There is a category of companies that actually appreciate in value when the world becomes more unstable: defense contractors, oil unions, gold miners. These are the classic examples, whose business models are fundamentally built on instability, turning such risk into pricing power.

Circle was not originally part of this category. Its token was designed to always be equivalent to 1 US dollar. Stability is the entire purpose of its product.

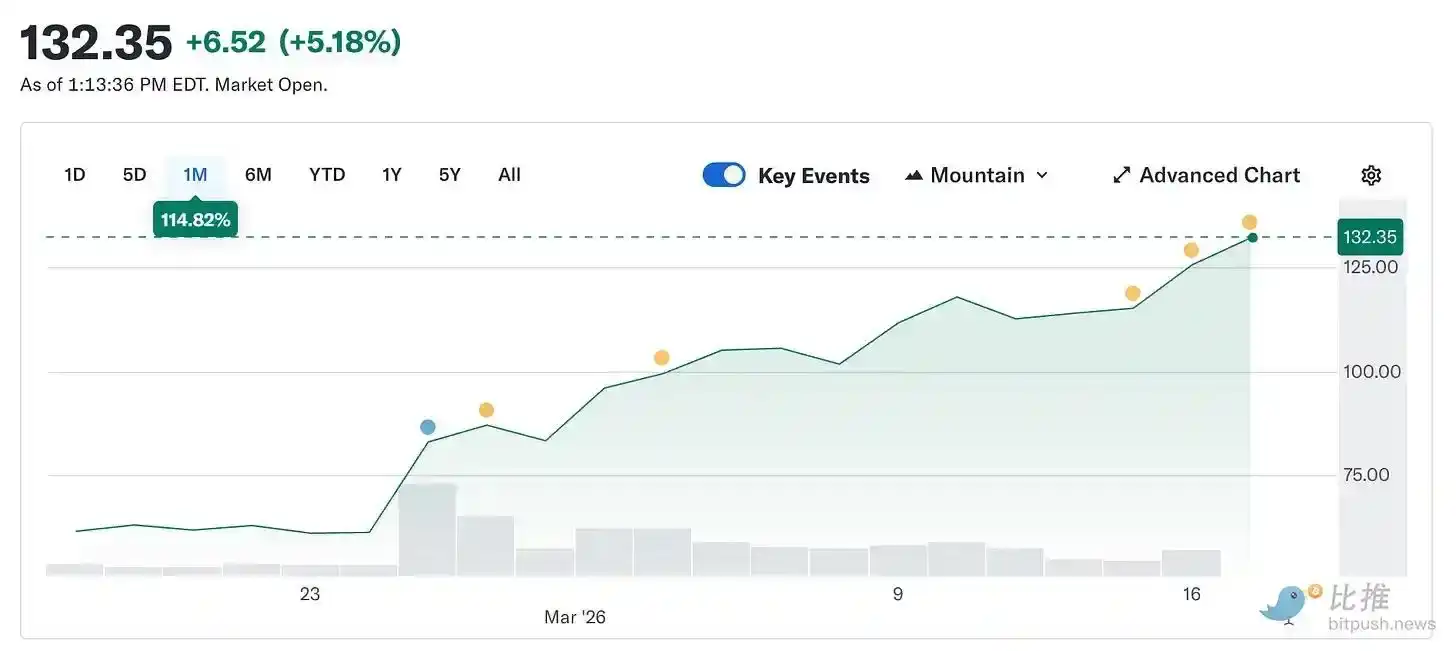

However, Circle's stock price has soared from $49.90 on February 5th to about $123 today, more than doubling in just five weeks. Meanwhile, the broader cryptocurrency market remains 44% below its peak levels from last October.

A company whose product is designed to pursue price stability has become one of the market's hottest trades precisely because the world has become more turbulent.

This article will explain the reasons behind this phenomenon and the discrepancy between Circle's true nature and its current market pricing.

What Exactly is Circle (Let's Get Back to Basics)

Strip away the branding, the payment narratives, and the dictionary of infrastructure references, and what you're left with is this: Circle holds U.S. Treasury bonds.

Every USDC dollar in circulation is backed by one dollar held in reserves of short-term government bonds. The interest from this debt belongs to Circle. This accounts for roughly 90% of the company's revenue in any given quarter. Once you see this, its business model isn't complex: Circle is a money market fund that issues a stablecoin.

