Original Author: Arthur Hayes, Co-founder of BitMEX

Original Translation: BitpushNews

Editor's Note: In Arthur Hayes' latest article "The Butterfly Touch," it is anticipated that US dollar and Renminbi liquidity will continue to rise, benefiting Bitcoin and cryptocurrencies.

AI Optimism

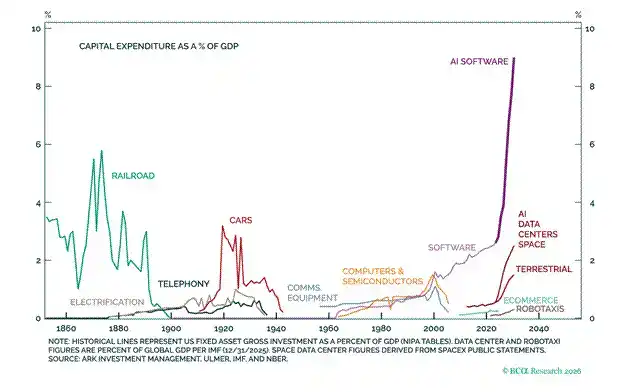

The capital expenditure (CAPEX) supporting AI model training and inference is unprecedented in human civilization. Many believe that this investment in intelligence will create value for humanity unlike any previous technological construction. I agree; however, as humans, we always tend to overdo things. In this universe, positive infinity and perfection are unattainable. Therefore, in anticipating a machine intelligence-driven future, we are likely to overbuild.

AI advocates cite nationalism as a reason for lavish spending, but patriotism should not have a price tag... Both the US and China believe that AI and technological hegemony are crucial to the survival of their domains.

Tech giants are also very happy to sell them horror stories: what will happen to this country if the other side gains hegemony in machine intelligence first. Objectively speaking, both leaders have witnessed firsthand how the proliferation of AI and drones can lead to victory and are convinced of it. Therefore, they will ensure that the primary economic and military objective is to further build the most efficient machine intelligence within their borders.

