Author: KarenZ, Foresight News

In Silicon Valley, the name Naval Ravikant is synonymous with credibility.

He is the co-founder of AngelList and one of the most representative early-stage investors of the past decade, having backed companies like Uber, Twitter, and Notion. Now, in the new USVC Venture Capital Access Fund (USVC), Naval is not just a symbolic figure. According to the fund's April 2026 supplemental disclosure document, he serves as the Chairman of the Investment Committee, responsible for portfolio construction and strategy oversight.

This arrangement is significant because USVC is not merely selling the concept of a "low-threshold fund." What it is truly attempting to package and offer is a capability that was previously available only to a select few: earlier access to pre-IPO growth-stage companies.

On the surface, USVC is most easily understood as a "venture capital fund for retail investors." But when viewed together—the official website, the prospectus, and the portfolio page—the core story AngelList wants to tell becomes clearer and more pointed: the most imaginative companies today are taking longer to go public; IPOs are increasingly becoming exit points rather than entry points; what ordinary investors are shut out of is not just the risk, but also the most "lucrative" period of growth.

The significance of USVC lies in its attempt to pry that door open a little.

The Core of USVC: Not a Fund, But Selling 'Pre-IPO' Access

The USVC homepage states the problem bluntly: The next wave of growth is happening in the private markets. The website also provides a telling comparison: in 1980, the median age of a U.S. company at IPO was 6 years; today, it's 13 years. Those extra 7 years mean a massive amount of value creation is occurring outside the public markets.

This is the crucial product logic behind USVC. The USVC prospectus clearly states that USVC primarily invests in VC funds, SPVs, and private, pre-IPO growth-oriented companies. The most easily overlooked, yet most critical term here is "pre-IPO growth-oriented companies." The definition in the document is equally direct: private companies that the investment adviser believes "have significant growth potential at the time of investment."

In other words, USVC's selling point is not the abstract "allocation to venture capital," but rather bringing ordinary investors face-to-face with the truly most attractive segment of assets in the private markets. It aims to sell a channel for accessing pre-IPO growth companies.

