Author: Rasheed Saleuddin

Compiled by: Deep Tide TechFlow

Deep Tide Guide: Last summer, the frenzy for Digital Asset Treasury (DAT) companies ended in a spectacular crash, with early investors losing up to 99%. One year later, the same scam is back under a new guise—this time packaged with SpaceX stock and the HYPE token. The cycle of greed and fear never ends, as retail investors continue to foot the bill for insiders' feasts.

Last Tuesday, the Triller Group (who?) announced it would become the world's first SpaceX treasury company. That is, it will use newly raised funds to buy and hold SpaceX stock. That's its business model: holding SpaceX. This news sent Triller's market cap soaring from $15 million to $63 million.

Matt Levine noticed this, and it caught my attention too. This announcement closely followed the rebranding of an "established" treasury company, LGHL—they previously bought crypto assets like SOL and SUI, and now they're buying the HYPE token. Because, well, hype.

We've seen this movie before. Just last summer. The ending was so bad you'd think it would never happen again. Worse, it was blatantly one of the most obvious scams, one I could see coming from a mile away.

The sequel is already showing. Because global speculators need their "spiritual opium," and pump-and-dump insiders are happy to supply it. Supply meets demand. When will they ever learn?

The Pioneer Made the Wrong Headlines

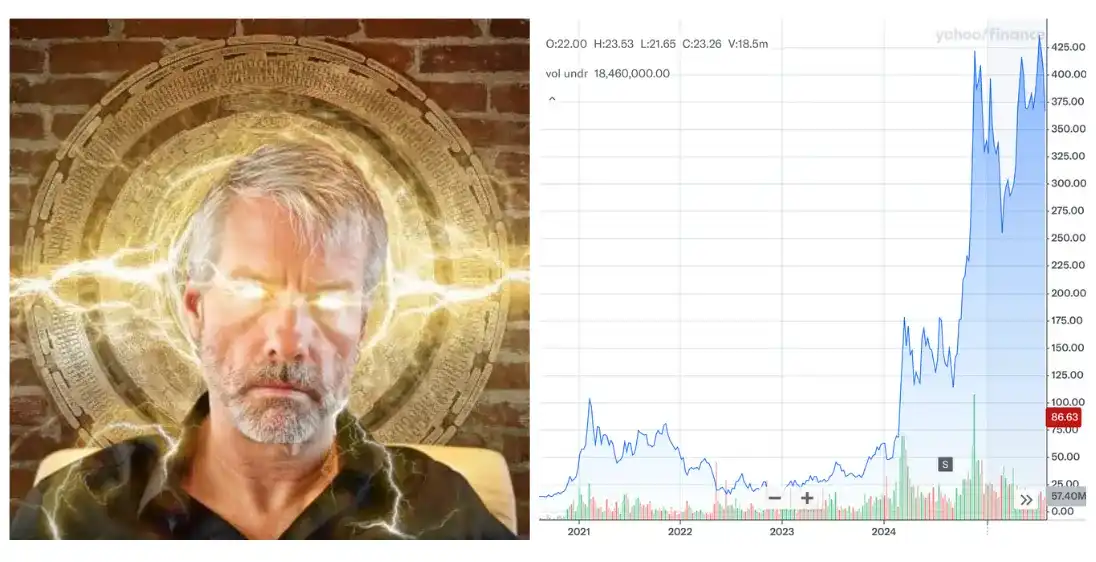

MicroStrategy/Strategy (MSTR) CEO Michael Saylor pioneered the concept of "Bitcoin yield." Through alchemy, a bitcoin held by a corporation somehow became worth more than a bitcoin held by someone not named Michael Saylor.

For a long and awkward period, the market agreed with him.

Not long ago, MSTR traded at 200% of the value of the Bitcoin on its balance sheet (Net Asset Value, NAV). You paid two dollars for one dollar's worth of Bitcoin. The sage Saylor, hailed as Satoshi Nakamoto reincarnated, frantically bought up all the Bitcoin he could, issuing expensive stock and even more complex financial instruments to new believers. The stock price looked like it would rise to infinity.

The Copycats

The premium on Strategy's stock attracted competitors, just as premiums always do. I documented this last May:

SPACs became Bitcoin buyers. Unprofitable operating companies ditched their original businesses to raise funds and buy BTC, ETH, or even more obscure crypto assets.

Spoiler alert: None performed as well as MSTR. And MSTR itself wasn't exactly a success story.

One year later, here's the situation:

Strategy (MSTR): Down 79% from its peak. This is the combined result of BTC falling 45% over the same period and the NAV premium compressing from 2x to 1x. Leverage magnifies gains and losses—that's how leverage works.

TwentyOne (XXI): Reached 5x NAV at its peak. Credit where it's due, it still trades above 1x NAV, though it's down 85% from its peak. Even some insiders got caught.

Metaplanet: Down 87% from a year ago, and down another 50% since the crash.

