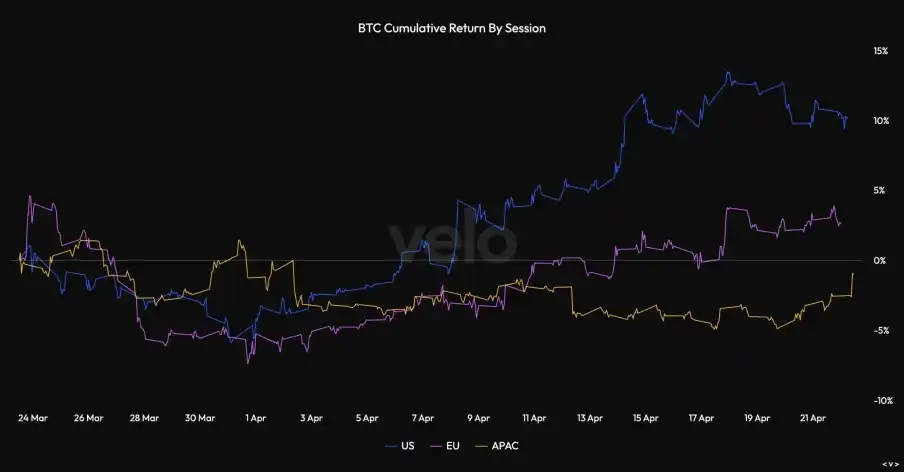

За последний месяц движение биткоина, кажется, подает сигнал: когда Strategy входит на рынок, BTC находит поддержку; наоборот, как только Strategy временно уходит, рынок быстро слабеет.

На прошлой неделе компания потратила 2,54 миллиарда долларов на покупку 34 164 BTC, доведя общий объем своих активов до 815 061 BTC. Стратегия TWAP Strategy внесла реальный спрос на спотовом рынке, в то время как рынок все еще выжидает: сможет ли текущая динамика самостоятельно стабилизироваться у ключевого уровня сопротивления в 80 тысяч долларов.

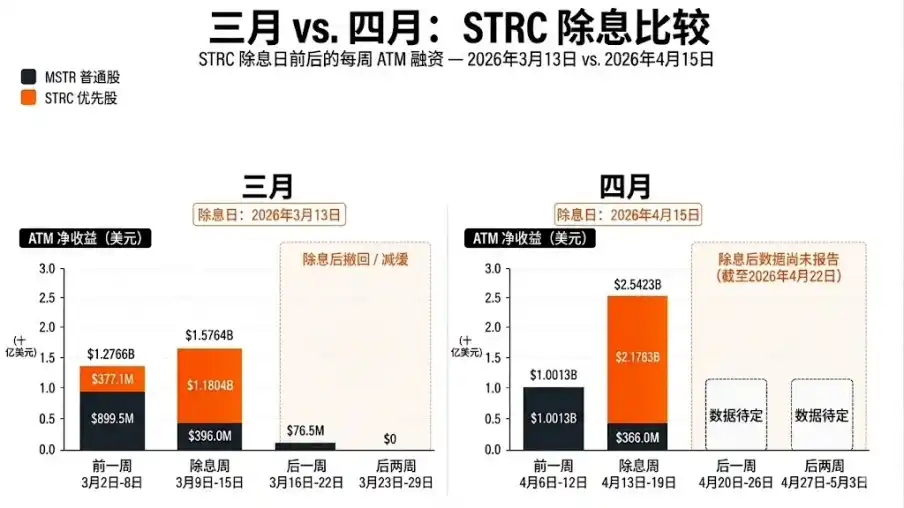

Оглядываясь на март, после недели экс-дивидендов (ex-dividend week) Strategy явно замедлила темпы покупки BTC, что также потянуло вниз цену BTC. То, что BTC смог удержать цену, полностью объясняется тем, что Strategy поддерживала его. Дальнейшая динамика полностью зависит от того, сохранится ли этот покупательский спрос после закрытия окна экс-дивидендов.

Движение в марте уже выявило риски. Strategy активно скупала активы в течение окна, а затем затихла, и цена BTC почти сразу же «рухнула». В пост-дивидендный период апреля ситуация повторилась. Теперь реальный вопрос в том, будет ли Strategy продолжать покупать после закрытия окна экс-дивидендов.

