Автор: Changan I Biteye, команда контента

Знаете, почему вы не можете обыграть лидеров на Polymarket? Потому что они внимательно изучают правила, словно юристы, разбирающие контракты.

В апреле 2026 года на Polymarket разгорелся спор вокруг лидера Венесуэлы, который взбудоражил сообщество.

На Polymarket был рынок с вопросом: «Кто будет лидером Венесуэлы к концу 2026 года?» Многие трейдеры, руководствуясь интуицией, считали: Мадуро в американской тюрьме, Дельси возглавляет кабинет в Каракасе, фактически у власти находится Дельси, поэтому они ставили на Дельси.

Но правила и дополнительные пояснения были четко прописаны: «официально занимает» относится к официально назначенному, приведенному к присяге лицу. Признанное ООН правительство Венесуэлы не официально отстранило или заменило Мадуро, официальная правительственная информация по-прежнему считает его президентом. В правилах также специально добавлено: «Временное授权 на осуществление президентских полномочий не равно передаче президентского поста.»

Согласно этим правилам, даже если Мадуро остается в американской тюрьме, он по-прежнему является законным президентом Венесуэлы.

Подобных примеров много:

-

После выпуска стейблкоина Polymarket возник спор на рынке «Какая FDV у токена Polymarket?»: считается ли стейблкоин токеном, разница в одном слове

-

Уран Ирана: критерий «согласия», условное заявление против официального подписания соглашения

За этими случаями стоит одна и та же логика: в Polymarket правила являются核心 (ядром). Но когда возникают споры о правилах, у Polymarket есть完整的 процесс арбитража для их разрешения: в этой статье рассказывается, как работает этот механизм, и в чем его сходство с традиционным судом и где существуют фундаментальные различия.

一、Механизм арбитража Polymarket

Неоднозначность текста правил не только создает разногласия в ценообразовании, но и превращается в正式ный (официальный) спор при расчетах.

На Polymarket ежедневно рассчитывается большое количество рынков, особенно те, которые связаны с политическими заявлениями, дипломатическими позициями и военными действиями,容易引发争议 (легко вызывают споры).

Спорные события на самом деле являются нормой для预测рынков (prediction markets). Неоднозначность создает разногласия в ценообразовании на этапе торговли и превращается в конфликт на этапе расчетов — это одна и та же проблема, проявляющаяся в разные моменты времени.

Для разрешения этих споров Polymarket создал完整的 (полный) процесс арбитража. Процесс расчетов разделен на два пути: обычные расчеты и арбитраж споров.

