Deep Tide Guide: This edition of a16z's Chart Weekly covers four topics, each worthy of a standalone article: the Jevons Effect triggered by falling AI costs, the true scale of tech giants' capital expenditures, Kalshi prediction markets outperforming professional forecasting agencies, and the comprehensive postponement of life milestones among 30-year-olds in the US. With solid data sources and a calm, restrained perspective, it serves as a high-quality reference for understanding the intersection of current tech and macro trends.

DExit......Real Trend or Illusion?

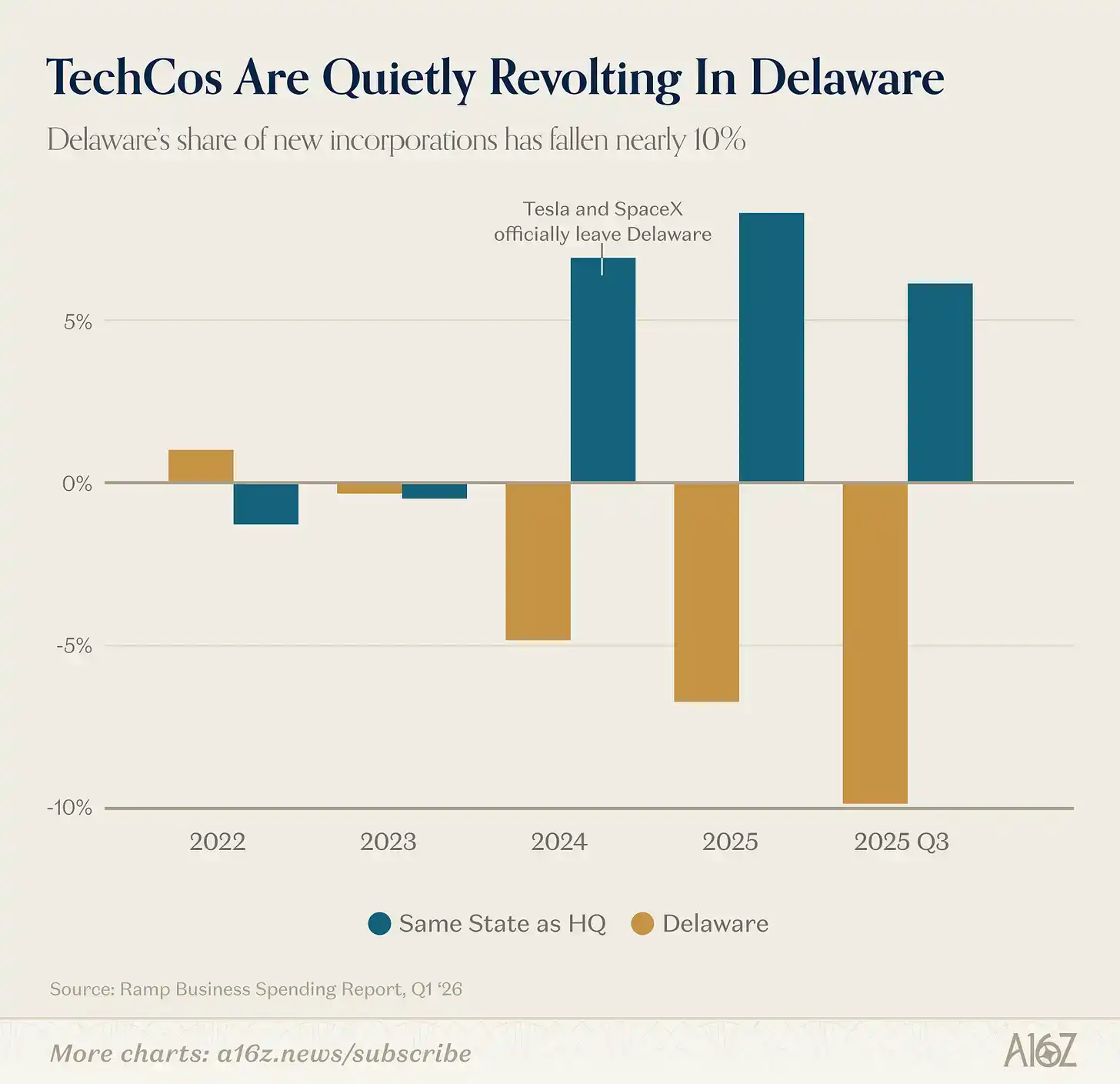

Delaware remains the preferred state for US corporate registration, but this status is quietly loosening:

According to Ramp's data, Delaware's share of new company registrations has been declining since 2023, with a drop of about 10% in Q3 2025.

History doesn't repeat itself exactly, but it often rhymes......maybe.

Delaware wasn't always the holy land for corporate registration.

About a century ago, Delaware replaced New Jersey—the original "Mother of Trusts"—as the preferred state for incorporation. New Jersey lost its edge because then-Governor Woodrow Wilson tried to curb "corporate abuses," severely worsening the state's business environment. Delaware's corporate law was modeled on pre-Wilson era New Jersey law and was happy to welcome fleeing businesses. It then spent nearly 100 years, alongside the Delaware Court of Chancery, building a reputation as a mature and fair venue for resolving disputes between companies and investors.

However, what took a century to build began to shake in just a few years. Rightly or wrongly, the Delaware Court of Chancery has recently taken a more lenient stance on shareholder lawsuits (including, but not limited to, several high-profile cases like Tesla), and companies have genuinely started moving their registrations elsewhere. Goodnight, and good luck, Delaware.

This is at least the mainstream narrative, but other data shows a more complex picture.

