Written by: ChandlerZ, Foresight News

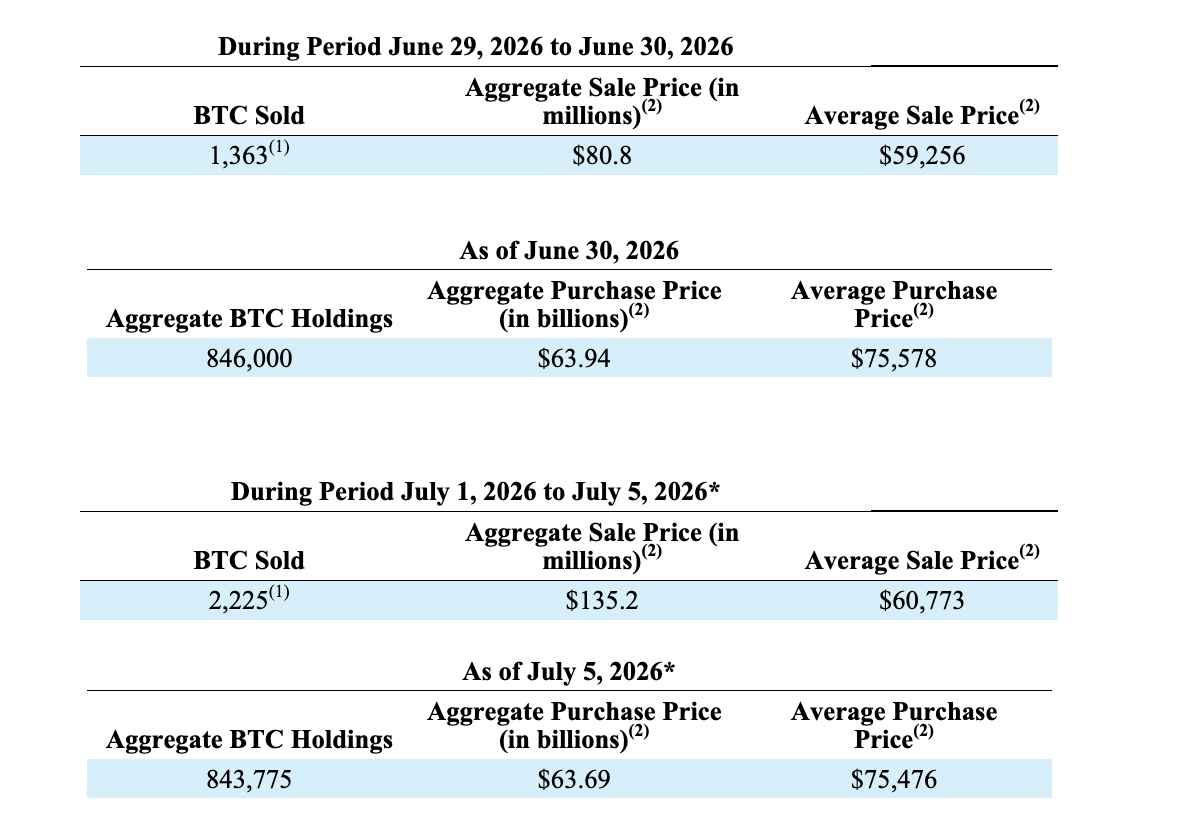

On July 6, Strategy (formerly MicroStrategy) disclosed in an SEC 8-K filing that the company sold 1,363 Bitcoin from June 29 to 30 at an average price of approximately $59,256, totaling about $80.8 million; and sold 2,225 Bitcoin from July 1 to 5 at an average price of approximately $60,773, totaling about $135.2 million. The proceeds were used to pay preferred stock dividends and supplement US dollar reserves.

This is the largest net sale by Strategy since initiating its Bitcoin strategy in 2020, and the company's first institutionalized reduction of core assets in six years. The average selling price was approximately $60,200, below the company's average cost basis of about $75,476 per Bitcoin, resulting in a loss of approximately $15,276 per coin, totaling $54.81 million.

As of July 5, Strategy cumulatively holds 843,775 Bitcoin, with a total acquisition cost of approximately $63.69 billion. It remains the publicly traded company with the largest Bitcoin holdings globally.

According to official statements, as of July 5, Strategy's US dollar reserve balance was $2.55 billion, unchanged from the previous week. In the second quarter of 2026, the company reported a digital asset loss of approximately $8.32 billion, including approximately $8.31 billion in unrealized losses and about $900,000 in realized losses. As of June 30, the book value of its Bitcoin holdings decreased to $49.67 billion, falling below the acquisition cost. Strategy will record a full valuation allowance for the related deferred tax assets.

After the disclosure, Bitcoin quickly dipped below $61,500, then reversed after the US stock market opened, with buying interest pushing it back up to around $64,500. MSTR's stock price corrected by about 2% following a 21% gain the previous week but is still down over 35% year-to-date.

From 32 to 3,588, a 100-Fold Increase in Six Weeks

Selling Bitcoin was once a taboo for Strategy. In September 2020, after completing his first $425 million Bitcoin purchase, founder Michael Saylor told CoinDesk in an interview, "I didn't buy it to sell it. Ever." For the next five years, Strategy only bought and never sold, positioning itself as a permanent holder of Bitcoin using its corporate balance sheet.

December 2022 was the only exception. Strategy announced the sale of 704 Bitcoin at an average price of about $16,776, but repurchased 810 Bitcoin two days later, resulting in a net increase in holdings. The SEC filing characterized this move as tax-loss harvesting, using capital losses to offset previous capital gains for tax benefits.

