Original | Odaily Planet Daily (@OdailyChina)

Author | Qin Xiaofeng (@QinXiaofeng 888 )

In the first quarter that just ended, the crypto market performed sluggishly. Affected by factors such as geopolitical tensions (e.g., the Iran conflict), macroeconomic uncertainty, and declining risk appetite, Bitcoin fell from around $87,500 at the beginning of the year to approximately $66,700, a drop of about 23%, marking its worst quarterly start since 2018. Other altcoins fared even worse. Apart from the tokenization of traditional assets and the AI sector, which still maintained growth, the entire market narrative fell into a lull.

In contrast, the U.S. stock market seemed to follow a different script. Even though the "Magnificent Seven" all saw double-digit declines, with Microsoft plunging 23% for its worst quarterly performance since 2008, the profit-making effect did not disappear. Some hot sectors rotated quickly and achieved decent results. These high-quality assets were promptly listed on the decentralized RWA trading platform, Maiton MSX.

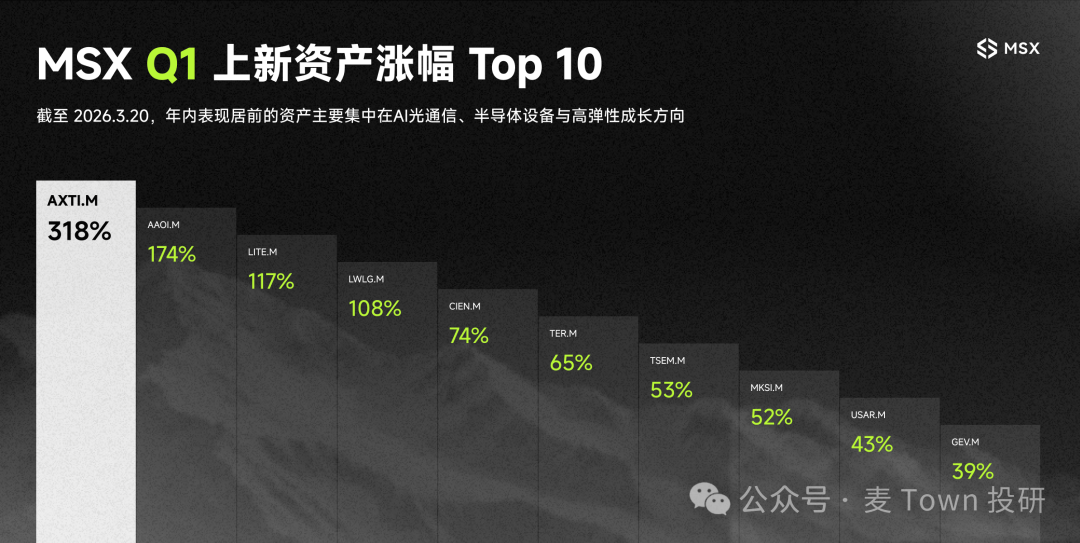

Data shows that in the first quarter of 2026, the MSX platform listed a total of 39 new U.S. stock token offerings, spanning U.S. individual stocks, sector ETFs, and macro tools, covering five main themes: aerospace & defense, energy & resources, AI hardware, optical communications, and regional allocation tools. The results show that this batch of offerings performed remarkably well overall. As of the time of writing, only 1 of the 39 offerings recorded a negative return (CRDO.M, -7.81%), while the rest were positive. Among them, a total of 4 offerings achieved year-to-date gains exceeding 100%: AXTI.M (+318.59%), AAOI.M (+174.70%), LITE.M (+117.58%), and LWLG.M (+108.95%), all concentrated in the AI hardware and optical communications themes. Additionally, 7 offerings saw gains exceeding 50%, accounting for nearly one-fifth of the total.

On the evening of April 2nd, Odaily Planet Daily invited Frank, a researcher from the MSX Maiton Research Institute, to review MSX Maiton's Q1 performance and provide a forward-looking perspective on Q2 new listings, helping the audience secure the main trends in U.S. stocks and select stocks precisely.

Odaily Planet Daily: MSX listed 39 new offerings in Q1, with 38 achieving positive returns and an average gain of 37.6%. Such a success rate is quite rare in the current volatile market. What is the core stock selection framework behind this 'top student' report card?