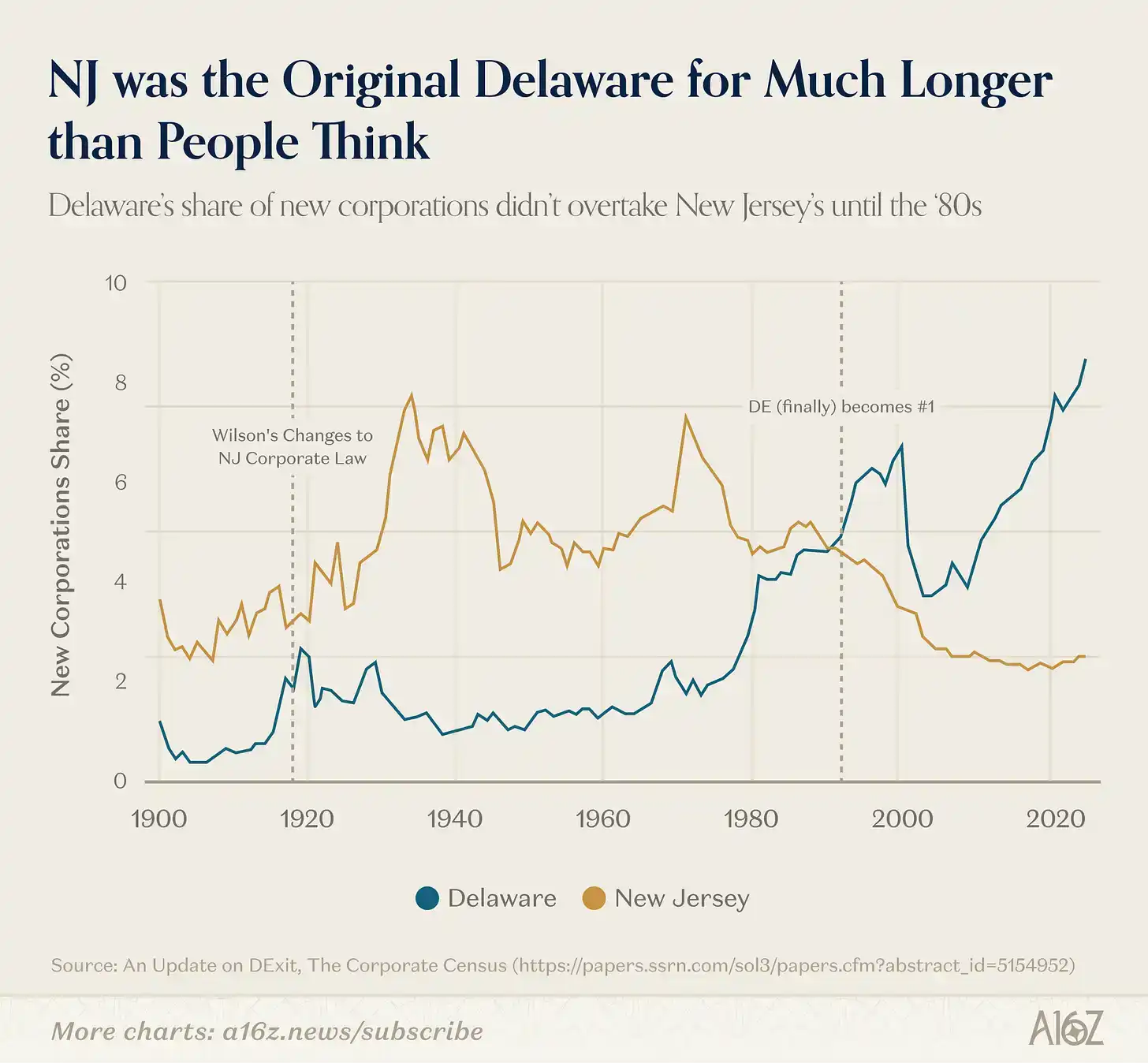

First, even Delaware's founding myth isn't entirely accurate.

It wasn't until the 1980s (about 60 years after Governor Wilson's term) that Delaware truly surpassed New Jersey to become the number one state for US corporate registrations:

New Jersey's dominance lasted much longer than the mainstream narrative suggests. The catalyst for Delaware's eventual overtaking was likely its passage of a series of laws related to director liability, which were particularly favored by public companies, coupled with self-reinforcing network effects that created their own inertia.

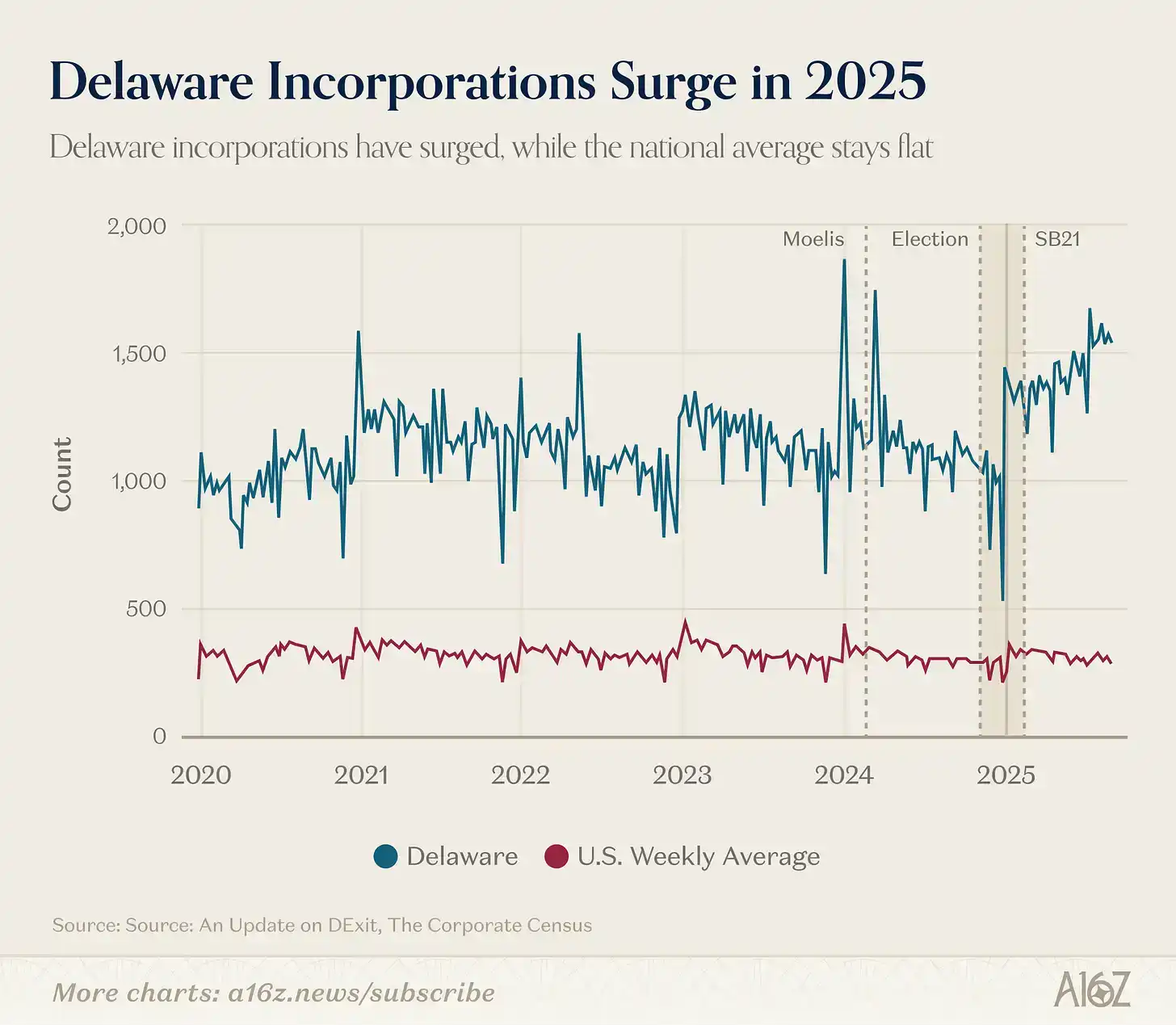

Second, regardless of what's happening with high-profile public companies (and the companies in Ramp's data), Delaware as a whole still seems to be doing well, even more than well:

According to data published by the Harvard Law School Forum on Corporate Governance, Delaware's share of the total number of US businesses actually grew significantly from late 2024 into 2025.

