Original Title: AI: PayPal』s $200M Wake-Up Call in AI Commerce

Original Author: LUKE SPILL,FintechBlueprint

Compiled by: Peggy,BlockBeats

Editor's Note: As AI agents begin to replace humans in product discovery, decision-making, and order placement, the traditional e-commerce funnel is being rapidly compressed. Payment is no longer the endpoint of a transaction but an embedded part of the infrastructure. This article uses PayPal's acquisition of Cymbio as a starting point to outline the new competitive landscape emerging with the rise of Agentic Commerce: Google and Shopify are attempting to control the routing layer with UCP, OpenAI and Stripe are seizing the agent execution layer with ACP, while PayPal is striving to shift from being a "payment button" to a key node in the "commercial workflow."

For fintech companies like PayPal and Stripe, whether they can embed themselves into the underlying protocols of AI commerce will determine if they can remain at the table. For the banking and crypto industries, the window of opportunity is equally brief.

Below is the original text:

Last week, PayPal acquired Cymbio, a platform that helps merchants complete sales on various AI interfaces, including channels like Microsoft Copilot and Perplexity. Market sources estimate the deal to be worth between $150 million and $200 million. It is widely seen as a key strategic move by PayPal to maintain competitiveness in the field of Agentic Commerce.

Thus, as AI agents continue to compress and reshape the traditional e-commerce funnel, PayPal is transitioning from a typical Web2 payment tool to more upstream, core commercial segments such as product discovery, catalog distribution, and order orchestration. This shift almost entirely confirms the analysis we conducted in January of this year regarding exponential growth, power-law effects, and increasing returns to scale in Agentic Commerce.

Simultaneously, the industry's infrastructure is rapidly taking shape:

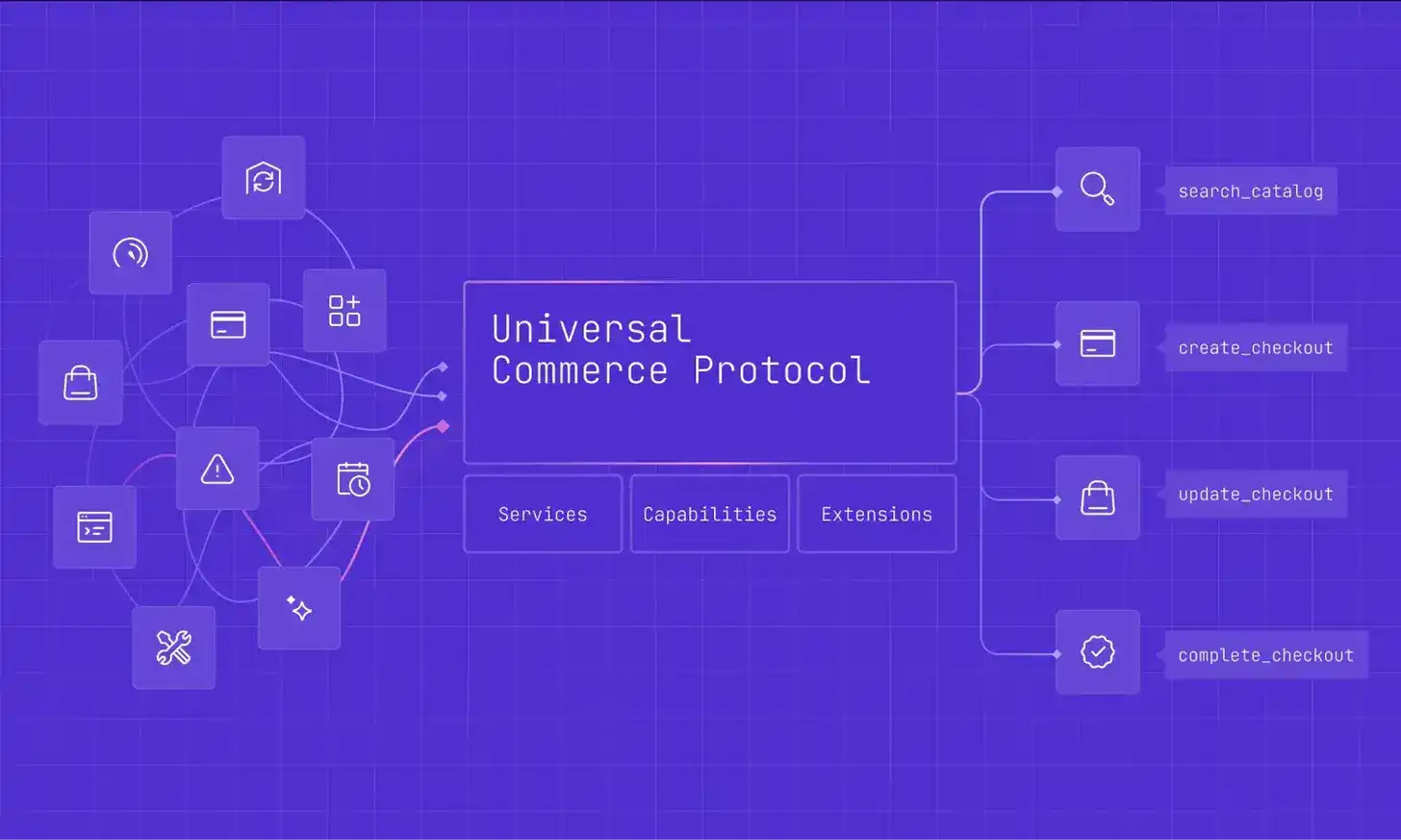

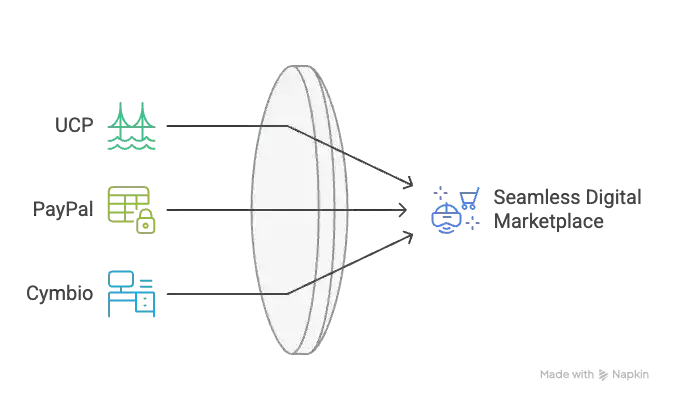

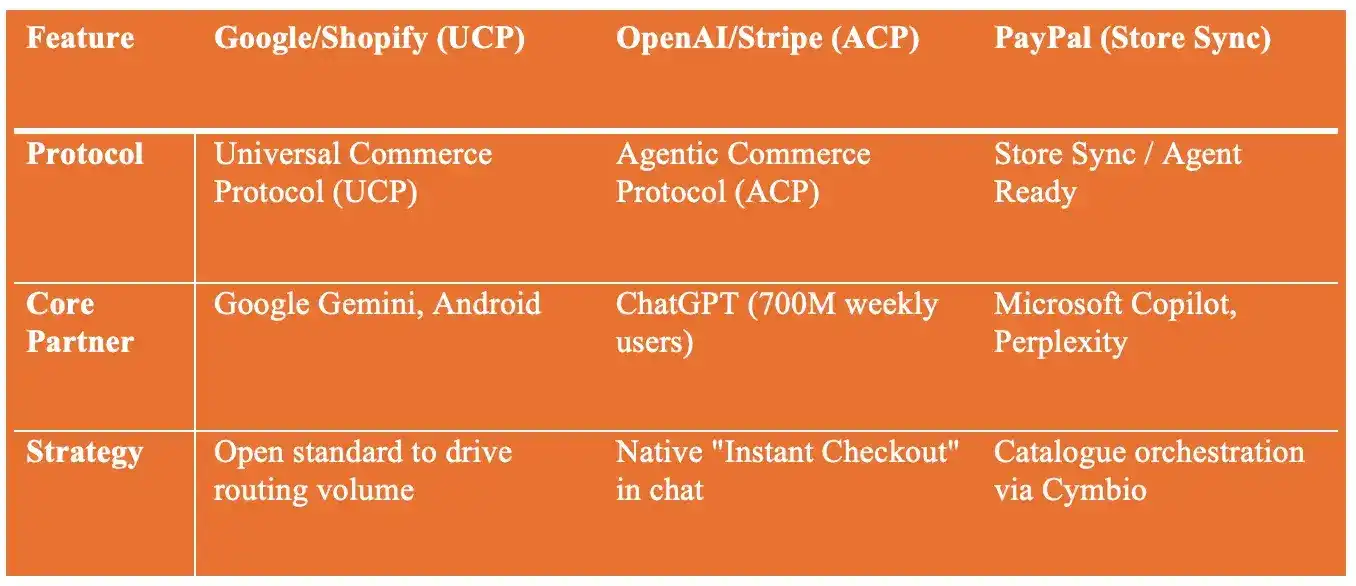

Google and Shopify are promoting the Universal Commerce Protocol (UCP);

OpenAI and Stripe are jointly advancing the Agentic Commerce Protocol (ACP);

Microsoft is embedding settlement capabilities directly into Copilot.

Shopping infrastructure built around "machines" rather than "human users" is being rewritten at an unprecedented speed. Agentic Commerce is fulfilling expectations of exponential growth in real-world ways. The predictions from various parties are both astonishing and converging:

McKinsey predicts: By the end of this decade, Agentic Commerce is expected to generate $1 trillion in revenue in the U.S. retail market, accounting for about one-third of all online retail sales.

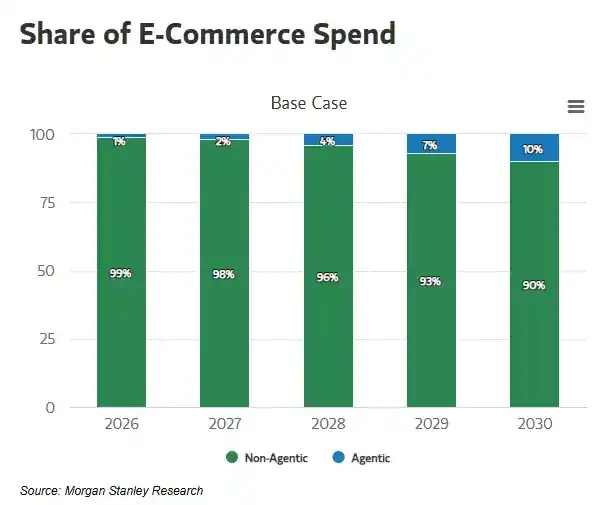

Morgan Stanley predicts: By 2030, Agentic Commerce will drive U.S. e-commerce spending to $190 billion to $385 billion, corresponding to a 10%–20% market penetration rate.

Bain predicts: By 2030, the market size of Agentic Commerce will reach $300 billion to $500 billion, accounting for 15%–25% of total online retail sales.

Current adoption data indicates we are at the inflection point of an exponential growth curve: As of November 2025, 23% of U.S. consumers had used AI to complete a purchase.

Cymbio could become PayPal's "Middle Layer" in AI Commerce

For PayPal, Cymbio's potential positioning is as an intermediate infrastructure layer within the AI commerce system. Its core value propositions include:

Synchronizing product catalogs across different markets and channels

Managing inventory availability in real-time

Routing orders to merchants' existing OMS (Order Management System) and fulfillment systems

Allowing merchants to continue acting as the legal Merchant of Record for transactions

