Strategy is rewriting its own business model. On July 6, the world's largest corporate Bitcoin holder disclosed that it sold 3,588 Bitcoins between June 29 and July 5, raising approximately $216 million to pay dividends on its preferred shares. This not only marks the largest Bitcoin sale in the company's history but also its third sale since launching its Bitcoin strategy in 2020.

This sale signals an important shift: Bitcoin is gradually transitioning from a "buy and never sell" strategic reserve for Strategy to an asset that can be used for liquidity management.

According to Bloomberg, the company recently expanded its authorization to allow Bitcoin sales to supplement liquidity when new stock financing becomes less attractive. This adjustment comes as both Bitcoin and Strategy's stock price face pressure. Over the past year, MSTR has fallen about 75%, and Bitcoin has declined over 45% from its all-time high.

Following the news, Strategy's stock price dropped over 5% intraday, and Bitcoin fell to around $61,800, below the company's average holding cost of approximately $75,700.

'Never Selling Bitcoin' Begins to Soften

Strategy long regarded "never selling Bitcoin" as the cornerstone of its business model, but this commitment has shown clear signs of weakening.

At the end of May this year, the company broke its own rule for the first time, selling 32 Bitcoins for approximately $2.5 million to pay preferred stock dividends. At the time, the company emphasized that this move was solely to fulfill its commitment to preferred stock investors and did not represent a strategic shift.

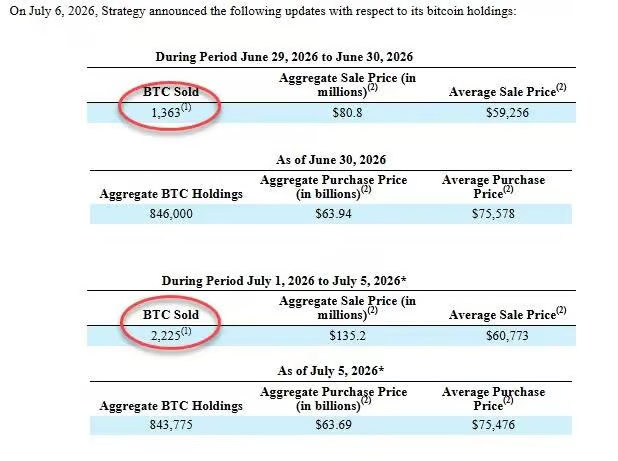

However, the scale of the latest sale has expanded significantly to 3,588 Bitcoins, about one hundred times the May sale. According to the company's disclosure, 1,363 of these were sold at an average price of about $59,300 each, and the remaining 2,225 were sold at about $60,800 each. This indicates that selling Bitcoin is no longer a one-off symbolic operation but is gradually being integrated into the company's regular financing system.

Under Pressure from $1.5 Billion Annual Dividend, Hundred-Fold Sale Exposes Tight Cash Flow

The proceeds from this sale will be specifically used to pay the Q2 dividends for the four preferred securities (STRF, STRE, STRK, STRD), as well as the June monthly dividend for STRC. Analyst Zach Pandl pointed out that Strategy's annual preferred stock dividend expenditure alone is as high as about $1.5 billion, which its software business cash flow cannot cover by itself. When cash reserves are insufficient, the company can only continue to raise funds or sell Bitcoin.

As of July 5, Strategy holds 843,775 Bitcoins, has cash reserves of $2.55 billion, with an average holding cost of about $75,700. Although the company quickly purchased an additional 1,550 Bitcoins after its first sale at the end of May, and had conducted large-scale purchases of $2.54 billion and $2.0 billion in April and May respectively, this latest sale does not mean a halt to accumulation. Instead, it represents a flexible adjustment within the system.

Strategy's operational logic is becoming increasingly clear: When financing is smooth, continue buying Bitcoin; when financing tightens, sell a small amount of Bitcoin to pay dividends, maintaining the closed-loop of its capital operation system. According to Bloomberg, the company recognized an $8.32 billion digital asset impairment loss in Q2, coinciding with a 14% drop in Bitcoin's price during the period, further intensifying pressure on its cash flow management.