市场观点

宏观流动性

货币流动性整体紧缩。本周三公布的美国7月CPI数据8.5%好于预期的8.7%,较前值的9.1%大幅回落,预示着美国通胀峰值或许已经过去。接下来会有9月22日加息减缓利好,大概率从75BP下降到50BP,具体要看新的8月CPI是否继续下降。CPI目前主要是油价决定,还可能有起伏。美元指数持续下挫1%创一个月新低,促使风险资产全面反弹走高。美股刷新三个月新高,进入技术性牛市,BTC大概率趋同跟随。

BTC依然是长期囤币党主导。随着市场从近期低点反弹,BTC长期持有者并未大幅减持。65%的BTC一年未动过,45%的BTC两年未动过。交易所余额由12.6%降低到12.4%,7日流入量达21个月低点。

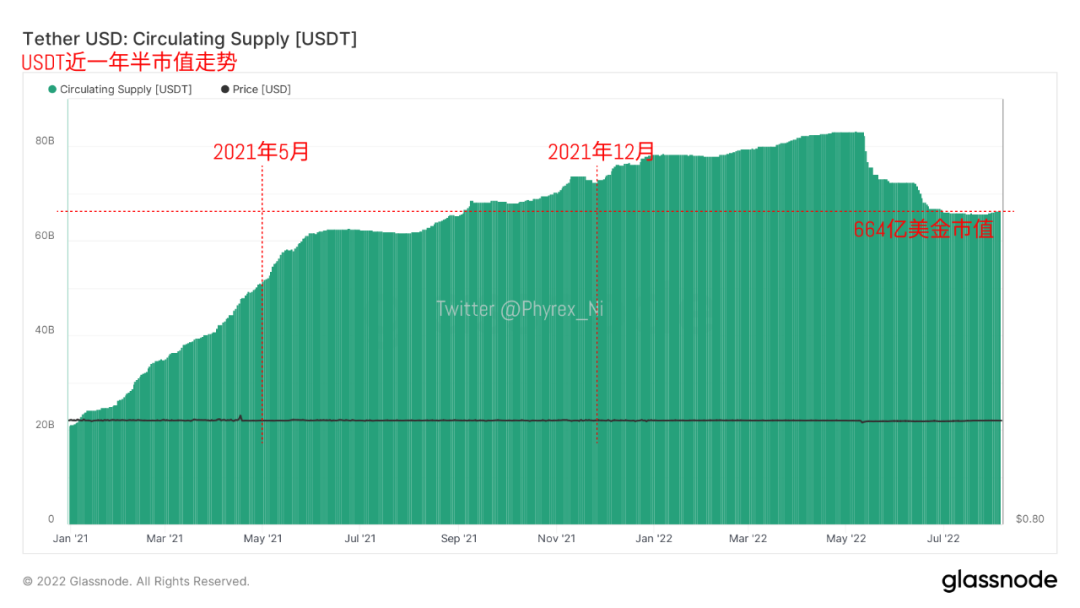

外部资金仍然未出现入场迹象。稳定币市值是最好衡量资金入场的根据。USDT继续在少量增加,而USDC则几乎在等量减少,这里更大的可能还是汇率搬砖。外部资金的刺激是市场是否会转向的信号,目前这个信号尚未出现。

BTC长期市场指标

长期趋势指标MVRV-ZScore以市场总成本作为依据,反映市场总体盈利状态。当指标大于6时,是顶部区间;当指标小于2时,是底部区间。当前指标为0.11,依然在底部低估区间。

