When a real Token price war erupts, how will the AI industry make money? The entire valuation logic for AI commercialization is at a moment where it needs to be rewritten. The era of competing on "cost-effectiveness" and "scarcity" may have arrived. For OpenAI, "the situation is deteriorating further." Analysis points out that "if OpenAI goes into decline, it could very likely drag down Nvidia, Oracle, Coreweave, and others."

The commercialization narrative of generative AI is facing its most profound self-examination in three years. From exchanging subsidies for users, to monthly subscription plans that hide costs, to Token-based billing exposing enterprise bill crises, the AI industry has completed a three-stage leap in commercialization within three years—and a potential price war could reset this entire monetization logic back to zero.

According to The Wall Street Journal, OpenAI is considering significantly lowering the Token fees it charges users, in order to compete for enterprise clients from rival Anthropic. Sources familiar with the matter stated that this move is partly to "seize the initiative," as OpenAI expects Anthropic to take similar price-cutting actions. OpenAI CEO Sam Altman recently admitted at an event that AI usage costs have become "a huge problem," and said the company will "help people get more value for less money."

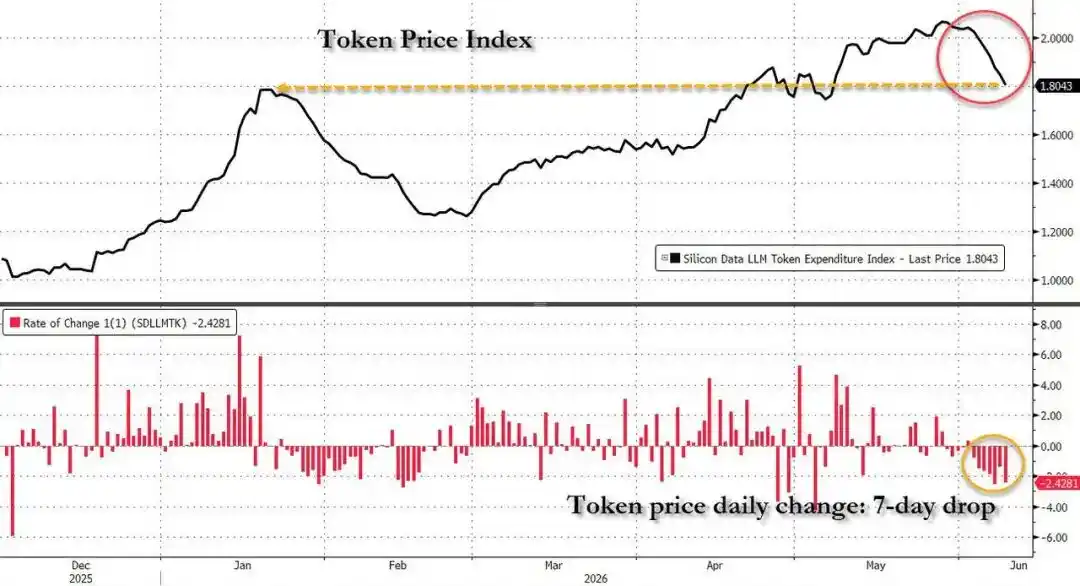

The timing of this news is particularly sensitive. OpenAI secretly filed for an IPO this week, while Anthropic is also in the final countdown to its own listing. Meanwhile, Bloomberg's Silicon Data LLM Token Expenditure Index has fallen for seven consecutive trading days, marking its longest losing streak since January this year, reflecting the market's deep-seated anxiety about the sustainability of AI bills. The report bluntly states that a price war would directly erode the profit margins of both companies—and both are already losing tens of billions of dollars due to the massive computing power required by AI systems.

The core of this discussion is no longer just a single price-cut decision, but a more fundamental question: As the narrative of "more Token consumption is better" reaches its end, who will tell the next commercialization story for the AI industry, and how will it be told?