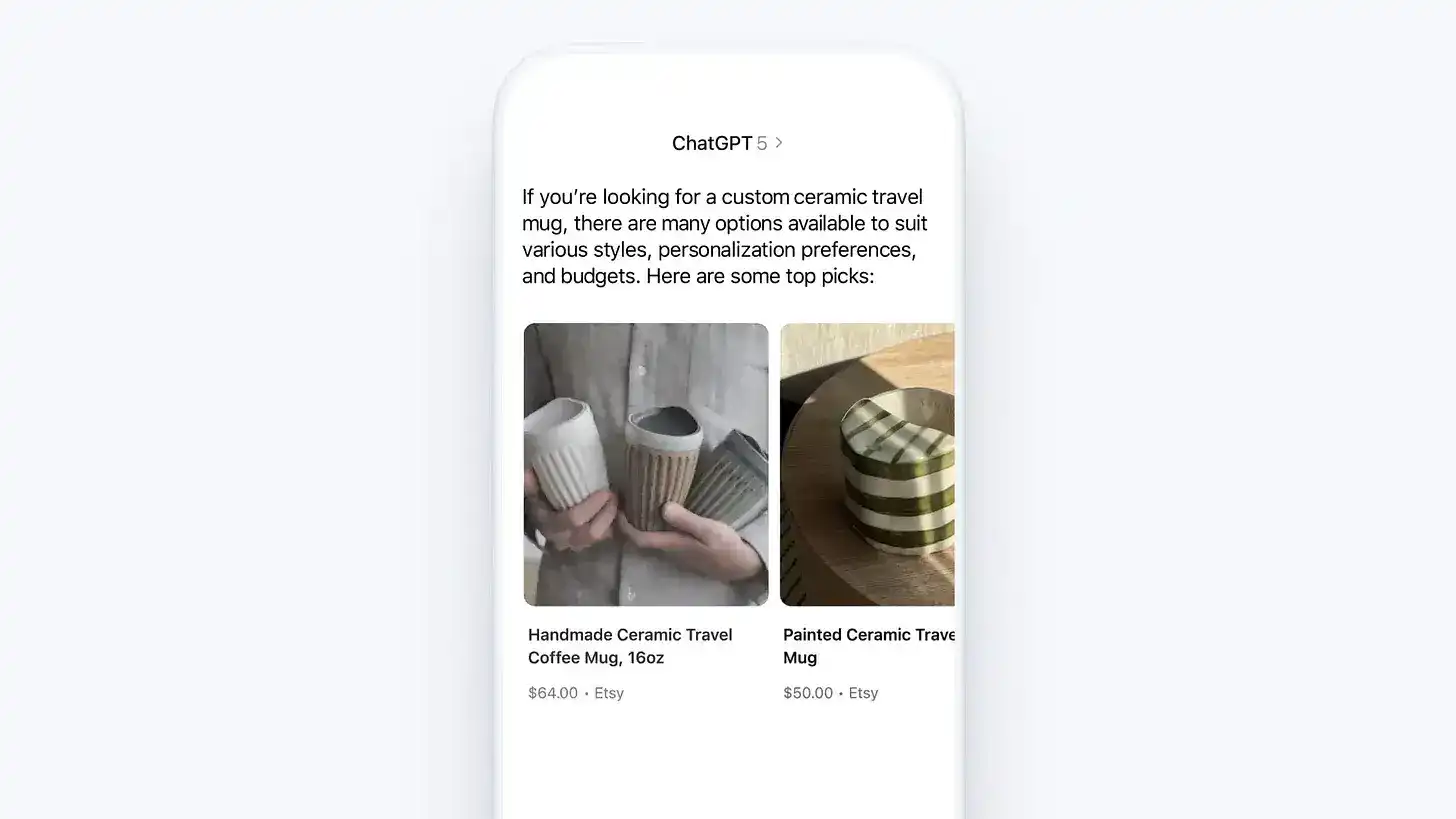

Among these, the Store Sync product enables merchants' product catalogs to be directly discovered by AI agents like Microsoft Copilot and Perplexity, with expectations to integrate with ChatGPT and Google Gemini next.

The prerequisite for AI agents to complete transactions is that product data, pricing, inventory, and fulfillment information must be machine-readable and highly reliable.

From "Checkout" to "Agentic Commerce Workflow"

PayPal processes over $1.7 trillion in total payment volume annually, with over 142 million monthly active accounts. In the traditional model, PayPal's core leverage point is the moment payment occurs.