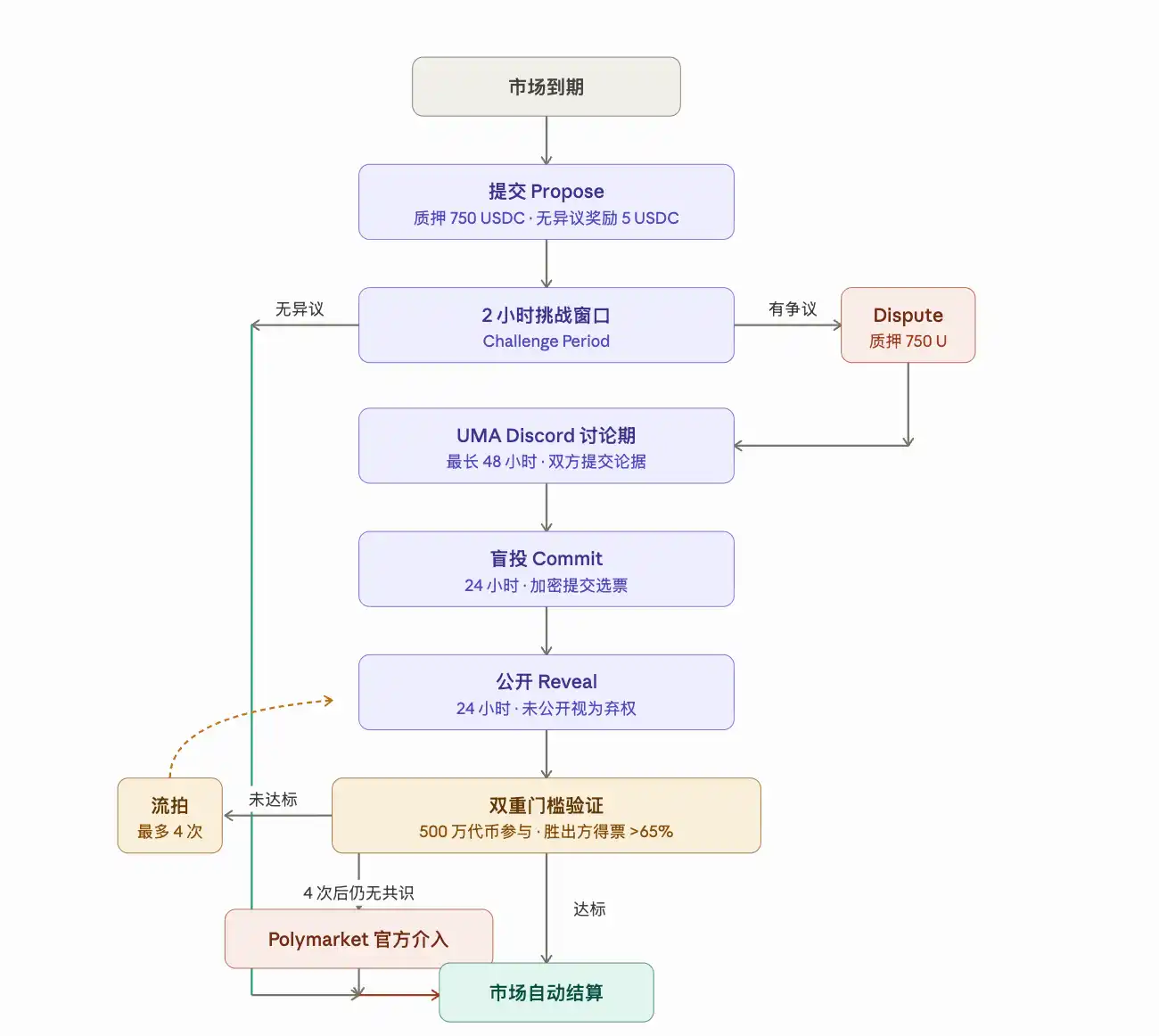

Первый шаг: Подача предложения (Propose)

Когда рынок满足条件 расчета (удовлетворяет условиям расчета), любой может подать результат арбитража, заявив, что рынок должен быть признан YES или NO. При подаче предложения необходимо внести залог в размере 750 USDC в качестве гарантии. Этот залог является обеспечением собственного суждения подающей стороны. Когда возражений по рынку нет, пользователь, подавший предложение, получает вознаграждение в 5 USDC.