This means Circle's income is tied to one key metric: the federal funds rate. When interest rates are high, Treasuries yield more, and Circle earns more income for every USDC in circulation. When rates fall, income contracts. Everything else is just scaling.

Here is the chain reaction that led to the 150% rebound in the stock price from its February low:

According to @finance.yahoo, the Iran conflict drove a ~35% rise since February 28th. A move to around $100 implied excessive panic, and excessive panic implied that a Fed rate cut would amplify recklessness. The decision to hold rates steady on March 18th was never really in doubt. Long before the war, CME FedWatch showed a probability of over 90% for unchanged rates.

What really changed were the expectations for rate cuts this year. Before the conflict, the market was pricing in two 25-basis-point cuts for 2026. After the conflict, this expectation shifted to one cut, prioritized for after September. The probability of no cuts at all in 2026 roughly doubled. With rates staying higher for longer, Circle's Treasury reserves continue to generate yield. More yield means more revenue, and more revenue means a higher stock price. A war broke out, and a stablecoin issuer became a beneficiary. This was a scenario that never appeared in anyone's predictive models.

Context: The bearish logic that suppressed Circle's stock price at $49 in February was essentially a bet on rate cuts.

The market was then predicting multiple Fed rate cuts in 2026, which would directly compress Circle's interest income. A rough illustration: at the current USDC supply level of $79 billion, every 25-basis-point cut would cause Circle to lose approximately $40 to $60 million in annualized revenue. Two cuts would erase nearly $100 million in top-line revenue by year-end. The war rendered this calculation obsolete overnight. Not because Circle changed, but because the macro context underpinning that bearish thesis ceased to exist.

How the Short Squeeze Began

While the interest rate story supported the stock price, the initial surge originated from positioning.

Before the Q4 earnings release on February 25th, approximately 17.8% of Circle's float was sold short. Hedge funds had built significant bearish positions. Their thesis was that rates would eventually fall, domestic income would compress, and this company's revenue wasn't defensible at the rate floor. From a fundamental perspective, this was hard to refute.

However, Circle reported Q4 earnings of $0.43 per share, versus a consensus estimate of $0.16. Revenue reached $770 million, against an expectation of $749 million. On-chain USDC transaction volume grew nearly $12 trillion quarter-over-quarter, up 247% year-over-year. Shorts covered. The stock surged 35% in a single trading session. According to 10x Research, hedge funds lost roughly $500 million on short positions that day. Subsequently, the war took the baton from the earnings report.

The Coinbase Problem

Here is a part often omitted from the updated narrative.

Circle reported a net loss of $70 million for 2025, not a profit. Q4 was strong, but the full year was not. To understand why, you need to understand its relationship with Coinbase, the most important and most underestimated fact of Circle's business.

When USDC first launched in 2018, Circle and Coinbase formed a joint consortium to manage it. This consortium was dissolved in 2023, with Circle gaining full control over USDC issuance. However, Coinbase retained a significant revenue share.

