Federal Reserve Chair Kevin Warsh did not announce an interest rate cut. Regarding inflation, he stated that inflation expectations and inflation risks have moderated over the past few weeks. He simultaneously reaffirmed that the Fed will maintain its 2% inflation target.

The latter part of his statement was not dovish, but the market first took the former part. Bitcoin quickly rebounded from its lows, once again approaching $60,000. Subsequently, weaker U.S. employment data continued to cool rate hike expectations, and the market movement evolved from "repair" into "relay."

Over the past few weeks, the market's greatest fear was that the Fed would continue to keep interest rates high, or even re-escalate tightening expectations. For Bitcoin, this is not an abstract macro judgment. The harder the interest rate expectations, the narrower the valuation space for risk assets, and the easier it is for leveraged positions to be liquidated first.

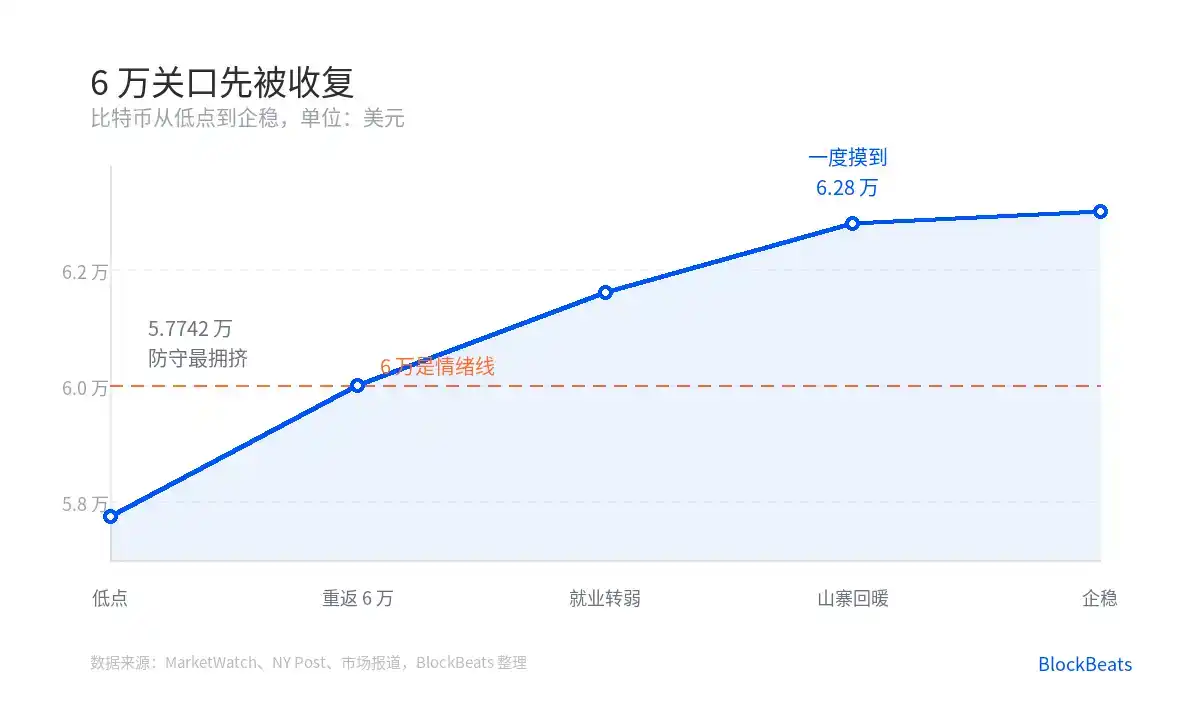

After Warsh downplayed inflation risks, the market first repriced "rate hike pressure." After weak employment data, this direction received another push. Bitcoin recovered from around $57,742 to above $60,000. While the price movement appears rapid, its essence is the market rolling back the previous round of panic trading.

On Deribit, traders concentrated on buying $50,000 put options. Open interest in gold perpetual futures reached a new high. A death cross also appeared on the technical charts. Several signals together indicate that the market is not simply bearish but is buying insurance against a decline.

This is different from an ordinary pullback. In an ordinary pullback, sellers simply want to exit. In a panic defense, traders simultaneously buy puts, purchase safe-haven assets, and reduce leverage. When the price touches a key level, liquidations amplify the volatility.