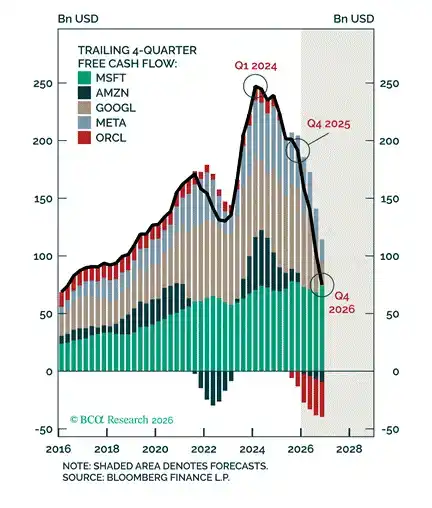

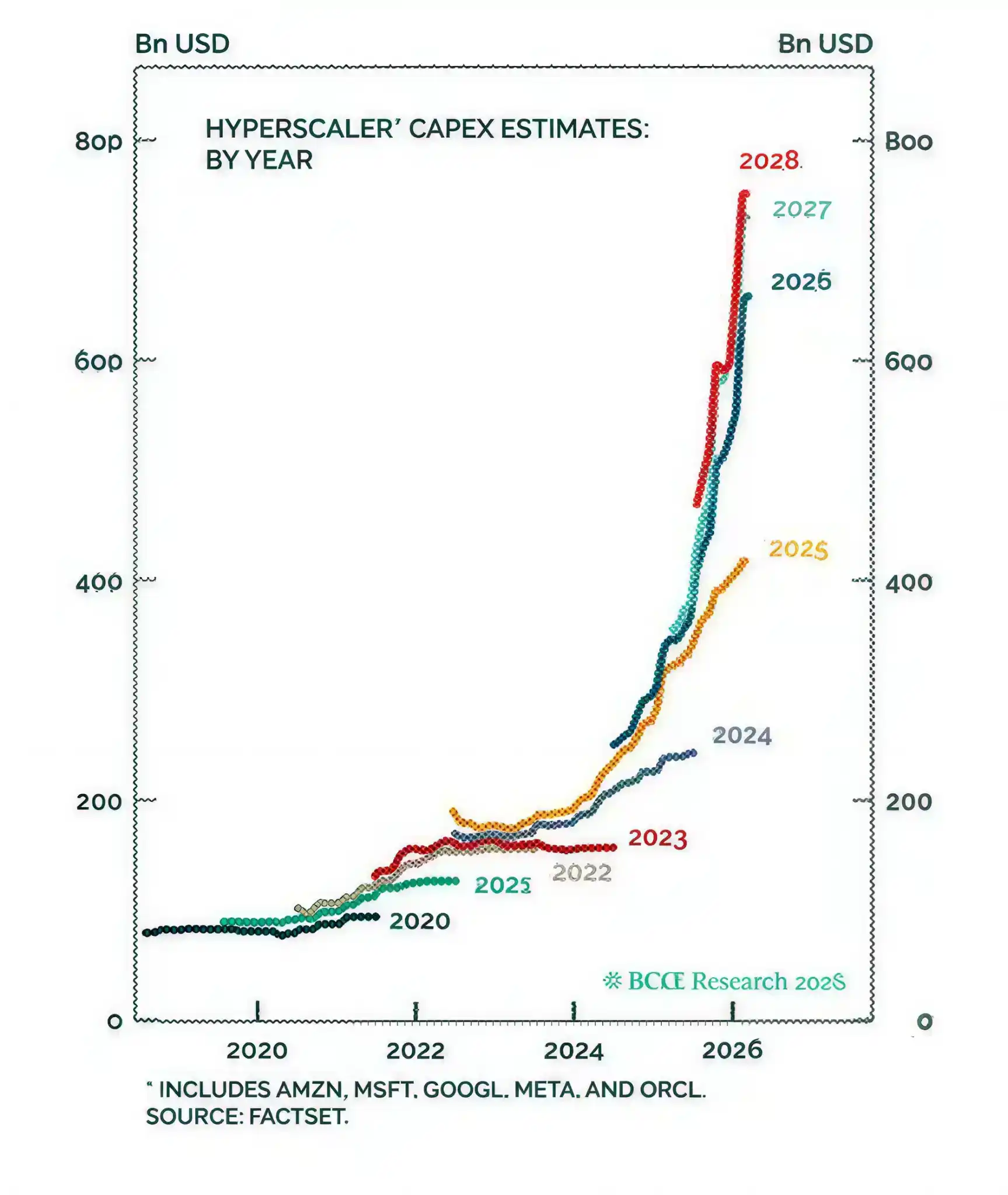

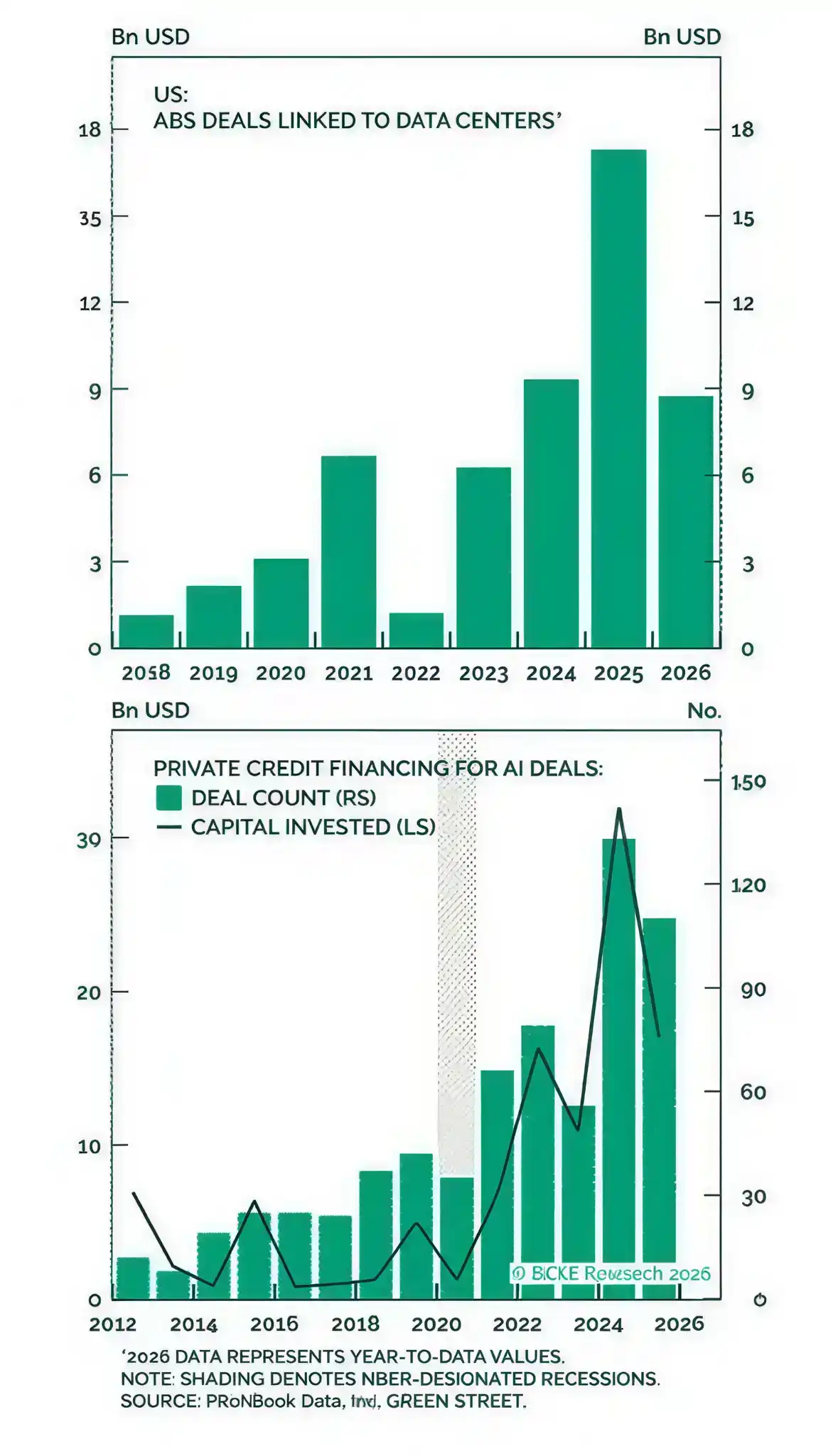

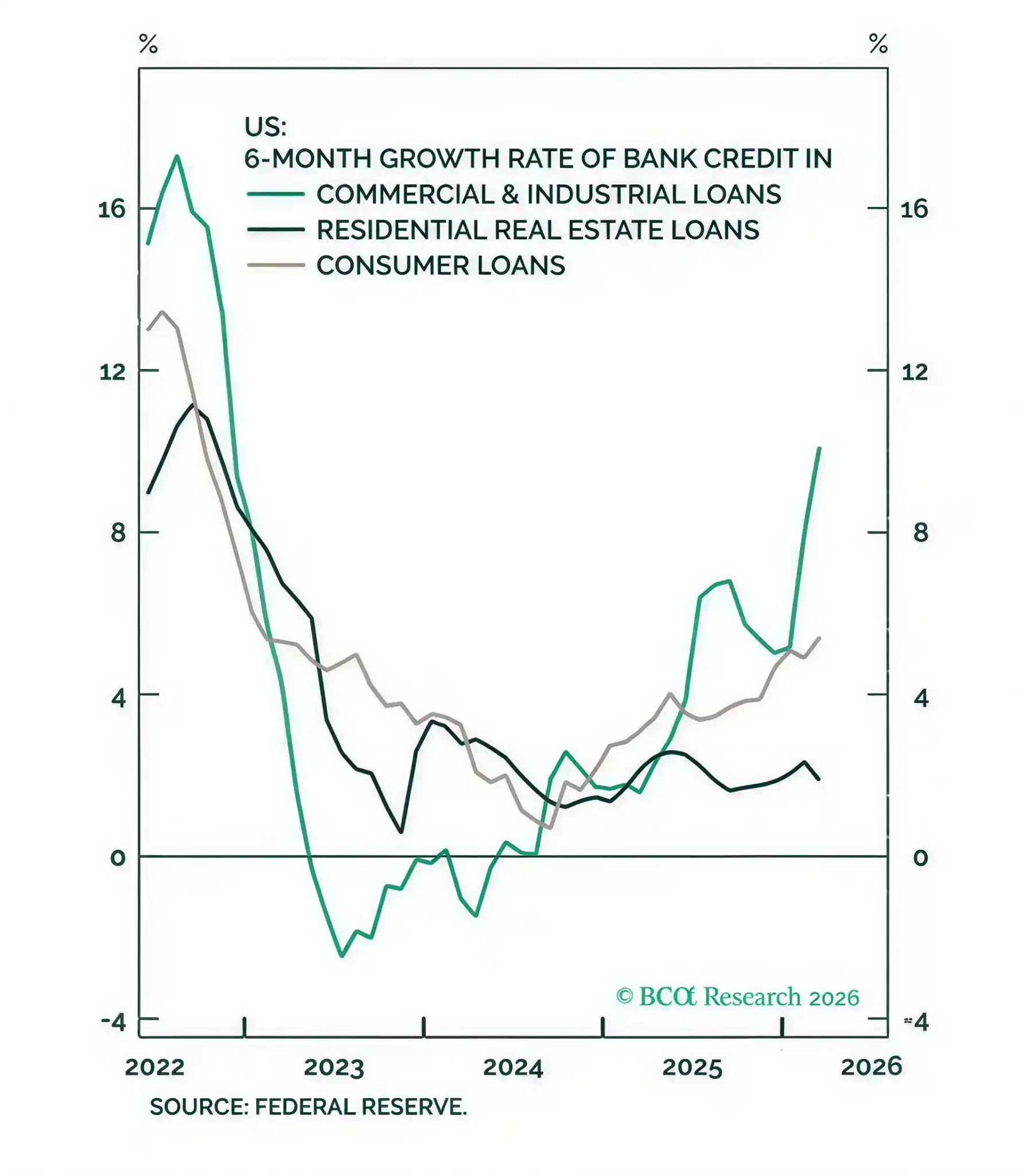

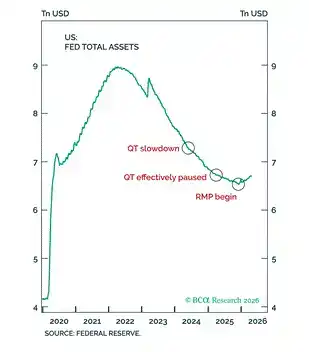

In the United States, most AI CAPEX to date has come from the operating cash flow of the most profitable software companies. But considering the scale of current and future expenditures, additional financing through credit channels will be needed.