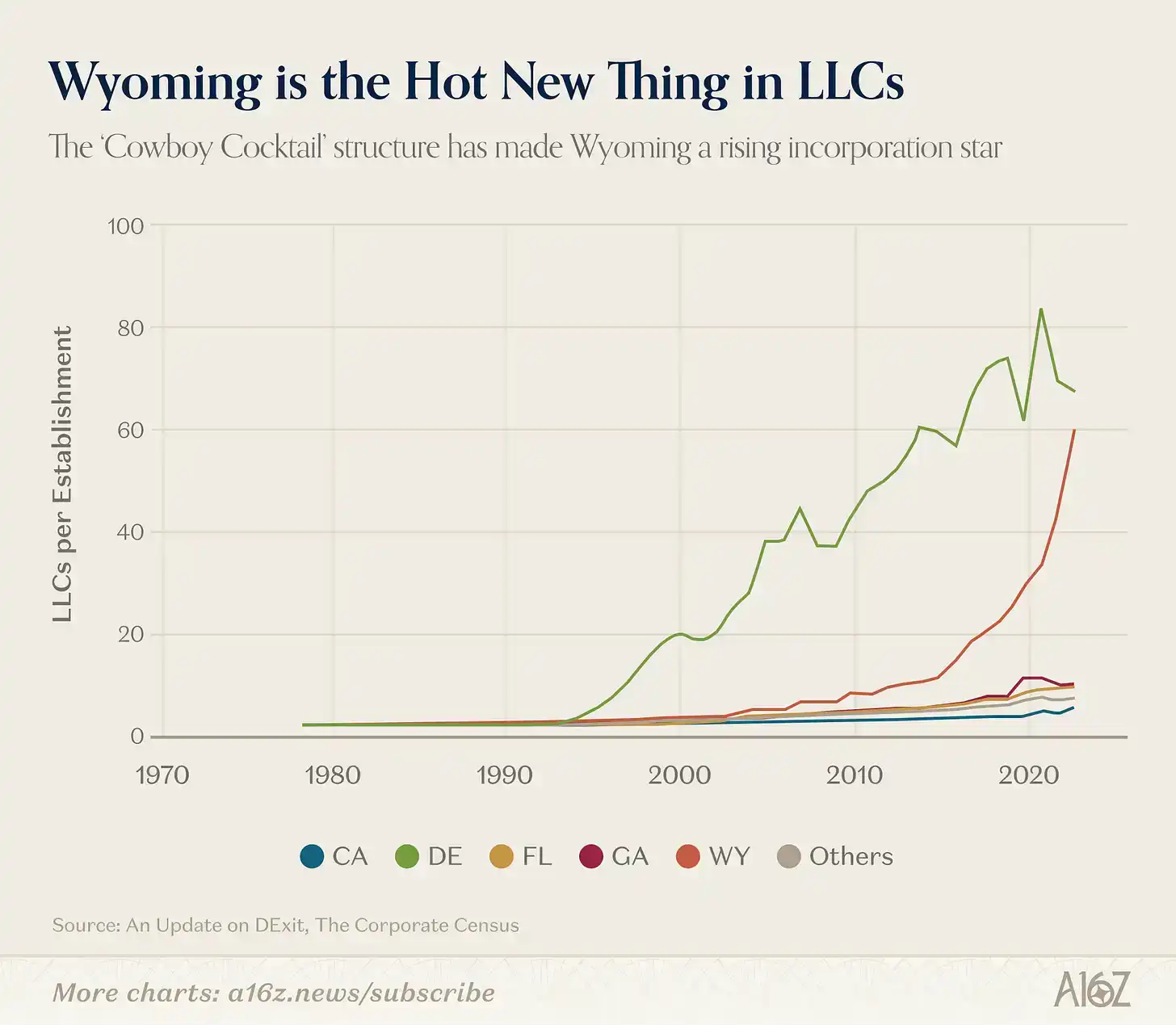

In fact, if you're looking for a clear case of "DExit," it's probably this one, and it has nothing to do with Tesla, but rather a specific type of company structure:

Wyoming LLCs began to surge around 2015.

Why? This is likely related to specific asset protection and privacy provisions in Wyoming's LLC law, which the state itself promotes as a "cowboy cocktail."

In short, the point here isn't that DExit isn't happening (because at least some data suggests it is—even if it's just a few high-profile companies moving out, it's significant), but the reality is certainly more complex than the mainstream narrative presents.

The reality is that Delaware still enjoys the advantage of being the default option, not to mention all the network effects tied to it, and these are very hard to shake.

We published an earlier version of this chart before, but as more data comes in, the effect becomes more striking.

