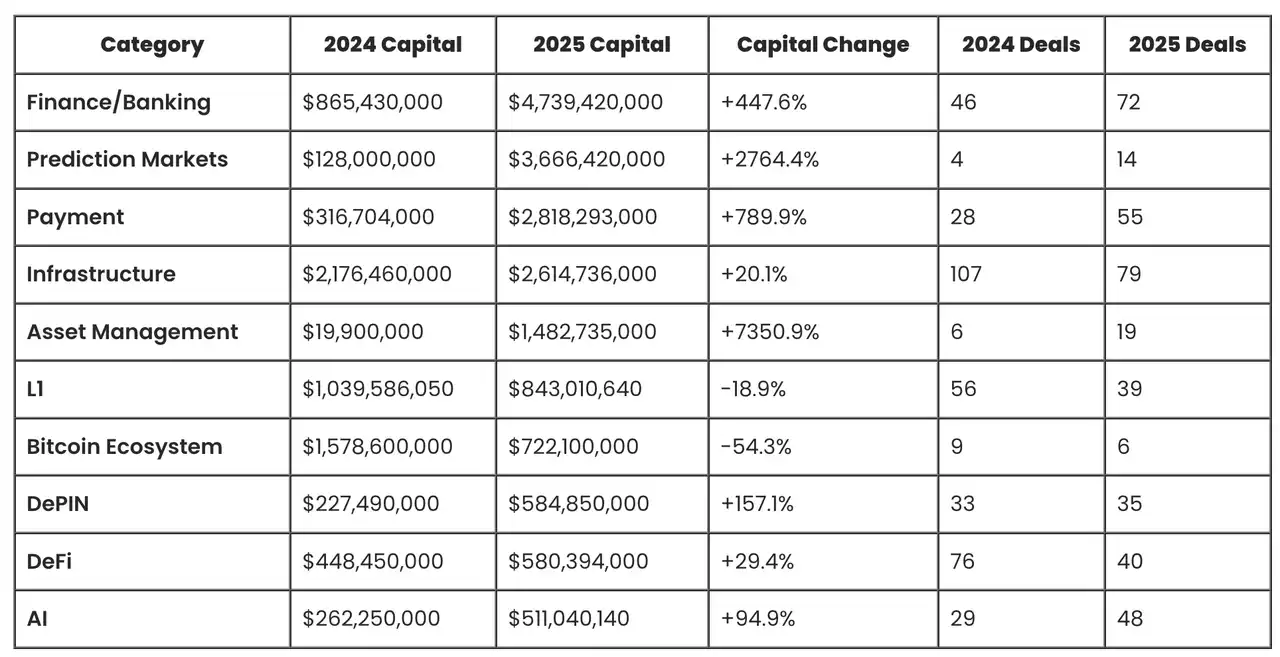

The few sectors showing an upward trend in deal count are financial services, exchanges, asset management, payments, AI, etc., which apply crypto technology, but have limited actual relevance to us—frankly, most won't "issue tokens." In contrast, native "projects" like L1, L2, DeFi, and social have seen a more significant decline in fundraising.

Odaily Note: Chart sourced from Crypto Fundraising

A easily misinterpreted data point is that while the number of fundraising deals has drastically reduced, the average amount per deal has risen. The main reason is that the "big projects" mentioned earlier have secured large amounts of capital from traditional finance, significantly pulling up the average. Additionally, mainstream VCs tend to double down on betting on a few "super projects," such as Polymarket's multiple hundred-million-dollar funding rounds.

From the crypto capital side, this top-heavy vicious cycle is even more pronounced.

