Author: Curry, Deep Tide TechFlow

The person who built this little fox doesn't want to build anymore.

On April 23, MetaMask co-founder Dan Finlay officially announced his departure from Consensys, ending a decade-long development career. The reason given was professional burnout and a desire to spend more time with family.

MetaMask is perhaps the most recognizable product application in the crypto world. That little orange fox logo is known to almost everyone who has ever installed a crypto wallet. In 2016, Finlay and another co-founder, Aaron Davis, created this browser plugin within Consensys, allowing ordinary people to interact with Ethereum without running a full node.

Over the past ten years, according to statistics from multiple third-party platforms, it has achieved over 100 million global installs, with approximately 30 million monthly active users. Its swap function has cumulatively generated over $325 million in fee revenue.

A look at public information reveals that Finlay has hardly given any interviews in the past decade. Previously a coder at Apple, he is fundamentally an engineer at heart, not someone who builds a public persona.

When such a person says they are tired, they usually mean it. It's just that the timing of his departure is hard not to overthink.

Just a few months ago, Consensys hired J.P. Morgan and Goldman Sachs as IPO advisors, with a target to go public as soon as this year, according to an Axios report.

The company's last funding round was in 2022, when it was valued at $7 billion. It has since undergone at least two rounds of layoffs. And the $MASK token, promised since 2021, still hasn't materialized after five years.

Issuing a token doesn't seem that necessary for a wallet. More frighteningly, it seems like the little fox isn't that necessary for everyone either.

The Default, But Not the Preferred Choice

In the past, the first step in many dApp development documents was "Please install MetaMask first." It was the default wallet for the industry, like the blue IE browser on your Windows desktop ten years ago.

The problem is, the default and the preferred choice have long ceased to be the same thing.