On May 5, 2026, during its Q1 earnings call, Strategy first signaled a potential sale. Michael Saylor stated, "We might sell some Bitcoin to pay dividends, to get the market accustomed to it."

He later told Fortune in an interview that the purpose of those remarks was "to create panic and squeeze shorts and haters." However, an SEC filing three weeks later revealed that Strategy sold 32 Bitcoin between May 26 and 31, raising approximately $2.5 million.

Six weeks later, that number grew from 32 to 3,588.

$1.25 Billion Sales Authorization, 17% Burned in a Week

The sale of 3,588 coins was not a temporary decision. On the same day as the first Bitcoin sale (June 29), Strategy released a new capital framework titled "Digital Credit Capital Framework," formally institutionalizing Bitcoin sales into company policy.

The framework's core provisions include a US Dollar Reserve Policy, adjustments to the STRC Dividend Policy, a Preferred Stock Repurchase Plan, a Common Stock Repurchase Plan, and a BTC Liquidation Plan. Key points authorize management to sell up to $1.25 billion worth of Bitcoin (approximately 20,800 coins at current prices, representing 2.5% of total holdings) when necessary; establish a US dollar reserve system with a minimum level equal to the sum of preferred stock dividends and interest expenses for the next 12 months; increase the STRC preferred stock's annual dividend rate from 11.5% to 12%, effective July 1; and authorize up to $1 billion in preferred stock repurchases and $1 billion in common stock repurchases.

As of June 28, Strategy's US dollar reserves stood at $2.55 billion. When releasing the framework, Strategy aimed to signal that selling Bitcoin was merely one option in its overall capital management toolbox and that the company had sufficient cash reserves to meet dividend obligations. However, the speed of the sales clearly exceeded market expectations. 3,588 coins, $216 million, meant that 17% of the $1.25 billion sales authorization was consumed in its first week of effectiveness.

From 2020 to 2025, Strategy's Bitcoin acquisition strategy was built on an aggressive financing engineering model—issuing convertible bonds, offering common stock, issuing preferred stock, and using all raised funds to purchase Bitcoin. This model worked perfectly during Bitcoin bull runs, as asset appreciation covered financing costs, creating a positive feedback loop between the company's stock price and Bitcoin.

Strategy currently has four series of preferred stock trading in the market: STRC (12% annual dividend), STRK (8%), STRF (10%), and STRD (10%), with combined annual dividend obligations of approximately $1 billion. Preferred stock dividends are rigid expenses that must be paid on time regardless of Bitcoin's price movement. The company's software business (formerly MicroStrategy's BI products) generates less than $500 million in annual revenue, far from enough to cover the dividends.

This creates a significant contradiction: Strategy raises funds by issuing preferred stock to buy Bitcoin, but the dividend obligations of those preferred stocks then force the company to sell Bitcoin to pay the dividends. This contradiction was masked when Bitcoin's price was above the acquisition cost.

Bitcoin has fallen significantly from its October 2025 all-time high. Strategy's comprehensive average cost is approximately $75,476, while this batch was sold at an average price of only about $60,200, incurring a loss of over $15,000 per coin. The Q1 financials recorded a $12.5 billion digital asset impairment loss, and Q2 recorded another $8.32 billion. The company is now selling Bitcoin below cost to pay dividends on securities issued to buy Bitcoin in the first place.

Premium Collateral

3,588 coins represent 0.4% of the total 840,000-coin holdings, having a limited direct impact on Bitcoin's market price. The $1.25 billion sales authorization ceiling represents 2.5% of total holdings; even if fully utilized, it's far from a liquidation. From a balance sheet perspective, Strategy faces no solvency crisis.

But MSTR's stock price has never been priced based solely on its balance sheet. This stock has long traded at a premium of 1.5 to 3 times its Bitcoin Net Asset Value (NAV). The premium investors pay is not for the 840,000 Bitcoin themselves (directly buying BTC or an ETF is cheaper). Instead, it's for a narrative product provided by Michael Saylor: a Bitcoin absorption machine that only buys and never sells, with holdings perpetually growing, never appearing on the sell side. This promise was the collateral for MSTR's entire premium.

As of June 28, Strategy had $2.55 billion in US dollar reserves and annual preferred stock dividend obligations of about $1 billion. The cash was sufficient to cover over two years of payments. Financially, Michael Saylor did not need to sell Bitcoin now. Yet, he still initiated the institutionalized sales framework, raised the STRC dividend rate, and executed $216 million in sales within a week. The four series of preferred stocks generate monthly cash outflow obligations, while the promise of "never selling" precluded using core assets for repayment.

When these two realities coexist on the same balance sheet, one must give way. Michael Saylor chose to give way on the latter.

Following the first coin sale this year, Michael Saylor's new narrative is that if the interest/dividends on issued bonds or preferred stocks can be serviced at a low financial cost, Strategy can use leverage to buy and lock in more Bitcoin at lower prices. Since overall asset appreciation during a bull market far outweighs interest costs, theoretically, through instruments like convertible notes, the company could buy 20 Bitcoin for every one it sells.

But each time Saylor sells Bitcoin, he must explain why it doesn't constitute breaking his promise, and the explanations themselves consume the credibility he has built over six years.

MSTR's premium over its BTC NAV has never been because this company holds Bitcoin more efficiently than an ETF. It was largely because Saylor turned "never selling" into a corporate governance-level religious ritual. Once the ritual is interrupted, MSTR becomes just a leveraged Bitcoin holding vehicle, and the market already has plenty of cheaper alternatives.

Strategy's balance sheet can withstand the paper volatility of 840,000 Bitcoin, but it may not withstand a story that is fading.