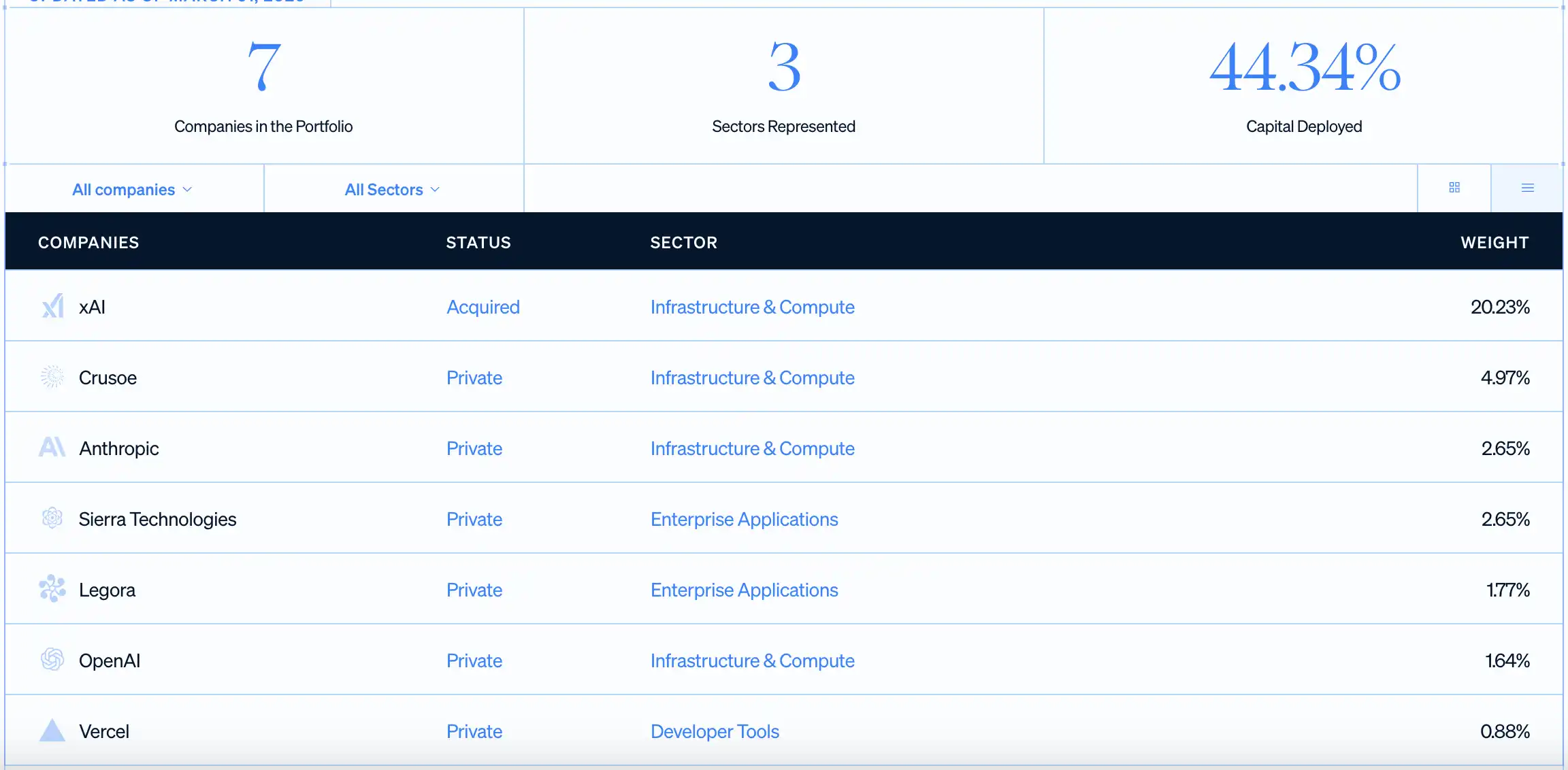

This is also why it consistently emphasizes names like OpenAI, Anthropic, xAI, and Vercel. The portfolio page on the website shows that as of March 31, 2026, USVC had deployed 44.34% of its capital, with 7 companies in its portfolio. The largest single holding is xAI, followed by Crusoe, Anthropic, Sierra, Legora, OpenAI, and Vercel. Regardless of the eventual performance of these positions, the message AngelList wants to send investors is clear enough: companies you once only read about in the news, you can now gain some exposure to *before* they go public, through a single fund.

This is highly attractive to ordinary investors. Because under the traditional path, they typically only get the chance to buy in *after* a company's IPO. And by that point, the earliest, most explosive growth has likely already been captured by the founding team, employees, early-stage funds, and institutional shareholders.

Legally, this fund is registered as a closed-end management investment company under the U.S. Investment Company Act of 1940. It was initially established on April 8, 2021, converted to a Delaware statutory trust on August 7, 2025, and is currently raising capital through a continuous offering. The initial investment threshold is $500, with no minimum for subsequent additions; the website even supports monthly dollar-cost averaging.

This packaging is clever. It retains the core attraction of the private markets—pre-IPO growth companies—while making the purchase process resemble a retail financial product as much as possible. U.S. users don't need to first become accredited investors, enter high-net-worth circles, or deal with the complex tax forms typical of traditional private funds. At the point of purchase, at least, AngelList tries to make it seem simple enough.

Access to Pre-IPO Companies Does Not Mean a Simple Investment

Precisely because USVC's narrative is so enticing, it's the constraints behind it that need to be clearly spelled out.

First, investors are buying a share of a fund. The fund holds these pre-IPO growth companies indirectly or directly through VC funds, SPVs, and direct investments. This means investors get *access* to pre-IPO growth companies, not the clear, readily realizable ownership experience of buying a stock.