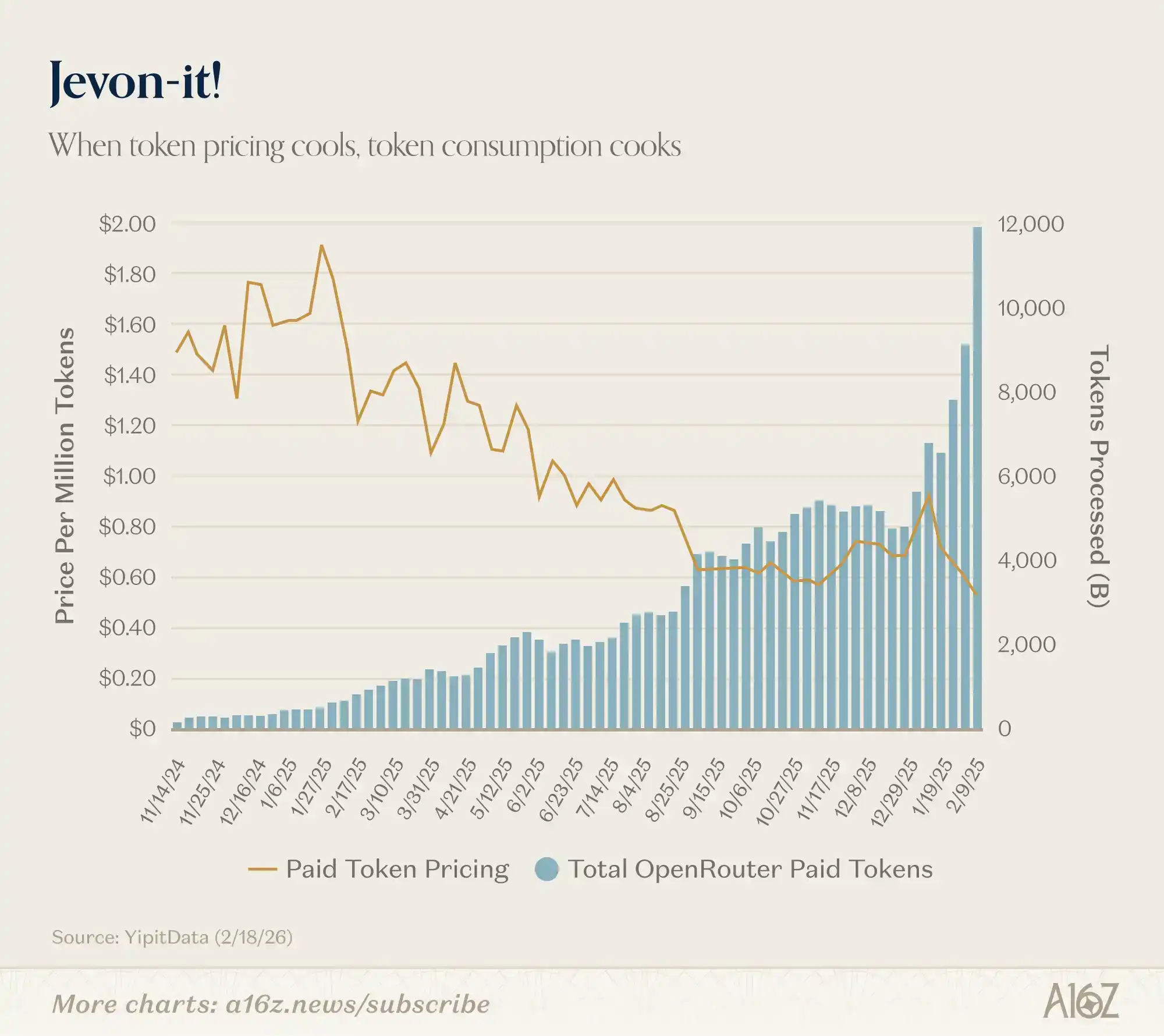

Token costs fall, Token consumption rises:

Since the beginning of this year, paid Token pricing has dropped from about 90 cents per million Tokens to 50 cents, while the number of Tokens processed has nearly doubled, from about 6,000 to 12,000.

This is a classic Jevons effect. The cheaper AI gets, the more AI we use. Delightful.

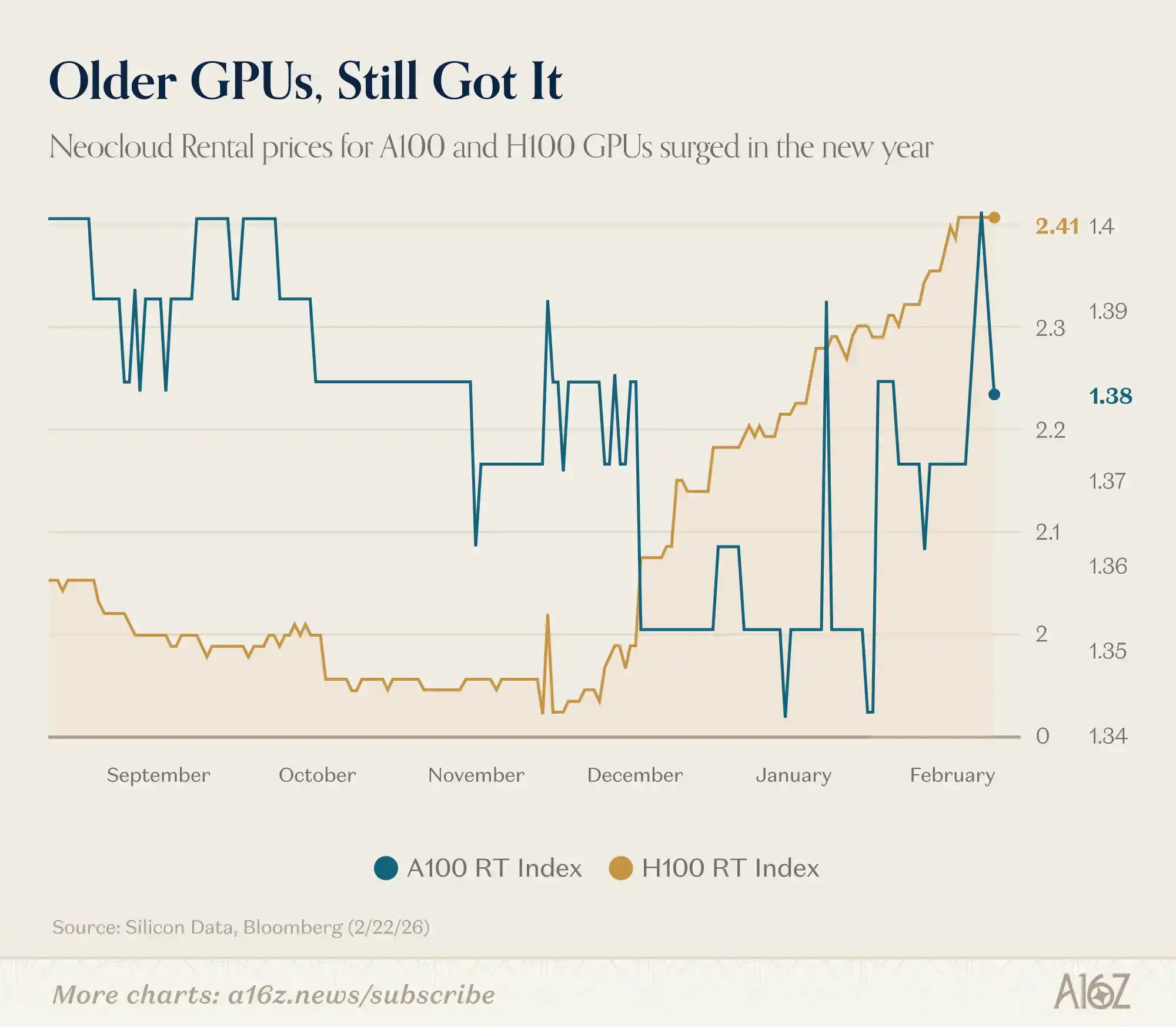

Remember when people said that when newer, better GPUs hit the market, the old ones would become worthless?

