The Aptos Foundation presents a summary version of the Aptos protocol tokenomics below. A more comprehensive explanation of Aptos tokenomics and values is coming soon.

Initial Supply

Mainnet was launched on October 12, 2022. The initial total supply of Aptos tokens (APT) at mainnet was 1 billion tokens. APT will have 8 digits of precision as part of the fraction where the minimal unit is called an Octa.

Category % of Initial Token Distribution Initial Tokens

Community 51.02% 510,217,359.767

Core Contributors 19.00% 190,000,000.000

Foundation 16.50% 165,000,000.000

Investors 13.48% 134,782,640.233

Distribution Schedule for the Community and the Aptos Foundation

This pool of tokens is designated for ecosystem-related items, such as grants, incentives, and other community growth initiatives. Some of these tokens have already been allocated to projects building on the Aptos protocol and will be granted upon the completion of certain milestones. A majority of these tokens (410,217,359.767) are held by the Aptos Foundation, and a smaller portion (100,000,000) are held by Aptos Labs. These tokens are anticipated to be distributed over a ten-year period:

125,000,000 APT available initially to support ecosystem projects, grants, and other community growth initiatives now and in the future for the Community category

5,000,000 APT available initially to support the Aptos Foundation initiatives for the Foundation category

1/120 of the remaining tokens for the community and the Foundation are anticipated to unlock each month for the next 10 years

Distribution Schedule for Core Contributors and Investors

All investors and current core contributors are subject to a 4-year lock-up schedule from mainnet launch that unlocks according to the following schedule:

No APT available for the first twelve months

3/48ths of such tokens unlock on the 13th month after mainnet launch and each month thereafter up to and including the 18th month

1/48th of the tokens unlock each month thereafter beginning on the 19th month after mainnet launch so that all such tokens are unlocked on the four-year anniversary of mainnet launch

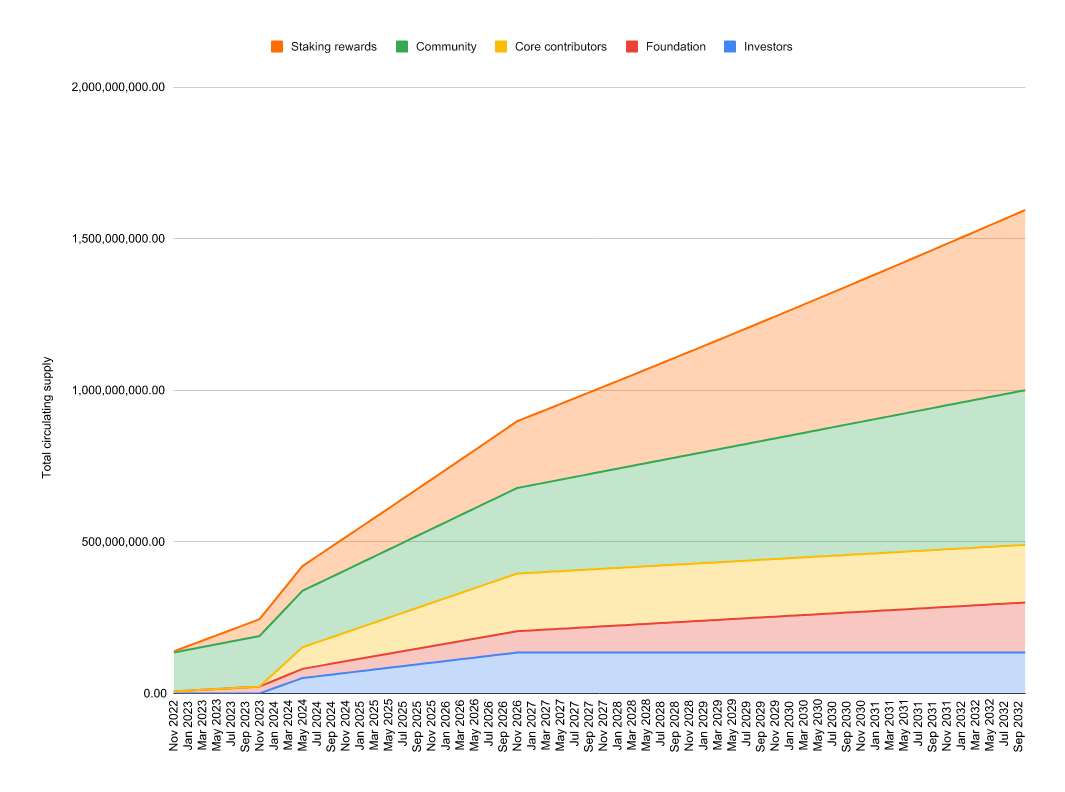

Estimated Token Supply Schedule

Today, more than 82% of the tokens on the network are staked across all categories, and a majority of these are currently locked in accordance with the distribution schedule above and not available for release.

Note: Both unlocked (i.e. tokens that are available for distribution) and locked (i.e. not available for distribution) tokens can be staked

Anticipated Total Circulating Token Supply for the next 10 years subject to network performance and staking assumptions.

Anticipated Token Supply Changes

Token holders who stake their tokens to a validator operator for purposes of securing the network and achieving consensus may receive staking rewards

Staking rewards are split between validator operators and stakers and are not subject to restrictions on distribution

Currently, the maximum reward rate starts at 7% annually and is evaluated at every epoch

The maximum reward rate declines by 1.5% annually until a lower bound of 3.25% annually

These rewards increase the total supply of the Aptos network and are dependent on the staked amount and validator performance

Transaction fees are currently burned, although this may be revisited in the future with on-chain governance voting

All rewards and reward mechanisms are also modifiable via on-chain governance