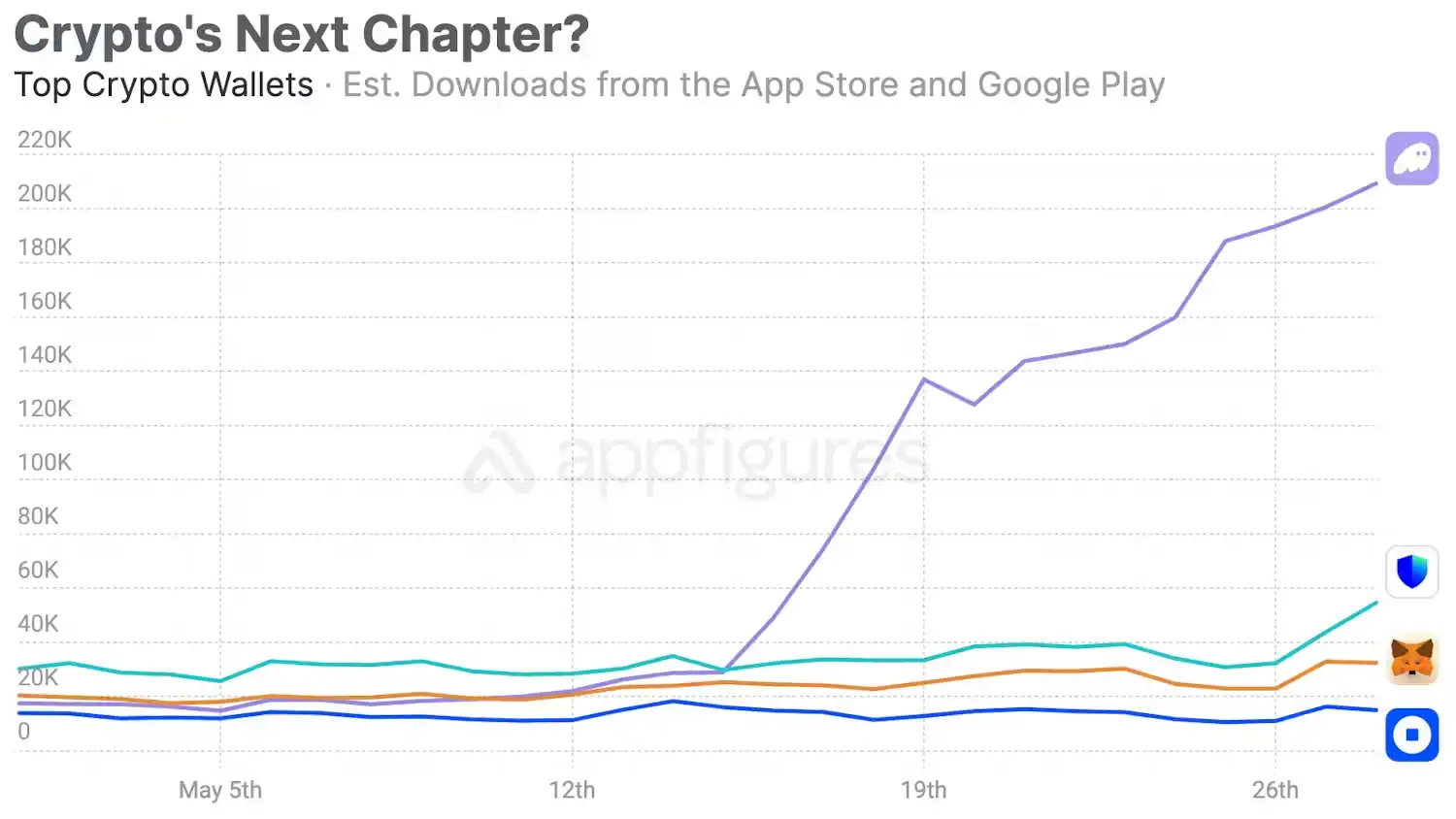

Phantom started out only as a Solana wallet, later expanding to Ethereum and Bitcoin. In January 2025, it raised a $150 million Series C, valuing the company at $3 billion.

According to estimates by whales.market based on on-chain data, Phantom's annualized revenue is approximately $108 million;相比之下 MetaMask's is about $46 million. More than double the difference, and Phantom is five years younger than MetaMask.

Phantom started on Solana in 2021, catching the entire process of the Solana ecosystem's recovery and explosion. According to Helius statistics, Solana's DEX trading volume surpassed Ethereum's in 2024, and on-chain application revenue reached $2.39 billion in 2025, a 46% year-on-year increase. 725 million new wallets conducted their first Solana transaction in 2025. Phantom was waiting at the door when these users came in.

And MetaMask? It only launched native Solana support in May 2025. Before that, users who wanted to access Solana through MetaMask had to install a third-party plugin called Snaps, an experience akin to installing a Chrome kernel on the IE browser...

In these five years, Solana went from a chain that nearly died due to the FTX crash to, at one point, the chain with the largest trading volume. Phantom's valuation rose accordingly, securing a $150 million Series C funding round in early 2025 with a $3 billion valuation.

The author believes MetaMask's slowness wasn't due to technical inability, but also an issue of identity. MetaMask is Ethereum's favored child; its parent company Consensys was founded by Ethereum co-founder Joe Lubin.

Supporting Solana was an expansion for Phantom, but a betrayal for MetaMask. By the time the Ethereum ecosystem's growth indeed slowed down and cross-chain became necessary, the window of opportunity had long passed.

Of course, MetaMask's compatibility within the Ethereum ecosystem is still the strongest. Almost all dApps on EVM chains test it as the default option. The 30 million monthly active users are real.

But this stickiness doesn't come from product strength; it comes from switching costs. And switching costs can only prevent old users from leaving, not stop new users from going elsewhere.

A person who started playing on-chain in 2025 is probably not being recommended MetaMask by their friends when they go to install a wallet.

The Little Fox Up for Sale

The product is falling behind, people are leaving, but Consensys is pursuing an IPO.