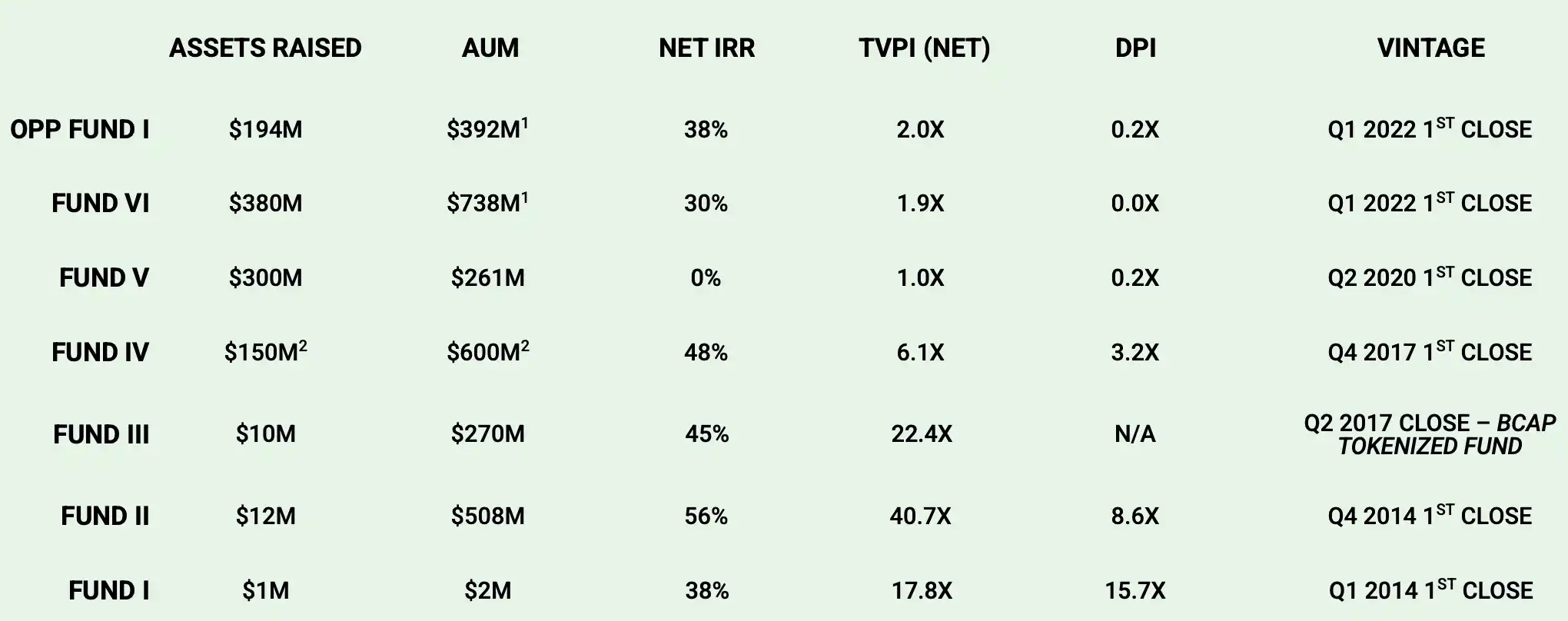

Not long ago, an outsider friend asked me about a well-known, super-old crypto fund currently raising capital. He was puzzled after seeing the Deck and asked me why their returns were "so poor." The table below shows the actual data from the Deck. I won't name the fund, just excerpted its fund performance data from 2014-2022.

It's clear to see that between 2017–2022, this fund's IRR and DPI changed significantly at the fund level—the former represents the fund's annualized return level, more reflecting "paper profitability," while the latter represents the multiple of cash returns actually returned to LPs.

Looking at different vintages (years), this set of fund returns shows a very clear "cycle断层 (fault/disconnect)": Funds established between 2014–2017 (Fund I, Fund II, Fund III, Fund IV) significantly outperformed, with TVPI generally in the 6x–40x range, Net IRR maintained at 38%–56%, and also already having a high DPI, indicating these funds not only had high paper gains but also completed large-scale realization, eating the era红利 (dividends) of early crypto infrastructure and top protocols going from 0 to 1.