Frank: I'd like to correct a statement first: Q1 wasn't 'volatile'; it was a genuine downturn.

Throughout the quarter, both the S&P 500 (-4%) and the Nasdaq (-7%) weren't moving sideways but were actually declining. This was especially true for weighted tech stocks, which faced significant pressure. Core assets like Microsoft, Tesla, Meta, Google, NVIDIA, Amazon, and Apple generally experienced不同程度的 pullbacks, even falling below their 200-day moving averages.

This means that Maiton MSX's Q1 report card—'39 new listings, 38 positive returns, 8 with gains over 50%'—was achieved against a backdrop of a falling overall market and declining heavyweight valuations.

If we break down the logic behind this result, frankly, precise timing was certainly a factor; the listing times for some offerings indeed coincided with just before their price increases. But beyond luck, the more important factor is that Maiton MSX has always adhered to a relatively stable principle in stock selection:

We avoid stocks that seem to have high potential but lack clear industry direction, and we don't bet on when large-cap blue chips might bottom out. Instead, we prefer to find small and mid-cap companies with clear industry trends, clear capital transmission chains, and the potential for gradual earnings realization.

Simply put, we are not betting on whether a major trend will suddenly reverse; we are digging down along the产业链 (industry chain) with the strongest certainty. We focus on who is receiving orders, who is undertaking capital expenditures, and who is truly benefiting from the expansion of industry trends.

To be more direct, we are not gambling on whether some grand narrative will suddenly reverse, but rather digging down the industry chain with the strongest certainty. Whoever is getting orders, undertaking capex, and truly benefiting from industrial expansion is more likely to enter Maiton MSX's observation and listing视野 (field of view). It is precisely for this reason that we were able to achieve a relatively beautiful 'top student' report card in Q1, even amidst an environment where indices and heavyweights were generally under pressure.

Odaily Planet Daily: You categorized the Q1 new listings into five main themes: AI Hardware, Optical Communications, Energy & Resources, Aerospace & Defense, and Regional Allocation Tools. How were these five themes identified and established as 'tradable directions' at the beginning of the quarter? Were there quantitative or macro indicators supporting this?

Frank: Actually, these five lines weren't 'planned out' at the beginning of the quarter. More accurately, they emerged gradually during the process of continuously tracking industry dynamics, earnings report data, and market anomalies.

A core daily activity of the Maidian Research team at Maiton MSX is to continuously monitor the earnings reports, Capex guidance, industry chain data of large tech companies, as well as the latest hot narratives and sectors with unusual fund movements.

For example, when Meta, Microsoft, Google, and Amazon continuously raised their capital expenditures related to AI infrastructure, these numbers might seem like cold budgets in the earnings reports, but in essence, they will inevitably be transmitted down the supply chain—flowing to chips, optical modules, power equipment, cooling, and testing环节 (links).

So, rather than saying we are making macro judgments, it's more like we are tracking the flow of funds and the path of industry realization. Because the money actually spent by big tech often has more explanatory power than many abstract macro indicators—PMI, interest rate expectations, and macro口径 (calibers) are certainly important, but the real signals are the genuine money from signed contracts, placed orders, and initiated capacity expansions.

On this basis, we further distinguish which companies in which sectors have actually received orders and started to reflect growth in revenue and profits, and which are merely concept-driven or sentiment-driven initially.

As for directions like Energy & Resources and Aerospace & Defense, their driving forces are not exactly the same as the AI industry chain; they are more influenced by policy, geopolitics, and cyclical logic. But essentially, they still符合 (conform to) Maiton MSX's same screening criteria: first, check if the driver is real; second, see if the benefit is specific; finally, assess if the trade is viable.

Odaily Planet Daily: Among them, AI Hardware and Optical Communications became the two strongest main themes in Q1. At what point did you确认 (confirm) that these two lines had 'systematic opportunities' rather than being short-term trading themes?

Frank: Our research institute actually started paying attention to the AI hardware line back in Q2 and Q3 of last year. At that stage, almost all market attention was focused on NVIDIA, but Maiton MSX started looking earlier at the upstream and downstream supply chain, searching for who does packaging, who does cooling, who does power management, and who is承接 (undertaking) more niche supporting demands.