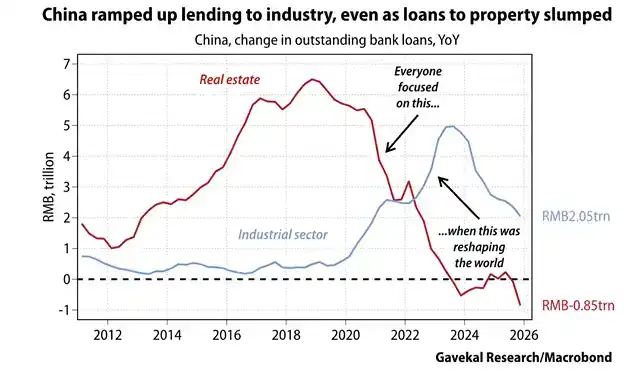

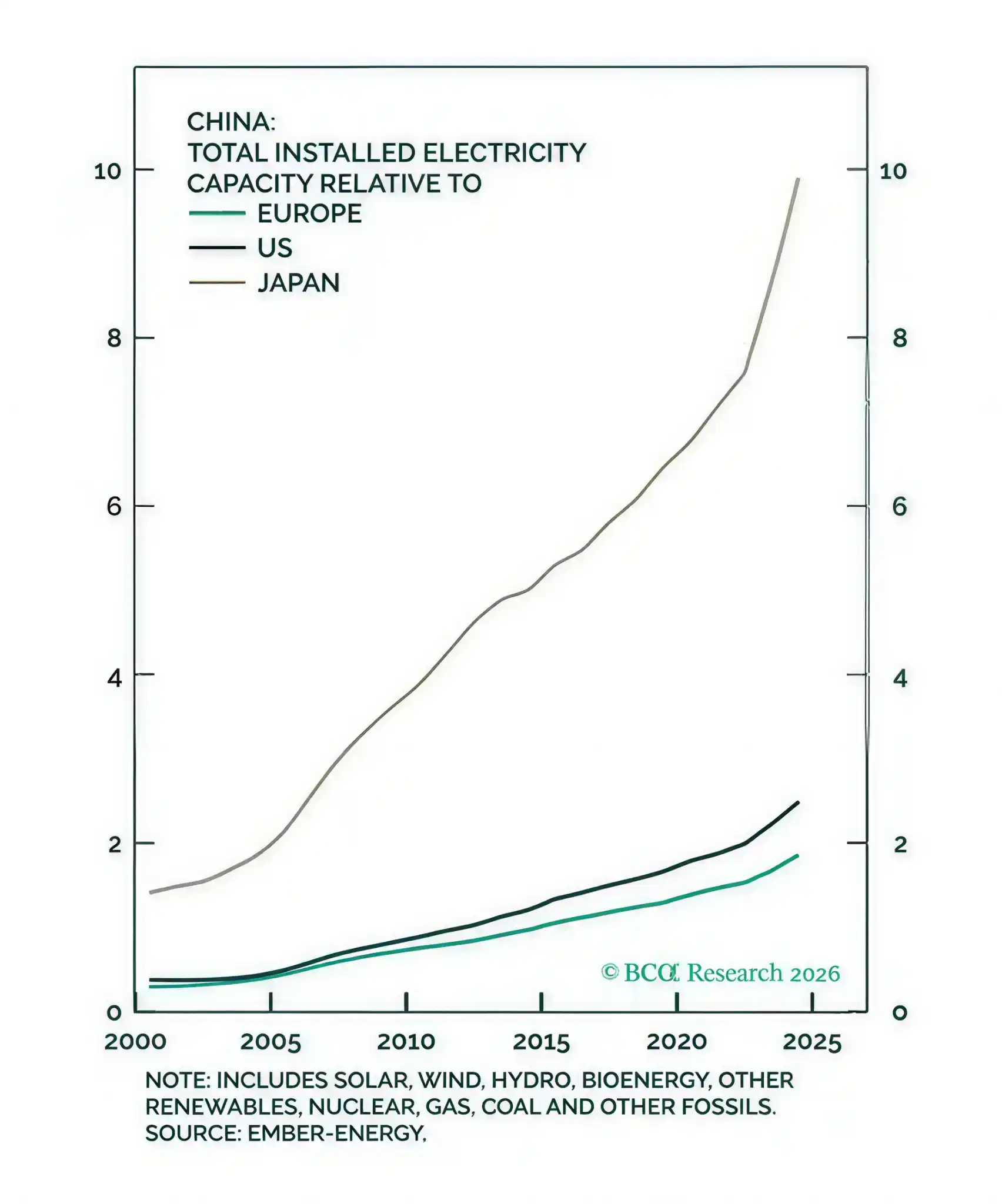

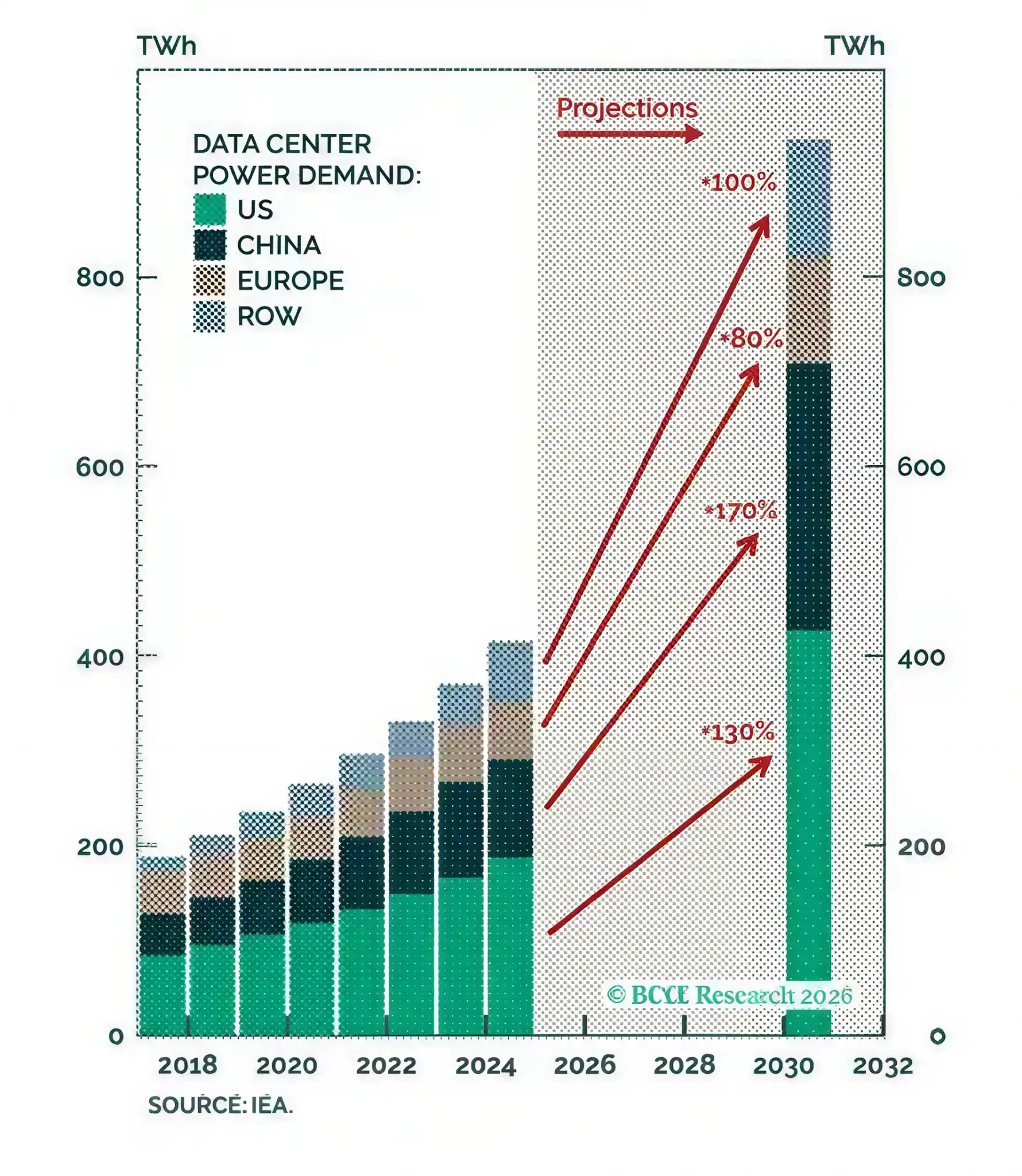

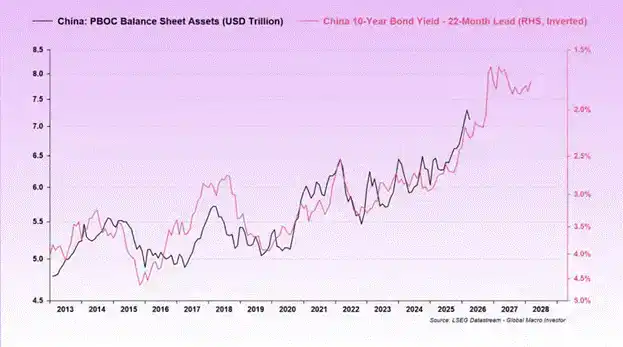

In China, banks are slowing down funding for real estate and instead funding the technology sector. In addition to data center-related expenditures, both the US and China are continuously investing funds to increase power supply.

That is to say, central banks are all creating more fiat currency and easing financial conditions.

The combination of political will (to win the AI race) and financial will (to fund construction through printing money and lending) creates a perfect environment for cryptocurrency. There will be far more fiat currency units tomorrow than today, and due to the surge in AI and electrification expenditures, the rate of change is accelerating. As the cost per unit of intelligence decreases and the complexity of tasks performed by AI increases, this means computational power consumption grows exponentially; this is the essence of "Jevons' Paradox."

Additionally, there is the "Red Queen Effect": as competitors improve model efficiency, a company's invested AI CAPEX quickly depreciates. This leads to a race to increase spending further to create better models to defeat opponents, while also making the hundreds of billions (soon trillions) invested by opponents obsolete. Therefore, unless hindered by exogenous market events, AI CAPEX spending will expand indefinitely.