In the Agentic Commerce system, AI systems can act on behalf of users to complete product discovery, comparison, and even place orders, while PayPal handles identity verification and payment authorization.

After integrating Cymbio, PayPal covers the complete chain:

Discovery: Products are recommended and presented within AI agents

Decisioning: Options are narrowed down through conversational interaction

Checkout: PayPal completes identity verification and payment

Fulfillment: Orders are directly injected into merchant systems for execution

Protocol Wars: Service vs Standard

While PayPal advances Agentic Commerce in the form of "products and services," Google and Shopify are building a cross-functional, standardized Agentic Commerce protocol system.

The key points are:

Google is embedding the UCP (Universal Commerce Protocol) directly into Search and Gemini

Shopify ensures its millions of merchants only need to integrate once to reach multiple AI agents

This means the underlying infrastructure of AI commerce is evolving from "point capabilities" to a "protocolized network."

The goal of UCP is to control the "routing layer" of AI commerce, rather than directly owning or operating the commerce itself.

This is more of a defensive layout: by making this layer a "free" public protocol and introducing strong network effects, it prevents any single competitor from monopolizing the core control of the AI commerce system.

Therefore, PayPal is not competing head-on with UCP but is actively embedding itself into this system.

Google has clearly stated that UCP-based checkout capabilities will support multiple payment service providers, including PayPal and Google Pay.

In other words, UCP aims to be a "neutral highway," while PayPal hopes to become an indispensable toll booth and payment node on this highway.

OpenAI and Stripe are the main competitors in this space.