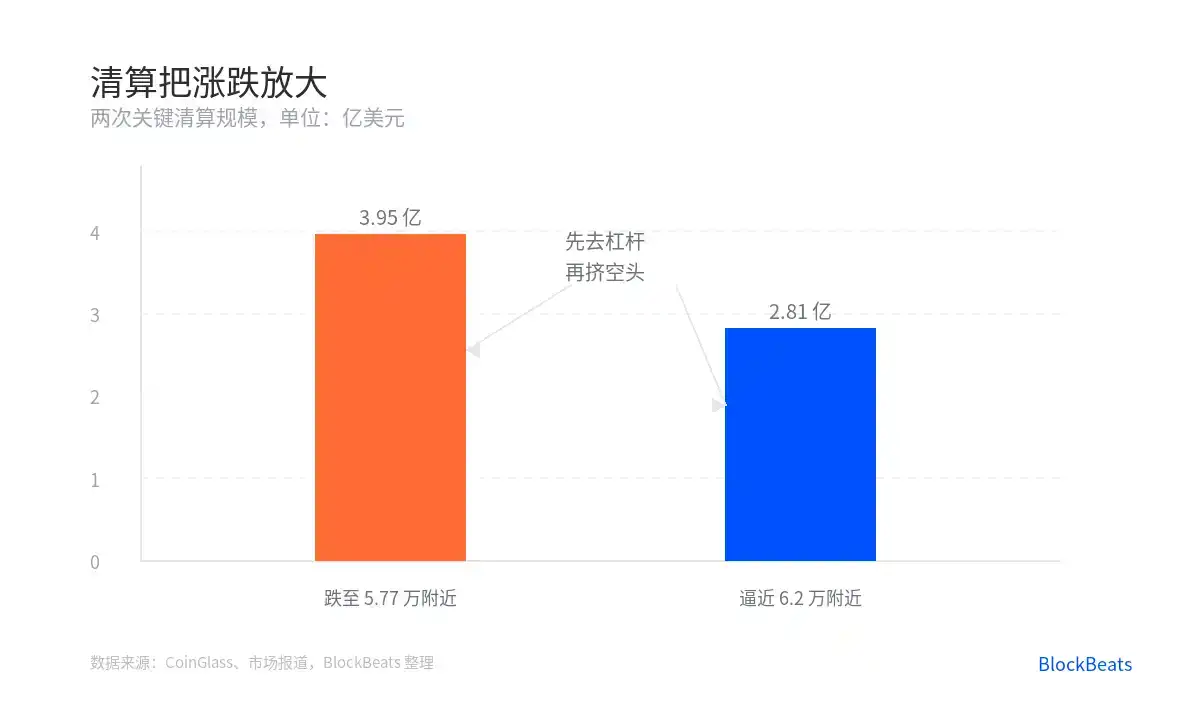

CoinGlass data shows that when Bitcoin fell near $57,700, it triggered approximately $395 million in liquidations. This figure indicates that the price decline was not solely driven by selling pressure but also by forced exits from leveraged positions.

After the forced exits, the market actually becomes more prone to a rebound.

The reason is straightforward. The previous decline liquidated some long leverage and pushed defensive sentiment to a high. When macro news marginally eased, the price only needed to return near a key level to make short sellers nervous. Short covering is essentially buying. The higher the price goes, the more it forces bearish positions to retreat.

This is the second layer of thrust. When Ethereum and Solana led the gains, Bitcoin once approached $62,000, liquidating approximately $281 million in bearish bets. This is not new-found belief but a reaction force from the position structure.

Therefore, this rebound cannot be attributed solely to one sentence from Warsh. A more accurate breakdown is into three stages.

First stage: Inflation risks were downplayed, easing market concerns about the Fed's path. Second stage: Weak employment data further pressured rate hike expectations downward. Third stage: Forced short covering pushed the spot price higher, faster.

If only looking at the first stage, the market movement can easily be interpreted as a "macro positive." If only looking at the third stage, one might mistakenly think it's a purely technical rebound. The real structure lies in both occurring within the same period. The macro provided the reason for prices to rise, while positioning provided the speed for prices to rise.

The reaction of altcoins also indicates this is not a single-coin market movement.

After Bitcoin reclaimed $60,000, Ethereum, Solana, and Dogecoin rose in sync. Ethereum subsequently led the gains among major cryptocurrencies, rising about 12% over the past week. When capital begins to spill over from Bitcoin to Ethereum and Solana, the market is no longer trading just "whether Bitcoin can hold."

The CoinMarketCap Altcoin Season Index rose to 52/100, the highest in three months. This level is微妙. It has just crossed the midpoint, indicating risk appetite has indeed returned, but it hasn't reached the stage of full altcoin frenzy.

This is the first thing to note. Warming altcoin sentiment does not mean an altcoin season is confirmed.

A true altcoin season typically requires broader capital dispersion. What we're seeing now is more like the market first buying back large-cap, liquid tokens after Bitcoin stabilized. The fact that Ethereum and Solana are outperforming while some smaller coins remain weak is itself a signal.

The second thing is that the options market does not fully believe in the rebound.

The put-call skew for BTC and ETH still shows traders are willing to pay a higher price for downside protection. The price has rebounded, but insurance isn't cheap. This detail is colder than the spot price.

If traders truly believed the trend had reversed, put option premiums would typically decline faster. The current state is more like the spot market pulled the price back first, while the derivatives market hasn't put away its umbrella.

The third thing is that a short squeeze cannot continue indefinitely.

Short covering brings buying pressure, but this pressure is one-off. It can push prices up from congested lows but cannot alone sustain an entire trend. After the liquidations end, the market needs new spot buying to take over.

So what really matters next is not whether Bitcoin has breached a certain integer level, but who is still buying after it does. Spot ETF flows, stablecoin liquidity, and the strength of follow-through gains in Ethereum and Solana will be more informative than a single day's gain.

The fourth thing is that macro variables remain the same sword.

This rally benefited from declining inflation risks and weakening employment. Looked at the other way, if subsequent data points again to sticky inflation, or if Fed rhetoric turns hawkish again, the market will price it in reverse using the same logic. Bitcoin is not an asset detached from macroeconomics; it just reacts faster to changes in macro expectations.

The price has bounced back from excessive defensiveness, but true confirmation will come when the options market is willing to remove the insurance.