When Will This Frenzy End?

I believe two events will occur almost simultaneously, changing people's perception of the necessity of spending trillions on building AI.

Market Indigestion: The occurrence of a massive and financially irresponsible AI-related IPO or mega-merger that the market cannot stomach. This will sober the market from its manic phase, and people will start questioning whether machine intelligence is truly worth this much money.

Shift in Political Winds: The 2028 US election. The increase in prices of raw materials, labor, and especially electricity due to massive AI construction is not popular in many regions. Furthermore, 90% of Americans do not hold significant amounts of stock and cannot benefit from soaring stock prices. Politically, it is very easy to campaign by being anti-AI, focusing on the value of human labor, and suppressing inflation.

But at this moment, US dollar and Renminbi liquidity will continue to rise. Bitcoin and cryptocurrencies will benefit from this.

Every Nation Sweeps Its Own Doorstep

Trump bombs Iran, fundamentally unconcerned about the war's impact on the global economy. Or perhaps he cares, but the assumption that this year's "special military operation" would lead to a quick victory has proven overly optimistic. The US possesses God-given cheap energy (fossil fuels) and fertile farmland. Things might get expensive, but Americans will not starve even if the Strait of Hormuz is partially closed—unless politicians decide to spend money on Fallujah instead of food stamps.

But the people of Europe, Africa, and much of Asia are less fortunate. Unfortunately, the political elites of these countries mistakenly believe that US politicians will consider their lack of food and energy when deciding whether to launch another war threatening the flow of basic commodities. Trusting the US, these countries stored their surpluses in US dollar financial assets instead of building pipelines, trade routes, or stockpiling necessities.

Marco Papic of BCA Research puts it best:

"The entire globe—literally—is wired for US hegemony... Why is German defense insufficient against Russia? Because... the US. Why do most Gulf states have little energy transport infrastructure bypassing the Strait of Hormuz? Because... the US. Why is global manufacturing concentrated in China? Because... the US."

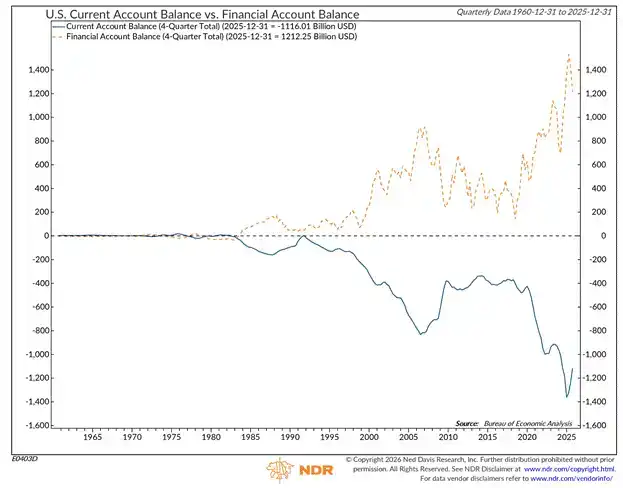

Due to an inability to access fertilizer or fuel, investment decisions in these countries will undergo dramatic changes. Holding US Treasuries or S&P 500 ETFs is meaningless when you cannot obtain food and energy because of a war you did not participate in. To remedy these deficiencies, sovereign nations will, in the future, marginally liquidate US dollar assets and instead invest in infrastructure, defense, and physical goods.

This is a problem for US financial markets due to the huge foreign ownership share. If left unchecked, the slow liquidation of US dollar assets will lead to market declines. US Treasury Secretary Bessent and other policymakers understand this. They have two options: encourage the use of US dollar swap lines or modify banking regulations.

