Author: Zhou, ChainCatcher

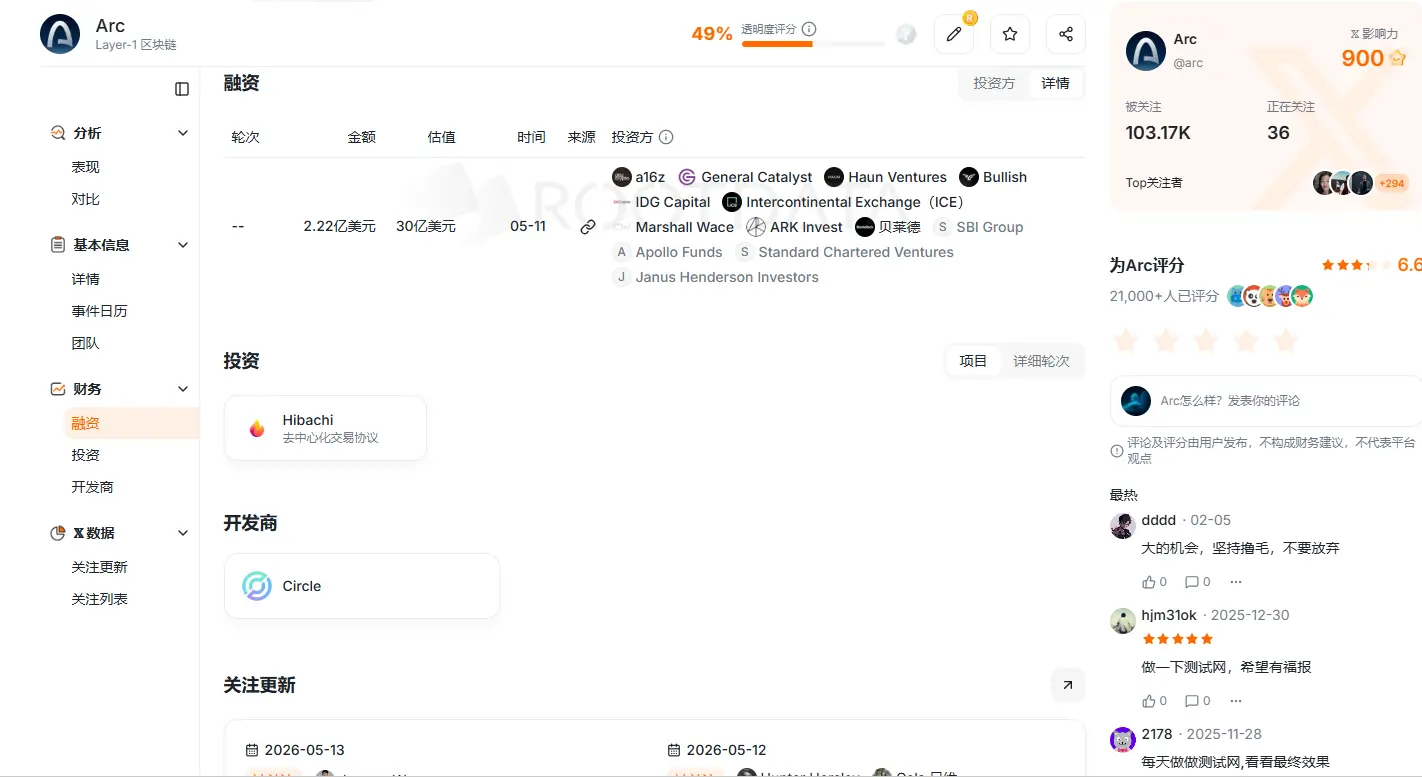

On May 11th, while releasing its Q1 2026 financial report, Circle announced that the ARC native token of its public blockchain Arc had completed a $222 million presale, with a fully diluted valuation of $3 billion for the network.

The round was led by a16z crypto with a $75 million investment, followed by top-tier institutions including BlackRock, Apollo, ICE (parent company of NYSE), SBI Group, SC Ventures, and ARK Invest.