BTC短期市场指标

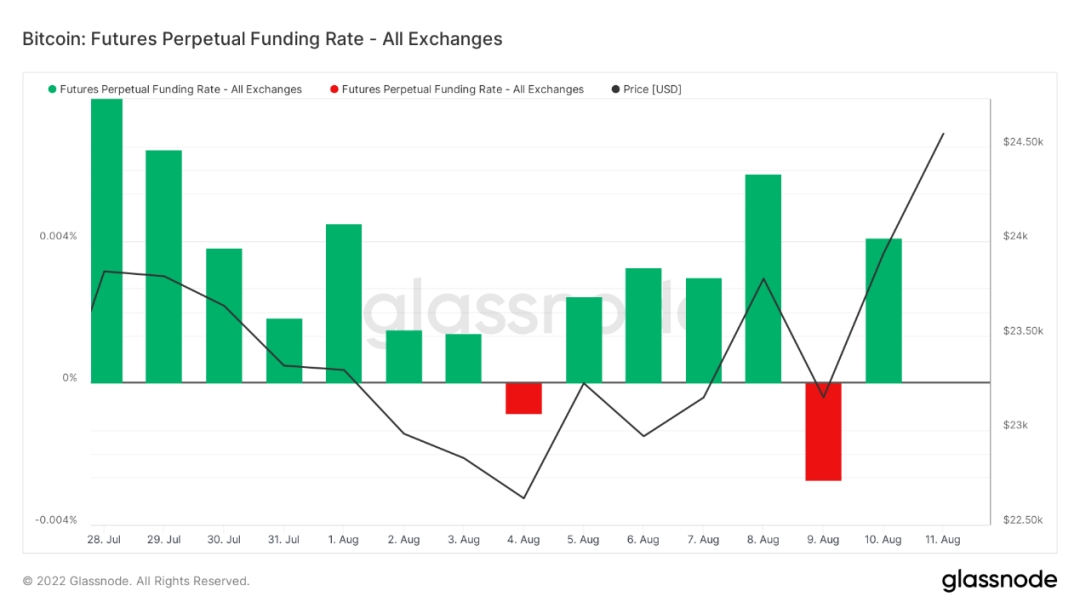

期货资金费率:上周资金费率较高,本周明显下降,说明回调时多头止损平仓较多。费率0.05-0.1%,多头杠杆较多,是市场短期顶部;费率-0.1-0%,空头杠杆较多,是市场短期底部。

期货多空比:1.1。市场继续上涨概率大。多空比数据波动大,参考意义有所削弱。

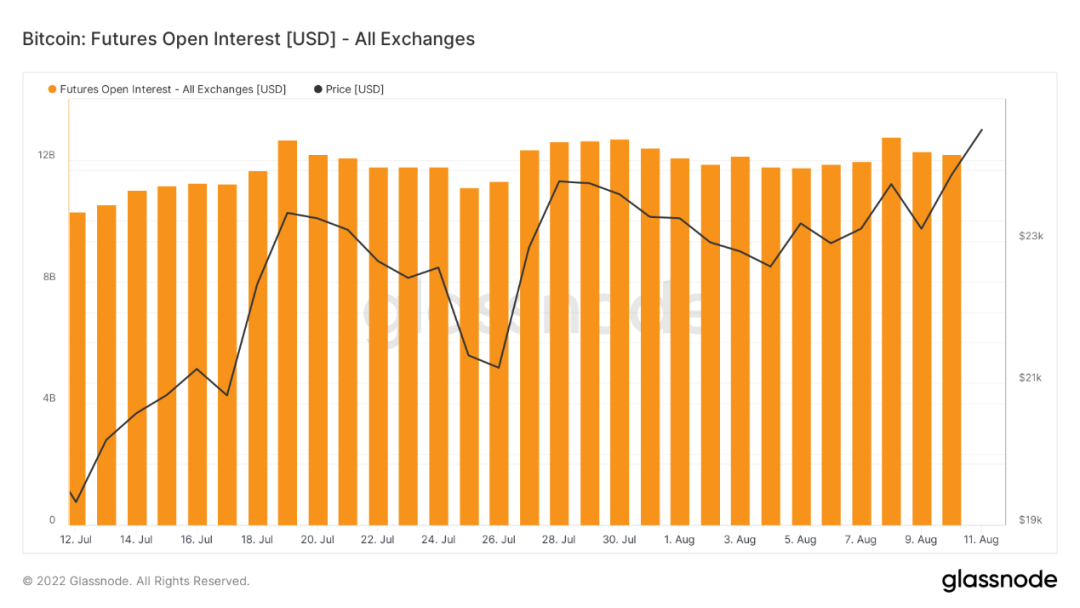

合约持仓量:本周持仓量小幅回落,变动不大。ETH合约量接近新高,历史上首次超过BTC。越来越多的交易者购买ETH现货,然后合约做空套保以获得分叉空投,套利交易变得拥挤。

BTC走势分析

本周BTC维持在反弹趋势线上方。目前大量山寨币市值降低情况下,资金更加偏重在BTC和ETH上。美股已经回到今年4-5月水平,BTC当时波动区间是34000-48000,合理价格约在40000左右。考虑LUNA崩盘、特斯拉减持等多项实质利空影响,打个八折约是30000。技术面上参考前期筹码密集区,上涨阻力位在28000-30000左右。

板块涨跌幅Top 100

本周BTC大涨7%,市场强劲反弹。市场押注ETH2.0合并成功,开发人员预测的日期为9月19日。自2022年6月低点以来,ETH/BTC汇率上涨了50%。大量早期DeFi龙头项目再次开始上涨,由UNI,AAVE,SNX等领导,时间维度与ETH2.0合并背景很好地保持一致。公链赛道(NEAR, AVAX, SOL, DOT)也跟随ETH反弹。或许要等BTC真正站稳25000,才会出现山寨币普涨行情。