This is based on a simple reasoning: NVIDIA's market cap is already in the trillions. While it has high certainty, its elasticity is limited. However, its Tier 2 and Tier 3 suppliers are still in the early stages of an earnings explosion. There are two transmissions here: one is the real transmission of orders, revenue, and profits along the industry chain; the other is the轮动传导 (rotational transmission) of market attention, capital preference, and narrative heat. The former determines the fundamentals, the latter determines pricing revaluation, and both require time.

The confirmation for Optical Communications came a bit later, roughly between last year's Q4 and January this year. The key inflection point came after the Q3 and Q4 earnings reports of major tech companies陆续落地 (landed one after another), with capital expenditure guidance becoming increasingly aggressive. Once you calculate this account, you realize that data centers need expansion, computing density needs increase, so the demand for infrastructure connecting these computing nodes, including optical modules, fiber optics, switching, and interconnects, isn't just potential—it's实实在在 (solid and real).

Therefore, the core standard for Maiton MSX to judge whether a theme has systematic opportunity is never how popular the concept is, but whether there are real orders being transmitted on this industry chain, whether real money is flowing, and whether there are companies卡在 (stuck in)关键环节 (key links) that have already reflected revenue growth.

Only when these conditions are met is it not a short-term炒作题材 (speculative theme), but a systematic opportunity worth持续配置 (continuous allocation) and listing. We generally avoid directions based purely on storytelling.

Odaily Planet Daily: In comparison, Aerospace & Defense and Regional Allocation Tools did not see outstanding gains but were still included in the system. How do you evaluate their true value in the portfolio?

Frank: The fact that their gains are not outstanding precisely indicates that their intended role was never to be the 'spearhead of attack'.

A mature platform product logic cannot allocate all exposure to high-volatility sectors. For example, if users held only AI hardware and optical communication stocks, looking back at Q1, they would have feasted, but一旦 (once) the main theme corrects, they would be very passive. Just like an article I read today about Cathie Wood, her investment style is very aggressive. Although she operates in the secondary market, her underlying logic is like VC-style radical investment.

This easily becomes a double-edged sword. When catching the left side, it can rise特别猛 (extremely fiercely), like the tech stock frenzy in 2020-2021 during the big rate cuts, which helped propel Cathie Wood to be hailed as the 'female Warren Buffett,' with assets under management once reaching $59 billion. But the declines are equally brutal; now it has fallen by 70%, evaporating hundreds of billions...

Ultimately, high elasticity is an advantage, but without structural hedging and diversification, it同样会变成 (can also become) a double-edged sword.

Therefore, the value of Aerospace & Defense and Regional Allocation Tools lies in providing 'exposure in different directions.' After all, Aerospace & Defense has its own independent driving factors, with very low correlation to the AI cycle—escalating geopolitical games and increasing national defense budgets are logics completely out of sync with the tech cycle. Regional Allocation Tools are more instrumental, for example, allowing users to conveniently configure some exposure to non-US markets.

Such offerings may not be intended to contribute the highest gains, but they allow users to build a more complete and resilient portfolio structure on the MSX platform. We are not just providing users with the things that can rise the most; we are providing足够多 (sufficiently many),足够好用 (sufficiently easy-to-use) configuration tools to help users cope with different market environments.

This is also a point that MSX Maiton has always insisted on in its listing system: having both offensive elasticity and structural completeness.

Odaily Planet Daily: The Q1 listing rhythm showed明显的分阶段推进 (clear phased progression):偏向 (leaning towards) macro underlying framework in January, deep diving into AI infrastructure in February, and supplementing tools and materials in March. How should we understand this dynamic follow-up mechanism? Was this rhythm the result of active design or a dynamic adjustment following market sentiment and fund flows?

Frank: It's a bit of both, but if we must assign weights, the proportion of dynamic adjustment is larger.

January leaned towards the macro framework because the clues related to energy, resources, and geopolitics heated up最先 (first) at the beginning of the year, and the market gave feedback on these directions first. By February, major tech earnings reports had陆续落地 (landed one after another), Capex data continuously exceeded expectations, allowing for more confident deep dives into the细分环节 (niche links) of AI infrastructure—who makes optical modules, who does liquid cooling, who provides power配套 (support), who actually received orders transmitted by the capacity expansion logic.