CRCL's stock price surged nearly 16% that day, with its market cap rebounding above $30 billion.

Image source: RootData

This development raises a core market question: Circle is already a public company; if investors are optimistic about its future, why not simply hold CRCL stock? Why issue the ARC token as well? Both are capturing the value of the Arc network. What exactly does each represent?

1. Why Did Circle Build Arc Itself?

Why did Circle choose to invest massive resources into building its own public blockchain instead of continuing to issue and use USDC on Ethereum or Solana?

a16z Crypto explains that as global finance gradually moves on-chain, only a few public blockchains will be able to serve as the "foundational base for an on-chain economic system."

Stablecoin transaction volume approached $9 trillion last year, placing it in the same league as global payment networks like Visa and PayPal. Cross-border payments, B2B settlement, and forex trading are becoming core use cases for stablecoins, which have upgraded to become a core layer of global financial infrastructure.

However, existing blockchain infrastructure is still primarily geared towards crypto-native users and individual developers, lacking native support for large-scale institutional-level demands.

Industry insiders point out that institutions face several core pain points when conducting business on-chain, including: the need for fully closed-loop on-chain/off-chain validation for asset issuance and redemption; payments requiring deterministic finality; compliance capabilities needing to be embedded at the foundational layer; configurable privacy protection; and the need for predictable Gas costs using USDC, among others.

Ethereum, Solana, and other existing public blockchains struggle to natively meet these demands.

For Circle, the company has historically relied primarily on USDC reserve interest for profitability. In Q1, USDC circulation reached $77 billion, a 28% year-over-year increase. As its business scale continues to expand, relying solely on existing public chains can no longer fully meet the deeper needs of institutional clients.

Therefore, Circle's launch of Arc aims precisely to fill this gap. The underlying logic is that having a stablecoin circulate on someone else's chain does not mean owning the stablecoin financial ecosystem—which is why Circle decided to build its own L1.

Image source: X user @vanisaxxm

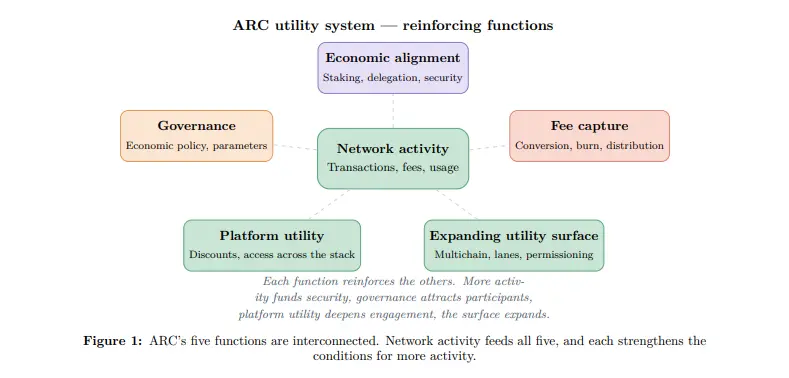

2. USDC Solves the Transaction Problem, ARC Solves the Coordination Problem

Since USDC is already the Gas token for Arc, why is another ARC token needed?

USDC has effectively solved the stability issue at the transaction level. Institutions can pay fees directly priced in USD, with predictable costs that can be accounted for, avoiding the troubles caused by crypto asset price volatility for finance departments.

However, for a network to operate healthily in the long term, solving the transaction problem alone is not enough. It also needs to address coordination problems.

According to the official whitepaper, Arc will gradually transition from its current Proof-of-Authority to Proof-of-Stake. Validator nodes need to stake assets to secure the network, with the core principle of staking being to bind node behavior through economic incentives; malicious actions risk slashing. USDC's value is pegged at $1, making it unable to truly bind node interests to the network's success or failure. Only the native ARC token can provide such dynamic economic incentives.