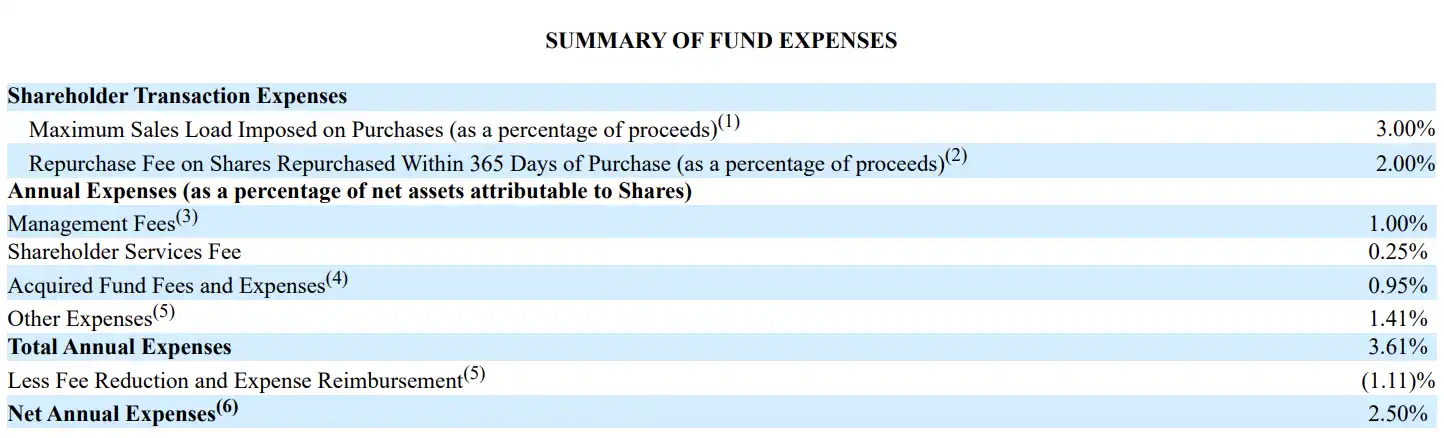

Second, this access comes at a cost, and it's not low. The fee table on page 20 of the Prospectus shows that USVC has a management fee of 1.00%, a shareholder servicing fee of 0.25%, underlying fund fees and expenses of 0.95%, other expenses of 1.41%, resulting in a total annual expense ratio of 3.61%. After fee waivers (in place at least until October 29, 2026), the net annual expense ratio is 2.50%. After accounting for the underlying VC vehicle and operational costs, investors are facing a product with a current net expense ratio that is not insignificant.

Third, this fund does not provide ordinary investors with a truly high-liquidity exit path. USVC is not listed on an exchange, has no public trading market, and liquidity primarily depends on whether the Board of Directors initiates quarterly share repurchases, which typically will not exceed 5% of net assets. The documents originally included a 2% repurchase fee for shares held less than a year, but the Board has currently decided to waive it (subject to modification or termination). This means it offers slightly more flexibility than a traditional VC fund, but is still far from "in and out anytime."

Fourth, USVC does not have a fixed termination/ liquidation date like a traditional 10+2 year venture capital fund, but it is still a long-term, closed-end structure with no defined end date. When the underlying assets realize their value still depends on liquidity events like IPOs, mergers and acquisitions, or private secondary transactions. The prospectus also clearly warns that many portfolio investments may take several years to appreciate significantly.

And even after a portfolio company goes public, it is often subject to lock-up restrictions, commonly for 180 days. During this period, the fund itself, or the managers of the underlying VC/SPV the fund invested in, may not be able to sell immediately.

Why is the Web3 Circle Paying Attention to This Fund?

The additional attention USVC is receiving from the Web3 circle is also related to Naval's and AngelList's sustained investment in the crypto industry over the years.

Naval has long been one of Silicon Valley's most publicly supportive investors of crypto assets and the Web3 narrative. In 2017, he told Laura Shin in an interview that his attention had largely shifted to Crypto; by 2021, he systematically discussed Web3, NFTs, and digital property rights with a16z partner Chris Dixon in a long conversation with Tim Ferriss.

On the platform side, AngelList has not treated Crypto as a fringe business in recent years, beginning to support investments in USDC on its platform in 2022. AngelList's website currently has a dedicated Crypto solutions page, explicitly stating its collaboration with CoinList to support Crypto SPVs and related fund vehicles.

Furthermore, on the other side, more and more cryptocurrency exchanges and Web3 projects are accelerating the launch of Pre-IPO products. USVC represents a slow-moving variable within the system, while most Web3 Pre-IPO products represent fast-moving variables driven by efficiency, often offering the ability to exit at any time.

These two worlds originally spoke different languages but are now competing for the same investors, the same narrative, and the same anxiety: If great companies are taking longer to go public, can ordinary people still get a share of the pie *before* the IPO?

Naval's name can push that door open. AngelList's platform network can bring pre-IPO companies closer. But the world behind the door hasn't necessarily become much easier because of it.