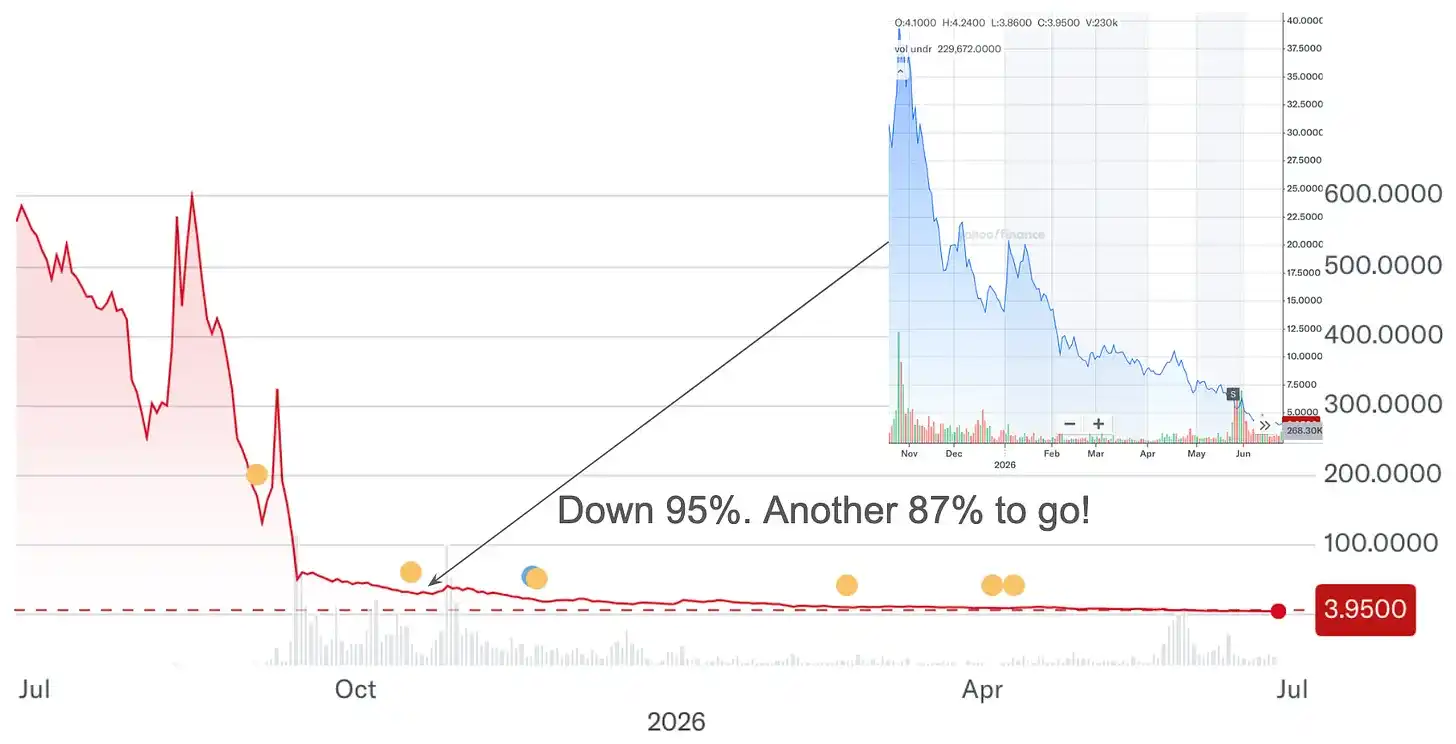

Nakamoto (NAKA) (formerly KindlyMD): Down 87% since October, after already falling 95% from its all-time high. If you put $100,000 into this stock a year ago, you'd have $650 left.

From $100,000 to $650. Enough for a (very) nice dinner. Speculators who "bought the dip," thinking "how much lower can it go," didn't fare much better than the original believers. The answer to "how much lower can it go" is often "quite a bit."

Why This Was Bound to Happen

Bitcoin ETFs exist. They charge only 9 basis points. Bitcoin itself exists. You can hold it yourself. There is no structural reason for DATs to trade at a premium—only greater fool theory, momentum trading, and a particular brand of financial nihilism where retail speculators, convinced the system is rigged, conclude they might as well play the rigged game with maximum aggression.

If you believe the traditional investment system doesn't work for you, the expected value of speculation looks different. FOMO plus dopamine plus gamification plus GameStop: Each alone is a manageable psychological condition. Together, they become a significant part of today's market structure.

Needless to say, insiders are always incentivized to meet the demand. They profit no matter which way the stock moves—another thing worth remembering.

About Tulips

The sad conclusion here is that no one cares when the market is irrational. This is a shame because the DAT crash is a perfect fable for the consequences of fear and greed. It should be a central case study for all bubble reporting. This is the Tulip Mania, only real and recent.

The 1637 dialogue "Waermondt and Gaergoedt" depicts two fictional Dutch weavers watching tulip prices collapse in real-time. One passage, spanning nearly four centuries, reads as if it were written last month:

"Things had gotten to the point that what used to be thrown into the dung heap to kill weeds in baskets was now selling for high prices. I thought I was rich enough. I thought I'd never have to weave again."

Polishing turds didn't work back then either. A flower that sold for 22 ducats in 1637 was trading at 400 ducats at its peak the year before. Then the liquidation came:

"I wish this country had never had flowers!"

I wonder how many retail investors, like those who turned an initial $100,000 into $650, wish they had never heard of Metaplanet, Nakamoto, or the phrase "Bitcoin yield."

One More Thing

I hold some Bitcoin. My venture fund holds crypto investments. I'm not against digital assets. I'm against this specific frenzy of packaging digital assets into companies, charging privileged fees, issuing debt for leverage, and then marketing the result as financial innovation.

I thought this frenzy was killed by the 2025 DAT crash. But the Golden Age of scams continues (with thanks to Shrubstack).

History repeats itself. Always. The pump-and-dump isn't a bug in the system; for those operating it, it's the product. Speculators provide the demand, insiders provide the product. Until we get the mother of all tulip crashes.

The pump-and-dump is the end in itself.