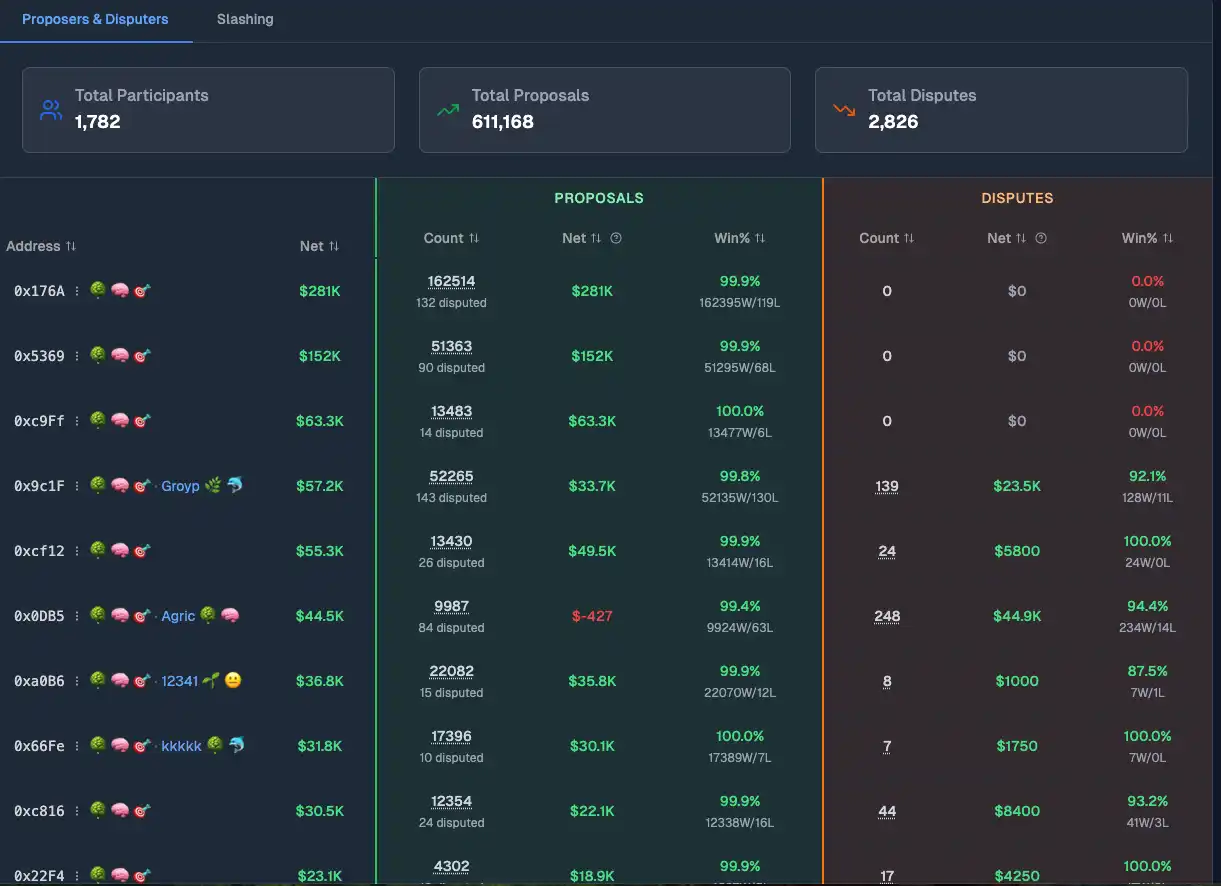

В настоящее время только 1782 пользователя подавали предложения (Propose) на рынках, а самый прибыльный пользователь уже заработал в общей сложности $281K.

Второй шаг: 2-часовое окно для оспаривания (Dispute)

После подачи предложения начинается 2-часовой период оспаривания. Это первая точка ветвления во всем процессе.

Если в течение 2 часов никто не высказывает возражений, система по умолчанию считает предложение правильным, рынок рассчитывается напрямую, процесс завершается. Большинство рынков идут по этому пути.

Если кто-то считает результат предложения ошибочным, он может оспорить его в течение этих 2 часов, также внеся залог в 750 USDC. В случае успешного оспаривания можно заработать奖金 (приз) в 250 USDC.

На рынке мало пользователей, специализирующихся specifically на Dispute. Пользователь, заработавший больше всех на этапе Dispute, это 0xB7A, с прибылью в $17123.

Третий шаг: Максимум 48 часов на обсуждение

После входа в轨道 спора (режим спора) стороны переходят на этап обсуждения в UMA Discord. Цель этого этапа — представить аргументы и доказательства: интерпретацию текста правил, соответствующие новостные сообщения, исторические прецеденты, официальные заявления — любые материалы, которые могут поддержать их позицию, могут быть представлены на этом этапе.

Период обсуждения длится максимум 48 часов и является единственным этапом в процессе, где можно полноценно изложить理由 (причины). Качество этого этапа во многом определяет направление последующего голосования.

Четвертый шаг: 48-часовое голосование

После обсуждения начинается этап голосования держателей токенов UMA. Голосование разделено на два этапа по 24 часа каждый.

-

Первый этап — слепое голосование. Это заставляет каждого голосующего принимать независимое решение на основе своего понимания правил, а не следовать за крупными игроками.

-

Второй этап — открытый. Те, кто не раскрыл свой голос на этом этапе, считаются воздержавшимися, и их голоса аннулируются.

После голосования UMA устанавливает два порога для расчета, которые должны быть выполнены одновременно для завершения арбитража:

-

По уровню участия: необходимо至少 (как минимум) 5 миллионов токенов для участия в голосовании, чтобы обеспечить достаточную представительность арбитража.

-

По абсолютному консенсусу: победившая сторона должна набрать более 65% голосов, а не простое большинство в 51%.

Если оба порога не выполнены одновременно, голосование проваливается (срывается), и переходит на следующий раунд переголосования, максимум до 4 раз. Если после 4 раундов консенсус не достигнут, Polymarket имеет право напрямую вмешаться в арбитраж.

Пятый шаг: Автоматический расчет

После подтверждения результатов голосования рынок рассчитывается автоматически, средства распределяются согласно результату. Апелляций, пересмотров, возможностей для исправления нет.