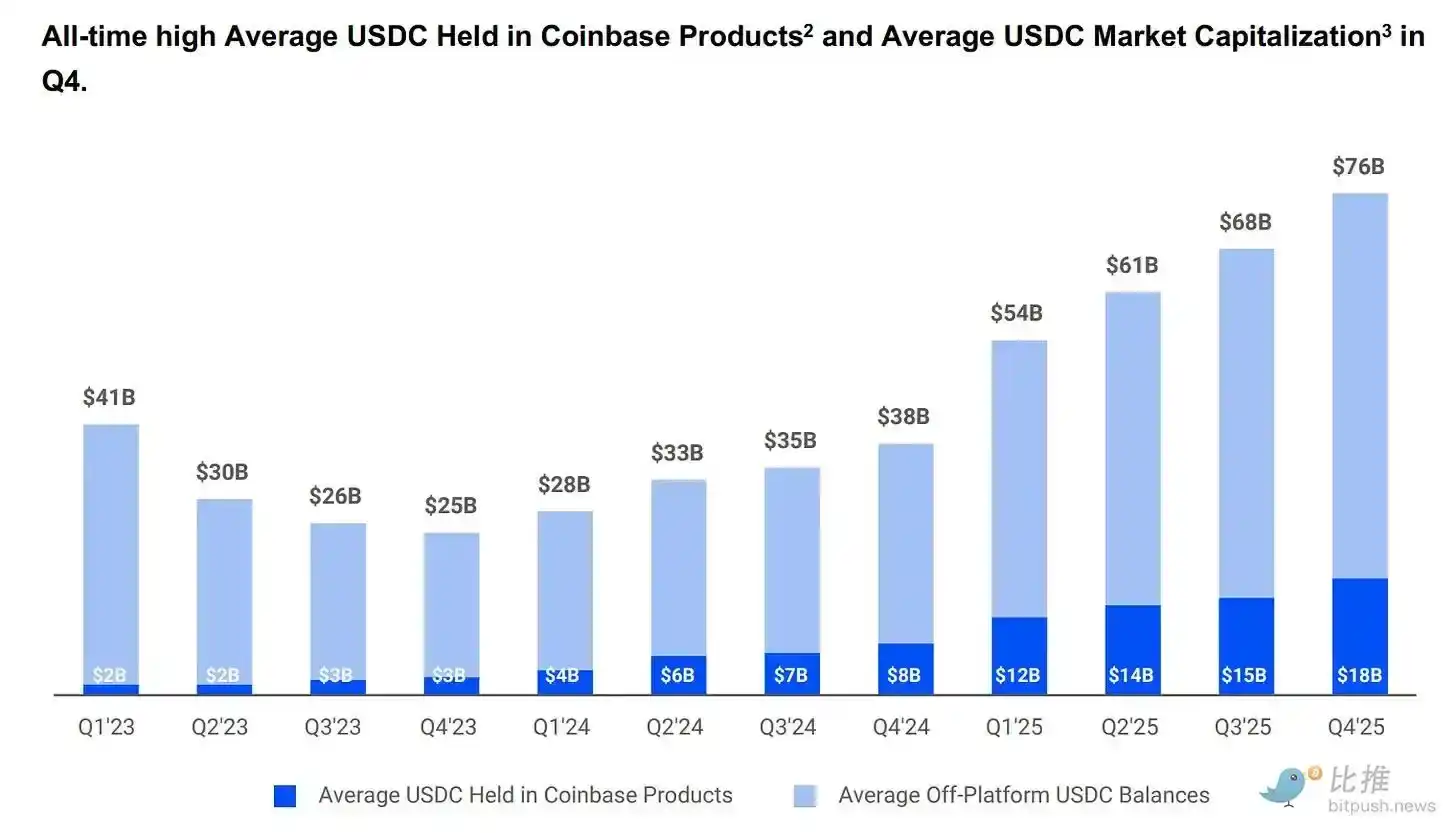

Coinbase takes 100% of the reserve yield from USDC held on its platform. For all other USDC, the yield is split 50/50 with Circle. In 2024, this arrangement directed $908 million of Circle's total $1.01 billion in distribution costs straight to Coinbase.

Roughly calculated, for every dollar of yield Circle's reserves generate, 54 cents flows to a company that neither issues the token nor handles the reserves. In early 2025, Coinbase held 22% of the total USDC supply, up from 5% in 2022. The more USDC grows on the Coinbase platform, the greater the share Circle pays out.

According to @q4cdn.com, the partnership automatically renews every three years, and Circle cannot unilaterally exit. Any outcome from the next renegotiation will directly impact Circle's margins. In Q4 2025, distribution costs alone were $461 million, up 52% year-over-year.

The current $70 million net loss is partly due to $424 million in stock-based compensation from IPO vesting, which makes the overall number look worse than the actual business performance. But the underlying business still faces a structural cost problem that no interest rate environment can fully solve.

The market prices Circle as infrastructure. The income statement shows it's an interest rate trade vehicle carrying expensive distribution costs. Both views can be true simultaneously. They just represent different pricing logics, and right now the market is paying for the 'best version' of both.