That doesn't seem to be the case either:

According to Silicon Data, rental prices for NVIDIA's H100 and A100 have both increased this year.

The market is far from showing signs of a compute oversupply; instead, it seems we haven't even scratched the surface of existing demand.

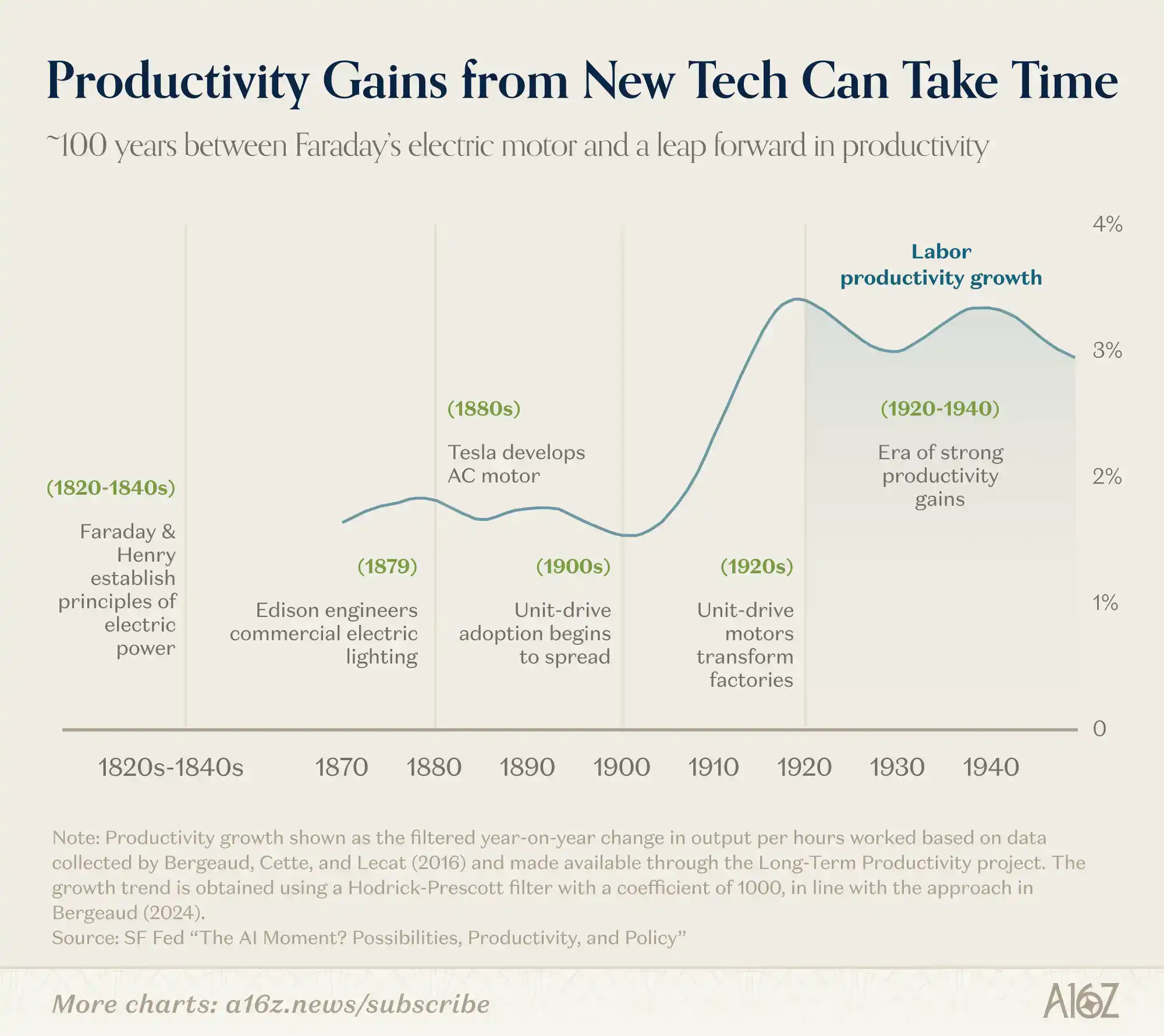

This comparison isn't a perfect analogy, but if history is any guide, it might take us a while longer to truly "see" what an AI-driven "economy" actually looks like:

From the initial discussions of electric current by Faraday and Henry to the true explosion of industrial productivity in the first half of the 20th century, it took about 100 years.

Technology iteration cycles have indeed accelerated since the 1820s, but the variables involved in a platform-level shift remain extremely numerous.

Roy Amara famously said: "We tend to overestimate the effect of a technology in the short run and underestimate the effect in the long run."

