Recent reports indicate that Moonshot AI has notified its shareholders, officially initiating the dismantling of its VIE and red chip structure to clear obstacles for a Hong Kong IPO.

Just half a year ago, Moonshot AI founder Yang Zhilin reiterated in an internal letter that the company was "in no hurry to go public in the short term."

"This step is more like clearing structural hurdles before an IPO, meaning the company has seriously entered the IPO preparation phase. But several hurdles remain: equity structure, regulatory communication, domestic filing, security review, HKEX materials, financial audits, and market timing," said Huang Lichong, President of Huisheng International Capital. Dismantling VIE and red chip structures essentially clarifies the positions of control rights, responsible entities, and regulatory boundaries. If smooth, the window could be six months to a year; if complex due to regulations, shareholders, tax, or foreign capital arrangements, it might take longer.

Phoenix WEEKLY Finance inquired with Moonshot AI regarding the IPO, but received no reply by the time of publication.

Regarding expectations, the capital market has already given its answer in advance. When founded in 2023, Moonshot AI's valuation was approximately $3 billion; by May 2026, this figure had surpassed $20 billion.

In reality, with the successive listings of Zhipu AI and MiniMax on the Hong Kong stock market, the valuation logic of the secondary market for large model companies has suddenly been unlocked. The long-term reliance on narratives to support valuations in the primary market has become a thing of the past. "Going public" itself is also shifting from an outcome to a competitive method.

"Moonshot AI's move considers both seizing the golden window for a Hong Kong listing and is forced by industry competition prompting proactive layout," said Zhang Yi, CEO of iiMedia Consulting Group.

Perhaps for Moonshot AI, the real question is no longer "whether to go public," but rather, when other competitors have already entered the next round, Moonshot AI cannot afford to stand still.

$20 Billion Valuation May Be Tinged with Capital Market Sentiment

Since the beginning of 2026, the capital "atmosphere" in the large model industry has rapidly heated up.

Over the past three years, Chinese AI startups have undergone a transformation from being neglected to becoming darlings of capital. However, what truly turned the industry sentiment around was the successive Hong Kong listings of Zhipu AI and MiniMax earlier this year.

On January 8, 2026, Zhipu AI took the lead in listing on the HKEX with an issue price of HK$116. On its first trading day, the stock closed at HK$131.5 per share, up 13.17%, with a total market capitalization reaching HK$57.89 billion. In the following months, Zhipu AI's stock price continued to rise. As of the close on May 26, its total market capitalization had exceeded HK$599.6 billion, nearly a tenfold increase from its initial listing.

On January 9, MiniMax followed suit, listing on the HKEX with an issue price of HK$165. On its first trading day, the stock closed at HK$345 per share, a surge of 109% from the issue price, with a total market capitalization surpassing HK$106.7 billion. Currently, its total market capitalization exceeds HK$241.1 billion.

This provided the entire industry with pricing benchmarks. Since then, AI is no longer seen as just a technological story but as the next platform-level opportunity.

With such precedents, Moonshot AI's valuation also rapidly climbed.