Весь процесс спора, от подачи оспаривания до окончательного расчета, обычно занимает不到 недели.

二、Polymarket и традиционный суд: одна логика, разный дизайн

На поверхности процесс арбитража Polymarket и традиционный суд高度相似 (очень похожи): есть сторона, выдвигающая требование, есть сторона, оспаривающая требование, есть этап обсуждения и изложения, и в конце есть арбитр, выносящий результат.

Но эти две системы коренным образом отличаются в одном фундаментальном аспекте设计 (дизайна): разделение властей.

-

Власть в суде изолирована

В традиционном суде истец и ответчик имеют только право на изложение, но не на решение. Судья имеет только право на решение, но не имеет利益立场 (заинтересованной позиции). Что более важно, судья и дело должны быть независимы друг от друга. Как только судья имеет какую-либо заинтересованность в деле, он обязан устраниться, и дело передается другому судье.

Арбитр и заинтересованная сторона — никогда не одно и то же лицо.

-

В Polymarket нет этой изоляции

Держатели токенов UMA являются арбитрами, но они同时 (одновременно) могут полностью иметь позиции (позиции) на спорном рынке. То, в какую сторону будет вынесено решение, напрямую влияет на их прибыли и убытки. То, что судья и заинтересованная сторона — одно и то же лицо, в традиционном суде называется конфликтом интересов и ведет к обязательному отводу, в Polymarket это законно и нормально.

Этот设计缺陷 (конструктивный недостаток) является根源ом следующих двух проблем.

1️⃣ Почему этап обсуждения терпит неудачу

В суде позиции истца и ответчика фиксированы с момента подачи иска. Адвокаты не меняют позицию в середине судебного заседания и не отзывают свои заявления из-за сильного давления противоположной стороны. Позиции четкие, роли ясны, все дебаты построены на этой стабильности.

Обсуждение в UMA Discord сталкивается с двумя проблемами одновременно.

-

Эффект толпы: обсуждение проходит открыто и под реальными именами. Как только влиятельный KOL высказывает свое мнение, последующие很容易变成跟风 (легко превращаются в подражание). Многие участники пишут только «P1» или «P2», не приводя никаких理由 (причин).

-

Смена позиции: участники обсуждения одновременно имеют позиции на спорном рынке. Когда позиция меняется, мнение естественным образом меняется вместе с ней. Именно поэтому в UMA Discord часто можно увидеть, как высказавшие мнение затем удаляют его.

Корень обеих проблем один и тот же: арбитр и заинтересованная сторона не разделены. Суд с помощью системы обязательного отвода разделяет эти две роли, гарантируя стабильность позиций в процессе обсуждения. В Polymarket этого разделения нет.

2️⃣ Почему результаты арбитража не прозрачны

В суде судья, заслушав полные заявления обеих сторон, выносит решение. В решении указывается, какие аргументы были приняты, на чем основано решение и почему было принято такое решение. Проигравшая сторона может быть недовольна, но по крайней мере знает, где проиграла, и в следующий раз может целенаправленно усилить свои аргументы.

Эти решения суда формируют систему прецедентов, которую можно изучать. Последующие судьи, адвокаты и стороны могут на них ссылаться, благодаря чему стандарты судебных решений становятся проверяемыми, изучаемыми и предсказуемыми.

После голосования UMA есть только один исход: YES или NO. Участвующие в обсуждении стороны не знают, что видели голосующие, во что поверили, почему склонились в ту или иную сторону. Выигравшие не знают, какой аргумент сработал, проигравшие не знают, где им не хватило убедительности. Именно потому, что логика судей никогда не раскрывается, результаты споров难以被学习和积累 (с трудом поддаются изучению и накоплению).

Судебные решения формируют систему прецедентов, а арбитраж Polymarket оставляет после себя только результат.

三、В заключение

Таким образом, Polymarket никогда не был просто рынком «угадывания событий». Это больше похоже на систему, которая переводит реальные события в юридические тексты, а затем переводит юридические тексты в результаты расчетов.

Понимание правил так же важно, как и проведение исследований. Преимущество лидеров часто проистекает из глубины понимания правил, знания того, что承认 (признает) эта система, что будет принято в арбитраже.

Тот, кто раньше осознает, что между «реальностью» и «правилами» существует щель, имеет больше шансов заработать на той части ценового отклонения, которая создается неверным толкованием, спорами и эмоциями.