According to an Axios report in October 2025, Consensys hired J.P. Morgan and Goldman Sachs as IPO advisors, targeting a public listing as soon as this year. If successful, this would be the first company deeply tied to Ethereum core infrastructure to list on the US stock market.

But in the same year it hired the investment banks, Consensys underwent at least two rounds of layoffs.

In October 2024, it cut 20% of its staff, about 160 people, with CEO Joe Lubin citing macroeconomic pressures and regulatory uncertainty. Another round occurred mid-2025, this time justified as "driving profitability."

On the well-known job review community Glassdoor, employee reviews are uglier than the layoffs themselves.

Someone wrote that the company lays off people at least twice a year, always cutting frontline contributors, never management. Another said that after sharing their promotion aspirations with their superior, their name appeared on the next layoff list.

It's unclear how much of these reviews are emotion and how much is fact. But a company conducting significant layoffs while employee morale hits rock bottom, all while sprinting towards an IPO, is itself a signal.

Then there's the story of the MASK token.

In 2021, Lubin tweeted "Wen $MASK?", causing a stir in the community. In 2022, he further explained plans for a token and DAO to promote "progressive decentralization." In May 2025, Finlay was interviewed by The Block and asked when the token would come; his answer became maybe.

For users, the MASK token is a carrot, dangled to keep using, interacting, and contributing on-chain data to MetaMask. For Consensys, the token is a card not yet played before the IPO.

Issuing it too early dilutes the valuation narrative; issuing it too late loses community support. Now the co-founder has left, the token hasn't been issued, but the IPO is coming.

MetaMask's product competitiveness is declining, a trend difficult to reverse in the short term. But MetaMask's brand recognition remains; that little orange fox is still the world's most recognizable crypto logo.

Brand value and product value decay at different rates; brand decays slower.

For crypto companies, an IPO often sells not the product, but the brand plus the narrative. "Ethereum infrastructure," "Web3 gateway," "World's largest self-custody wallet"... These labels still work well on pitch decks, even years later. Lubin himself is an Ethereum co-founder, an identity that carries its own halo effect in front of traditional investors.

So Consensys's choice is to package MetaMask into a public company shell while the brand is still valuable, while the regulatory window is still open, while Wall Street still has enthusiasm for crypto infrastructure, and let the public market set the price.

Silence is Not Golden

The reaction to co-founder Finlay's departure was muted in Crypto Twitter (CT). No long farewell posts went viral, no laments about "the end of an era," most people didn't even care about the news.

The comings and goings of Metamask's co-founder generated less buzz than some KOL complaining about shrunken conference swag in Hong Kong.

This in itself says something.

MetaMask is a rare case in the crypto industry. It possesses one of the industry's largest brands, but its founders have almost no personal brand.

In an industry where the founder is often the biggest marketing resource, MetaMask's two founders chose to remain invisible. The product spoke for them, until the product could no longer speak effectively.

The author believes MetaMask's story is essentially one about being the "default."

In the technology industry, becoming the default option is the most powerful competitive advantage, and the most dangerous sedative. When you are the default, user growth happens without you to do anything.

But this growth masks the fact that the product itself is aging. By the time you notice users leaving, the exodus has often been ongoing for a long time.

IE was the default browser, lost to Chrome. Nokia was the default phone, lost to iPhone.

Windows Media Player was the default media player, lost to everyone. These products lost while their market share was still high, brand recognition still strong, but new users were no longer choosing them.

MetaMask is now in this position. The existing user base remains, the brand is still loud, but the growth has gone elsewhere. Consensys's IPO plan is, ultimately, about monetizing the existing user base.

When brand value exceeds product value, selling is indeed the rational choice.

On the day Finlay left, MetaMask just launched a new feature called ERC-7715 for advanced permissions. He said he looked forward to experiencing it as a regular user in the future.

A product's creator becoming its ordinary user is probably the most朴实 (simple/unadorned) and quietest farewell in the crypto industry.

But for MetaMask, how many ordinary users will still click on that little fox every day next year? Are you still using it?