By March, supplementing tools and materials was more because the main theme stocks had already experienced a wave of gains, and capital naturally began searching for surrounding links not yet fully priced,补涨逻辑 (catch-up logic), and relatively low-priced beneficiary assets. Coupled with catalysts like GTC and major optical communication industry conferences, the market's focus would further diffuse from leaders to supporting and application layers.

So you can understand MSX Maiton's listing rhythm as: having前瞻判断 (forward-looking judgment) on the general direction, but what specifically gets listed each month, how many, and which category first, is dynamically advanced following the landing rhythm of industry data and market capital preferences.

It's not a monthly plan made by拍脑袋 (a snap decision), but more like a mechanism of 'advance when the signal arrives.' This is also why MSX Maiton's listings don't seem mechanical but more like持续 (continuous) high-frequency interaction with the market.

Odaily Planet Daily: In an environment of globally tight liquidity, the cost-effectiveness of U.S. stocks and Crypto is being re-evaluated. How do you view the trend of this 'capital either-or choice'? Will it continue into Q2?

Frank: Altcoins have indeed entered a 'wise man's time' (lull period). In the U.S. stock market over the past two years, there have been too many stocks that doubled or even increased tenfold in a few months. For example, LITE, listed in Q1, more than doubled in just a month or two.

So I don't think this is entirely a simple 'either-or' situation, but rather a re-prioritization of capital allocation. Over the past two years, Crypto users have undergone a significant learning curve, for instance, moving from pure MEME and pure on-chain gaming to gradually paying attention to (关注) macroeconomics, the Fed, and major tech earnings reports.

This cognitive upgrade, once it happens, is irreversible. When they find opportunities in U.S. stocks with higher certainty and relatively controllable volatility, a portion of their capital will naturally allocate there.

Will it continue into Q2? I think it's highly likely, and may even accelerate. The reason is simple: the Crypto market currently lacks new large-scale narratives, on-chain activity is declining, while the earnings realization cycle for the AI industry in U.S. stocks has just begun. Smart money will flow towards places with higher certainty.

Based on this trend judgment, MSX recently专门做了一个 (specially conducted) content activity called 'The Great U.S. Stock Learning' (if you're interested, you can find the 'Beginner & Education' entry in the Maidian section on the official website), aimed at helping users with a Crypto background understand the basic logic of U.S. stocks—how to read earnings reports, how to understand valuations, how to analyze industry chains—helping everyone systematically补上 (make up for) the basic ability of 'reading earnings reports, understanding valuations, and analyzing industry chains.'

This content isn't just for传播 (dissemination); it's because we genuinely see changing user needs. People don't necessarily want to 'abandon Crypto,' but rather want to allocate funds to more efficient and profitable directions in the current market environment, so there is a real need to learn about U.S. stocks and actively add a new arsenal for themselves.

This change is the trend more worthy of attention.

Odaily Planet Daily: After the落地 (landing) of securities tokenization, the 'entry barrier' for U.S. stocks is lowering. How do you think this will change the structure of retail investors in U.S. stocks in the future?

Frank: The most直观的 (intuitive) change is that as the threshold lowers, the people coming in will naturally change.

In the past, an Asian retail investor wanting to participate in U.S. stocks often had to go through a series of frictions: traditional broker account opening, deposits/withdrawals, account systems, minimum capital requirements, etc. As securities tokenization gradually lands, users can participate in related offerings through a more lightweight on-chain method, and holdings can be more flexible and fractionalized.

In essence, this isn't simply moving the trading interface on-chain; it's about unlocking a batch of new users who were previously blocked by infrastructure barriers.

From a structural change perspective, our MSX Research Institute believes two trends will be relatively clear.

First, the proportion of retail investors from the Asia-Pacific region and emerging markets will increase. They weren't without demand before; they were blocked by channels, costs, and processes. Once these constraints are weakened, incremental users will naturally come in.

Second, the trading style of these new users in the future will likely be more 'industry-theme driven' rather than traditional passive index配置 (allocation). Because these users are naturally accustomed to赛道思维 (sector thinking),叙事思维 (narrative thinking), and主题投资思维 (thematic investment thinking). They follow new narratives and chase new sectors in Crypto. When they enter the tokenized securities market, they likely won't simply buy an index and hold long-term; they will actively seek more elastic niche opportunities within the industry chain.

