Автор: Alex Xu

Не оптимистично — это не значит, что я не верю в развитие бизнеса Ethereum (имею в виду долгосрочный рост пользовательской базы и количества транзакций, который, я считаю, будет), а значит, что я не хочу покупать по текущей цене, потому что она слишком высока относительно его фундаментальных показателей.

По нескольким графикам мы можем составить портрет текущего Ethereum:

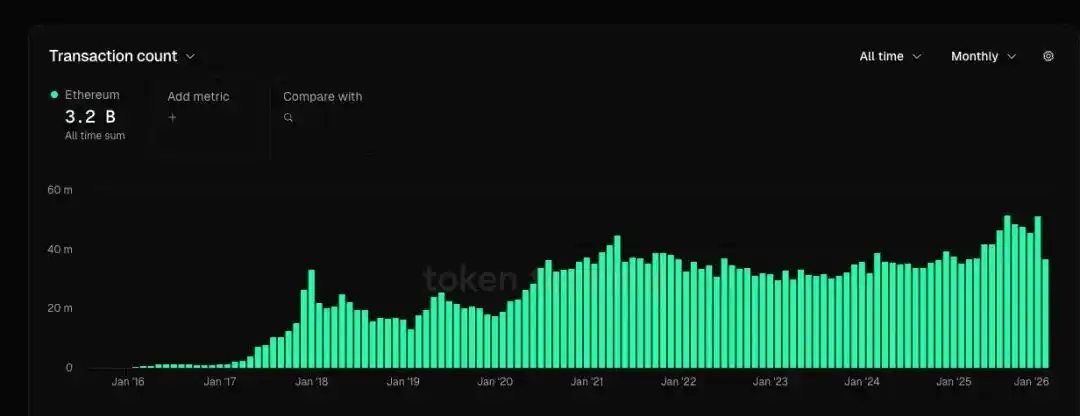

1. Количество активных пользователей волнообразно растет, достигая новых максимумов (на 44% выше пика предыдущего цикла), количество переводов также обновляет рекорды (на 13% выше пика предыдущего цикла). Темпы роста этих показателей еще ниже, чем темпы роста GMV некоторых ведущих электронных коммерческих платформ.