市场数据

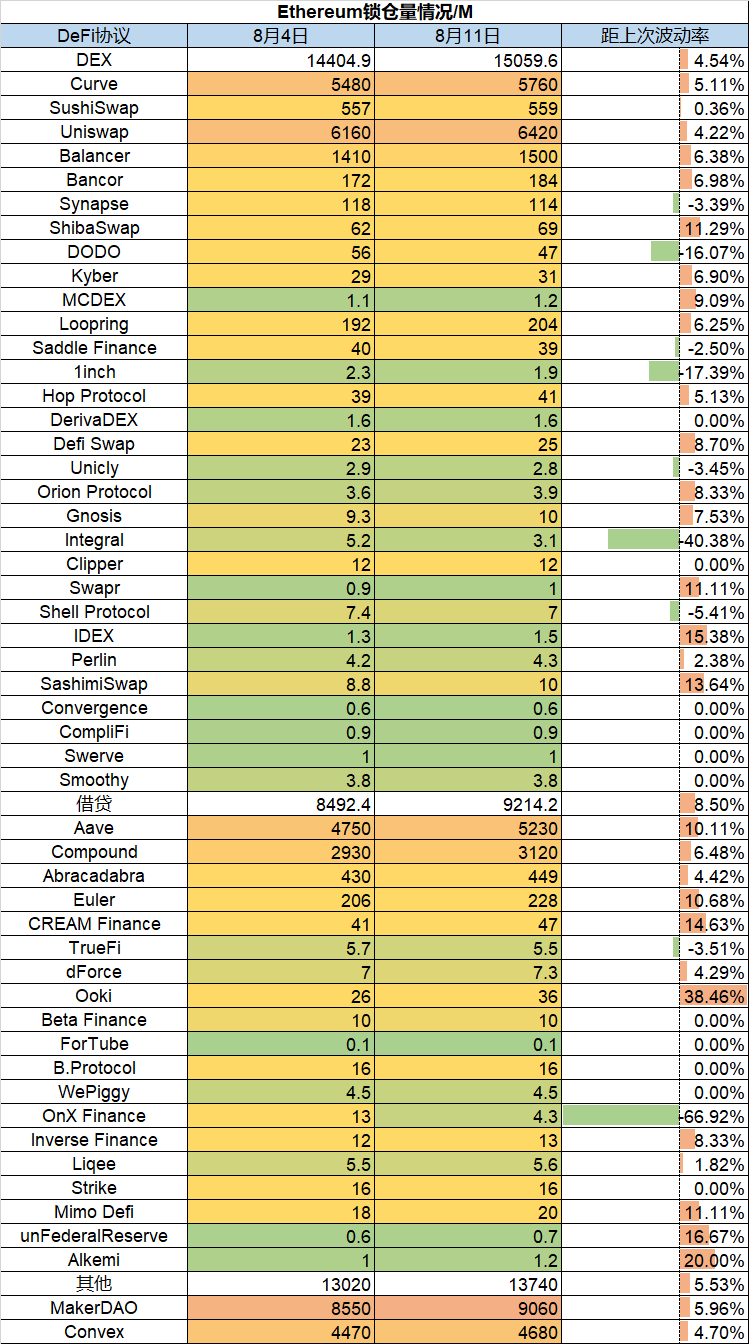

公链总锁仓量情况

本周整体TVL上升1.6B,上升幅度达2.3%,同期BTC上涨3.3%,ETH上涨达10.97%,上涨远不及主流代币涨幅。

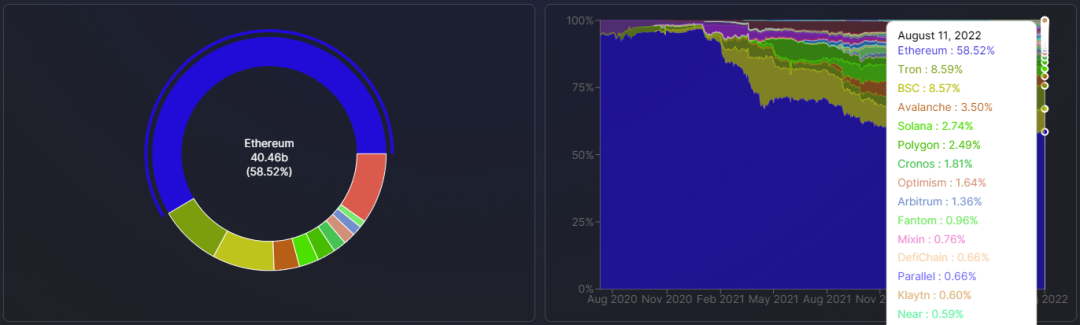

各公链TVL占比情况

虽然同期ETH行情大涨,但占比缺没有出现增长,反而下跌了0.46%,而Optimism链继续出现增长,打到1.64%,目前排在第八位,其余各链占比变化较小。

各链协议锁仓量情况

1)ETH锁仓量情况

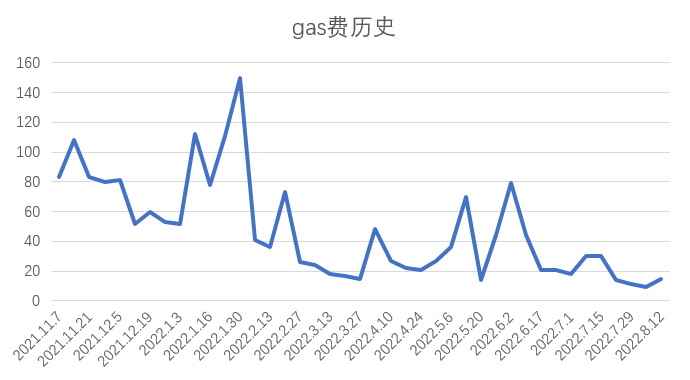

ETH Gas fee历史情况

当前链上转账费用约为$0.72,Uniswap交易费用约为$2.44,Opensea的交易费用约为$0.95,本周Gas Price出现触底反弹,有逐渐上升的趋势,高点于8月10日,当日Gas Price均值为27.