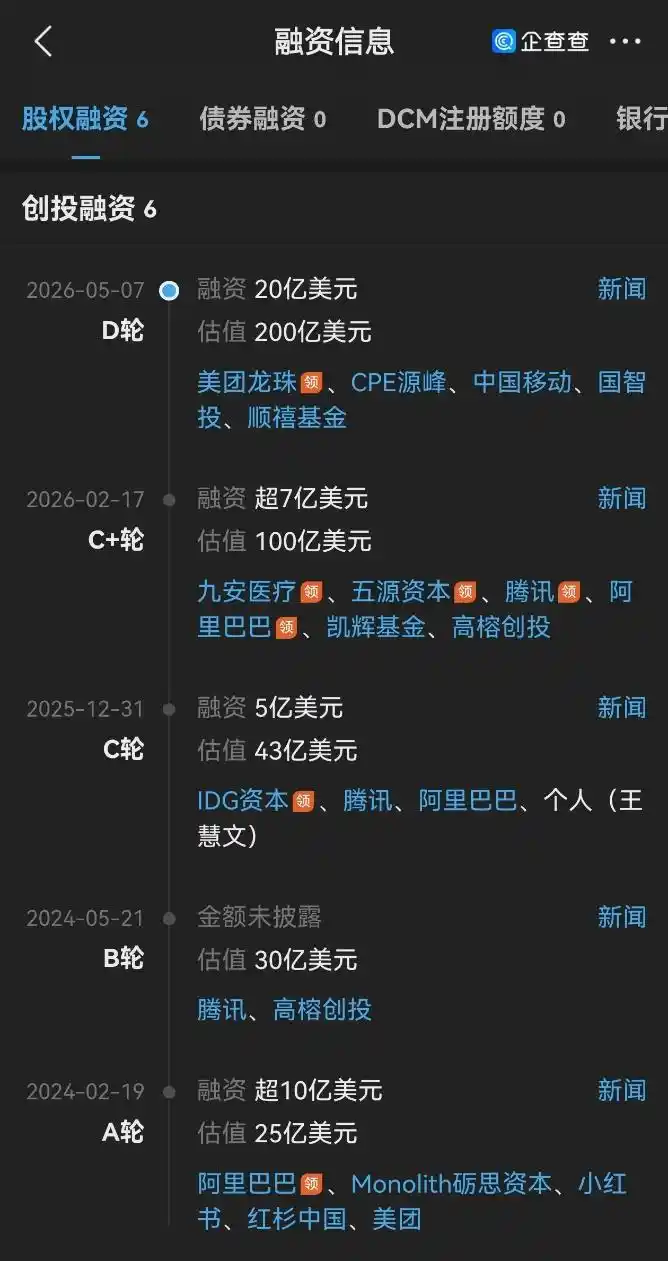

In November 2025, Moonshot AI's valuation was $4.3 billion; by May 2026, it had exceeded $20 billion. In just half a year, its valuation nearly quadrupled, with cumulative financing exceeding $3.2 billion. Moonshot AI has also completed a rare capital leap for a domestic large model startup.

"Revenue is the foundation. Capital pricing mainly focuses on three things: first, foundational model capabilities; second, user access and developer ecosystem; third, the imaginative space for future platformization," Huang Lichong believes. For companies like Moonshot AI, capital is buying not today's profit statement, but a scarce ticket in the Chinese large model race. Whoever can become the next-generation AI gateway may gain access to new profit pools like search, office work, developer tools, enterprise services, and Agent execution.