Governance also requires interest alignment. Key decisions such as fee rates, inflation parameters, and burn ratios require participants to adopt a long-term perspective. If voting were based solely on USDC, holders could easily lack sustained motivation, potentially voting and then exiting. ARC holders' asset value is directly tied to network performance, giving them stronger motivation to make choices beneficial for the network's long-term development.

The whitepaper also clarifies that ARC's governance authority has phased boundaries. Economic parameters are determined by token holder votes, but important matters like protocol upgrades, security incident handling, and validator qualification reviews initially remain under Circle's control, with gradual decentralization planned as governance matures.

In simple terms, USDC is the lifeblood of the Arc network, responsible for efficient daily flow; ARC is the equity of the network, responsible for aligning the long-term interests of all parties. This dual-token design also partially transforms the cost of ecosystem development from Circle's fixed cash expenditures into incentive arrangements tied to the network's success or failure.

3. CRCL and ARC: Which Pieces of the Pie Do They Capture?

Thus, Circle now holds both the publicly listed equity CRCL and the network's native token ARC, both capturing the value of the same Arc network. So, which pieces of the pie do they respectively capture?

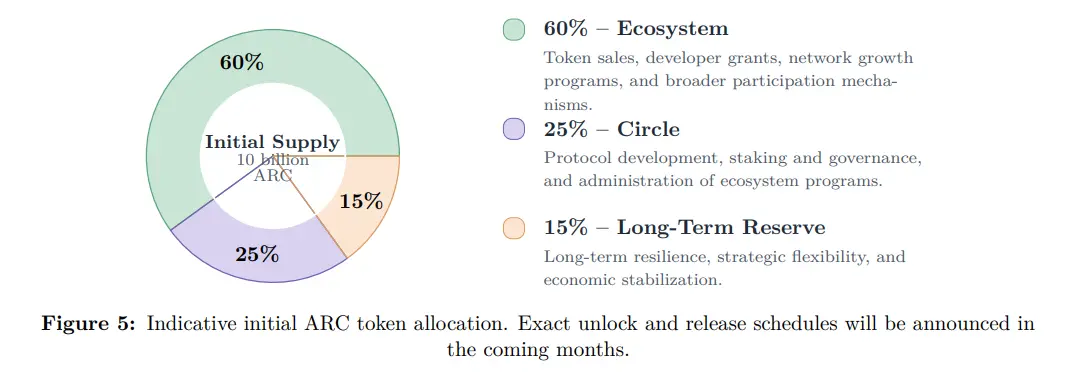

According to the whitepaper, the total supply of ARC is 10 billion tokens, with a clear allocation: 60% for the ecosystem, including developer incentives, network growth programs, and user participation rewards; 25% allocated to Circle for operating validator nodes, staking, and governance; 15% as a long-term reserve for network stability and strategic flexibility.

Regarding the fee mechanism, all protocol fees on Arc, regardless of the asset used for payment, will be fully converted to ARC at the protocol layer, with a portion permanently burned and a portion distributed to stakers and validators. The more active the network, the stronger the value capture by ARC.

CRCL shareholders primarily benefit through Circle as a company. The company continues to enjoy the core revenue from USDC reserve interest, along with gains from the growth of other businesses like the payment network CPN. Simultaneously, Circle's 25% ARC holdings allow it to indirectly share in network-level rewards.

Crypto analyst BTCdayu proposes a three-dimensional valuation framework for CRCL: The first dimension is reserve interest income, the most stable current cash flow and the valuation floor. The second dimension is payment network revenue, which, as CPN scales, could approach a Visa-like network fee model. The third dimension is the network option value brought by Arc, reflecting market expectations for Circle's transformation from a stablecoin issuer to a financial infrastructure platform.

Simply put, CRCL captures the company's overall stable cash flow and existing business growth, while ARC captures the growth elasticity at the network level, including Gas fee conversion, ecosystem expansion, and long-term network effects.

This forms a clear dual-track structure. The more successful the Arc network, the greater the USDC usage and business synergies, benefiting Circle at the corporate level. Concurrently, the rising value of the ARC token increases the value of Circle's 25% share, ultimately benefiting CRCL shareholders.