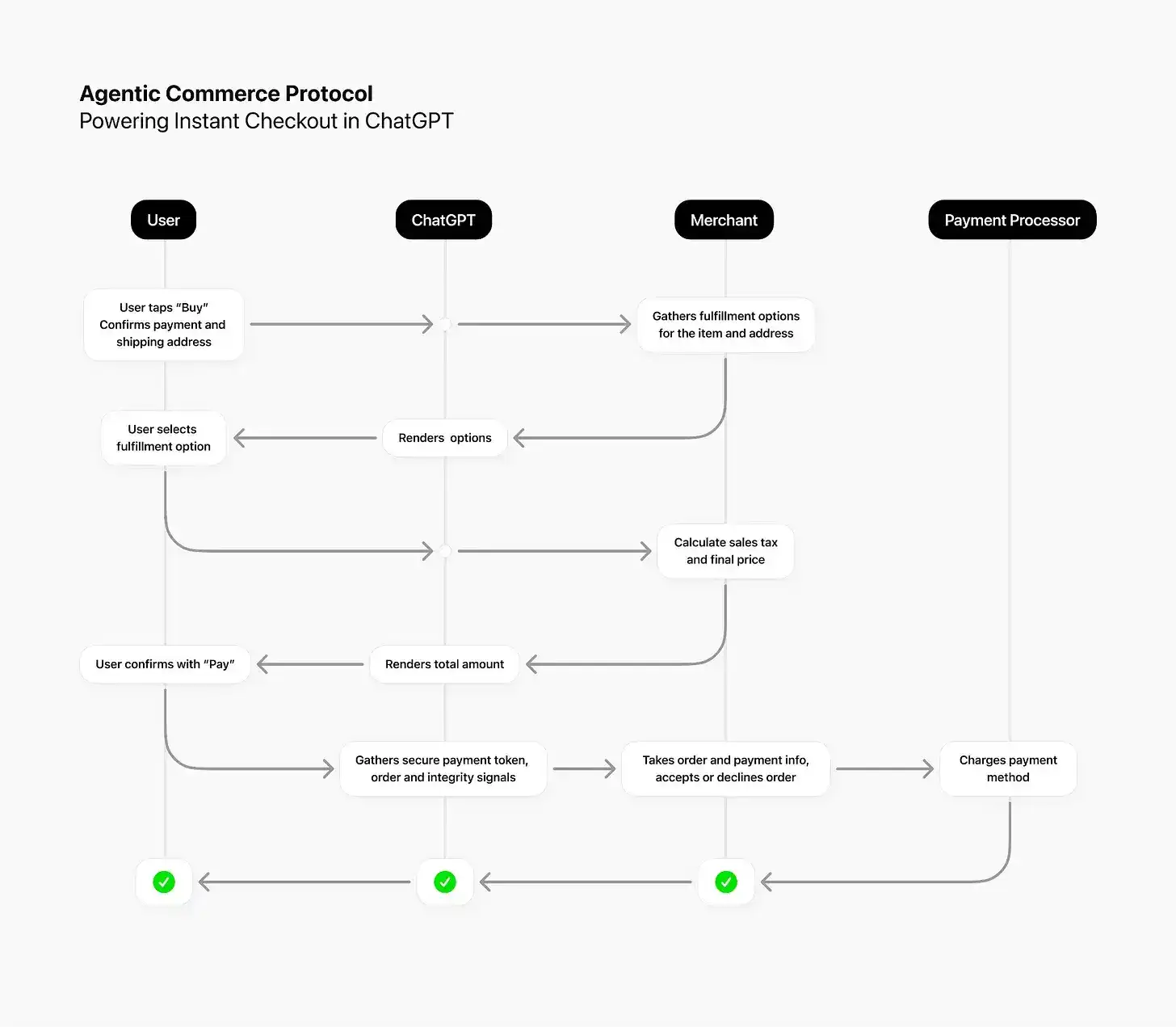

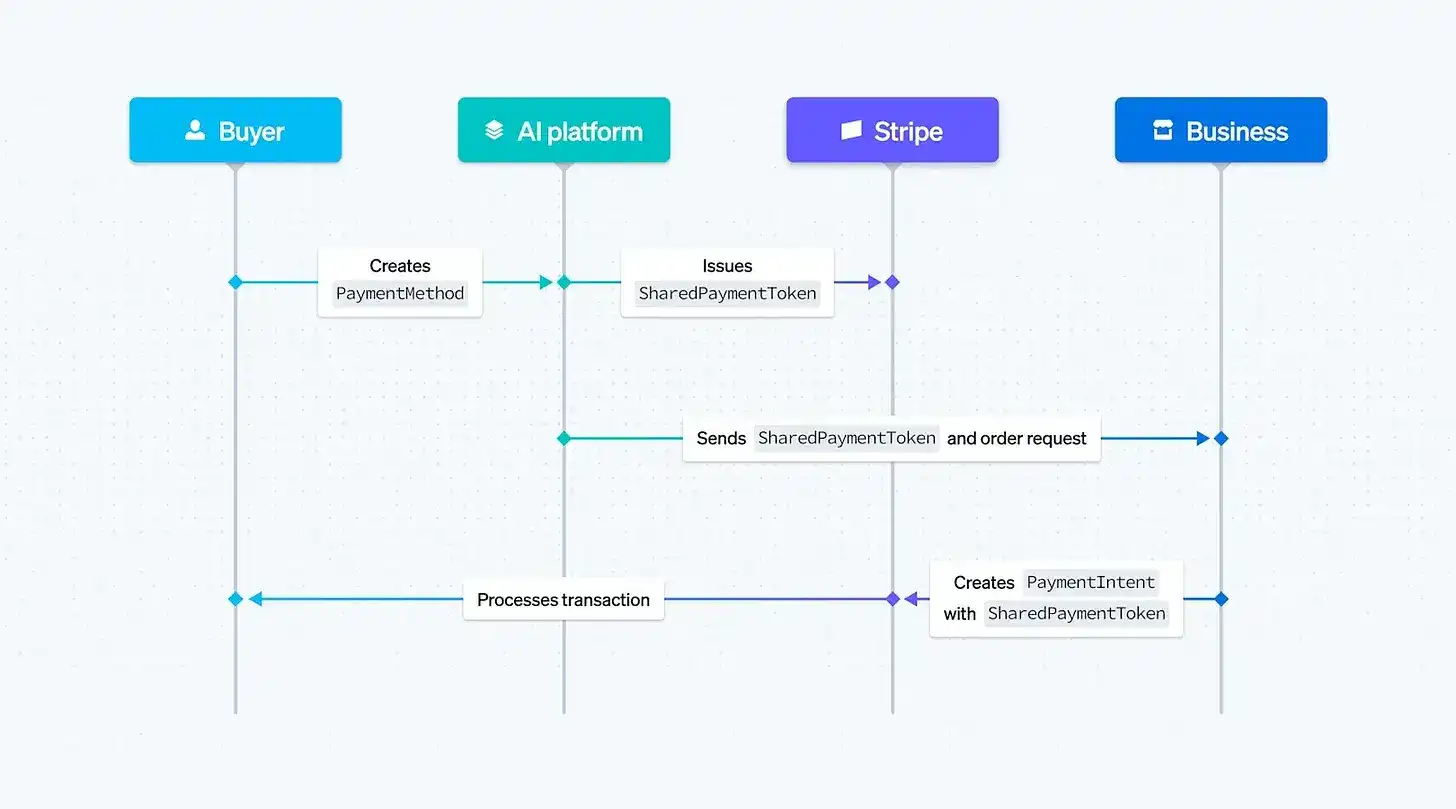

As early as September, Stripe and OpenAI announced the launch of Instant Checkout in ChatGPT, powered underlyingly by the Agentic Commerce Protocol (ACP).

ACP allows AI agents to proactively initiate purchase requests through structured APIs, with Stripe issuing shared payment tokens to confirm payments under agent authorization. This enables AI, once authorized, to complete the entire transaction process from order placement to payment on behalf of the user.

Stripe subsequently launched the Agentic Commerce Suite in December 2025, enabling merchants to:

Publish product catalogs for direct access by AI agents

Autonomously choose which AI agents to sell through

Handle payments, risk management, and dispute resolution through Stripe

Pass order events back to existing business systems

Stripe processed over $1 trillion in payment volume in 2024, serving millions of businesses globally. Its competitive strategy is clear: become the "default wallet" and "action execution layer" for AI agents—highly similar to its path to becoming the default payment API for internet companies.

In this context, PayPal and Stripe are clearly in direct confrontation:

They are competing not just for payment itself, but for the key control points when AI agents actually "execute transactions."

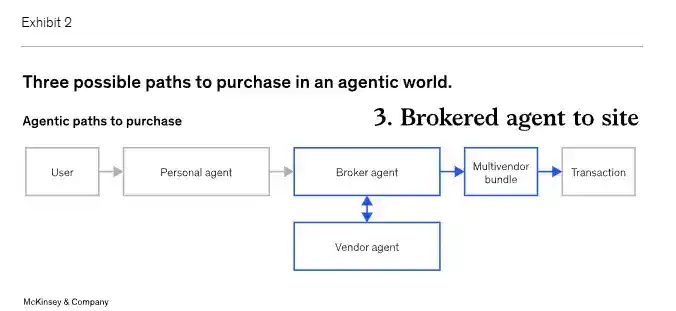

Comparing the three systems together

(This section would involve a横向 comparison of UCP / ACP / PayPal + Cymbio:

Who controls the routing layer, who controls the protocol, who controls payment and fulfillment execution—and the sources of their respective network effects.)

If you wish, I can directly help you organize the next part into a comparison table or a highly summarized "landscape assessment," clarifying the division of labor and博弈 among the three parties at once.

Key Takeaways

Three impacts are particularly prominent:

Commercial behavior will become conversational and executable by agents

Purchasing will no longer be a step-by-step process completed by users, but rather understood by AI through conversation and completed on their behalf under authorization.

Merchants will achieve "integrate once, distribute everywhere"

Merchants won't need to adapt for each platform individually; a single integration will allow their products to reach users through multiple AI agents and channels.

Payments will become embedded infrastructure, no longer the endpoint of transactions

Payment will no longer be a "final step button" but a deep-seated capability embedded within the discovery, decision-making, and fulfillment processes.

Payment Networks' Advance Preparation

Incidentally, Mastercard announced in January 2026 that it is researching "AI Commerce Rules," essentially attempting to抢先一步 participate in defining the governance framework for this transformation.