01

The Initial Three Stages: From Monthly Subsidies to Token Bills

The commercialization of generative AI has undergone a clear three-phase evolution in just three years.

Stage One: Monthly and Annual Subscriptions set the industry baseline. In February 2023, OpenAI launched ChatGPT Plus with a monthly fee of $19.99, pioneering paid C-end access for large models; Baidu, Alibaba, and Tencent followed suit, making fixed-fee subscriptions the standard for early-stage business models.

Stage Two: The subsidy war erupted in full force. To boost ARR (Annual Recurring Revenue), the core anchor for financing valuations, major players turned to large-scale subsidies: Google offered students 15 months of Gemini Advanced for free, OpenAI launched a Team membership plan at $1 for the first month, ByteDance's Doubao entered the market with pricing "99.3% lower than the industry standard," and Baidu announced its core models would be free. The essence of subsidies was trading losses for growth—reportedly, Microsoft lost an average of over $20 per user per month under the GitHub Copilot subscription model, with some heavy users costing up to $80 a month in losses.

Stage Three: The forced switch to usage-based billing. On June 1, 2026, Microsoft announced that all GitHub Copilot plans would officially transition to Token-based billing, converting the $19 monthly fee directly into an equivalent Token credit. This change brought the true costs long hidden by subscription models into the open—according to user calculations in the Reddit community, a single agent programming session could consume $30 to $40, depleting a monthly plan in just one use.

02

Bill Out of Control: When Tokens Cost More Than People

The implementation of Token-based pay-as-you-go billing fully revealed the true face of enterprise AI expenditure.

The numbers on the enterprise side are staggering. Uber COO Andrew Macdonald publicly stated in May 2026 that the link between the growth in Token consumption and substantive product improvement "does not yet exist," and even coined a term for it: "tokenmaxxing," describing employees performing valueless tasks to boost usage metrics.

More direct data: Uber exhausted its annual Token budget in just the first four months of 2026; Salesforce expects to pay Anthropic around $300 million for the full year.

Anthropic's own developer documentation shows that developers using Claude Code incur an average cost of about $13 per workday, with 90% of users having daily costs below $30—translating this, a 10-person development team could spend over $75,600 per year on Token fees alone.

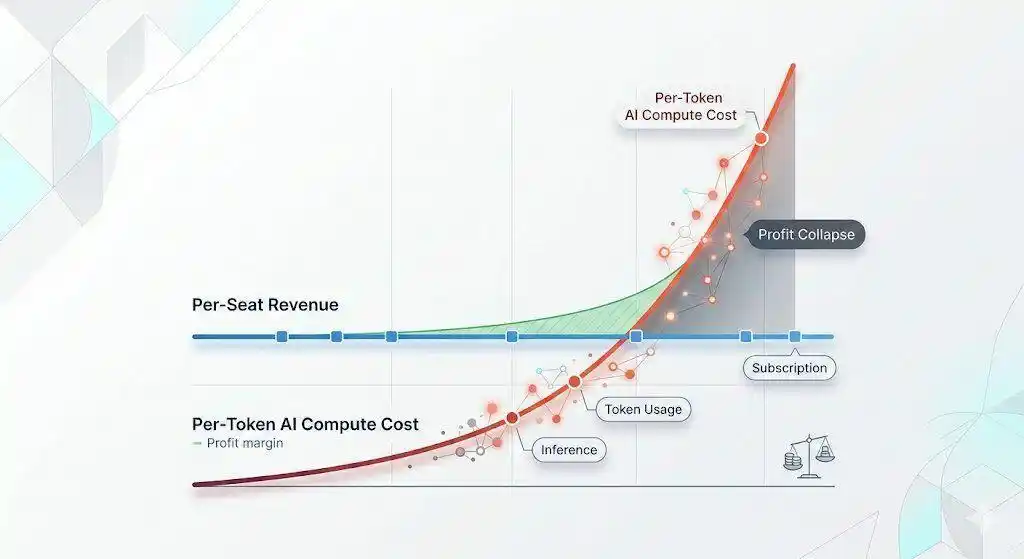

The return on investment is equally alarming. Enterprise data platform Entelligence.AI, after aggregating data from 2,444 companies, found that for every $1 spent on AI Token fees, only 18 cents generated actual value that reached users; 44 cents were used to fix bugs introduced by the AI itself, 27 cents went towards rework, and 11 cents were consumed by review friction.