However, the two are legally completely separate. As mentioned officially, ARC does not represent equity in Circle and does not grant any claim to Circle's revenue, profits, assets, or CRCL shares. This means ARC holders lack the fiduciary duty protections afforded to public company shareholders; their returns depend entirely on the network's actual adoption and the tokenomics design.

4. How Can Ordinary Users Participate?

Having understood the value distribution between CRCL and ARC, a practical question arises: Who exactly is the ARC token being sold to? And how can ordinary users participate at low cost?

The first category of buyers is strategic institutional investors. They entered via the $222 million presale at a unit price of $0.3, with lock-up periods ranging from 1 to 4 years. These institutions not only provide capital but are also potential users and builders of Arc. For example, BlackRock is already testing tokenized asset settlement on the testnet; ICE, as the parent of NYSE, and SBI Group, as Japan's largest financial group, are strategically positioning themselves for future business on Arc.

The second category is ecosystem builders and long-term holders. Developers and liquidity providers receive ARC incentives for their contributions; the 60% ecosystem allocation is for this purpose. They prioritize the network's long-term growth, akin to early employees holding company equity.

The third category is retail speculators and participants. They focus on early narrative opportunities and ecosystem incentives, anticipating price volatility post-mainnet launch.

For ordinary users without presale access, Arc offers several low-cost participation paths.

The Arc Testnet launched in October 2025 and has processed over 244 million test transactions to date. The mainnet is expected to launch in the summer of 2026. Users can claim free test tokens to perform operations like Swaps, bridging, and contract deployment to familiarize themselves with network interaction.

The Arc House community is the primary entry point for ordinary users. Users can accumulate points by registering, staying active, posting, reading content, and participating in Q&A. Having an answer accepted yields extra points.

Advanced methods include content contribution, video sharing, event organization, and even hosting offline Meetups. Additionally, users with teams or products can apply for Circle Developer Grants.

It should be noted that Arc House points merely represent community contribution recognition; they hold no monetary value, nor do they guarantee any specific rights allocation. Specific rules are subject to the latest official announcements.

Conclusion

Currently, competition in the institutional on-chain sector is fierce, and Arc is not alone. Canton Network, under Digital Asset, is reportedly completing a new funding round at a valuation of around $2 billion, led by a16z crypto; Plasma positions itself as a stablecoin-native settlement layer with a relatively more attractive valuation; Visa included Arc, Canton, Plasma, Base, Tempo, and others as stablecoin settlement test points in April. This indicates the sector is still in a phase of parallel development with multiple competitors.

Against this backdrop, Arc's $3 billion presale FDV (Fully Diluted Valuation) sits at a relatively high level. Retail investors considering secondary market participation need to thoroughly evaluate the project's narrative potential and the competitive landscape within the sector.

From a long-term perspective, holding ARC, which carries an annual inflation of 2% to 3%, requires the network to generate sufficient real transaction fees to offset the inflation pressure for value appreciation. CRCL, in contrast, relies on USDC reserve interest and payment network revenue, supported by relatively clear cash flows. They represent different risk-return structures.

Short-term, market sentiment often follows its own logic. Around the mainnet launch, concentrated narrative hype could bring periodic opportunities. During such times, the value of Circle's 25% ARC holdings would also appreciate, benefiting CRCL shareholders.

On the regulatory front, the passage of the GENIUS Act has solidified Circle's moat, while the CLARITY Act's new draft version has been made public and is advancing in Congress, potentially providing clearer regulatory certainty for the digital asset ecosystem—a significant positive for Circle.

Overall, Arc is currently one of Circle's key strategic initiatives. As the whitepaper states, "A global economic operating system cannot be coordinated by a single entity; it transforms participants who use Arc into participants who sustain Arc." Whether this vision ultimately materializes still depends on the network's ability to attract sufficient real institutional transactions and economic activity after the mainnet launch.

Until all data lands, all narratives remain just narratives.