Funds established after 2020 (Fund V, Fund VI, and the 2022 Opportunity Fund) clearly dropped a grade, with TVPI basically concentrated in the 1.0x–2.0x range, DPI close to zero or very low, meaning most returns are still on paper and cannot be converted into real exit proceeds. This reflects that against the backdrop of valuation inflation, intensified competition, and declining project supply quality, the primary market cannot replicate the excess return structure driven by "new narratives + new asset supply."

The real story behind the data is that after the DeFi Summer hype in 2019, valuations for crypto-native protocols in the primary market became inflated. When these projects finally issued tokens 2 years later, they faced weak narratives, industry tightening, exchanges controlling their fate and临时 (temporarily) changing terms, etc.,普遍 (generally) performing poorly, even with市值倒挂 (market cap inversion), leaving investors as the disadvantaged group and making fund exits difficult.

But these周期错配 (cycle-mismatched) funds can still create a false appearance of prosperity locally within the industry, until the惨烈 (bleak) real data was直观地 (visibly) seen during fundraising by some massive star funds in the past 2 years.

The fund I used as an example currently has AUM of nearly $3 billion, which further indicates it's a mirror to observe the industry cycle—doing well or not is no longer a question of individual project selection, the general trend is gone.

And while old牌 (veteran) funds nowadays find fundraising difficult, they can still survive, lie flat, eat management fees, or transition to investing in AI. More funds have already shut down or turned to secondary markets.

For example, the current "Ethereum Bull King" in the Chinese market, Boss Yi Lihua—who remembers that not long ago he was a representative figure in primary, investing in over a hundred projects annually?

The Substitute for Altcoins Was Never Meme

When we say crypto-native projects are drying up, a counterexample is the explosion of Memes.

Over the past two years, a说法 (saying) repeatedly mentioned in the industry is: The substitute for altcoins is Meme.

But looking back now, this conclusion has actually been proven wrong.

In the early days of the Meme wave, we played Meme the way we played "mainstream altcoins"—screening a large number of Meme projects for so-called fundamentals, community quality, narrative rationality, trying to find the one that could survive long-term, constantly refresh itself, and eventually grow into Doge, or even the "next Bitcoin."

But today, if someone still tells you to "hold Meme," you'd definitely think they've lost their mind.

Current Meme is a mechanism for the instant monetization of热度 (heat/attention): a game of attention vs. liquidity, a product批量 (mass-produced) manufactured by Devs and AI tools,

an asset form with an extremely short lifecycle but a continuous supply.

It no longer aims to "survive," but aims to be seen, traded, and utilized.

There are also several consistently profitable Meme traders in our team. Clearly, they focus not on the project's future, but on rhythm, spread speed, sentiment structure, and liquidity paths.

Some say Meme is unplayable now, but in my view, after Trump's "final pump," it恰恰 (precisely) allowed Meme, as a new asset form, to truly mature.

Meme was never a substitute for "long-term assets"; it returns to attention finance and liquidity博弈 (game theory) itself. It has become purer, crueler, and also less suitable for most ordinary traders.

Seeking Solutions Outward

Asset Tokenization

So when Meme becomes professionalized, Bitcoin becomes institutionalized, altcoins萎靡 (wither), new projects are about to断层 (break/run out), what can we ordinary folks who like value research, comparative analysis, judgment, have speculative attributes, but aren't purely high-frequency probability gamblers, and want sustainable development, actually play?

This question doesn't just belong to retail.

It also lies before exchanges, market makers, and platforms—after all, the market cannot forever rely on higher leverage and more aggressive contract products to maintain activity.

In fact, when this entire固有 (inherent) logic begins to collapse, the industry has long started seeking solutions向外 (outward).

The direction we are discussing is repackaging traditional financial assets as on-chain tradable assets.