Faced with runaway bills, enterprises have begun proactive control measures. Amazon halted internal AI usage leaderboards, instructing employees "not to use AI just for the sake of using it"; Microsoft plans to gradually phase out Claude Code subscriptions for employees in some key product divisions. Goldman Sachs notes that some companies' spending on AI Tokens already accounts for 10% of their total employee labor costs, and this proportion could rise further in the coming quarters. This isn't about demand disappearing, but the end of the era of reckless AI spending.

03

Act Four: Price War Ignited, OpenAI Considers Major Price Cuts

It is against this backdrop that the fuse for a price war was lit.

According to The Wall Street Journal, Altman's consideration of price cuts was directly triggered by the pressure to catch up with Anthropic. Anthropic's revenue has grown significantly recently, its programming tool Claude Code has become popular among software engineers, and this five-year-old startup's valuation has even surpassed OpenAI's for the first time.

However, the cost of this price war will be exceptionally heavy. If prices are significantly lowered, it will further compress the already negative profit margins of both companies, and the competitive landscape offers very limited room for maneuver.

And a fundamental risk long identified by investors is that OpenAI and Anthropic's products are highly substitutable; clients can easily switch from one to the other—meaning price cuts, even if they retain customers in the short term, cannot truly build a moat and only delay market share loss.

This dilemma also transmits outwards through the financial cycle between cloud computing giants and AI labs.

According to corporate disclosure documents compiled by The Information, OpenAI and Anthropic together account for over half of the approximately $2 trillion in future cloud service commitments from Microsoft, Oracle, Google, and Amazon. If price cuts lead to downward revisions in revenue expectations, this transmission chain will face pressure from both ends.

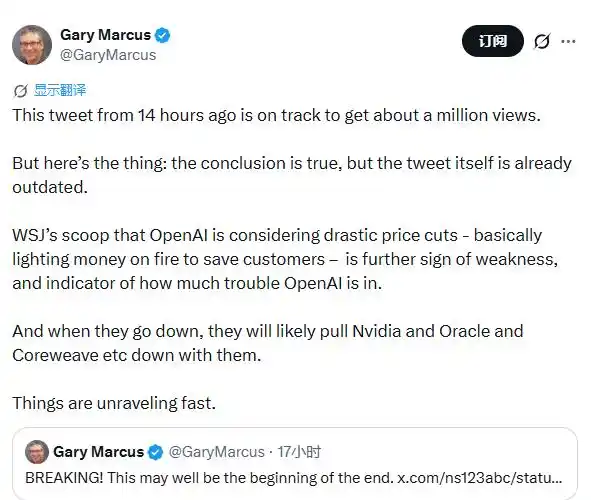

American neuroscientist and AI expert Gary Marcus said: "This further exposes the fragility of OpenAI and indicates how serious the predicament it faces is. If OpenAI goes into decline, it could very likely drag down companies like Nvidia, Oracle, Coreweave. The situation is deteriorating rapidly."

A divergence of views is playing out openly on Wall Street. JPMorgan TMT analyst Mark Schilsky believes the current billing anxiety is merely a "minimum speed bump on the road to higher spending": if the average price per million tokens falls, but the penetration rate of paid AI among US companies continues to rise, overall token usage will mathematically increase substantially; coupled with agentic AI pushing single-task token consumption to several times that of traditional Q&A modes, long-term total expenditure is expected to be significantly higher than current levels.