Если в апреле удастся избежать повторения явления «последивидендной слабости», как в марте, бычья логика станет гораздо более обоснованной. Если нет, то это всего лишь повторение прошлого сценария.

Краткое содержание (TL;DR)

- Маржинальный покупатель: Strategy является крупнейшим маржинальным покупателем на рынке. Недавнее ралли в американские торговые часы доказывает, что доходность биткоина за последний месяц в значительной степени обусловлена ею.

- Сценарий марта: Strategy активно скупала BTC перед окном экс-дивидендов $STRC, но затем в течение двух недель цена BTC резко упала.

- Отличие апреля: По состоянию на 22 апреля BTC пока не столкнулся с последивидендной слабостью, цена по-прежнему держится около 77,5 тысяч долларов.

- Ключевой сигнал: Предстоящий файл 8-K (крайний срок 27 апреля) крайне важен, он определит, продолжает ли Strategy покупать после закрытия окна экс-дивидендов.

- Долгосрочный риск: Высокая стоимость дивидендной доходности Strategy в 11,5% обходится дорого. Если рынки капитала ужесточатся, в конечном итоге им, возможно, придется продавать BTC или размывать акции для ее финансирования.

Крупнейший маржинальный покупатель биткоина: Strategy

За последний месяц почти весь рост BTC пришелся на американские торговые часы. Отчасти это связано с спотовыми ETF, но в большей степени — с покупательским давлением со стороны Strategy. Лучший способ понять эту волну — рассматривать ее не как размытое ралли «возвращения аппетита к риску (risk-on)», а как сосредоточенное желание американского капитала открывать длинные позиции при поддержке потоков ETF. Ежедневные данные Farside показывают чистый приток средств около 10 миллиардов долларов, подчеркивая реальный рыночный спрос.

Однако одного этого недостаточно для полного объяснения динамики рынка. За неделю по состоянию на 19 апреля объем покупок Strategy в 2,54 миллиарда долларов превысил чистый приток в ETF. Это подтверждает более разумную интерпретацию: не «ETF отсутствовали», а и ETF, и Strategy покупали, причем объем покупок Strategy был достаточно велик, чтобы стать одним из最重要的 маржинальных покупателей на рынке, что полностью соответствует движению графика по времени торгов. Поскольку почти вся прибыль пришлась на американские торговые часы, и один из крупнейших покупателей в США влил 2,54 миллиарда долларов, абсолютное влияние Strategy на цену BTC не требует доказательств.

Настоящее испытание для ралли наступает после экс-дивидендной даты

В марте Strategy активно покупала в окне экс-дивидендов $STRC, но затем в течение двух недель цена BTC резко упала. На неделе по 22 марта спрос на $STRC упал с 1,18 миллиарда долларов до жалких 76,5 миллиона долларов. Активность дополнительных эмиссий (ATM, At-The-Market) обыкновенных акций MSTR также упала до нуля. К неделе по 29 марта общий доход от ATM стал нулевым. Это также стал первым случаем за 13 недель, когда Strategy вообще не купила ни одного BTC.

Двухнедельное отсутствие Strategy совпало с падением BTC в тот же период, что является самым четким случаем, доказывающим определяющую роль Strategy в движении цены BTC. BTC steadily снижался до отметки чуть выше 70 тысяч, достигнув около 70 400 долларов 20 марта и около 70 600 долларов 23 марта. Рынок отражал реальность: когда выпуск STRC остановился, а обыкновенные акции MSTR не заполнили этот пробел, покупательский спрос значительно ослаб.

Следовательно, ключевой вопрос сейчас в том, повторит ли апрель «мартовское похмелье» или打破这一魔咒 (нарушит этот шаблон).

Следующий файл 8-K (крайний срок 27 апреля) будет охватывать неделю по 26 апреля. Если объем выпуска STRC снова упадет до уровня статистической погрешности, а ATM обыкновенных акций MSTR продолжит оставаться near zero, то апрель окажется просто увеличенной копией марта, а не настоящим сдвигом парадигмы. Однако, если STRC останется активным, а ATM обыкновенных акций MSTR достигнет значительного объема (более 1,5 миллиарда долларов), то сценарий действительно изменится.