This point is highly契合 (aligned) with MSX Maiton's target screening logic because we are not just building a generalized entry point offering only broad market tools, but are striving to build a thematic, structural trading platform more suitable for the new generation of on-chain users to understand and operate.

In other words, securities tokenization changes not just 'how to buy,' but also 'who buys, what to buy, and why buy.'

Odaily Planet Daily: Standing at the starting point of Q2, how do you view the continuity and switching risks of the current main themes in U.S. stocks? Will AI Hardware and Optical Communications still be the core of the offense? Are there new main themes entering MSX's listing视野 (field of view)?

Frank: I believe the AI narrative will most likely continue, but its form is already changing.

In Q1, the market actually began to move away from the singular thinking mode of 'if NVIDIA rises, it's an AI行情 (market)' and instead looked at who truly benefited from the incremental growth after AI infrastructure expansion. This means that AI Hardware and Optical Communications will still be the core offensive directions in Q2, but the行情 (market activity) will likely gradually shift from 'broad-based gains' to 'differentiated screening.'

That is, the direction may not necessarily weaken, but the difficulty of stock selection will significantly increase. The future won't be about whether there is AI exposure, but about who is in the more critical, faster-realizing links.

Beyond this, our MSX Research Institute believes two directions are worth重点关注 (paying close attention to).

The first is Aerospace. This isn't entirely a new main theme, but entering Q2, its certainty is higher than in Q1. The reason behind this is that the geopolitical environment continues to change, the landing rhythm of defense budgets and related orders is clearer, and the earnings visibility of some segmented companies is increasing.

MSX Maiton敏锐捕捉 (keenly captured) this trend recently,提前上新 (listing in advance) several small and mid-cap commercial aerospace offerings, which普遍迎来 (generally welcomed) double-digit gains. Especially in these past few days when the overall market has been weak, they still managed to show relatively independent performance, which actually indicates that this direction has value for continued observation and布局 (positioning).

The second is the Software SaaS sector that was 'wrongly sold off' by Q1 sentiment. In Q1, software stocks were often sold off with a broad brush; the market first priced them based on risk appetite, then differentiated the fundamentals later. But among them, there will definitely be a batch of companies with high customer retention rates, healthy cash flow, and clear niche barriers, which were dragged down together just because of sector sentiment pressure. Once such assets enter a valuation repair phase, their elasticity can often be considerable.

Therefore, MSX Maiton's understanding of Q2 is大致 (roughly): the main themes remain, but the style will switch from 'casting a wide net' to 'deep screening.' While continuing to grasp high-certainty main themes like AI Hardware and Optical Communications, we will also begin searching for new structural opportunities in directions like Aerospace and software repair.

Odaily Planet Daily: Under the current macro background (interest rate path, geopolitical environment, profit cycle), are you more inclined towards offensive targets or配置型工具 (allocation tools)? How do you balance elasticity and defense?

Frank: I think the key to this question is not simply answering whether to偏向 (lean towards) offense or defense, but rather how to understand the macro environment at this current stage.

- First, regarding the interest rate path, the market's expectations for rate cuts have been repeatedly revised, so strategies overly based on the assumption that 'rates will definitely cut at a certain time' can be very dangerous;

- Second, uncertainty at the geopolitical level remains high;

- Third, in terms of the profit cycle, although capital expenditures of big tech are still expanding, the speed of revenue realization has not completely同步跟上 (kept pace). This means the market will increasingly care about 'when the money spent turns into real profits';

Therefore, against this background, MSX Maiton's preference is not for all-out attack or all-out defense, but rather for conducting offense with defense.

Specifically, the core仓位 (positions) will still优先放在 (be prioritized in) the AI infrastructure chain with the highest certainty, because these companies are supported by more real order and revenue growth logic. At the same time, we will also retain一部分 (a portion) of defensive exposure with low correlation to the tech cycle, such as energy, defense, and a certain proportion of tool-type allocation offerings.

This is also the overall thinking behind MSX Maiton's platform listings: we won't押中 (bet) all resources on high-elasticity offensive stocks, but will continuously supplement some defensive and tool-type assets, allowing users to find suitable coping methods in different market environments.

Ultimately, a truly effective long-term system is not about押中 (catching) the fiercest main theme for a certain period, but always having the ability to find a balance between offensiveness, certainty, and portfolio stability. The Q1 report card is essentially a阶段性体现 (stage reflection) of this logic.