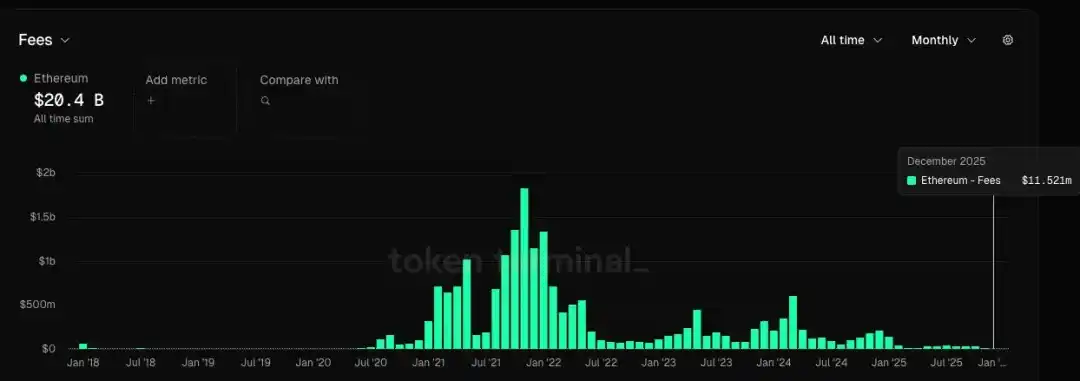

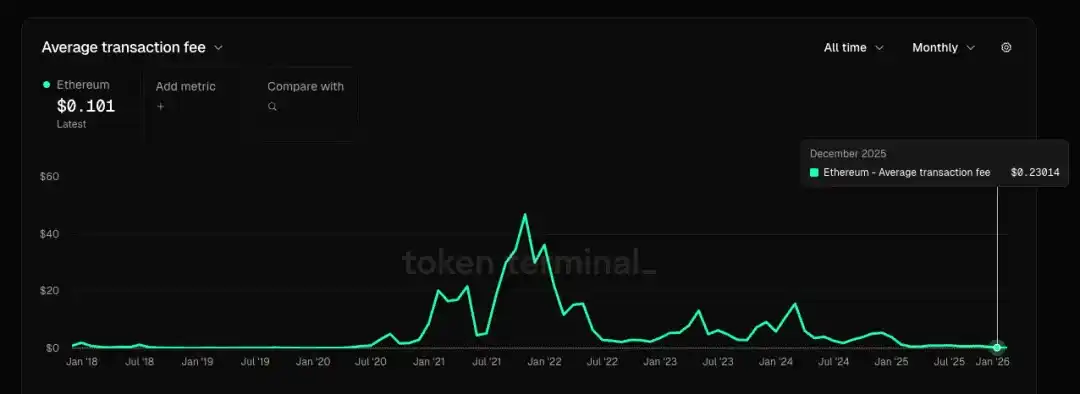

2. Текущие ежемесячные комиссионные составляют лишь 0.6% от пика предыдущего цикла, средняя комиссия за транзакцию — всего 0.5% от пиковых значений. То есть, медленный рост пользователей и количества транзакций был достигнут ценой резкого снижения стоимости услуг. Когда рост достигается ценой резкого снижения цен на продукт или услугу — это плохой знак для компании в любой отрасли.

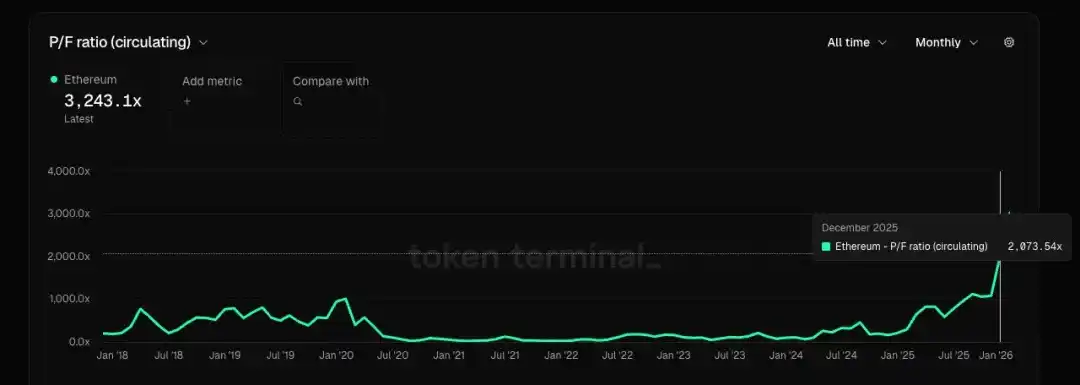

3. Если рассматривать Ethereum как компанию, предоставляющую услуги блок-пространства, то по данным на декабрь, его PF (цена/комиссия) превышает 2000x, PS (цена/выручка) превышает 10000x. Его чистая прибыль отрицательна, поэтому показатель P/E (цена/прибыль) отсутствует. В то время как у традиционных облачных компаний мультипликатор P/E обычно находится в диапазоне 20-30, а PS — в пределах однозначных чисел.

4. Если считать Ethereum не компанией, а товаром (аналогично цифровой нефти), то его проблема в том, что другие публичные блокчейны и rollups также могут предоставлять аналогичные услуги блок-пространства (как заменяемая нефть). Кто-то может сказать, что у Ethereum более сильные свойства децентрализации и устойчивости к цензуре, поэтому его как ресурс должен стоить дороже. Но действительно ли он должен быть настолько дороже? А разговоры о том, что eth заменит btc в качестве средства сбережения, которые были в прошлом цикле, сейчас практически исчезли, поскольку сформировался консенсус: в то время как btc — это цифровое золото, eth больше похож на tech-компанию + специализированного облачного провайдера, и его товарная позиция также обладает высокой заменяемостью.

5. Криптонативные приложения с PMF (Product-Market Fit) практически отсутствуют, в этом цикле почти не появилось ценных приложений. Недостаточный спрос и растущее предложение (количество rollup-решений и публичных блокчейнов продолжает расти) привели к серьезному переизбытку блок-пространства. Сама отрасль публичных блокчейнов демонстрирует вялый рост или даже сокращается.

6. А грандиозная картина, которую рисуют Tom Lee и некоторые местные VC, о том, что «Ethereum — это Уолл-стрит в блокчейне, и в будущем все будет на Ethereum», по моему мнению, на данный момент не подкреплена достаточными данными и фактами для подтверждения этой истории. Нет конкретной логической цепочки, это больше похоже на накачку. Наши инвестиционные решения должны основываться на рациональности, а не на вере. Их нарисованный пряник я пока есть не хочу. Если в будущем появятся данные и факты, которые постепенно смогут подтвердить эту историю, тогда можно будет и поесть.