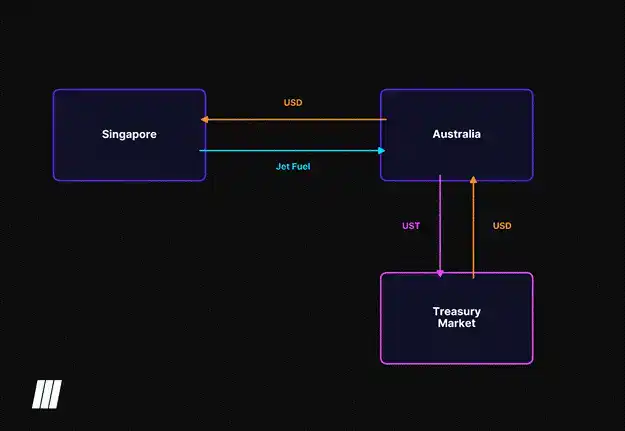

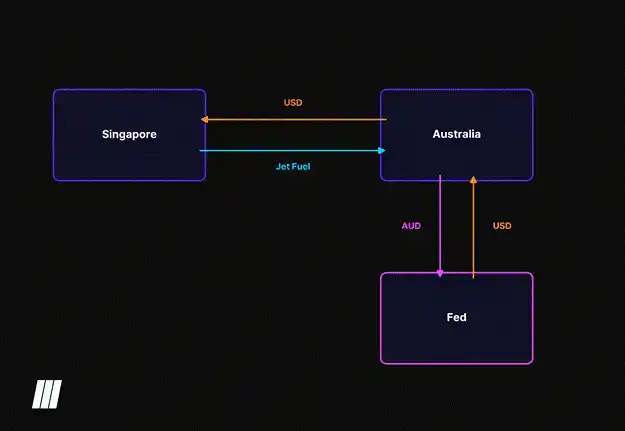

"Bad" Australia: Sells US Treasuries to buy jet fuel.

"Good" Australia: Borrows US dollars from the Fed to buy jet fuel.

If US markets need more momentum to offset sovereign selling, regulations can be eased to allow banks to hold more US Treasuries and stocks. The relaxation of eSLR (Enhanced Supplementary Leverage Ratio) related capital requirements is a step in this direction.

Since the establishment of the Petrodollar system in the 1970s, saving surplus in US dollar assets has been "best practice." But today, holding US dollar assets no longer guarantees you a ship of fertilizer or oil. "Just-in-time" logistics is dead; "just-in-case" is here to stay. This is a structural trend that will last for decades. This means monetary policymakers must maintain loose financial conditions to fill the void left by foreigners investing their savings in physical infrastructure rather than "phantom US dollar financial assets."

Higher + Longer

War is inflationary, and the US-Iran conflict is no exception. AI CAPEX and infrastructure construction are excuses for increasing lending. Politicians support money printing due to real and perceived necessity. This is why Bitcoin has outperformed other major risk assets like gold and US tech stocks since February 28th.

Bitcoin bottomed at $60,000 earlier this year, backed by trillions of US dollars and Renminbi yet to be created, and a return to $126,000 is a certainty. Many naysayers refuse to participate in this rally because Bitcoin's performance over the past 24 months has lagged behind tech stocks and gold. They don't understand why Bitcoin remains effective as a hedge against money printing. But it will demonstrate extreme sensitivity to fiat liquidity expansion. I expect the rally to intensify, becoming explosive once it breaks through $90,000 and many call option sellers are forced to cover.

I don't know how high Bitcoin can go, but I will set Maelstrom's portfolio risk to maximum unless a major change occurs. By the November midterm elections, US political sentiment towards AI and inflation could become very hostile, which might be a small hurdle in the ascent.

But remember: High oil prices don't hurt Trump as much as people think. MAGA is destined to lose in California (where energy policy leads to the highest gas prices in the US), but $100 crude and infrastructure reconstruction in Venezuela and the Middle East will benefit the oil and gas industries in states where Trump supporters reside. As long as money can be put in the pockets of ordinary Americans, Trump still has time to win re-election. So, let's go, baby, S&P 500 to 10,000!

It's time to play with Shitcoins. Besides Hyperliquid ($HYPE) and Zcash ($ZEC), which we are already heavily invested in, my next favorite is $NEAR. My next article will explain our thesis: why the "privacy narrative" combined with "Near Intents" will create positive cash flow for the protocol. This will completely reverse the token's sluggish price performance and create a massive catch-up opportunity, rapidly propelling it towards its all-time high from years ago.

It's a bull market; close your eyes and hit the buy button. There will be a time to sell, but it's not now. Don't mess it up, let's get crazy together.