Why This Isn't Just a Macro Trade

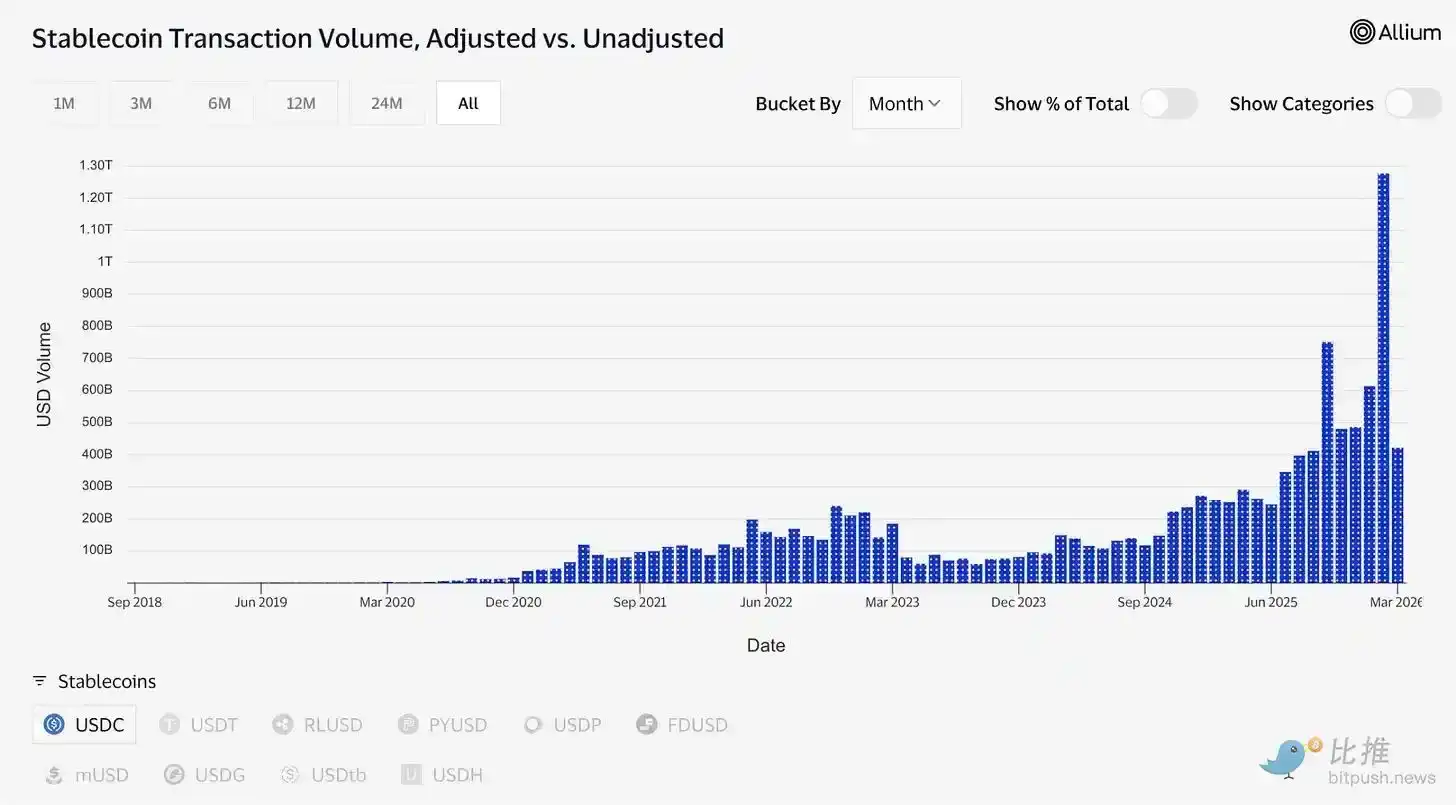

USDC's supply recently reached a new all-time high of $79 billion, while the broader crypto market is down sharply, 44% from October. This divergence is worth pondering. When markets fall, speculative assets typically decline. USDC's growth suggests people are using it to move value, not just as a speculative bet.

During the Iran conflict, demand for USDC surged in the Middle East precisely because traditional banking became unreliable. When normal channels are blocked, people use it for cross-border and cross-currency transfers. This is how payment infrastructure behaves under stress: its usage increases, not decreases.

Transaction data confirms this. In February alone, USDC processed approximately $1.26 trillion in adjusted volume, compared to $514 billion for USDT. Tether (USDT)'s market cap remains $184 billion, versus USDC's $79 billion. In terms of total supply, they are not comparable. But USDC currently moves more volume than USDT.

As shown by @visaonchainanalytics, "sleeping supply" is a different concept from "active settlement." The former shows where people park their dollars; the latter shows which dollar people use when they need to move value.