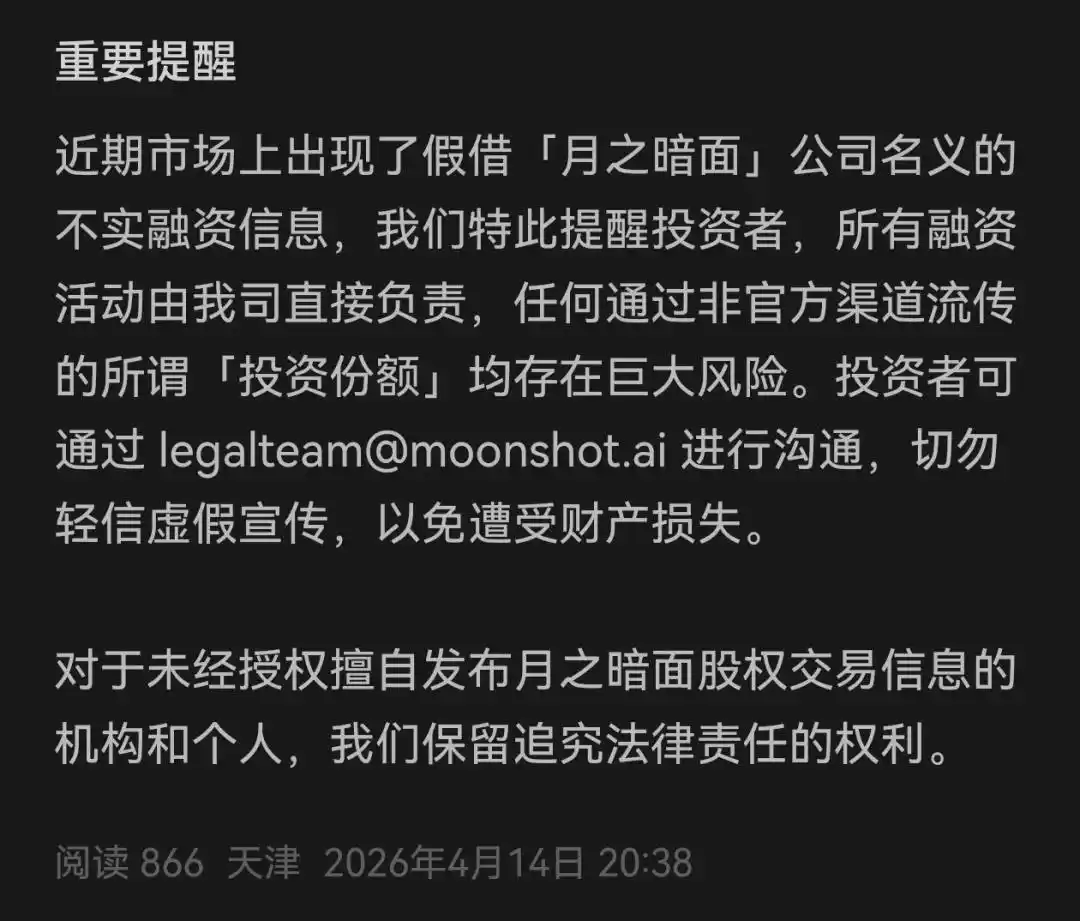

This year, information about unofficial financing shares not from Kimi has even frequently appeared in the market.

In April, Kimi publicly refuted rumors, stating, "Recently, false financing information purporting to be from 'Moonshot AI' has appeared in the market. We hereby remind investors that all financing activities are directly handled by Moonshot AI. Any so-called 'investment shares' circulated through unofficial channels carry significant risks."

Screenshot of Kimi's response.

When capital frantically searches for the "next Zhipu AI" or "next MiniMax," it's difficult for Moonshot AI to keep capital at bay.

"A $20 billion valuation seems more like an advance payment on the future," Zhang Yi believes, attributing it to the capital market pricing in growth dividends ahead of time.

Huang Lichong stated, "This valuation only holds up if three things materialize: continued model leadership, sustained commercialization scaling, and declining unit inference costs. Otherwise, it's just sentiment-driven valuation."

R&D Pace May Be Constrained, Commercialization Moves to the Forefront

Among domestic large model startups, Moonshot AI is an "outlier."

For a long time, Yang Zhilin has been one of the most typical "tech-focused" representatives among domestic AI entrepreneurs. Compared to traffic competition and commercial expansion, he emphasizes foundational model capabilities, organizational efficiency, and long-term R&D investment. This has long positioned Moonshot AI as one of the domestic teams closest to the routes of OpenAI and Anthropic.

QuestMobile data shows that the monthly active user (MAU) count for the Kimi App dropped from 21.653 million in Q1 2025 to 9.027 million in Q4 2025.

In his year-end all-staff letter in 2025, Yang Zhilin clarified the direction of this round of adjustment: focus on Agents, not targeting absolute user numbers, persistently pursuing intelligence limits and productivity value, and significantly cutting annual advertising spending, shifting to technology-driven commercialization.

In January 2026, Kimi released its flagship model K2.5. According to multiple media reports, less than a month after the model's release, the company's revenue over nearly 20 days had already exceeded its total revenue for the entire year of 2025; as of April 2026, the company's Annual Recurring Revenue (ARR) exceeded $200 million, with paid subscriptions and API revenue gradually becoming new growth engines.

Moonshot AI is attempting to prove to the outside world that despite reduced MAU, Kimi's commercial capabilities remain intact.

Qichacha shows that in May this year, Moonshot AI completed another $2 billion Series D financing round, led by Meituan Longzhu, with participation from institutions like China Mobile and CPE, which may indicate capital's approval of Kimi's adjustments in its business model.

Screenshot of Moonshot AI's $2 billion Series D financing.

However, post-financing, AI companies cannot avoid the continuous investment race. Training compute, inference costs, data resources, and talent reserves all imply massive capital consumption.

If entering the secondary market, the rules begin to change. Beyond investment, investors will also demand corresponding returns.

Huang Lichong predicts significant changes for Moonshot AI post-IPO. First, the organization will become heavier. Financial disclosure, internal controls, compliance, model safety, and data governance will become institutionalized. Second, the R&D pace will be more constrained. In the past, it could focus solely on model breakthroughs; post-IPO, it must explain input-output ratios, compute expenses, loss boundaries, and commercialization paths. Third, commercialization will be brought to the forefront. Investors won't pay for "model leadership" indefinitely; they will look at subscriptions, APIs, enterprise clients, Agent revenue, and gross margins.

"Only raising funds without model leadership will eventually be disproven. Only making models without capital and commercialization won't survive to the end," in Huang Lichong's view. The real test for Moonshot AI post-IPO is whether it can transform "technological scarcity" into "sustainable revenue" and "explainable valuation."

(Image source: Moonshot AI official)

This article is from the WeChat public account "Phoenix WEEKLY Finance", author: Wang Han