Payment networks clearly realize that the power to set rules and standards will determine future positioning before AI agents execute transactions on a large scale.

As we pointed out in our January analysis: banks, fintech companies, and the crypto industry must ensure they are "at the table," rather than being incorporated afterwards.

If financial institutions cannot embed themselves into these platforms提前, their financial functions may ultimately be internalized by Big Tech.

The Situation and Choices of Different Camps

For Banks

Traditional banks lack the technical infrastructure to compete head-on with Google, OpenAI, or Microsoft at the Agentic Commerce level. However, they still hold three key resources: payment clearing channels, customer credit relationships, and compliance and regulatory experience.

These assets mean banks won't disappear, but they must reposition themselves.

For Fintechs

Companies like PayPal, Stripe, and Adyen realized early on that merely handling payments is no longer sufficient to巩固 long-term positions.

Therefore, they are actively moving upstream into: commerce orchestration, merchant services, and the infrastructure layer of the AI era.

For Crypto

The Agentic Commerce protocol systems announced so far are almost entirely traditional financial paths: credit cards, Google Pay, PayPal, Stripe, etc., occupy core positions.

In UCP, ACP, and Store Sync, cryptocurrency and stablecoins are largely absent, aside from some零星 experiments involving Stripe or Coinbase.

Whether this is: a huge strategic oversight or an intentional exclusion remains to be seen.

For crypto companies, the window of opportunity is clear: if they can build payment rails natively suited for AI agents (instant settlement, programmable money, global reach) and successfully embed themselves into AI platforms before the protocols solidify completely, they might achieve a leapfrog overtaking of traditional finance; otherwise, they risk being permanently excluded from the system.

Conclusion

Fundamentally, PayPal is striving to catch up with Stripe and adapt to rapidly changing consumer behavior.

As people increasingly complete daily life decisions within AI platforms, these platforms will gradually evolve into the "default virtual storefronts" for brands.

Whoever can embed themselves into the infrastructure behind these storefronts will be able to remain at the table.

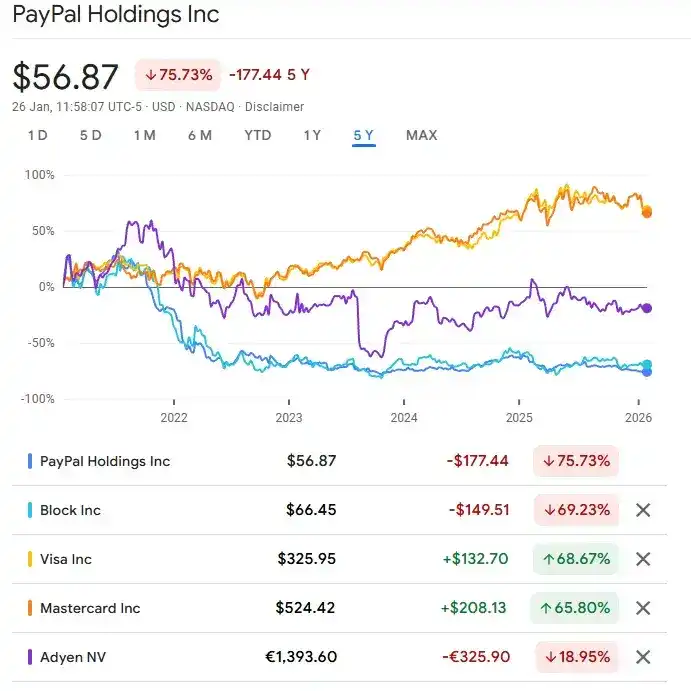

PayPal's stock price has been sluggish for a while, down about 37% from its 52-week high. Investors continually question whether the company maintains structural relevance in the long term, and the rise of the Crypto + AI narrative has反而加剧了 these concerns.

In this context, the diversification布局 around Agentic Commerce is not an offensive choice but a "necessary cost" to maintain relevance. For PayPal, this is not icing on the cake but an admission fee it不得不付出: only by completing this shift can it potentially remain in a core position within the next generation of commercial infrastructure.