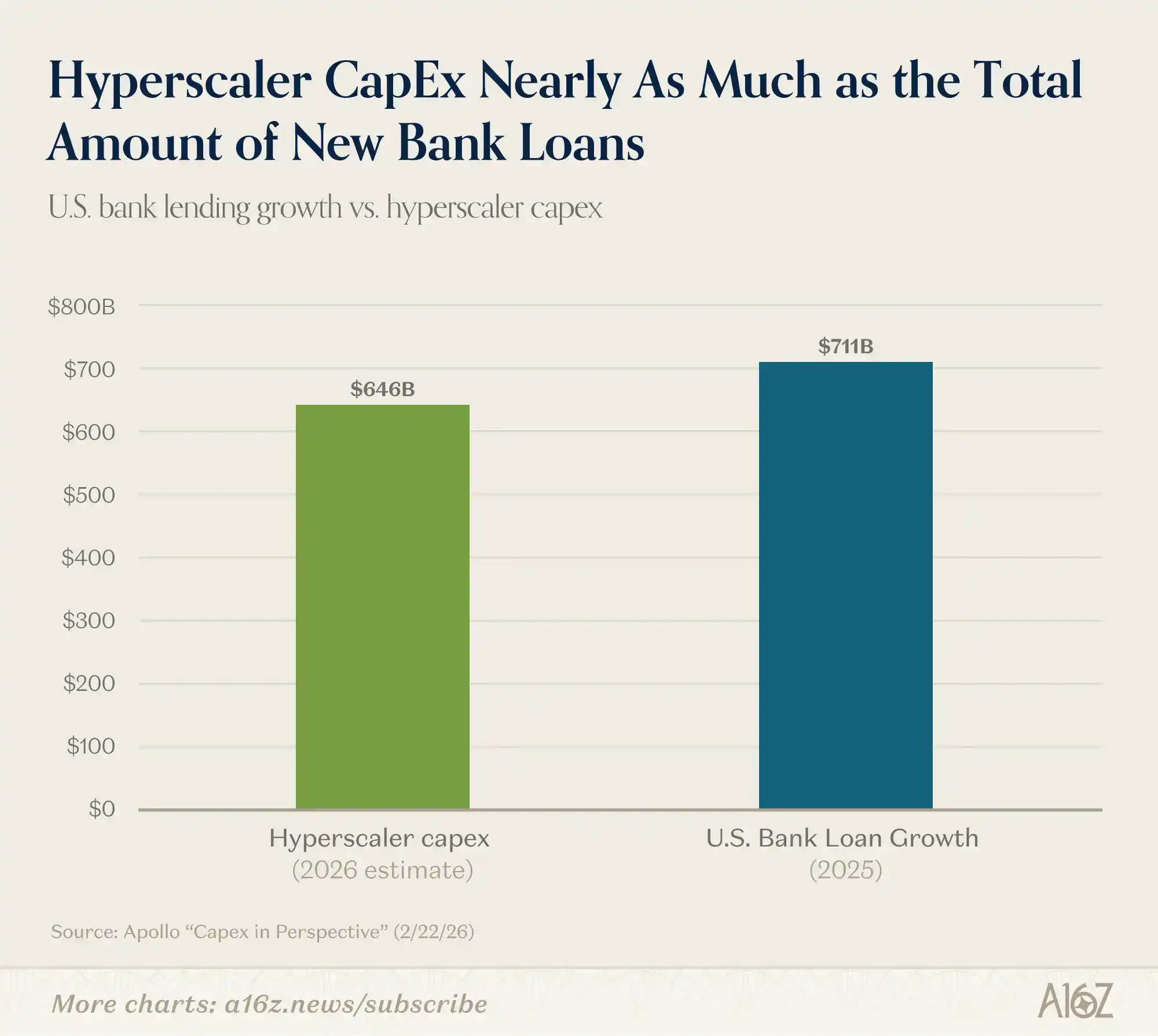

Capital Expenditure, Put on the Axis

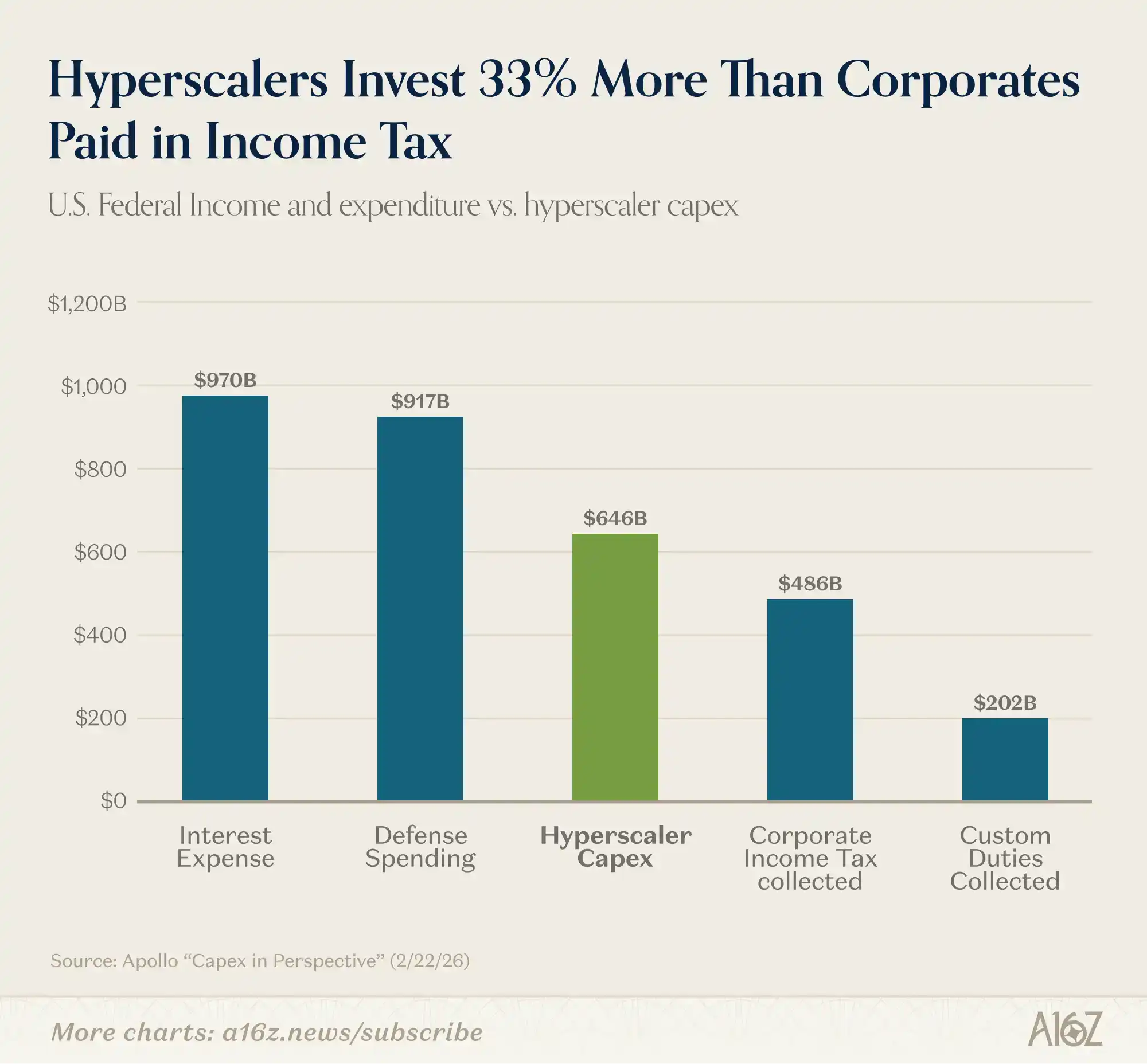

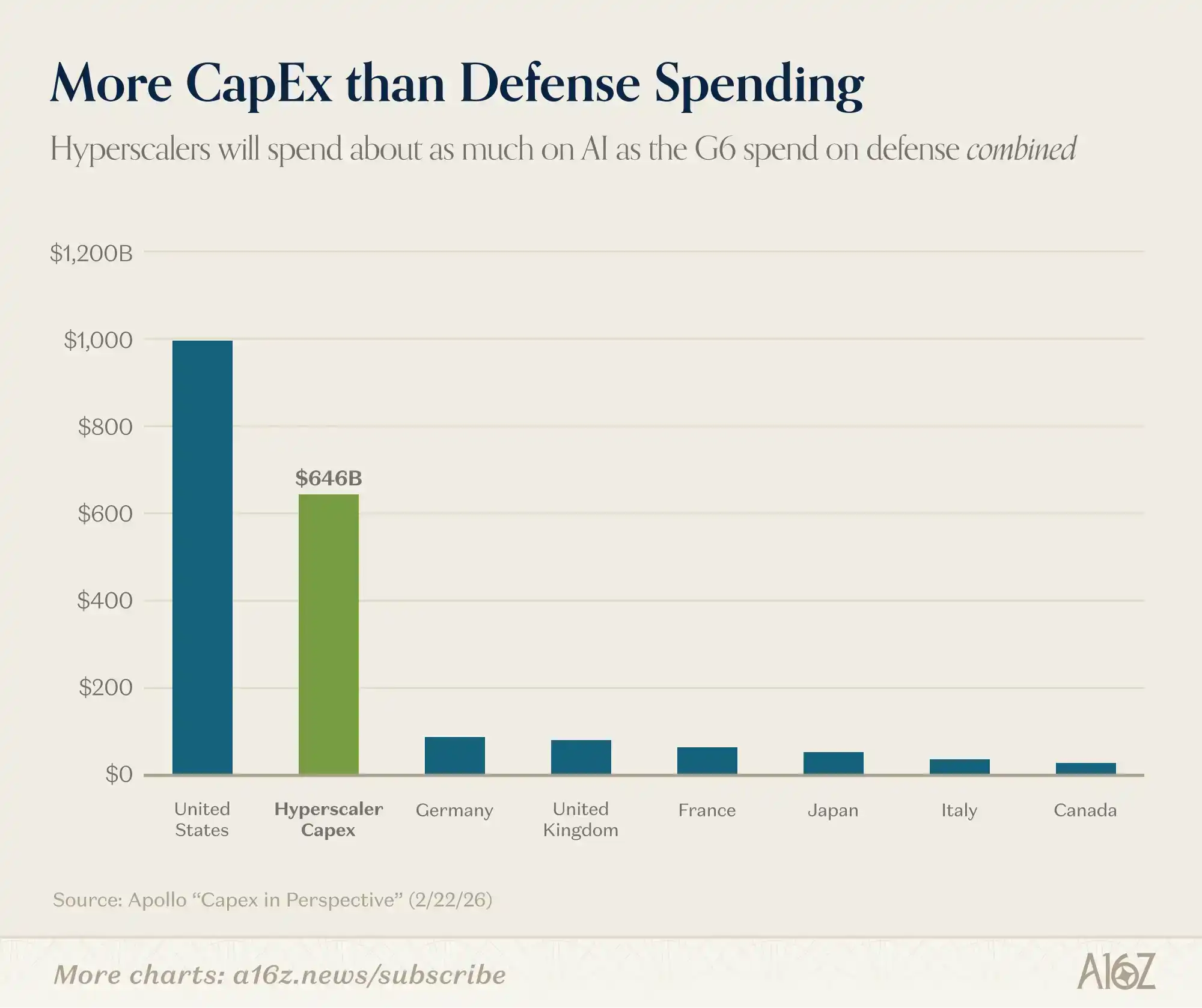

Here's a set of data that will never gets old: AI capital expenditure is huge.

Consider these comparisons:

2026 AI capex is projected to be close to the total net new lending by all US banks in 2025:

Capex is about 33% higher than total US corporate income tax revenue and about 3 times the total tariff revenue:

Capex is about 6 times the total military budget of any non-US G7 member country:

So, yes, capital expenditure is really huge.