Stock tokenization and precious metal assets are becoming the top priority for exchange布局 (layout/planning). From a host of centralized exchanges to the decentralized platform Hyperliquid, this path is already seen as the key to breaking the deadlock, and the market has given positive feedback—during the most疯狂 (crazy) days for precious metals last week, Hyperliquid's daily silver trading volume once exceeded $1 billion, with tokenized stocks, indices, precious metals, and other assets once occupying half of the top ten trading volume spots, pushing HYPE up 50% short-term under the narrative of "full-asset trading."

Admittedly, some current slogans, such as "providing new choices and low thresholds for traditional investors," are still premature and unrealistic.

But from a crypto-native perspective, it might solve internal problems: After the supply and narratives of native assets slow down, old coins萎靡 (wither), and new coins断供 (supply cut off), what new trading rationale can crypto exchanges still provide to the market?

Tokenized assets are easy for us to pick up. In the past, we researched: public chain ecosystems, protocol revenue, token models, unlock schedules, and narrative space.

Now, the research objects are starting to become: macroeconomic data, financial reports, interest rate expectations, industry cycles, and policy variables. Of course, we've already been researching many of these parts.

In essence, this is a migration of speculative logic, not simply a category expansion.

Listing gold tokens and silver tokens isn't just about adding a few more币种 (coin types); what they are truly trying to introduce are new trading narratives—bringing the volatility and rhythm originally belonging to traditional financial markets into the internal crypto trading system.

Prediction Markets

Besides bringing "external assets" on-chain, another direction is bringing "external uncertainty" on-chain—prediction markets.