Druckenmiller said something relevant this week. In a Morgan Stanley interview recorded on January 30th and released on Thursday, he predicted the global payment system will run on stablecoins in 10 to 15 years, calling cryptocurrency "a solution in search of a problem."

One of the world's most trusted macro investors bifurcated the space: stablecoins are the nascent infrastructure, and everything else is still finding a reason to exist. This framework provides a bullish endorsement.

The Infrastructure Bet

Tokenized assets have grown from about $1.5 billion in early 2023 to about $26.5 billion today. Many of these products (including BlackRock's tokenized Treasury fund BUIDL, which holds over $2 billion) rely on USDC for subscriptions, redemptions, and settlement processing.

Prediction markets processed over $22 billion in volume in 2025, mostly settled in USDC (Polymarket alone). Visa currently supports stablecoin-linked cards in over 50 countries globally, with annual settlement volume of about $4.6 billion.

Circle is building the infrastructure beneath all of this. The Circle Payments Network connects 55 financial institutions, with an annualized processing volume of $5.7 billion, allowing banks and payment providers to convert USDC across borders and settle in local currency directly.

Arc is Circle's own Layer-1 blockchain, designed to fully support institutional systems. This is a settlement infrastructure that is not dependent on Ethereum or Solana. While the revenue impact from Ethereum and Solana is currently negligible, both are future-oriented strategic plays if interest rates fall.

The AI ecosystem is small in dollar terms but structurally interesting. Data released in March by Circle's Global Head of Expenditure shows that over the past 9 months, AI agents completed 140 million payments totaling $43 million. 98.6% were settled in USDC, with an average transaction size of $0.31. There are now over 400,000 AI agents with purchasing power. While the dollar amounts are still small, the trend is undeniable.

If AI agents need to pay each other for compute power, data access, and API calls with high-frequency, sub-penny transactions, they need tools that can settle instantly and send value at near-zero cost. Circle just launched Nano payments specifically for this need: supporting USDC transfers as low as $0.000001 with no gas fees, using off-chain resources and batch settlement. The testnet already supports 12 chains including Arbitrum, Base, and Ethereum mainnet.

This is the Circle the market is willing to pay $123 per share for: a company at the center of tokenized finance, AI agent commerce, cross-border payments, and prediction markets, with regulatory tailwinds from the GENIUS Act and the CLARITY Act likely to pass before summer. Bernstein has a $190 price target, Clear Street $136. Seaport Global, the most bullish on Wall Street, targets $280.

The Lingering Contradiction

Here, I want to candidly discuss a point that bulls often overlook.

Circle's profitability relies on maintaining high interest rates. This is not a permanent condition. The Fed will cut rates at some point. When that happens, the yield from the Treasury reserves backing USDC will contract, and Circle's interest income will shrink.

Circle recognizes this. It has been expanding into fees, enterprise services, the payments network, and Arc—businesses that don't rely on the interest rate environment to function. But currently, these revenue streams are small. Interest income is still the entirety.

So, you find these two logics coexisting in the same stock price, but they are not the same bet.

The infrastructure thesis posits that USDC is becoming genuine payment plumbing. The pipes are regulated, transparent, and poised to embed deeply into traditional finance, an embedding that is sticky regardless of rates. This thesis is supported by data: transaction volume digitization, integrations, Druckenmiller's framework, and Macquarie calling stablecoins the base layer of global financial infrastructure.

If this thesis is correct, Circle looks cheap in any interest rate environment because its total addressable market is the entire global payment system.

The rates trade thesis views Circle as a leveraged bet on "higher for longer" rates, with the stock price already reflecting a scenario where the Fed never cuts as expected. If this is the primary driver of the price, then every future Fed cut is a headwind, and the stock is overvalued relative to its fundamentals in a normalized rate environment.

Both views are being priced in. The war makes it difficult to discern which one the market is buying.

This is perhaps the most useful way to understand CRCL (Circle's ticker) right now. The focus isn't on whether it will hit $190, but on whether you are buying "infrastructure" or "a Treasury bill repackager that learned to tell a good story." The former is a long-term position; the latter implodes the moment Powell changes his mind.

For now, the price action keeps both possibilities alive. The dollar is doing the hard work it must. And in the gap between these two versions of the company lies its true tension—it figured out how to manufacture internet money denominated in dollars, but now must figure out how to survive the moment those dollars no longer yield 5%.