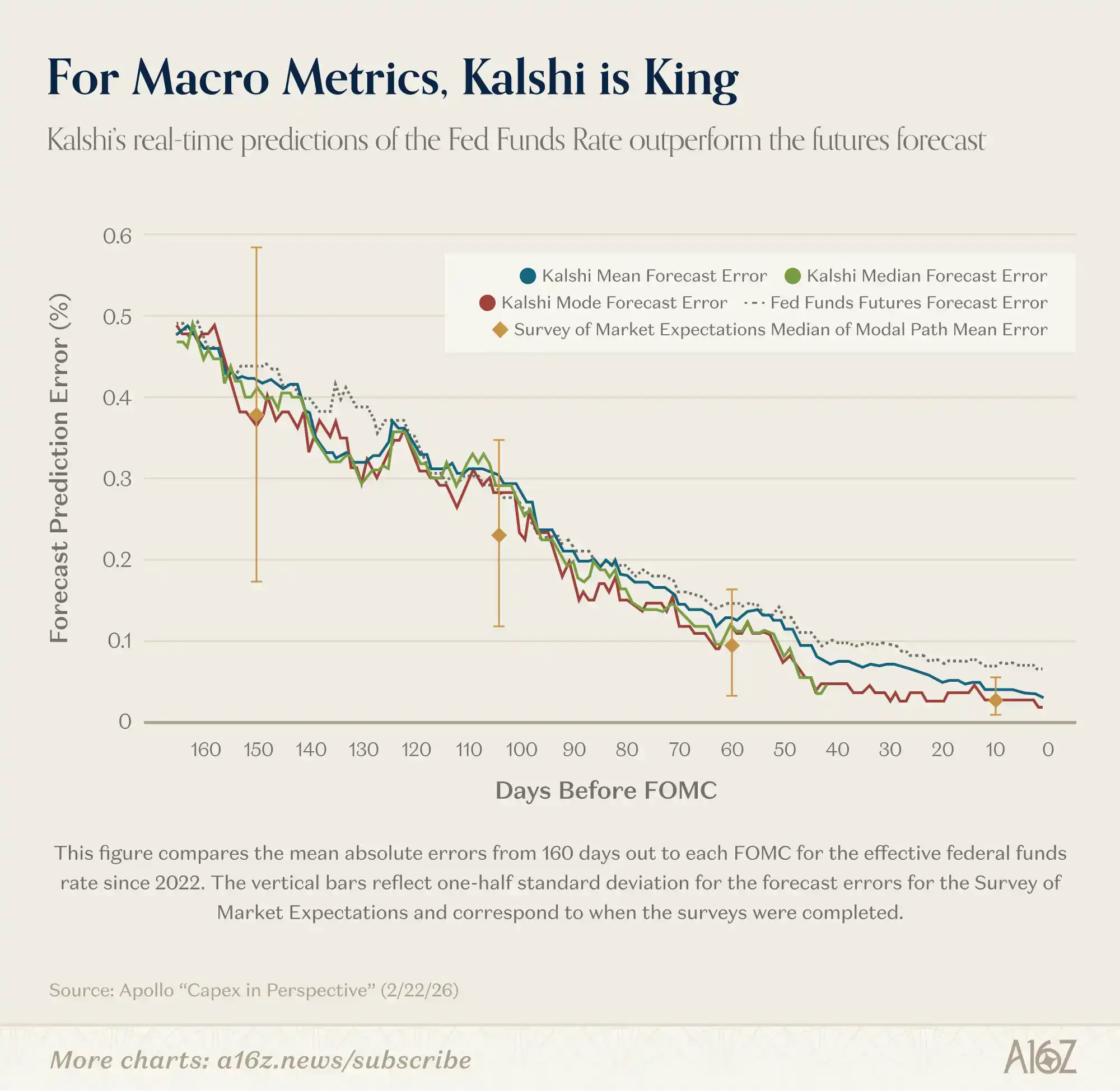

Kalshi Moves into Macro Forecasting

Federal Reserve researchers think prediction markets are pretty good.

At least on one metric, Kalshi's predictions for the federal funds rate have already outperformed professional forecasting agencies:

For predictions of the federal funds rate 150 days later (i.e., after 3 FOMC meetings), Kalshi's mean absolute error is very close to that of professional forecasters. But unlike surveys that provide only a snapshot of the modal path every six weeks, Kalshi provides a continuously updated full probability distribution......We find that Kalshi's median and mode predictions have a perfect track record on the day before FOMC meetings, which is a statistically significant improvement over federal funds futures predictions.

In other words, while all predictors start out similar, Kalshi's continuously updated predictions optimize over time, eventually achieving a perfect prediction record the day before the rate is officially announced. Furthermore, Kalshi's performance is also better than predictions from futures markets.

Kalshi's advantage extends beyond the federal funds rate. As the Fed researchers point out, since there are no other options markets for macro indicators like inflation, growth, and unemployment, Kalshi is the only place that provides a "high-frequency, continuously updated, probability distribution-rich 'baseline' reflecting 'crowd' judgments on the direction of these economic indicators.

Sounds pretty important.

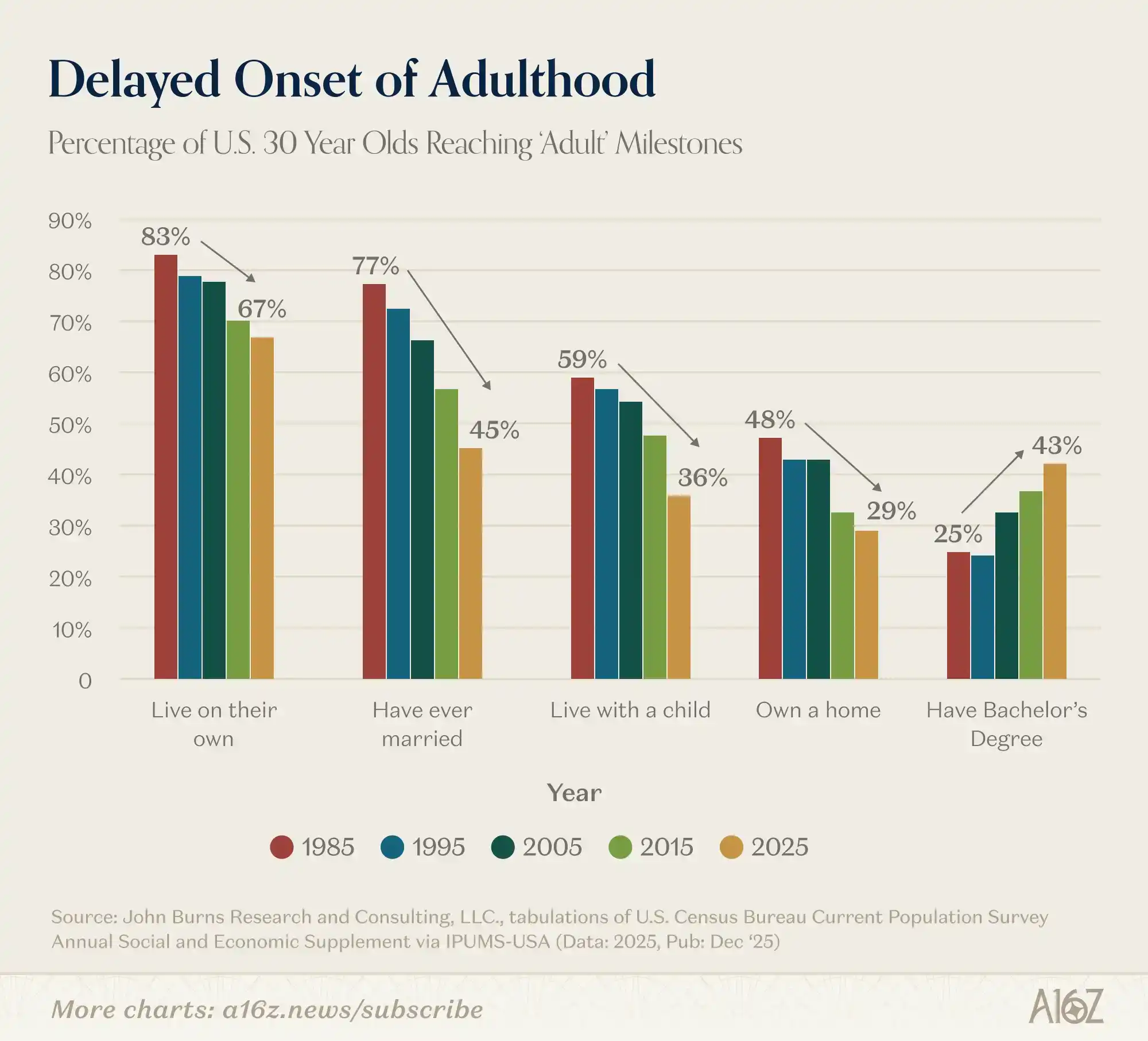

The Delay of Adulthood

Here is a thought-provoking chart, with (a little) commentary:

The proportion of 30-year-olds achieving major life milestones has been declining quite steeply since at least the 1980s.

Fewer and fewer 30-year-olds:

Live independently;

Have ever been married;

Live with children;

Own their home.

The only exception is college enrollment—the proportion of 30-year-olds with a bachelor's degree has almost doubled since 1995.

So, is college worth it?

Milestones? More like milestones around the neck, right?!

Maybe, maybe not, but a sense of "buyer's remorse" seems to be in the air.