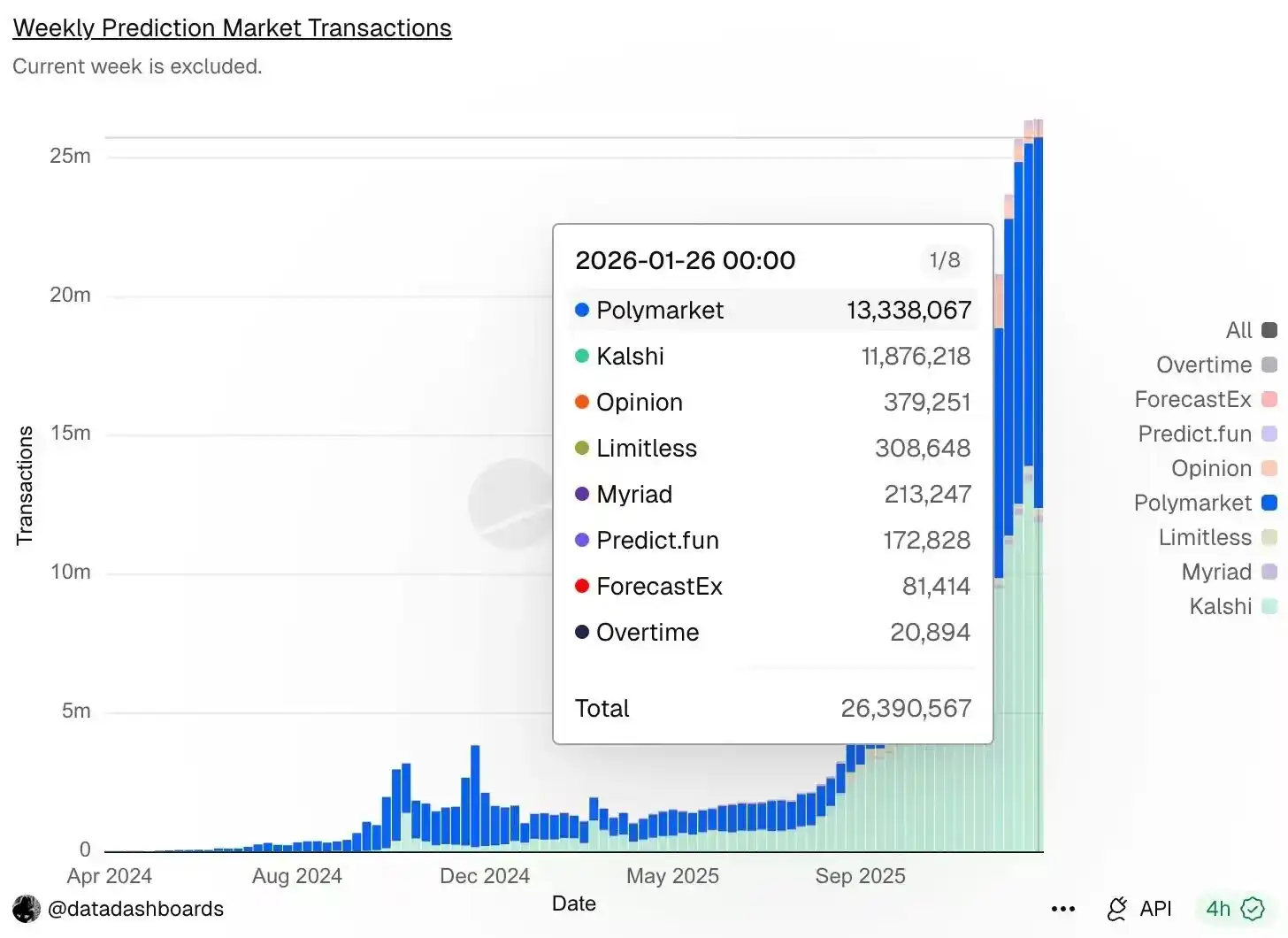

According to Dune data, although the crypto market crashed last weekend, prediction market trading activity反而 (instead) increased, hitting a new historical high of 26.39 million weekly transactions. Leading platform Polymarket had 13.34 million transactions, followed closely by Kalshi with 11.88 million.

We won't elaborate on the development prospects and scale expectations of prediction markets here, as Odaily最近 (recently) writes over 2 analysis articles on prediction markets daily...... You can search for them yourself.

I want to talk from the perspective of币圈 (coin circle) users: Why do we play prediction markets? Is it because we are all degenerate gamblers?

Of course.

Actually, for a long time, altcoin traders weren't essentially betting on technology, but on events: Will it get listed? Is there a partnership announcement? Is it about to issue a token? Is it launching a new feature? Is there a regulatory benefit? Can it ride the next narrative wave?

Price is just the result; the event is the starting point.

Prediction markets, for the first time,拆 (disassembled) this from an "implied variable in the price curve" into an object that can be directly traded.

You no longer need to buy a token to indirectly bet on whether a certain outcome will happen; you can directly bet on "whether it will happen" itself.

More importantly, prediction markets fit the current environment of "new project supply cut-off and narrative scarcity."

When new tradable assets become fewer, market attention反而 (instead) concentrates more on macro, regulation, politics, big player behavior, and major industry nodes.

In other words, the tradable "assets" are decreasing, but the tradable "events" are not decreasing, even becoming more.

This is also why the liquidity that prediction markets have truly gained in recent years almost entirely comes from non-crypto-native events.

It essentially introduces the uncertainty of the external world into the internal crypto trading system. From a trading experience perspective, it's also more friendly to original coin circle traders:

The core question is极度简化 (extremely simplified) to one—Will this outcome happen? And, Is this current probability expensive?

Unlike Meme, the门槛 (barrier) for prediction markets isn't execution speed, but information judgment and structural understanding.

Hearing this, doesn't it feel like maybe I can try this too.

Conclusion

Perhaps the so-called币圈 (coin circle) will eventually die out in the not-too-distant future, but before dying out, we are still折腾 (hustling/trying hard). After "new-coin-driven trading" gradually exits, the market will always need a new, low-participation-threshold, narratively传播性 (spreadable/viral), sustainable speculative载体 (vehicle).

Or rather, the market won't disappear; it will only migrate. When the primary market no longer produces the future, what the secondary market can truly trade are these two things—the uncertainty of the external world, and tradable narratives that can be repeatedly重构 (reconstructed).

What we can do is perhaps adapt提前 (in advance) to yet another migration of the speculative paradigm.