Goldman Sachs semiconductor analyst Jim Covello holds a more pessimistic view, believing that the current industry chain prosperity has directed almost all value towards semiconductor companies, a phenomenon "unprecedented in history and unsustainable." Once enterprises face the true price of usage-based billing, the capital flows supporting GPU procurement and model training could face a reversal.

04

Act Five: The Next Story for Token Economics?

After the price war, the next chapter of AI industry commercialization has yet to be written, but its outline is emerging.

A report from Citadel Securities offers a directional framework: tiered pricing and charging based on scarcity. Its core logic is that inference-intensive frontier AI won't disappear but will increasingly concentrate in the hands of a few large enterprises capable of bearing the compute costs; for the broader range of enterprises, simpler models might be a more productive path until physical constraints ease. This implies AI usage will move towards stratification—high-value, complex tasks will continue to use frontier models, while routine and batch tasks will shift towards cheaper or local models.

JPMorgan holds a relatively optimistic judgment: even if the per-unit token price falls, the proliferation of agentic AI will multiply token consumption per task—existing data shows that after agentification, token consumption per task can become 3.5 times the original—potentially still expanding the overall expenditure scale. The current billing anxiety might just be a "minimum speed bump on the road to higher spending."

Nebius Chief Revenue Officer Marc Boroditsky proposed the concept of "valuemaxxing," advocating for the industry to shift from pursuing Token consumption maximization to making every Token truly generate value. This direction is gradually becoming an industry consensus—but true commercial implementation still requires AI labs to find a pricing system that both reflects the true cost and is acceptable to enterprise clients. This is precisely the core unresolved proposition in all current debates.

However, perhaps the most overlooked variable in this price war is Chinese models.

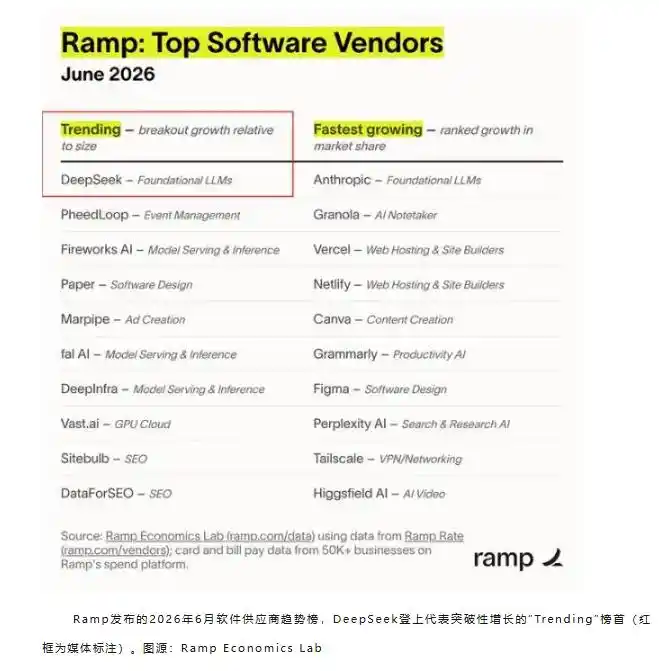

According to June data from American corporate spend management platform Ramp, DeepSeek has topped the list for growth in US enterprise software subscriptions. Ramp Chief Economist Ara Kharazian specifically emphasized that this is not about local deployment of open-source models, but rather "enterprises are directly sending and receiving data through DeepSeek," indicating real paid direct usage—he admitted "did not anticipate US companies would go and use DeepSeek." According to third-party estimates, DeepSeek V4-Pro's API price is about one-tenth that of GPT-5.5, and about one-eleventh that of Claude Opus 4.7.

As OpenAI and Anthropic, two tigers, fight, the ultimate beneficiary might be the player that has long embedded "accessible pricing" into its DNA and doesn't need to answer to IPO investors about profit margins. This may not be the most popular ending for this price war, but it is becoming an increasingly hard-to-ignore reality.

This article is from the WeChat public account "Hard AI," author: Xu Chao