Апрель крайне важен, потому что BTC до сих пор держится

15 апреля 2026 года стала экс-дивидендной датой для $STRC за апрель, годовая дивидендная доходность STRC по-прежнему составляет 11,50%. На неделе по 19 апреля Strategy привлекла 2,5 миллиарда долларов и купила 34 164 BTC,释放了极其庞大的需求 (выпустив чрезвычайно огромный спрос). Однако,真正的看点在于这之后 BTC 的表现 (настоящая изючка заключается в последующих показателях BTC): в отличие от марта, цена BTC не сразу рухнула.

Можно сказать, что Strategy изменила рыночную динамику. Но предстоящие документы гораздо важнее предыдущих. Если обычная «последивидендная слабость» появится снова, то апрель может оказаться просто повторением мартовского сценария. Если нет, то рынок должен серьезно задуматься над одним: Strategy покупает не только в течение окна, но и поддерживает BTC в более долгосрочной перспективе.

Будет ли покупательский спрос продолжаться?

Вот что действительно волнует трейдеров.

Просто заметить, что Strategy на прошлой неделе купила много BTC, — на этом не заработаешь. По-настоящему важно, продолжится ли этот покупательский спрос после того, как чистая логика экс-дивидендного дня исчерпает себя.

Опыт марта показывает, что одной сильной недели экс-дивидендов недостаточно. Strategy купила 22 337 BTC в отчетном периоде по 15 марта, но в последующие две недели практически исчезла, и цена BTC ослабла.

Показатели апреля указывают на то, что перемены все еще возможны, потому что Strategy купила больше — целых 34 164 BTC — и рынок BTC еще не повторил мартовское падение.

Логика здесь очень проста и понятна. Если следующий файл 8-K покажет, что после экс-дивидендной даты все еще были существенные покупки, рынок должен будет по умолчанию считать, что этот покупательский спрос все еще активен. Если же он покажет, что объем выпуска снова резко упал, это будет означать, что мартовские показатели являются их стандартной моделью работы, а не случайностью.

Почему сейчас можно быть бычьим — но будущие риски сохраняются

По состоянию на апрель 2026 года годовая дивидендная доходность STRC составляет 11,50%. Пока рынок готов платить за такую структуру, и цена BTC растет, это не проблема. Но если BTC остановится в росте, а рынки капитала станут менее щедрыми, ситуация может стать очень сложной.

Хотя это среднесрочная проблема, а не текущая торговая логика, риск объективно существует. 这个飞轮只有在 BTC 上涨且投资者胃口大开时才能完美运转 (Это маховик完美运转 (идеально работает) только тогда, когда BTC растет, а аппетит инвесторов велик).

因此,最纯粹的理解框架是 (Таким образом, самая чистая框架 понимания такова): пока Strategy продолжает покупать, это бычье влияние на BTC, но это не означает, что ее funding structure毫无风险 (беспроблемна). Просто сейчас рынку нужно关注这句话的前半段就够了 (关注 (обращать внимание) только на первую половину этого предложения).

Заключение

Недавнее движение BTC похоже на рынок, поддерживаемый одним необыкновенным супер-маржинальным покупателем. Март уже показал нам, что происходит, когда этот покупатель исчезает. Когда $STRC Strategy прекратит привлечение капитала в первые две недели после экс-дивидендов, ценовое движение апреля, скорее всего, повторится.

Поэтому правильный способ解读当下市场 (интерпретировать текущий рынок) — не зацикливаться на заголовках о последних цифрах покупок, а задать более простой вопрос: продолжает ли Strategy делать ставки на покупку BTC после очевидного окончания окна?

Если ответ утвердительный, BTC, вероятно, продолжит находить поддержку. Если ответ отрицательный, то BTC скоро на себе ощутит, каково это — «потерять поддержку крупнейшего видимого маржинального покупателя». Если в тот момент он сможет продолжать расти, то это будет предельно ясный окончательный бычий сигнал.