NFT市场数据变化

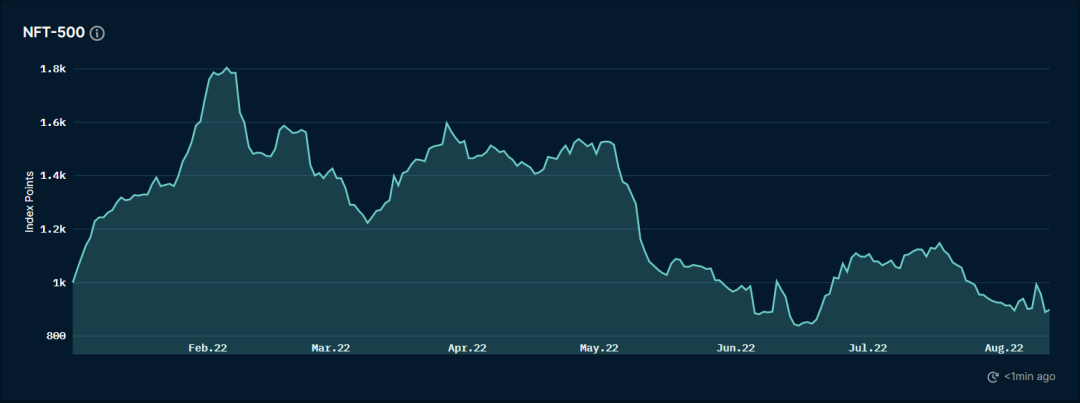

NFT指数市值

NFT市场交易概览

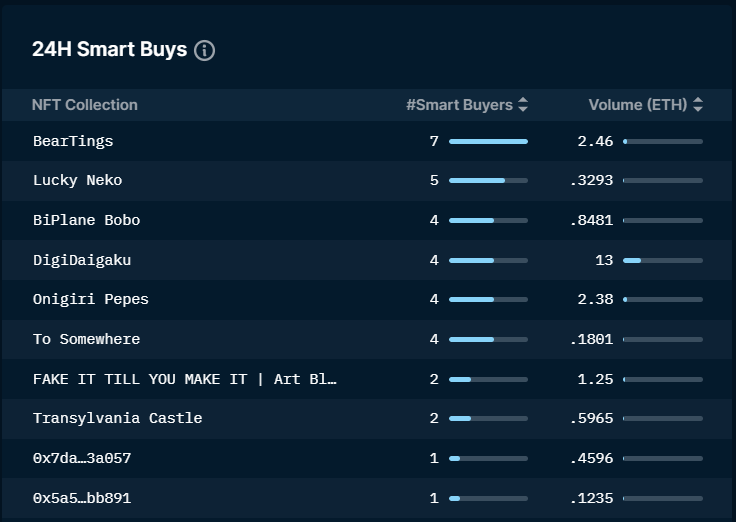

NFT“聪明的钱”购买排序

NFT市场活跃度依旧较低,短期值得关注的项目,一个是NFTiff,由Tiffany & Co公司发行的250个艺术品NFT,在本周出现较高交易量增长。另一个是10KTF发行的Battle.town,10KTF是之前发行以无聊猿为主元素的潮鞋发行商,其可以支持将一部分蓝筹NFT项目做为模板,发行对应的子潮品,本次发行的Battle.town是基于游戏元宇宙背景下,一套以战斗装备为基础的盲盒NFT,近期交易较为活跃。